Ballast Water Treatment Systems Market Size, Growth Drivers, and Industry Insights (2025–2034)

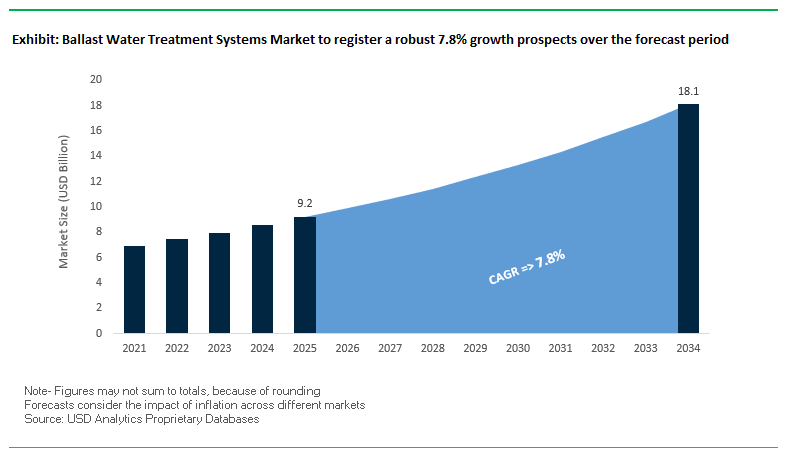

The global Ballast Water Treatment Systems (BWTS) market is projected to reach USD 9.2 billion in 2025 and expand to USD 18.1 billion by 2034, growing at a CAGR of 7.8%. The growth is propelled primarily by stringent maritime regulations such as the International Maritime Organization’s (IMO) Ballast Water Management (BWM) Convention and the U.S. Coast Guard (USCG) regulations, which mandate the treatment of ballast water to prevent the spread of invasive aquatic species.

The IMO's D-2 standard, coming into force on September 8, 2019, has already caused a mass wave of retrofit installations within the global fleet. Paris and Tokyo Memoranda of Understanding on Port State Control will conduct a joint Concentrated Inspection Campaign (CIC) between September and November 2025 to verify vessel documentation, crew competence, and operational effectiveness of BWMS. These initiatives not only provide assurance of compliance but also step-up demand for trusted, dual-certified treatment units capable of meeting both IMO and USCG requirements.

There is an important shift towards retrofit installations because newbuilding ships already meet the D-2 standard in a majority of cases. Retrofits continue to drive demand for small-footprint, module-based, and hybrid designs that minimize vessel downtime while meeting stringent regulatory requirements. Furthermore, since August 2025, over 48 BWMS have achieved double type approval and can be operated internationally in an unrestricted manner as a driving factor for key operators who function within a range of jurisdictional regimes.

Key Insights:

- Market Value 2025: USD 9.2 Billion

- Market Value 2034: USD 18.1 Billion

- CAGR (2025–2034): 7.8%

- Primary Drivers: IMO BWM Convention, USCG regulations, intensified inspections

- Dominant Segment: Retrofit installations over newbuilds

- Critical Feature Demand: Dual IMO & USCG certification for global compliance

Market Analysis: Regulatory Enforcement and Technology Developments Shaping the BWTS Market

Regulatory environment in 2025 is putting unprecedented pressure on shipowners to invest in high-capacity BWMS. The combined Paris and Tokyo MoU CIC (September–November 2025) will intensively review compliance via template-style questionnaires and will have detention power against non-compliant ships. Regulatory drive will act as a catalyst on the demand side in the near term for systems that can be documentation-ready and operator-friendly.

On the technology front, August 2025 saw DESMI Ocean Guard launch its CompactClean BWMS, a filter and UV-based system with dual IMO and USCG approvals. Its patent-pending UV design delivers both energy efficiency and ease of installation are key selling points in the retrofit-heavy market. Similarly, Wärtsilä has solidified its position with Aquarius systems in both filter-UV and filter-electro-chlorination versions, enabling unmatched operational flexibility.

Strategic production extension is also impacting market competitiveness. Alfa Laval started manufacturing PureBallast 3 systems in Qingdao, China, in 2021, centralizing supply to Asian ship repair yards where most retrofits take place. Headway Technology's OceanGuard, an electro-chlorination-based solution, continues to be certified by USCG, solidifying its foothold on trade routes bound for the United States. The USCG's continuously updated approved systems list continues to be a key procurement guide for operators, who then ensure that they invest in solutions meeting both performance and environmental protection criteria.

Trends and Opportunities in Ballast Water Treatment Systems Market

Trend 1: UV+Electrochlorination Hybrid Systems

Ballast water treatment systems (BWTS) markets continue to move toward hybrid technology employing a combination of UV and electrochlorination treatment technologies. Dual-technology systems utilize both methods' strengths to provide solid and reliable microbial control across a range of waters and high-flow operating applications. Wärtsilä's hybrid BWTS, for example, employs filtration combined with UV and electrochlorination and has achieved IMO type approval and new ferry constructions. Hybrid technology resolves UV-only system regrowth issues while still ensuring adequate disinfection in cloudy or low-salinity waters where UV penetration is minimal. Employing a combination not only complies with stringent regulation but also supplies ships' operations with flexibility, rendering hybrid systems a better solution for global maritime operations operating in a wide range of aquatic ecosystems.

Trend 2: Port-Based Treatment Solutions

Apart from onboard systems, the market is experiencing increased uptake of port-based and mobile ballast water treatment systems, usually presented as service propositions. Such shore-side treatment facilities are highly desirable in ships incapable of fitting out onboard BWTS or needing backup protection due to system failure. For instance, a bulk carrier employed a mobile system at a port to treat 8,200 cubic meters of highly turbid ballast water that would be difficult to treat for conventional UV systems. Port-based applications similarly avoid large retrofit expenditures between $500,000 to $5 million per ship deliver pay-per-use treatment making them financially desirable for small ships, old fleets, or dedicated trade routes within a region. Flexibility, reduced upfront capex burden, and operational ease make a port-based BWTS an emerging trend within the maritime treatment scene.

Opportunity 1: Great Lakes Fleet Retrofits

Specialized Great Lakes fleet presents a large market opportunity for ballast water treatment companies. Lakers, which is how these mass cargo ships are referred to, sail in cold, freshwater low-salinity seas that bring special challenges to treating ballast waters. Retrofits on these ships need standardized BWTS fitted out with filtration, UV, electrochlorination, and sometimes ozonation technology suited to local conditions. High ballast capacities ranging between 30,000 and 70,000 metric tons per trip generate predictable demand for good systems. Effective retrofits, like the afore-mentioned 165-foot Ranger III installation, validate feasibility and need for special solutions and put BWTS companies in a position to serve a special but highly regulated market segment within the Great Lakes area.

Opportunity 2: Cruise Ship Compliance

Cruise ships, due to their sophisticated operational routines and high ballast capacities, pose a highly attractive prospect for sophisticated BWTS. Such ships need to meet both IMO and USCG approval requirements, generating demand for double-approved systems. Effective ballast treatment is essential in order to escape fines, brand harm, and operational disruptions. Cruise ships need systems designed to accommodate ballasting and frequent deballasting operations in a wide range of waters, ranging from freshwater river intakes to high-salt oceans. Suppliers offering capable, large-capacity BWTS designed suited to cruise operations enjoy long-term contracts and repeat sales due to ongoing requirements for consistent compliance, environmental responsibility, and brand protection.

Ballast Water Treatment Systems Market Share Insights

Market Share by Technology Type: Hybrid Systems as the Preferred Choice

Hybrid ballast water treatment systems are projected to capture nearly 45% of the global BWTS market share in 2025, making them the undisputed industry leader. By combining technologies such as filtration with UV or electrochlorination, hybrid systems provide versatility across diverse water conditions, including varying salinity and turbidity levels, which is critical for vessels operating globally. Their dominance is reinforced by shipowners’ preference for reliability, broad compliance assurance with both IMO and USCG ballast water regulations, and reduced operational risk. While physical UV-based systems are favored for their chemical-free operation, they can be challenged in turbid waters, whereas chemical treatment remains effective but faces scrutiny due to residual discharge and handling risks. The market trend clearly indicates that hybrid systems have become the benchmark for regulatory certainty and long-term operational confidence.

Market Share by Vessel Type: Merchant Vessels Driving Core Demand

Merchant vessels are expected to account for around 65% of the BWTS market in 2025, making them the primary revenue driver. Bulk carriers, oil tankers, and container ships dominate The category due to their high ballast water capacities and global trading routes, which mandate strict compliance with international regulations. The segment alone represents the backbone of ballast water treatment demand, given the urgency to meet enforcement deadlines under IMO D-2 standards. Offshore vessels form the next significant segment, requiring rugged and reliable systems due to frequent ballasting operations in harsh environments. Cruise ships and ferries are smaller in number but represent a high-value market as operators emphasize UV-based eco-friendly solutions to support sustainability commitments and brand reputation. Naval and special purpose vessels contribute niche demand, often with customized systems, but the merchant fleet remains the largest and most critical growth engine.

Market By Vessel Type (2025).png)

Market Share by System Capacity: Medium Systems as the Market Sweet Spot

The medium capacity segment (500–3,000 m³/h) is projected to hold the largest share at about 45% of the BWTS market by 2025, reflecting its suitability for the majority of Panamax container ships, medium-sized tankers, and offshore vessels. These systems represent the highest volume demand due to their alignment with the operational profiles of the world’s most common vessel types. Large-capacity systems (>3,000 m³/h), accounting for 40%, generate significant revenues as they serve VLCCs and ultra-large bulk carriers but involve fewer contracts due to the limited number of such vessels. Small systems (<500 m³/h), at around 15%, cater to tugs, ferries, and yachts, where compactness and cost efficiency matter most. The distribution highlights how the BWTS market is strongly shaped by vessel size demographics, with medium-capacity systems forming the commercial backbone while large systems drive engineering complexity and high-value contracts.

Market Share by Installation Type: Retrofit Installations Dominating Fleet Compliance

Retrofit installations are projected to represent nearly 70% of the BWTS market share in 2025, underscoring the industry’s ongoing compliance push. The retrofit wave gained momentum following the IMO 2017 enforcement and US Coast Guard regulations, compelling thousands of in-service vessels to integrate treatment systems. Although the initial retrofit surge has passed, extensions and phased compliance continue to drive installations, particularly across aging fleets that cannot defer upgrades any longer. Newbuild installations, accounting for 30%, are steadily becoming the stable long-term segment as every newly constructed ship is now delivered with a BWTS integrated into its design. The structural shift indicates that while retrofits dominate near-term revenues, the newbuild segment will define the sustainable baseline demand over the next decade as shipbuilding cycles normalize.

Market Share by Treatment Stage: Two-Stage Systems as the Industry Standard

Two-stage treatment systems are expected to command about 60% of the BWTS market share in 2025, cementing their position as the industry standard. The configuration combining pre-filtration with a secondary disinfection stage such as UV or chemical treatment ensures compliance even in challenging water conditions by targeting both large sediments and smaller pathogens. Multi-stage systems are gaining traction among vessels that operate across highly variable water qualities, where advanced oxidation or additional filtration steps enhance performance. By contrast, single-stage systems are declining due to their reduced effectiveness in turbid waters and limited operational flexibility. The dominance of two-stage systems reflects a broader market shift toward regulatory certainty, operational resilience, and shipowner preference for proven solutions that balance cost with compliance.

Country Analysis of the Ballast Water Treatment Systems Market

United States: Regulatory Compliance and UV-Based Technologies Lead Adoption

US ballast water treatment systems market is mainly driven by the stringent regulations of the United States Coast Guard (USCG), which exceed international IMO norms often. Regulatory landscape has fueled intense demand for USCG Type Approved BWTS mainly in key shipping centers such as the Port of Los Angeles and the Port of New York and New Jersey. US operators overwhelmingly prefer UV-based ballast water treatment systems that provide non-chemical, environmentally friendly ballast water solutions meeting both USCG and IMO discharge specifications. Consolidation of market players in regional marine equipment supply bases is also observed, facilitating integrated ballast water compliance packages and post-install facilities. Modular and scalable systems are also becoming popular, especially for the inland waterway fleet, due to a shift toward flexible and efficient ballast water solutions.

China: Shipbuilding Growth and Smart BWTS Integration

China contributes to global BWTS demand primarily due to its role as a large shipbuilding nation. Newbuild ships account for a large part of the market, and state policies mandating marine environmental protection further increase use of modern ballast water treatment facilities. Chinese law requires appropriate ballast water discharge, creating demand for automated and sensor-based separation units. Approval by Shanghai Ocean University's DNV GL-approved Ballast Water Detecting Lab further increases market capacity for compliance testing and research. China's 14th Five-Year Plan further supports use of energy-efficient wastewater treatment technology, further boosting use of smart BWTS across both industrial and maritime bases.

South Korea: Shipbuilding Expansion Spurs Hybrid System Adoption

As a premier shipbuilding country, South Korea serves a double role both as a large manufacturer and user of BWTS. Expansion in bulk carrier and containership segments triggers installation of new build ships with IMO-certifiable ballast water treatment systems. South Korean shipping equipment supplies like Techcross continue to widen service networks across the world to facilitate maintenance and retrofit works. The segment further gains traction due to growing demand for hybrid BWTS employing a variety of disinfection methods to suit changing port water quality and provide environmental compliance. It places South Korea at a center both for production and innovation in ballast water treatment technology.

Japan: Technological Innovation and Compact Energy-Efficient Units

Japanese BWTS market is characterized by cutting-edge technology development and a strong shipbuilding industry. Nansei Corporation teamed up with Korea NK Co., Ltd. to unveil ozone-based NK-O3 BlueBallast systems that can be easily installed and maintained with minimal effort. JFE Engineering Corporation stands out in keeping things simple and making units small and power-efficient. Japan's push on R&D serves to nurture hybrid systems combining a number of disinfection technologies to suit divergent port and water scenarios while maintaining environmental friendliness. Focus on innovation makes Japan a force to be reckoned within both Japanese and overseas BWTS markets.

Singapore: Stringent Port Regulations and Green Shipping Initiatives

Singapore, a major global shipping hub, enforces strict ballast water regulations, driving adoption of advanced BWTS solutions. The Maritime and Port Authority of Singapore (MPA) actively promotes green shipping practices, emphasizing sustainability and environmental compliance. Singapore’s role as a trans-shipping nexus creates high demand for systems capable of handling diverse water conditions. The market increasingly favors automated and modular ballast water treatment technologies, ensuring vessels meet international and local discharge standards while supporting efficient port operations.

Germany (Europe): Modular and Energy-Efficient Systems for Container Fleet

Germany, as part of the European BWTS market, benefits from the EU’s rigorous environmental standards that often surpass IMO requirements. The country sees high adoption of modular and energy-efficient ballast water systems, particularly for container ships. Leading global players like Alfa Laval and Wärtsilä drive innovation through remote monitoring, automation, and data analytics integration, creating intelligent ballast water management solutions. Germany’s strong maritime industry and regulatory compliance focus continue to fuel demand for advanced, high-performance BWTS across Europe.

Competitive Landscape – Leading Players Driving Market Innovation

The BWTS market is dominated by established marine technology providers that combine regulatory compliance, engineering expertise, and global service capabilities. These companies are differentiating through system flexibility, retrofit compatibility, and dual certifications that allow for unrestricted operation in any port jurisdiction.

Alfa Laval – Pioneering UV-based BWMS Solutions

Alfa Laval has become a market leader in PureBallast BWMS that is a non-chemical UV-based technology certified both by IMO and USCG. By offering PureBallast 3 Compact Flex as a module system in a 20% reduced-footprint version, Alfa Laval tackles retrofitting's space and engineering limitations. With a service network in more than 100 countries supporting full lifecycle services ranging from commissioning to crew training, Alfa Laval is a preferred choice among operators who require low-maintenance but high-compliance solutions.

Wärtsilä – Dual-Technology Flexibility for Global Operations

Wärtsilä sells the Aquarius BWMS in two configurations: filter-UV and filter-electro-chlorination. Both configurations possess double IMO and USCG approval, enabling ships to sail freely anywhere in the world. Full lifecycle support is a key part of the firm's approach and encompasses engineering, installation, maintenance, and crew training within a single service model. Wärtsilä's broad-based portfolio of marine technology makes it a flexible partner to shipowners.

DESMI Ocean Guard – Energy-Efficient, Compact Solutions

DESMI's CompactClean BWMS was introduced in August 2025 and integrates filtration and a highly optimized UV reactor in a highly energy-efficient and highly compact package. It has no salinity, temperature, or turbidity restrictions on waters and is consequently a fully global compliance solution. Its integrated ballast stripping pump eliminates a common operating issue and makes it highly sought after for retrofit applications.

Headway Technology – Electro-Chlorination Expertise for Large Volumes

Headway Technology's OceanGuard BWMS employs electro-chlorination to handle high ballast volumes at a low power operating condition. With USCG approval having been attained, it is appropriate for ships trading to the United States and overseas. Headway's established position in the Asian shipbuilding market alongside a product development profile driven by compliance will keep it a major contender in the BWTS marketplace.

Ballast Water Treatment Systems Market Report Scope

Ballast Water Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.2 Billion

|

|

Market Size (2034)

|

$18.1 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Technology Type (Physical Treatment Systems, Chemical Treatment Systems, Hybrid Systems), By Vessel Type (Merchant Vessels, Offshore Vessels, Naval Vessels, Cruise Ships & Ferries, Special Purpose Vessels), By System Capacity (Small Systems (<500 m³/h), Medium Systems (500-3,000 m³/h), Large Systems (>3,000 m³/h)), By Installation Type (Newbuild Installations, Retrofit Installations), By Treatment Stage (1-Stage Treatment Systems, 2-Stage Treatment Systems, Multi-Stage Treatment Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Alfa Laval, Veolia Water Technologies, Wärtsilä, Xylem Inc., Panasia, Techcross, Desmi, Ecochlor, Trojan Marinex, Mitsubishi Heavy Industries, Hyde Marine, Qingdao Sunrui, JFE Engineering

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ballast Water Treatment Systems Market Segmentation

By Technology Type

- Physical Treatment Systems

- Chemical Treatment Systems

- Hybrid Systems

- UV + Chemical

- Filtration + Electrochlorination

- Mechanical + Chemical

By Vessel Type

- Merchant Vessels

- Offshore Vessels

- Naval Vessels

- Cruise Ships & Ferries

- Special Purpose Vessels

By System Capacity

- Small Systems (<500 m³/h)

- Medium Systems (500-3,000 m³/h)

- Large Systems (>3,000 m³/h)

By Installation Type

- Newbuild Installations

- Retrofit Installations

By Treatment Stage

- 1-Stage Treatment Systems

- 2-Stage Treatment Systems

- Multi-Stage Treatment Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Ballast Water Treatment Systems Market

- Alfa Laval

- Veolia Water Technologies

- Wärtsilä

- Xylem Inc.

- Panasia

- Techcross

- Desmi

- Ecochlor

- Trojan Marinex

- Mitsubishi Heavy Industries

- Hyde Marine

- Qingdao Sunrui

- JFE Engineering

* List Not Exhaustive

Research Coverage

This report investigates the Global Ballast Water Treatment Systems (BWTS) Market, offering detailed analysis reviews of regulatory enforcement, retrofit demand, and technological breakthroughs reshaping compliance strategies in the maritime industry. Published by USDAnalytics, it highlights how the IMO Ballast Water Management Convention, U.S. Coast Guard (USCG) approvals, and regional port state control initiatives are driving large-scale adoption of dual-certified systems. The study also highlights trends such as hybrid UV-electrochlorination solutions, port-based treatment services, and opportunities in specialized segments like the Great Lakes fleet and cruise ships. By profiling leading players, market dynamics, and regulatory timelines, this report is an essential resource for shipowners, regulators, marine equipment providers, and investors seeking clarity on compliance readiness, retrofit strategies, and long-term growth opportunities in the BWTS market.

Scope Includes:

- Segmentation: By Technology Type (Hybrid, UV, Electro-Chlorination, Ozone & Others), By Vessel Type (Merchant, Offshore, Cruise/Ferries, Naval/Special Purpose), By System Capacity (<500 m³/h, 500–3,000 m³/h, >3,000 m³/h), By Installation Type (Retrofit, Newbuild), and By Treatment Stage (Single-Stage, Two-Stage, Multi-Stage).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic & Forecast: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Competitive profiling and strategic analysis of 15+ leading BWTS companies globally.

Methodology

The research methodology applied by USDAnalytics combines primary and secondary intelligence to ensure robust market estimation and insight validation. Primary research included interviews with shipowners, marine engineers, port authorities, and ballast water equipment manufacturers to capture real-time adoption challenges and compliance strategies. Secondary research leveraged regulatory documents, IMO/USCG approvals, corporate disclosures, technical papers, and marine trade databases. Market sizing was conducted through both top-down and bottom-up approaches, reconciled via data triangulation and scenario analysis for regulatory enforcement timelines and retrofit cycles. This methodology provides stakeholders with a comprehensive, validated, and forward-looking view of the BWTS market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Ballast Water Treatment Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights

1.3. Global Market Snapshot

2. Ballast Water Treatment Systems Market Size, Growth Drivers, and Industry Insights (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $9.2 Billion

2.2.2. Forecasted Market Size (2034): $18.1 Billion at 7.8% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Stringent Maritime Regulations (IMO BWM Convention & USCG Regulations)

2.3.2. Dominance of Retrofit Installations

2.3.3. Demand for Dual-Certified Systems

3. Market Analysis: Regulatory Enforcement and Technology Developments

3.1. Overview of Market Dynamics

3.2. Regulatory Enforcement and Inspection Campaigns

3.2.1. Paris and Tokyo MoU Concentrated Inspection Campaign (CIC)

3.3. Technological Advancements

3.3.1. DESMI Ocean Guard's CompactClean BWMS

3.3.2. Wärtsilä's Aquarius Systems

3.4. Strategic Production and Certification

3.4.1. Alfa Laval's Manufacturing in China

3.4.2. Headway Technology's USCG-Approved OceanGuard

4. Trends and Opportunities in Ballast Water Treatment Systems Market

4.1. Trend 1: Hybrid Systems (UV + Electrochlorination)

4.1.1. Combining Strengths for Versatile Water Conditions

4.1.2. Enhanced Reliability and Compliance

4.2. Trend 2: Port-Based Treatment Solutions

4.2.1. Service Propositions for Ships with Installation Limitations

4.2.2. Reduced Upfront Capital Expenditure for Shipowners

4.3. Opportunity 1: Great Lakes Fleet Retrofits

4.3.1. Specialized Solutions for Cold, Freshwater Environments

4.3.2. High-Capacity Demand from Lakers

4.4. Opportunity 2: Cruise Ship Compliance

4.4.1. Attractive Market for Sophisticated, Dual-Approved Systems

4.4.2. Protecting Brand Reputation and Avoiding Fines

5. Ballast Water Treatment Systems Market Share Insights

5.1. By Technology Type

5.1.1. Hybrid Systems

5.1.2. Physical (UV-based) Systems

5.1.3. Chemical Treatment

5.2. By Vessel Type

5.2.1. Merchant Vessels

5.2.2. Offshore Vessels

5.2.3. Cruise Ships & Ferries

5.3. By System Capacity

5.3.1. Medium Systems (500–3,000 m³/h)

5.3.2. Large Systems (>3,000 m³/h)

5.3.3. Small Systems (<500 m³/h)

5.4. By Installation Type

5.4.1. Retrofit Installations

5.4.2. Newbuild Installations

5.5. By Treatment Stage

5.5.1. Two-Stage Treatment Systems

5.5.2. Multi-Stage and Single-Stage Systems

6. Country Analysis of the Ballast Water Treatment Systems Market

6.1. United States: USCG Regulations and UV-based Technology

6.2. China: Shipbuilding and Smart BWTS Integration

6.3. South Korea: Shipbuilding and Hybrid System Adoption

6.4. Japan: Technological Innovation and Compact Units

6.5. Singapore: Stringent Port Regulations

6.6. Germany (Europe): Modular and Energy-Efficient Systems

6.7. Other Country Analysis

7. Ballast Water Treatment Systems Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Technology, Vessel Type, Capacity, and Installation

7.2. Europe Market Size Outlook to 2034

7.2.1. By Technology, Vessel Type, Capacity, and Installation

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Technology, Vessel Type, Capacity, and Installation

7.4. South America Market Size Outlook to 2034

7.4.1. By Technology, Vessel Type, Capacity, and Installation

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Technology, Vessel Type, Capacity, and Installation

8. Company Profiles: Top Companies in Ballast Water Treatment Systems Market

8.1. Alfa Laval

8.2. Wärtsilä

8.3. DESMI Ocean Guard

8.4. Headway Technology

8.5. Veolia Water Technologies

8.6. Xylem Inc.

8.7. Panasia

8.8. Techcross

8.9. Ecochlor

8.10. Trojan Marinex

8.11. Mitsubishi Heavy Industries

8.12. Hyde Marine

8.13. Qingdao Sunrui

8.14. JFE Engineering

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations