Asia-Pacific Cooling Water Treatment Chemicals Market: Growth Analysis, Value Projections, and Industry Forecast

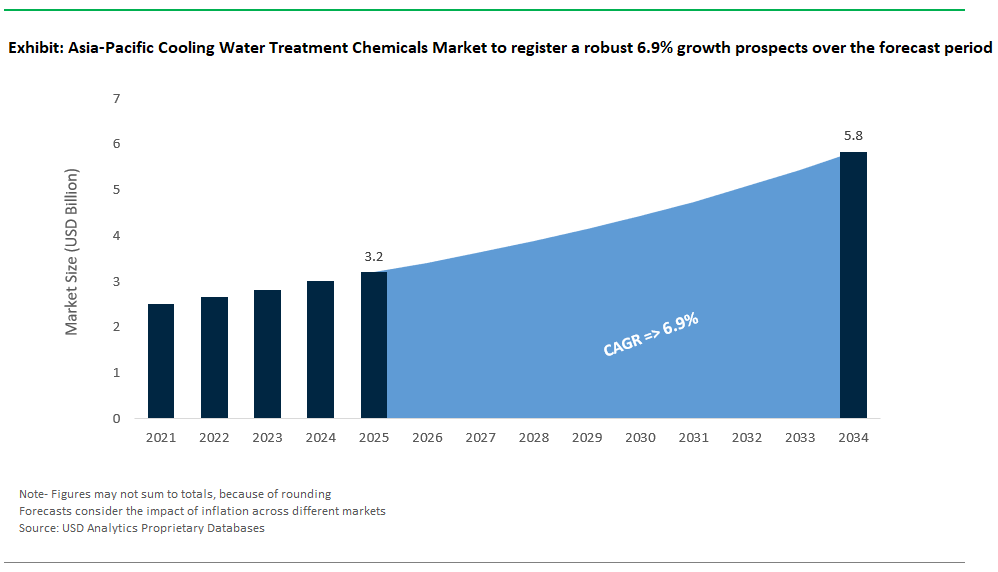

Asia-Pacific Cooling Water Treatment Chemicals Market Size is estimated at $3.2 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 6.9% to reach $5.8 Billion by 2034.

The cooling water treatment chemicals market in Asia-Pacific is evolving rapidly under the combined influence of regional climate extremes and increasingly stringent environmental regulations. Industrial facilities across countries like China, India, Japan, and Southeast Asia are contending with high ambient temperatures, elevated UV radiation, and feedwater with variable compositions, including high levels of silica and salinity. These factors create significant challenges for scale and corrosion control, which remain the foundational goals of cooling water treatment programs. Phosphonate-based inhibitors continue to be the industry standard for scale prevention, typically dosed between 8 to 20 ppm to maintain acceptable scaling indices and minimize corrosion rates often targeting thresholds below 0.1 mm per year in line with internal facility standards or national guidelines. However, site-specific conditions such as elevated silica levels in parts of India have prompted the increased use of polymer-silicate blends, which provide greater tolerance for silica levels while maintaining system efficiency. Likewise, environmental constraints in countries such as Japan, where zinc discharge into water bodies is tightly regulated, have encouraged a transition toward zinc-free carboxylate polymers that offer comparable corrosion inhibition without the regulatory drawbacks.

Biological control in cooling water systems also demands region-specific strategies, especially in tropical areas like Southeast Asia where year-round humidity exceeds 80%, creating ideal conditions for microbial growth. Oxidizing biocides, such as chlorine dioxide and brominated compounds like BCDMH, are commonly applied to suppress bacterial proliferation and biofilm formation. In some industrial applications, non-oxidizing biocides such as glutaraldehyde or THPS are added periodically to enhance control against biofilms and algae. These strategies are particularly important in sectors like power generation, where microbiological fouling can impact thermal efficiency and increase maintenance costs. Meanwhile, environmental and regulatory pressures especially in countries with evolving chemical safety frameworks like South Korea’s K-REACH have accelerated the adoption of green chemistry solutions. Natural dispersants based on tannins and enzymatic biofilm removers are being tested and deployed in facilities across Vietnam, South Korea, and Japan. Many of these formulations comply with OECD biodegradability standards and offer performance levels comparable to traditional chemistries, including greater than 80% dispersion of calcium sulfate scales and significant reductions in biofilm thickness within 48 hours of application.

Digitally enabled dosing and water treatment monitoring is emerging as a critical enabler of efficiency and sustainability across Asia-Pacific’s industrial water landscape. Countries like India, under initiatives such as the Smart Cities Mission, are increasingly adopting IoT-based platforms that integrate sensors measuring pH, ORP, conductivity, and residual biocide levels with automated dosing systems. These systems offer the advantage of real-time chemical adjustment and can reduce biocide consumption by 15% to 30% depending on site complexity and microbial load. Moreover, data from these systems is helping operators maintain microbial counts below critical thresholds (often <10⁴ CFU/mL), while avoiding chemical overdosing and complying with local water quality regulations. This convergence of automation and analytics is helping plants optimize chemical use, extend asset life, and minimize environmental footprint all of which are vital in regions facing water scarcity and energy efficiency mandates.

Water conservation is also becoming an integral goal in cooling system operations. Through optimized chemical treatment and tighter process control, many plants have successfully increased their cycles of concentration from traditional 3–5× to as high as 8–12×. This improvement translates directly to reduced freshwater withdrawal sometimes by as much as 30% according to regional reports including those from the Asian Development Bank. At the same time, pressure is growing on chemical suppliers to provide solutions with lower embodied carbon. Life-cycle assessments show that commonly used water treatment chemicals carry a carbon intensity ranging from 0.8 to 1.2 kg CO₂ per kilogram of product manufactured. As a result, end users across the region are showing greater preference for suppliers that can demonstrate low-emission production processes and provide documentation aligned with corporate sustainability metrics. In this context, chemical providers who offer integrated programs combining advanced formulations, digital monitoring, and sustainability support are becoming essential strategic partners for water-intensive industries navigating Asia-Pacific’s evolving regulatory and environmental landscape.

Market Trend: Industrial Growth and Water Scarcity Driving Sustainable Cooling Water Treatments

The Asia‑Pacific cooling water treatment chemicals market is rapidly evolving under the combined pressures of accelerating industrial development and increasing water scarcity, especially in countries like China, India, Vietnam, and Southeast Asia. As these economies accounting for more than two‑thirds of regional demand move away from traditional formulations containing phosphates, chromates, and heavy metals, they are adopting more sustainable alternatives such as biodegradable polymers, molybdate‑free corrosion inhibitors, and automated dosing systems. This shift is driven not only by the need to meet stricter discharge standards but also by growing resource efficiency mandates.

In China, legislation such as the Yangtze River Protection Law is prompting industrial facilities to improve water quality and reduce chemical pollution. In India, extended efforts under Zero Liquid Discharge (ZLD) policies are pushing thermal power, steel, and chemical plants toward recirculating cooling systems and low-bleed chemical programs. With nearly half of thermal power plants in Southeast Asia facing high water stress, the push toward closed-loop systems paired with advanced scale and corrosion control agents is strengthening.

While precise data on water savings varies, case studies show that automated monitoring and treatment systems can reduce water use by 20–40% and help maintain stringent effluent guidelines. In Vietnam, regulatory frameworks are increasingly incorporating financial penalties to enforce compliance with cooling water disposal rules. As a result, water chemistry in the Asia‑Pacific region is transitioning from a purely operational concern to a critical component of corporate compliance and sustainability strategies.

Market Opportunity: Data Center Expansion Fueling Specialized Cooling Chemistry Demand

The surge in hyperscale data centers across Asia‑Pacific driven by the growth of cloud computing, AI, and edge infrastructure has opened up a growing market for specialized cooling water treatment chemicals. Data center cooling systems require ultra‑clean, non‑fouling chemistries that are compatible with high-conductivity environments and sensitive materials like aluminum heat exchangers. They also demand microbial control solutions that avoid harsh oxidizers, especially when using direct-to-chip or immersion cooling technologies in countries like Singapore, Japan, India, and Australia.

Singapore’s latest green data center guidelines, introduced in 2024, require enhanced water efficiency and microbial safety in new cooling installations. Similarly, Japan’s upcoming revisions to industrial water reuse regulations are prompting data center operators to source treatment solutions capable of supporting higher water recirculation without compromising equipment integrity.

In response, suppliers are developing digital water treatment packages that combine sensor‑based monitoring, cloud analytics, and tailored chemical blending often delivered under a chemical‑as‑a‑service model. By enabling real‑time control of parameters like pH, conductivity, and microbial activity, these systems support improved water reuse, reduce fresh water withdrawals, and help data centers meet strict sustainability requirements. As datacenter operators emphasize low‑fouling, maintainability, and system resilience, vendors offering smart, compliance‑driven chemical solutions are well‑positioned to secure long‑term, high‑margin partnerships.

Competitive Landscape: Asia-Pacific cooling Water Treatment Chemicals Market

The Asia-Pacific cooling water treatment chemicals market is shaped by chemical innovation, digital automation, and specific service models. Companies that can deliver integrated cooling water programs lead the market. These programs address corrosion and scale control, microbial risk, and adapt to various water qualities, regulations, and climate challenges in countries like India, China, Japan, and Australia. Ecolab (Nalco Water) and Kurita Water Industries are among the leaders. They combine effective chemistries with real-time monitoring systems and strong local technical support.

Ecolab, through its Nalco Water division, sets the standard for digital water treatment in industrial segments like power generation, steel, and food and beverage across APAC. Its 3D TRASAR™ technology platform is a key advantage. It uses smart sensors, automation, and cloud analytics to manage scaling, corrosion, and biofouling with little operator intervention. In countries with varying water quality, like Vietnam and Indonesia, Ecolab’s data-driven programs optimize chemical use and maintain operations. The company’s cooling water offerings include phosphonate-based corrosion inhibitors, non-oxidizing biocides, and polymeric dispersants, often provided through service contracts that promote sustainability and meet regulatory requirements.

Kurita Water Industries, based in Tokyo, is a major player with strong engineering and formulation skills tailored to Asian industrial water systems. The company uses its S.sensing® CS platform to automate chemical dosing based on scaling and microbial load changes, especially in fast-growing markets like Thailand and India. Kurita’s unique method combines proprietary polymers, chelating agents, and multifunctional biocides with localized R&D. This allows them to adapt treatments for tropical climates, high recirculation loads, and difficult effluents. Their growth strategy focuses on eco-friendly chemistries under the “Kurita Dropwise” brand, aiming to reduce water and energy use while meeting stricter discharge rules in Southeast Asia.

Other global companies like Solenis and Veolia Water Technologies also play competitive roles by emphasizing system efficiency and chemical sustainability. Solenis provides high-performance dispersants and threshold inhibitors designed for pulp and paper cooling systems in China and Indonesia. Veolia, through its Hydrex™ brand, combines customized biocides and scale inhibitors with its broader water technology solutions, including cooling tower upgrades and hybrid cooling loop designs. These offerings help Veolia seize opportunities in high water-stress areas like Western Australia, where demand for water reuse-compatible cooling programs is increasing rapidly.

The regional market is also influenced by membrane-friendly antiscalants and microbiological control chemicals that fit hybrid and closed-loop cooling systems. Specialty suppliers like Avista Technologies are gaining popularity with their compatible formulations that reduce membrane fouling in RO-pretreated systems. Regional formulators in India and Malaysia are also providing customized cooling water blends to meet cost-performance needs in tier-2 industrial districts. Meanwhile, raw material suppliers like BASF and SNF continue to provide the basic polymers and coagulants used in many local formulations, though they usually work through local distributors instead of direct engagement with end users.

Competitive advantage in Asia-Pacific increasingly relies on combining formulation science with responsive digital tools. Industrial facilities are looking for higher concentration cycles, reduced blowdown, and lower biological fouling while maintaining asset integrity. Companies that blend proprietary chemistry with on-site analytics, prompt field support, and modular dosing systems are best positioned to thrive in this diverse and highly localized market.

Asia-Pacific Cooling Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Cooling System Type: Open Recirculating Systems Dominate While Chillers & Heat Exchangers Grow Fastest

Open recirculating cooling systems hold the largest share in the Asia-Pacific cooling water treatment chemicals market, accounting for approximately 42.9% in 2025. Their dominance is driven by widespread deployment in power plants, refineries, and chemical manufacturing facilities, where continuous water reuse is essential to reduce consumption and manage thermal loads. These systems require consistent chemical treatment including corrosion inhibitors, antiscalants, and biocides to maintain performance and prevent scaling and biofouling under high heat and contamination conditions. In contrast, chillers and heat exchangers represent the fastest-growing system type, projected to expand at a 7.4% CAGR through 2034. Rapid industrial automation, cleanroom growth, and climate-controlled logistics in countries like China, India, and Vietnam are fueling demand for efficient and compact thermal management systems that require high-purity water treatment regimens. Evaporative condensers also show strong growth as they gain favor in commercial HVAC and light industrial setups. Closed-loop cooling systems maintain steady adoption, particularly in electronics and data center infrastructure, while once-through cooling systems continue to decline due to water use restrictions and thermal discharge regulations across water-stressed Asia-Pacific regions.

.png)

By End-User Industry: Power Generation Leads While Manufacturing Sector Grows Fastest

Power generation remains the leading end-user industry for cooling water treatment chemicals in Asia-Pacific, capturing approximately 38.1% of market share in 2025. The dominance of coal-fired thermal plants especially in India, Indonesia, and Southeast Asia drives massive cooling water demand, with open-loop and recirculating systems requiring aggressive scale, corrosion, and microbial control programs. Despite renewable energy growth, thermal generation remains central to grid stability in many emerging markets, sustaining chemical consumption for cooling operations. Meanwhile, the manufacturing sector is emerging as the fastest-growing end-user, projected to grow at a 7.9% CAGR through 2034. The expansion of semiconductor fabrication, electric vehicle (EV) battery plants, and advanced electronics production across China, South Korea, and India is driving the adoption of precision cooling systems that demand high-performance chemical treatment. The chemical and petrochemical industry continues to show strong demand due to its reliance on high-load process cooling. The commercial segment, including commercial real estate, malls, and high-rise buildings in megacities such as Bangkok, Manila, and Jakarta, is adopting HVAC cooling water treatment chemicals, albeit at a slower growth rate. Other industrial sectors like food processing and textiles maintain a consistent but modest share of the market.

Asia-Pacific Cooling Water Treatment Chemicals Market Report Scope

Asia-Pacific Cooling Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.2 Billion

|

|

Market Size (2034)

|

$5.8 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Type of Chemical (Corrosion Inhibitors, Scale Inhibitors, Biocides and Disinfectants, Dispersants, pH Adjusters/Control Chemicals, Defoamers and Antifoaming Agents, Pre-treatment Chemicals), By Cooling System Type (Open Recirculating Cooling Systems, Closed Cooling Systems, Once-Through Cooling Systems, Evaporative Condensers, Chillers and Heat Exchangers), By End-User Industry (Power Generation, Chemical and Petrochemical, Manufacturing, Commercial, Other Industrial Sectors), By Form of Chemical (Liquid, Powder/Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Kurita Water Industries Ltd. (Japan), Solenis LLC (U.S.), Kemira Oyj (Finland), Veolia Water Technologies (France), BASF SE (Germany), Ion Exchange (India) Ltd. (India), Thermax Limited (India), NCH Asia Pacific (U.S.), The Dow Chemical Company (U.S.),

|

|

Countries

|

China, India, Japan, South Korea, Australia, South East Asia

|

Asia-Pacific Cooling Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Corrosion Inhibitors

- Phosphonates

- Molybdates

- Nitrites

- Azoles

- Zinc compounds

- Proprietary blends

- Scale Inhibitors

- Polyacrylates

- Phosphonates

- Copolymers

- Specialty silica inhibitors

- Biocides and Disinfectants

- Oxidizing Biocides

- Non-Oxidizing Biocides

- Dispersants

- pH Adjusters/Control Chemicals

- Defoamers and Antifoaming Agents

- Pre-treatment Chemicals

By Cooling System Type

- Open Recirculating Cooling Systems

- Closed Cooling Systems

- Once-Through Cooling Systems

- Evaporative Condensers

- Chillers and Heat Exchangers

By End-User Industry

- Power Generation

- Chemical and Petrochemical

- Manufacturing

- Steel, Mining and Metallurgy

- Automotive

- Textile

- Pulp and Paper

- Food and Beverage

- Pharmaceutical

- Electronics and Semiconductors

- Other Industrial Manufacturing

- Commercial

- Other Industrial Sectors

By Form of Chemical

By Country

- China

- India

- Japan

- South Korea

- Australia

- South East Asia

- Rest of Asia

Top Companies in Asia-Pacific Cooling Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Kurita Water Industries Ltd. (Japan)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- Veolia Water Technologies (France)

- BASF SE (Germany)

- Ion Exchange (India) Ltd. (India)

- Thermax Limited (India)

- NCH Asia Pacific (U.S.)

- The Dow Chemical Company (U.S.)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the Asia-Pacific Cooling Water Treatment Chemicals Market, delivering a comprehensive analysis of market size, growth dynamics, and innovation trends shaping the regional cooling water treatment sector. It highlights breakthroughs in sustainable chemical formulations, IoT-enabled dosing systems, and green alternatives for scale, corrosion, and microbial control. The analysis reviews the role of advanced chemistries, digital automation, and compliance strategies in driving market performance across power generation, manufacturing, and commercial applications. This report is an essential resource for stakeholders seeking actionable insights on industrial water management and evolving environmental regulations across Asia-Pacific.

Scope Includes:

- Segmentation

- By Type of Chemical: Corrosion Inhibitors, Biocides & Disinfectants, Dispersants, pH Adjusters/Control Chemicals, Defoamers, Pre-treatment Chemicals

- By Cooling System Type: Open Recirculating Systems, Closed Cooling Systems, Once-Through Cooling Systems, Evaporative Condensers, Chillers & Heat Exchangers

- By End-User Industry: Power Generation, Chemical & Petrochemical, Manufacturing (Steel, Automotive, Textile, Electronics, etc.), Commercial, Other Industrial Sectors

- By Form of Chemical: Liquid, Powder/Solid

- Geographic Scope: Analysis of China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Companies Covered: Ecolab Inc., Kurita Water Industries Ltd., Solenis LLC, Kemira Oyj, Veolia Water Technologies, BASF SE, Ion Exchange (India) Ltd., Thermax Limited, NCH Asia Pacific, The Dow Chemical Company

Methodology

This report applies a hybrid research methodology integrating primary research through interviews with regional water treatment experts and plant operators, and secondary research using verified sources such as industry white papers, regulatory databases, and technical publications. Market estimates utilize bottom-up and top-down approaches, supported by data triangulation for accuracy. Predictive modeling and adoption trend analysis ensure reliable projections for each segment. Validation through expert reviews and real-world case studies enhances credibility, making this analysis a robust tool for strategic decision-making.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements