Market Overview: Rising Demand for Efficient Membrane System Retrofitting and Upgrades

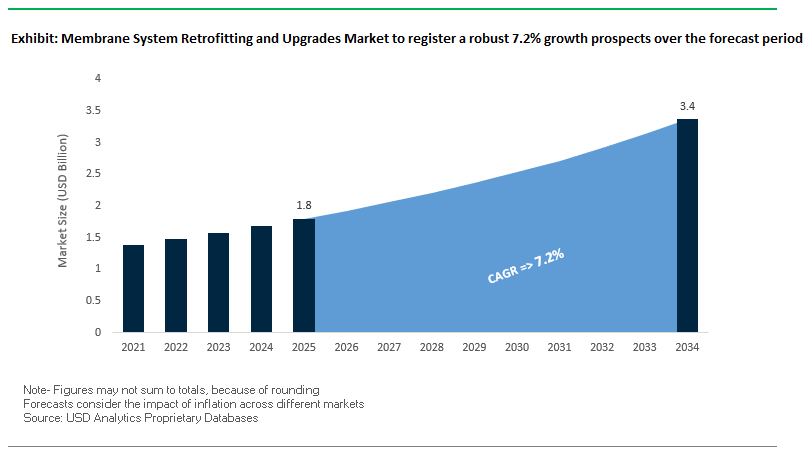

The global membrane system retrofitting and upgrades market is projected to grow from USD 1.8 billion in 2025 to USD 3.4 billion by 2034, registering a steady CAGR of 7.2%. This growth underscores the increasing importance of upgrading existing water treatment and industrial filtration systems to meet rising sustainability demands, reduce operational costs, and enhance energy efficiency.

Key Insights for Industry Stakeholders

- Cost-efficiency and sustainability are the primary drivers behind retrofitting projects, as industries seek to extend system life while reducing capital expenditure.

- Regulatory compliance in regions like North America, Europe, and Asia Pacific is accelerating retrofits, particularly in municipal and industrial wastewater sectors.

- Hybrid membrane systems are increasingly integrated into retrofits to optimize performance across RO, UF, and NF applications.

- Digital monitoring and predictive analytics are being incorporated into upgrades, offering real-time data that enhances system reliability and lowers maintenance costs.

Market Analysis: Innovations and Strategic Moves Defining Growth

The membrane system retrofitting and upgrades market is witnessing a strong wave of innovation, partnerships, and sustainability-focused advancements. Retrofitting existing systems has emerged as a cost-effective alternative to greenfield installations, with companies leveraging advanced polymeric membranes, hybrid systems, and AI-powered analytics to boost performance.

In August 2025, DuPont Water Solutions received the BIG Sustainability Award for its FilmTec™ Fortilife™ membranes, which are designed to enhance industrial wastewater reuse. This recognition highlights how retrofits are increasingly tied to environmental performance metrics, where the ability to recycle water while lowering energy use has become a competitive advantage. Similarly, March 2025 marked a pivotal moment when Toray Industries, Inc. introduced a new reverse osmosis membrane that cuts replacement frequency in half and reduces CO₂ emissions. Such innovations are directly reshaping the retrofitting market by extending system lifecycles and lowering total ownership costs.

Strategic collaborations are also shaping retrofitting opportunities. In July 2025, SUEZ partnered with AgriTech startup Seabex to apply advanced membrane-integrated biochar solutions in agriculture. Earlier, in April 2025, SUEZ and CNRS signed a five-year strategic R&D partnership to push the boundaries of sustainable water and waste management. These moves demonstrate how membrane upgrades are being aligned with cross-sector decarbonization and circular economy goals.

Meanwhile, Veolia Water Technologies has been aggressively advancing retrofit applications. In June 2025, the company secured a large municipal wastewater reuse project in Brazil, and in October 2024, it deployed its MemGas™ membrane modules in San Francisco to convert biogas into renewable natural gas. Such projects highlight the evolving role of retrofits in energy recovery and resource valorization, expanding their scope beyond water treatment.

The period also saw new applications of membrane retrofits in environmental sustainability. Nitto Denko Corporation showcased carbon-negative membrane technology at COP29 in November 2024, introducing CO₂ separation solutions for industrial exhaust. Alongside this, Kurita America’s July 2024 partnership with Solugen to develop carbon-negative water treatment chemicals reflects how the market is steadily evolving into a hub for climate-focused solutions.

Key Trends and Emerging Opportunities Driving the Membrane System Retrofitting and Upgrades Market

Stricter Environmental Regulations Driving Retrofitting Demand

One of the most influential trends reshaping the membrane system retrofitting and upgrades market is the rise of stringent wastewater discharge and drinking water standards. Operators of legacy plants are increasingly forced to retrofit with advanced membrane systems to maintain compliance. The U.S. Environmental Protection Agency’s (EPA) Drinking Water State Revolving Fund (DWSRF) Handbook explicitly categorizes projects addressing “emerging contaminants of concern” as eligible for funding, ensuring a financial pathway for municipalities to modernize. Moreover, technical insights from Integrated Water Services highlight that new discharge permits are increasingly targeting nutrients and trace contaminants, positioning membrane bioreactor (MBR) retrofits as a critical compliance solution. This shows how policy enforcement and funding incentives are accelerating the adoption of retrofitting services across municipal and industrial segments.

Technological Advancements in Membrane Materials and Digital Control Systems

Another defining trend is the integration of advanced membrane materials with AI-powered control systems. Recent studies published in ResearchGate demonstrate how machine learning models can accurately predict membrane fouling and optimize cleaning cycles, drastically improving uptime and efficiency. Similarly, research in MDPI highlighted that modifying existing membranes with nanomaterials enhanced permeability by more than 80%, showing how retrofits are delivering transformative efficiency gains. Beyond materials, upgrades in automation such as PLC, SCADA, and predictive AI monitoring are reducing operator intervention and minimizing energy costs. This shift underscores that retrofitting is no longer about physical replacement alone, but also about digitally enabling plants for smarter, more sustainable operation.

Cost-Effectiveness of Retrofitting Versus New-Build Facilities

The cost advantage of retrofitting is a dominant driver of market growth, as it allows operators to expand capacity and improve water quality without investing in new facilities. A case study from a global water company demonstrated that a large industrial facility retrofitted with tubular membranes for high-solids wastewater treatment achieved significant capacity expansion and water recovery saving millions in capital costs and avoiding long construction delays. Such examples reinforce the perception of retrofitting as a low-risk, high-ROI alternative to greenfield projects, especially for industries balancing sustainability goals with tight capital budgets.

Corporate Investments Linking Sustainability and Retrofitting Technologies

Corporate sustainability strategies are directly fueling investment in retrofitting technologies. A prime example is Micron Technology’s partnership with Aqua Membranes, where pilot projects are focusing on integrating advanced RO retrofits to boost water reuse in semiconductor fabrication facilities. This aligns with broader industrial trends where multinationals are embedding retrofitting programs into ESG commitments, reducing water intensity while protecting shareholder value. As a result, retrofitting has evolved from being purely an operational decision to a strategic sustainability investment, making it increasingly attractive to both corporate and municipal stakeholders.

Opportunities in Energy Efficiency, AI-Driven Upgrades, and Resource Recovery

Looking ahead, the strongest opportunities lie in energy efficiency retrofits, AI-enabled optimization, and resource recovery applications. Energy Recovery Devices (ERDs), high-efficiency pumps, and smart automation upgrades can reduce the largest operational cost in RO systems energy consumption by double-digit percentages, creating clear ROI cases. Similarly, the growing adoption of AI-driven membrane monitoring offers new service opportunities for predictive maintenance providers. Additionally, as industries place more value on resource recovery (e.g., nutrients, chemicals, clean water), retrofitting projects with hybrid membrane systems offer lucrative potential. Together, these opportunities ensure that membrane system retrofitting is positioned as both an economic and sustainability enabler for the global water sector.

Market Share Analysis of the Membrane System Retrofitting and Upgrades Market

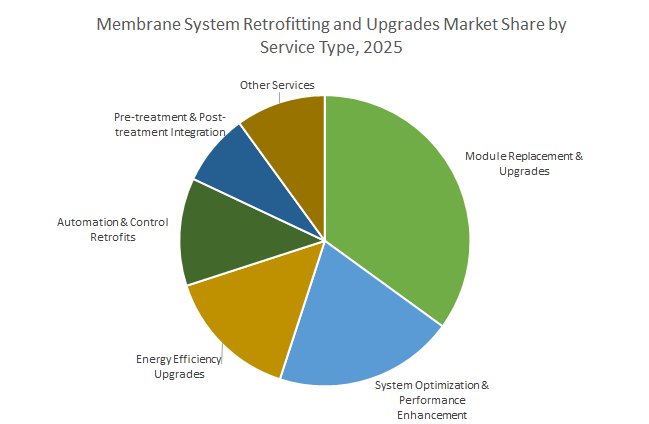

Module Replacement Dominates Services While Energy Efficiency Retrofits Drive Growth

By service type, module replacement and upgrades hold the largest share at 35%, reflecting the recurring demand created by the limited lifespan of membranes. This segment provides a stable revenue base for suppliers as operators consistently swap old modules for newer, high-performance versions. However, the growth engines are energy efficiency upgrades (15%) and automation retrofits (12%), which deliver measurable OPEX savings and improved plant intelligence. System optimization and performance enhancement, accounting for 20%, reflect the industry’s shift from reactive fixes to proactive, holistic asset management. As energy remains the most significant cost in RO and desalination systems, ERDs and high-efficiency pumps are among the most impactful retrofitting services, making this a priority area for plant operators seeking ROI-driven upgrades.

Reverse Osmosis Membranes Lead Retrofitting Demand With UF and NF Rising

In terms of membrane type, reverse osmosis (RO) dominates with 50% share of retrofitting demand, as RO systems are the most energy-intensive and operationally complex, offering the greatest potential for savings when upgraded. Replacing older RO elements with high-rejection, high-permeability, or anti-biofouling membranes provides immediate performance gains. Ultrafiltration (22%) and microfiltration (15%) membranes are primarily upgraded to protect downstream RO systems, ensuring reduced fouling and extended lifespan. Meanwhile, nanofiltration (8%) is rapidly emerging, as plants retrofit to tackle specific contaminants such as PFAS and hardness more efficiently than RO. Other niche membranes like FO and ED (5%) are gaining traction in hybrid retrofits, particularly for industrial separations and reducing RO burden. This segmentation highlights how RO upgrades anchor the market, while UF and NF retrofits expand its scope into compliance-driven and selective applications.

Water and Wastewater Treatment Anchors Applications While Desalination Maximizes Value

By application, water and wastewater treatment accounts for the largest share at 40%, as municipalities and industries worldwide prioritize retrofitting existing assets to meet tighter discharge standards and reuse targets. Desalination represents 25%, making it the most high-value application segment, as retrofits here can reduce enormous energy costs and extend plant capacity without major capital outlays. Industrial processing contributes 20%, driven by needs in food & beverage, pharmaceuticals, and chemicals, where upgrades enhance product quality and enable resource recovery. Power generation applications (10%) focus on boiler feed and cooling water reliability, while smaller segments (5%) cover commercial and residential systems. These insights highlight that while municipal water remains the foundation of demand, desalination and industrial retrofits are critical for unlocking higher-margin growth.

Municipal Utilities Lead End-Use, Industrial Facilities Emerging as Fast Adopters

By end-use industry, municipal and utility operators account for 45% of demand, as they manage aging public water infrastructure under the dual pressures of regulatory compliance and budget constraints. Retrofitting allows them to extend system lifespans without excessive capital expenditure, making it the most stable segment of the market. Industrial end-users (40%) including food & beverage, pharmaceuticals, chemicals, and power are the fastest adopters, as their investment decisions hinge on ROI, uptime, and sustainability goals. Commercial buildings (10%) such as hospitals and hotels adopt retrofits mainly for water quality improvement and operational efficiency, while residential demand (5%) remains fragmented and replacement-driven. This segmentation reflects how municipalities drive large, steady contracts, while industrial customers drive rapid, ROI-focused adoption of advanced retrofitting technologies.

United States: Federal Funding and Cutting-Edge Membrane Retrofits Transform Water Infrastructure

The United States market for membrane system retrofitting is significantly driven by government funding and technological innovation. The Bipartisan Infrastructure Law allocates over $50 billion to the EPA to enhance the nation’s water infrastructure, with dedicated funds to address emerging contaminants such as PFAS. The new PFAS Maximum Contaminant Levels established by the U.S. EPA are accelerating retrofit spending across existing treatment plants, driving the adoption of advanced membrane technologies. Public-private partnerships like the National Alliance for Water Innovation (NAWI) focus on lowering desalination costs and energy requirements, often through retrofitting older facilities with innovative membranes. Leading companies such as Veolia Water Technologies, Evoqua Water Technologies, and Koch Separation Solutions have introduced modular MBR systems that allow cost-effective retrofitting and enhanced operational efficiency. Applications are expanding across dialysis centers and biologics manufacturing, particularly in monoclonal antibodies, cell and gene therapies, and mRNA-based drugs, ensuring membrane retrofitting remains at the forefront of high-performance water treatment solutions.

China: Policy-Driven Retrofits and Advanced Modular Membrane Systems

China’s membrane retrofitting market is strongly influenced by stringent regulations and technological advancements. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge standards, encouraging the adoption of advanced membrane technologies in plant upgrades. The government’s “Guiding Opinions on Promoting the Utilization of Wastewater Resources” targets a recycled water utilization rate of 25% or more in water-scarce cities by 2025, making retrofitting of existing facilities critical. In 2024, researchers at the Chinese Academy of Sciences developed dual-functional RO membranes with antibacterial and anti-adhesion properties, ideal for modular retrofits. Domestic production localization and competitive pricing have allowed Chinese companies to win replacement and upgrade projects in the industrial wastewater sector, making retrofits economically feasible and technologically effective.

India: Government Missions and Infrastructure Investments Fuel Membrane Upgrades

India’s membrane retrofitting market benefits from government initiatives and large-scale infrastructure investments. The “Jal Jeevan Mission” drives membrane technology adoption in rural areas, while public-private partnerships (PPPs) in cities like Ayodhya and Prayagraj enable retrofitting of older sewage treatment facilities. The Ghaziabad Nagar Nigam’s ₹150 crore Certified Green Municipal Bond-funded Tertiary Sewage Treatment Plant (TSTP) serves as a model for retrofitting older plants with advanced membrane systems for industrial water reuse. Large-scale projects such as the 3x50 MLD desalination plant in Kakinada SEZ, backed by a ₹1,310 crore investment, provide opportunities for subsequent retrofitting and expansion phases to increase capacity and efficiency, positioning India as a rapidly evolving market for membrane system upgrades.

Germany: Industrial Wastewater Leadership and Innovative Retrofit Solutions

Germany leads in retrofitting industrial wastewater plants with advanced membrane systems. The Federal Wastewater Charges Act imposes fees on untreated discharges, encouraging companies to adopt retrofits using polymeric and ceramic membranes. Technological solutions, such as TIA-Abwasser’s textile knitted fabric, can be retrofitted into existing aeration tanks without interrupting operations, enhancing biomass and purification processes. Companies like PPU Umwelttechnik provide containerized membrane systems that can be installed in both new and existing tanks, offering cost-effective retrofit options. This combination of regulatory incentives and technological advancements positions Germany as a mature and innovative market for membrane system retrofitting.

Japan: High-Efficiency MBR Modules and Strategic Government Support for Upgrades

Japan’s membrane retrofitting market is driven by technological advancements and supportive government policies. In 2025, Toray Industries introduced high-efficiency separation membrane modules for biopharmaceutical manufacturing, offering over double the filtration performance of conventional systems by reducing clogging, making them ideal for retrofitting older facilities. The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) launched the A-JUMP project to promote full-scale MBR adoption, facilitating upgrades in medium- to large-scale sewage treatment plants. MBR technology is expected to become a core solution for plant reconstruction, retrofitting, and performance enhancement, maintaining Japan’s position as a leading market for advanced membrane retrofits.

Saudi Arabia: Strategic Desalination Retrofits and Energy-Efficient Membrane Adoption

Saudi Arabia’s retrofitting market is driven by large-scale desalination projects and the shift toward energy-efficient RO membrane systems. The Saudi Water Authority (SWA) secured US$650 million to modernize the Jubail Phase I and Khobar Phase II plants, converting them from multi-stage flash (MSF) to reverse osmosis technology. The Saudi Water Partnership Company (SWPC) continues to launch membrane-based desalination projects, reinforcing the nation’s strategic shift from thermal methods. The Saline Water Conversion Corporation (SWCC) is pioneering highly energy-efficient RO membranes, with facilities like Yanbu 4 producing 450,000 cubic meters per day. These retrofitting initiatives enhance operational efficiency, reduce energy consumption, and support sustainable water management in the Kingdom.

Competitive Landscape: Leading Players Driving Membrane System Retrofitting and Upgrades

The competitive landscape of the membrane system retrofitting and upgrades market is defined by global water technology leaders and specialized innovators, each focusing on performance improvements, sustainability, and digital integration. Companies are differentiating themselves through advanced product portfolios, capacity expansion, and strategic partnerships aimed at reshaping the future of retrofits and upgrades.

Kurita Water Industries Ltd. – Strengthening Sustainability through Innovation

Kurita leverages decades of expertise in water treatment chemicals and facility solutions. In April 2025, its North American arm, Kurita America, merged with Avista Technologies, strengthening its retrofit and membrane treatment solutions. Kurita also partnered with Solugen in July 2024 to co-develop carbon-negative water treatment additives, reinforcing its leadership in sustainable retrofits. Its portfolio spans wastewater treatment, ultrapure water systems, and process water solutions, particularly catering to industries such as petrochemicals and pulp & paper.

DuPont Water Solutions – Setting New Standards in Industrial Wastewater Reuse

DuPont remains at the forefront with its FilmTec™ and IntegraTec™ membranes, widely used for RO and NF applications. Its FilmTec™ Fortilife™ series, recognized in August 2025 with a BIG Sustainability Award, is engineered for industrial water reuse, especially in high-biofouling environments. With a strategic focus on climate resilience, DuPont’s Water & Nature strategy is aligning product innovation with water stewardship and carbon reduction goals, making it a benchmark for sustainable retrofitting solutions.

Evoqua Water Technologies LLC (A Xylem Brand) – Expanding Reach in Critical Retrofits

Now part of Xylem since 2023, Evoqua specializes in mission-critical water retrofits for industrial and municipal systems. The company operates in 160+ locations across 10 countries and serves 38,000+ customers globally. Its recent investment in a Sustainability and Innovation Hub in Pittsburgh underscores its commitment to emerging challenges such as PFAS removal and climate-driven water risks. Through its expanded portfolio under Xylem, Evoqua is poised to deliver highly customized retrofit solutions.

SUEZ Water Technologies & Solutions – Driving Digital-Integrated Retrofitting

With operations in 130 countries, SUEZ plays a pivotal role in retrofitting large-scale facilities. The company secured major contracts in Asia for seawater RO and industrial wastewater recycling plants, advancing its commitment to 100% water reuse. Its AQUADVANCED® Water Networks platform integrates predictive analytics with physical upgrades, optimizing retrofits for efficiency and resilience. By linking membrane retrofits with digitalization, SUEZ is redefining what sustainable upgrades can deliver.

Veolia Water Technologies – Expanding Retrofit Applications in Energy and Water

Veolia, a global leader in ecological transformation, manages 13 million m³/day treatment capacity across 44 countries. In May 2025, the company took full ownership of its Water Technologies and Solutions subsidiary to streamline innovation and accelerate delivery. Veolia’s MemGas™ membrane modules, deployed in San Francisco (October 2024), showcase retrofit applications in renewable natural gas production, proving its versatility in both water reuse and energy recovery markets.

Toray Industries, Inc. – Innovating High-Performance RO Membranes

Toray, a leader in polymer and composite materials, has been driving innovation in RO membranes for decades. In March 2025, it introduced a next-generation RO membrane that delivers water savings, double chemical resistance, and reduced CO₂ emissions, all of which are critical for retrofits in water-scarce regions. Its Water Treatment Technology Center in Saudi Arabia strengthens its Middle Eastern footprint, ensuring technical support and scalability in regions with acute water challenges.

Membrane System Retrofitting and Upgrades Market Report Scope

Membrane System Retrofitting and Upgrades Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$3.4 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

By Service Type (Module Replacement & Upgrades, System Optimization & Performance Enhancement, Energy Efficiency Upgrades, Automation & Control Retrofits, Pre-treatment & Post-treatment Integration, Cleaning & Maintenance Optimization, Hybrid System Integration, Capacity Expansion & Plant Modification), By Membrane Type (Reverse Osmosis (RO), Nanofiltration (NF), Ultrafiltration (UF), Microfiltration (MF), Forward Osmosis (FO), Electrodialysis Membranes), By Application (Water & Wastewater Treatment, Desalination (Seawater & Brackish), Industrial Processing, Power Generation, Municipal Utilities, Residential & Commercial Systems), By End-Use Industry (Municipal & Utility Operators, Industrial, Commercial Buildings, Residential)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Toray Industries, Inc., SUEZ, Veolia, Pentair plc, Xylem Inc., The Dow Chemical Company, Koch Industries, LG Chem, Evoqua Water Technologies, MANN+HUMMEL, Aquatech International, Kubota Corporation, Kuraray Co., Ltd., Mitsubishi Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Membrane System Retrofitting and Upgrades Market Segmentation

By Service Type

- Module Replacement & Upgrades

- System Optimization & Performance Enhancement

- Energy Efficiency Upgrades

- Automation & Control Retrofits

- Pre-treatment & Post-treatment Integration

- Cleaning & Maintenance Optimization

- Hybrid System Integration

- Capacity Expansion & Plant Modification

By Membrane Type

- Reverse Osmosis (RO)

- Nanofiltration (NF)

- Ultrafiltration (UF)

- Microfiltration (MF)

- Forward Osmosis (FO)

- Electrodialysis Membranes

By Application

- Water & Wastewater Treatment

- Desalination (Seawater & Brackish)

- Industrial Processing

- Food & Beverage

- Pharmaceuticals & Biotechnology

- Chemicals & Petrochemicals

- Pulp & Paper

- Oil & Gas

- Power Generation

- Municipal Utilities

- Residential & Commercial Systems

By End-Use Industry

- Municipal & Utility Operators

- Industrial

- Commercial Buildings

- Residential

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Membrane System Retrofitting and Upgrades Industry include-

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- SUEZ

- Veolia

- Pentair plc

- Xylem Inc.

- The Dow Chemical Company

- Koch Industries

- LG Chem

- Evoqua Water Technologies

- MANN+HUMMEL

- Aquatech International

- Kubota Corporation

- Kuraray Co., Ltd.

- Mitsubishi Chemical Corporation

*- List not Exhaustive

Research Coverage

This report investigates the global Membrane System Retrofitting and Upgrades Market, delivering analysis reviews on demand drivers, breakthrough upgrade pathways, and operational benchmarks that improve energy efficiency, reliability, and lifecycle economics. Produced by USDAnalytics, this report is an essential resource for utilities, industrial operators, EPCs, and technology providers seeking to modernize legacy assets under tightening compliance and sustainability targets. It highlights how hybrid configurations, digital performance monitoring, and next-generation membranes convert existing plants into high-efficiency systems, underscores OPEX-centric ROI models, and showcases upgrade archetypes that reduce downtime while boosting capacity and water recovery offering decision-ready insights for retrofit road-mapping and capital planning. Scope Includes-

- Segmentation: By Service Type (Module Replacement & Upgrades, System Optimization & Performance Enhancement, Energy Efficiency Upgrades, Automation & Control Retrofits, Pre-treatment & Post-treatment Integration, Cleaning & Maintenance Optimization, Hybrid System Integration, Capacity Expansion & Plant Modification); By Membrane Type (Reverse Osmosis (RO), Nanofiltration (NF), Ultrafiltration (UF), Microfiltration (MF), Forward Osmosis (FO), Electrodialysis Membranes); By Application (Water & Wastewater Treatment, Desalination (Seawater & Brackish), Industrial Processing (Food & Beverage, Pharmaceuticals & Biotechnology, Chemicals & Petrochemicals, Pulp & Paper, Oil & Gas), Power Generation, Municipal Utilities, Residential & Commercial Systems); By End-Use Industry (Municipal & Utility Operators, Industrial, Commercial Buildings, Residential).

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): DuPont de Nemours, Inc.; Toray Industries, Inc.; SUEZ; Veolia; Pentair plc; Xylem Inc.; The Dow Chemical Company; Koch Industries; LG Chem; Evoqua Water Technologies; MANN+HUMMEL; Aquatech International; Kubota Corporation; Kuraray Co., Ltd.; Mitsubishi Chemical Corporation.

Methodology

Our methodology integrates bottom-up sizing by service type, membrane type, application, and end-use across each country with top-down triangulation using utility capex, industrial water intensity, and retrofit penetration ratios. Primary research comprised interviews with plant managers, maintenance heads, OEMs, integrators, and digital solution providers to validate upgrade costs, performance deltas, and payback periods. Secondary research included technical standards, environmental rules, tender databases, and vendor specifications to benchmark baseline versus post-retrofit KPIs (specific energy, flux, recovery, clean-in-place frequency, and uptime). Scenario models quantify sensitivities for energy prices, ERD adoption, anti-fouling elements, and automation maturity, yielding robust 2025–2034 forecasts and decision-grade guidance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Membrane System Retrofitting and Upgrades Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

1.3.1. Current Market Size (2025): USD 1.8 Billion

1.3.2. Forecasted Market Size (2034): USD 3.4 Billion

1.3.3. Projected Compound Annual Growth Rate (CAGR): 7.2%

2. Membrane System Retrofitting and Upgrades Market Outlook (2025–2034)

2.1. Introduction: Rising Demand for Efficiency and Sustainability

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends and Emerging Opportunities

2.3.1. Stricter Environmental Regulations Driving Retrofitting Demand

2.3.2. Technological Advancements in Membrane Materials and Digital Control Systems

2.3.3. Cost-Effectiveness of Retrofitting Versus New-Build Facilities

2.3.4. Corporate Investments Linking Sustainability and Retrofitting Technologies

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent News and Strategic Moves

3.1.1. DuPont Water Solutions Wins Sustainability Award (August 2025)

3.1.2. Toray Industries Introduces New High-Performance RO Membrane (March 2025)

3.1.3. SUEZ Forms Strategic Partnerships with AgriTech and R&D Centers (July & April 2025)

3.1.4. Veolia Expands Retrofit Applications in Energy and Water Reuse (October 2024 & June 2025)

3.1.5. Nitto Denko Showcases Carbon-Negative Membrane Technology at COP29 (November 2024)

3.1.6. Opportunities in Energy Efficiency, AI-Driven Upgrades, and Resource Recovery

4. Competitive Landscape: Membrane System Retrofitting and Upgrades Market

4.1. Market Overview: Leaders Driving Innovation and Global Adoption

4.2. Profiles of Top Players

4.2.1. Kurita Water Industries Ltd.

4.2.2. DuPont Water Solutions

4.2.3. Evoqua Water Technologies LLC (A Xylem Brand)

4.2.4. SUEZ Water Technologies & Solutions

4.2.5. Veolia Water Technologies

4.2.6. Toray Industries, Inc.

5. Membrane System Retrofitting and Upgrades Market – Segmentation Insights (2025–2034)

5.1. By Service Type

5.1.1. Module Replacement & Upgrades: Largest Segment (35% Share)

5.1.2. Energy Efficiency Upgrades: Fastest Growing Segment (15% Share)

5.1.3. Automation & Control Retrofits

5.1.4. Other Services (Optimization, Pre-treatment Integration, etc.)

5.2. By Membrane Type

5.2.1. Reverse Osmosis (RO): Largest Segment (50% Share)

5.2.2. Ultrafiltration (UF) and Microfiltration (MF)

5.2.3. Nanofiltration (NF)

5.2.4. Other Membranes (FO, ED)

5.3. By Application

5.3.1. Water & Wastewater Treatment: Largest Segment (40% Share)

5.3.2. Desalination

5.3.3. Industrial Processing

5.3.4. Power Generation

5.4. By End-Use Industry

5.4.1. Municipal & Utility Operators: Largest Segment (45% Share)

5.4.2. Industrial Sector: Fastest Adopting Segment (40% Share)

5.4.3. Commercial Buildings and Residential

6. Country Analysis and Outlook: Membrane System Retrofitting and Upgrades Market

6.1. United States: Federal Funding and Cutting-Edge Membrane Retrofits Transform Water Infrastructure

6.2. China: Policy-Driven Retrofits and Advanced Modular Membrane Systems

6.3. India: Government Missions and Infrastructure Investments Fuel Membrane Upgrades

6.4. Germany: Industrial Wastewater Leadership and Innovative Retrofit Solutions

6.5. Japan: High-Efficiency MBR Modules and Strategic Government Support for Upgrades

6.6. Saudi Arabia: Strategic Desalination Retrofits and Energy-Efficient Membrane Adoption

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Membrane System Retrofitting and Upgrades Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Service Type

7.1.2. By Membrane Type

7.1.3. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Service Type

7.2.2. By Membrane Type

7.2.3. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Service Type

7.3.2. By Membrane Type

7.3.3. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Service Type

7.4.2. By Membrane Type

7.4.3. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Service Type

7.5.2. By Membrane Type

7.5.3. By Application

8. Company Profiles: Leading Players in Membrane System Retrofitting and Upgrades Market

8.1. DuPont de Nemours, Inc.

8.2. Toray Industries, Inc.

8.3. SUEZ

8.4. Veolia

8.5. Pentair plc

8.6. Xylem Inc.

8.7. The Dow Chemical Company

8.8. Koch Industries

8.9. LG Chem

8.10. Evoqua Water Technologies

8.11. MANN+HUMMEL

8.12. Aquatech International

8.13. Kubota Corporation

8.14. Kuraray Co., Ltd.

8.15. Mitsubishi Chemical Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures