Asia-Pacific pH Adjusters and Softeners for Water Treatment Market Value Analysis and Forecast to 2034

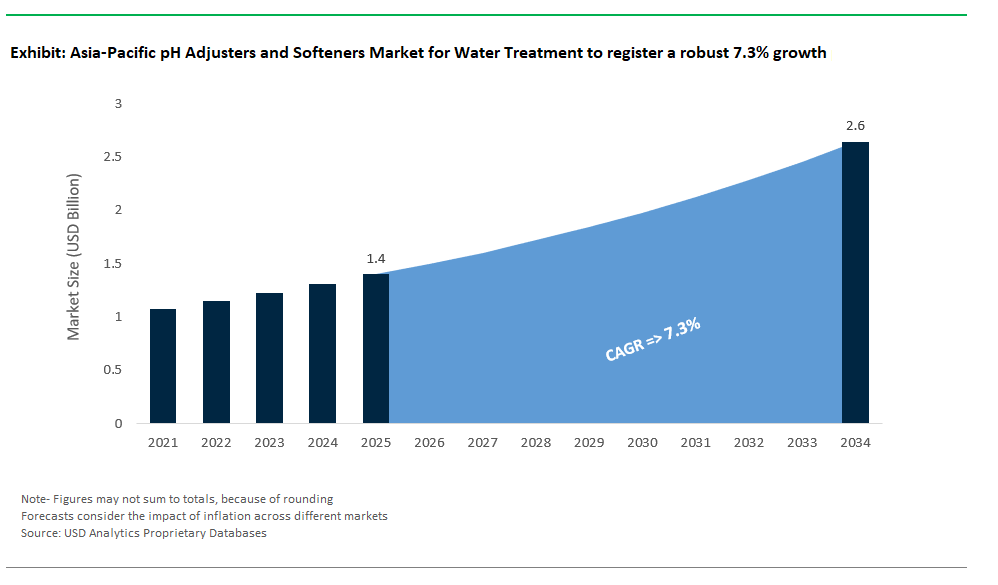

Asia-Pacific pH Adjusters and Softeners Market for Water Treatment Size is estimated at $1.4 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 7.3% to reach $2.6 Billion by 2034.

The Asia-Pacific pH adjusters and softeners market serves as a foundational pillar for both conventional and high-purity water treatment infrastructure, responding to the region’s highly variable raw water conditions, regulatory nuances, and sector-specific treatment tolerances.

pH adjustment remains a critical pre-treatment and conditioning step across food & beverage, semiconductor, and municipal sectors, where fine control of alkalinity, corrosivity, and chemical compatibility dictates downstream system performance. Sulfuric acid (H₂SO₄), a staple acidulant, is widely dosed at 0.5–8 mL/m³ to bring pH into the 6.5–7.5 range and lower alkalinity by 50–100 mg/L as CaCO₃. Yet, its adoption is governed by strict containment protocols, particularly in China, where concentrations >75% demand specialized FRP storage tanks under GB 13690, emphasizing the need for appropriate handling of hazardous substances like concentrated sulfuric acid.

In response, carbon dioxide injection is gaining ground in food and beverage facilities across Singapore, Malaysia, and Australia due to its non-corrosive nature, lack of chemical storage risk, and ability to fine-tune pH (6.8–7.2) without elevating TDS levels.

On the alkaline front, lime slurry (Ca(OH)₂) offers compelling cost advantages typically $0.05–0.15/m³ in markets like Indonesia, though it contributes to turbidity loading (5–15 NTU per 10 mg/L dose), necessitating post-dosing clarification per national water treatment guidelines. Sodium hydroxide (NaOH), while more expensive ($0.20–0.40/m³), is favored for applications demanding precision, such as semiconductor fabrication and ultrapure water systems, where automated control ensures ±0.1 pH unit accuracy.

In parallel, softening solutions both ion exchange and chemical precipitation are scaling to meet rising industrial and urban demand. Strong acid cation (SAC) resins remain dominant, offering exchange capacities of 1.8–2.2 eq/L with optimized NaCl regeneration protocols (80–150 g/L), as per Chinese national standards for ion exchange specify macroporous strongly acidic styrene type cation exchange resins. In Japan, post-treatment hardness leakage is routinely maintained below 1.5 mg/L CaCO₃ in line with stringent water quality requirements for industrial and municipal use, supporting applications in district cooling, beverage bottling, and electronics. However, coastal and high-TDS source waters, such as those found in Thailand, necessitate dual-barrier designs typically SAC resin followed by RO membranes to consistently achieve <1 mg/L residual hardness.

Meanwhile, the lime-soda process persists in mid-scale municipal deployments across Vietnam and the Philippines, with dosing schemes (100–200 mg/L Ca(OH)₂ + 50–100 mg/L Na₂CO₃) delivering final hardness in the 40–80 mg/L range, as outlined in Vietnamese national technical regulations on drinking water quality. Yet, the process generates significant sludge volumes (0.6–1.2 kg dry solids/m³), which are under greater scrutiny from environmental agencies like the DENR.

Across both categories, regulatory and economic forces are converging to drive demand for dosing automation, chemical lifecycle optimization, and hybrid treatment trains. Vendors offering compatibility with IoT-based pH and conductivity monitoring, low-waste regeneration chemistries, and regional safety certifications are better positioned to meet the operational and sustainability benchmarks emerging across Asia-Pacific’s fast-evolving water infrastructure landscape.

Competitive Landscape: Asia-Pacific pH Adjusters and Softeners Market for Water Treatment

The Asia-Pacific pH adjusters and softeners market for water treatment involves a blend of chemical formulation knowledge, customized applications, and the use of digital monitoring and treatment systems. Market leadership belongs to those companies that can provide complete solutions for various raw water profiles, industrial discharge standards, and management challenges related to hardness and pH levels, which vary significantly in countries like India, China, Japan, and Southeast Asia.

Multinational firms like Ecolab and Kurita Water Industries lead the market by offering fully integrated programs. These programs combine acid and base pH control chemicals, ion exchange-based softening systems, and unique digital platforms. Ecolab’s offerings include mineral acids and alkalis for pH correction, ion exchange resins, and antiscalants, all packaged with its 3D TRASAR™ system, which allows for real-time monitoring and control of important parameters. These bundled solutions are commonly used in industrial and municipal facilities throughout the region, helping to optimize chemical use and meet stricter discharge standards.

Kurita has a strong presence in Japan and is expanding in Southeast Asia, India, and China. This growth enhances its competitive advantage, thanks to a wide range of products designed for regional water chemistries. The company offers various pH adjustment chemicals, from sulfuric acid to CO₂-based buffers, and advanced softening solutions such as specialty resins and membrane-compatible antiscalants. Kurita’s commitment to designing localized programs and understanding regional water infrastructure challenges makes it a preferred partner for complex industrial clients, especially in manufacturing areas facing varying feedwater hardness and pH changes.

The market also features other formulation-driven competitors like Solenis, Kemira, and Veolia Water Technologies. These companies focus on specialty polymers and chemical softening aids for high-scaling environments. Solenis has established a niche with advanced phosphonate- and polymer-based softening technologies, particularly in cooling and process water systems used by the paper, refining, and chemical sectors. Kemira adds to the mix with its strong presence in coagulation and flocculation technologies. These technologies indirectly improve softening efficiency by minimizing particulate fouling and helping with pretreatment in systems experiencing high hardness.

Veolia Water Technologies addresses the market through systems integration. It combines chemical pH correction, such as caustic and acid dosing, with engineered ion exchange softening and membrane preconditioning solutions under the Hydrex™ brand. Veolia's strength lies in its ability to connect chemicals with physical systems and long-term service agreements, especially in large municipal and industrial setups that require reliability over time and control of multiple contaminants.

Indian companies like Ion Exchange and Thermax significantly boost regional competitiveness with their focus on ion exchange resin technology and complete softening plant solutions. Ion Exchange leads domestic demand with its vertically integrated range of resins, chemical dosing solutions, and pH adjustment agents. Thermax also provides pH adjusters and softening chemicals but stands out in designing and supplying water treatment equipment, such as softening skids and dosing systems, which are increasingly adopted in rapidly industrializing areas of India and Southeast Asia.

Raw material suppliers like BASF, Dow, and Nouryon play a key role in this market by supplying the acids, alkalis, phosphonates, polymers, and monomers that base pH adjustment and softening formulations. BASF and Dow also provide ion exchange resins, such as DOWEX™, and other key components integrated into softening systems by manufacturers and original equipment manufacturers. Nouryon’s global supply of caustic soda, sulfuric acid, ethylene amines, and branded chelants like Dissolvine® is crucial for mixing operations in Asia, particularly in high-demand industrial regions for base chemicals and performance additives.

Competitive dynamics are increasingly influenced by regional regulatory challenges, variations in water quality, and the need for customized treatment systems that combine chemical and mechanical softening approaches. Companies that can adjust pH correction and softening programs to local water chemistries, provide quick technical support, and incorporate monitoring technologies will be better prepared to grow. As industries such as power, oil and gas, chemicals, and food and beverage seek higher water reuse and stricter effluent controls, the market favors those players that offer deep formulation knowledge, equipment expertise, and real-time process insight.

Asia-Pacific pH Adjusters and Softeners Market for Water Treatment – Segmentation Insights (2025–2034)

By Type of Chemical: Acidic pH Adjusters Lead While Water Softeners Grow Fastest

Acidic pH adjusters dominate the Asia-Pacific pH adjusters and softeners market, accounting for approximately 44.2% of the total share in 2025. This segment’s dominance is driven by the widespread use of sulfuric acid (H₂SO₄) and hydrochloric acid (HCl) across industrial and municipal water treatment systems to reduce alkalinity and maintain optimal pH balance, particularly in cooling and boiler water circuits. These acidic agents are essential for preventing scaling, improving the efficacy of coagulants, and protecting metallic infrastructure from corrosion. In contrast, water softeners including sodium-based ion exchange resins and lime-soda ash formulations represent the fastest-growing category, projected to expand at a 8.9% CAGR through 2034. Growth in this segment is propelled by rising demand in regions facing severe hard water issues, especially across India, Indonesia, and the Philippines, where high calcium and magnesium concentrations impair equipment performance and increase maintenance costs. Alkaline pH adjusters such as caustic soda and lime continue to play a pivotal role in neutralizing acidic industrial effluents, ensuring compliance with discharge regulations and protecting downstream biological systems.

.png)

By Application: Raw Water Treatment Leads While Desalination Grows Fastest

Raw water treatment remains the largest application for pH adjusters and softeners in Asia-Pacific, accounting for approximately 29.4% of the market in 2025. This is largely due to the high turbidity and variable alkalinity of surface water sources like rivers and lakes across the region, especially in rapidly urbanizing areas. pH balancing and hardness removal are essential pretreatment steps for municipal utilities and industries drawing from such sources, ensuring compatibility with filtration, membrane, and chemical treatment processes. Meanwhile, desalination is the fastest-growing application segment, forecast to grow at a 9.1% CAGR through 2034. With major seawater reverse osmosis (SWRO) and brackish water desalination projects underway in China, South Korea, and coastal India, there is increasing demand for precise pH control and scaling prevention in high-pressure membrane systems. Process water treatment also shows strong momentum particularly in electronics, pharmaceutical, and food industries where ultrapure water requirements are fueling the use of high-precision pH correction and hardness stabilization. Boiler and cooling water treatments continue to account for a substantial share, especially in power and heavy industries, while wastewater treatment applications are expanding as industries aim to improve effluent quality and meet increasingly strict discharge norms.

Asia-Pacific pH Adjusters and Softeners Market for Water Treatment Report Scope

Asia-Pacific pH Adjusters and Softeners Market for Water Treatment

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$2.6 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Type of Chemical (pH Adjusters (Acids), pH Adjusters (Bases), Water Softeners), By Application (Raw Water Treatment, Boiler Water Treatment, Cooling Water Treatment, Wastewater Treatment, Process Water Treatment, Desalination), By End-User Industry (Municipal, Industrial, Commercial

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Kurita Water Industries Ltd. (Japan), BASF SE (Germany), Kemira Oyj (Finland), Solenis LLC (U.S.), Ion Exchange (India) Ltd. (India), Veolia Water Technologies (France), Thermax Limited (India), The Dow Chemical Company (U.S.), Nouryon (The Netherlands),

|

|

Countries

|

China, India, Japan, South Korea, Australia, South East Asia

|

Asia-Pacific pH Adjusters and Softeners Market for Water Treatment Market Segmentation

By Type of Chemical

- pH Adjusters (Acids)

- pH Adjusters (Bases)

- Water Softeners

By Application

- Raw Water Treatment

- Boiler Water Treatment

- Cooling Water Treatment

- Wastewater Treatment

- Process Water Treatment

- Desalination

By End-User Industry

- Municipal

- Drinking Water Treatment Plants

- Municipal Wastewater Treatment Plants

- Industrial

- Power Generation

- Chemical and Petrochemical

- Food and Beverage

- Pulp and Paper

- Mining and Metallurgy

- Textile

- Pharmaceutical

- Electronics and Semiconductors

- Oil and Gas

- Other Manufacturing Industries

- Commercial

- China

- India

- Japan

- South Korea

- Australia

- South East Asia

- Rest of Asia

Top Companies in Asia-Pacific pH Adjusters and Softeners Market for Water Treatment

- Ecolab Inc. (U.S.)

- Kurita Water Industries Ltd. (Japan)

- BASF SE (Germany)

- Kemira Oyj (Finland)

- Solenis LLC (U.S.)

- Ion Exchange (India) Ltd. (India)

- Veolia Water Technologies (France)

- Thermax Limited (India)

- The Dow Chemical Company (U.S.)

- Nouryon (The Netherlands)

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the Asia-Pacific pH Adjusters and Softeners Market for Water Treatment, providing a comprehensive analysis of market dynamics, technological trends, and growth opportunities shaping the regional water treatment sector. It highlights breakthroughs in acid and base formulations, softening technologies, IoT-enabled dosing automation, and integrated solutions for industrial and municipal applications. The analysis reviews key factors such as raw water variability, regulatory compliance, and performance-driven chemical optimization strategies. This report is an essential resource for utilities, industrial operators, and chemical suppliers aiming to achieve operational efficiency, water quality compliance, and sustainable treatment programs across Asia-Pacific.

Scope Includes:

- Segmentation By Type of Chemical: pH Adjusters (Acids, Bases), Water Softeners

- Segmentation By Application: Raw Water Treatment, Boiler Water Treatment, Cooling Water Treatment, Wastewater Treatment, Process Water Treatment, Desalination

- Segmentation By End-User Industry: Municipal (Drinking Water & Wastewater), Industrial (Power Generation, Chemical & Petrochemical, Food & Beverage, Pulp & Paper, Electronics & Semiconductors, Mining, Oil & Gas, Others), Commercial

- Geographic Scope: Analysis of China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Companies Covered: Ecolab Inc., Kurita Water Industries Ltd., BASF SE, Kemira Oyj, Solenis LLC, Ion Exchange (India) Ltd., Veolia Water Technologies, Thermax Limited, The Dow Chemical Company, Nouryon

Methodology

This report adopts a comprehensive research approach, combining primary interviews with water treatment specialists, plant engineers, and chemical manufacturers, with secondary research from verified industry databases, government publications, and technical journals. A dual estimation model using bottom-up and top-down methodologies ensures accurate market size projections. Advanced data triangulation, demand modeling, and regulatory analysis are applied to refine forecasts. The report incorporates scenario-based forecasting for regional regulatory shifts and technology adoption trends, ensuring actionable insights for strategic planning.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements