Market Overview: Strong Growth Driven by Industrial Wastewater, ZLD Systems, and Advanced Ceramic Materials

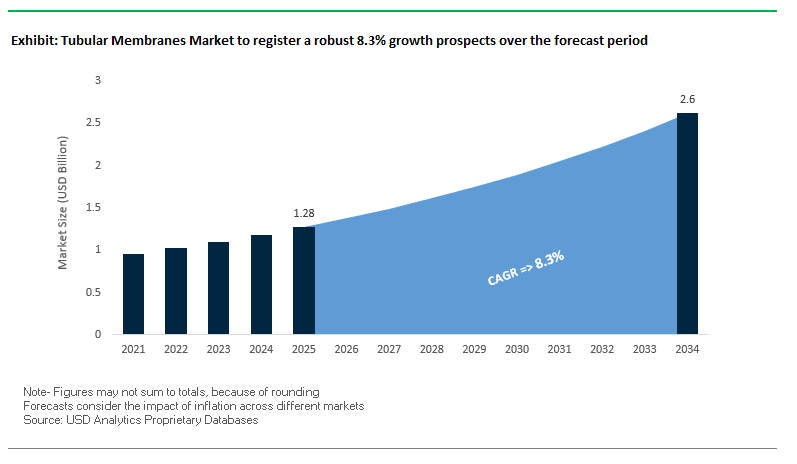

The tubular membranes market is set to expand significantly, growing from USD 1.28 billion in 2025 to USD 2.6 billion by 2034, registering a CAGR of 8.3%. This rapid growth is being propelled by the rising demand for efficient wastewater treatment technologies, increasing adoption of Zero Liquid Discharge (ZLD) systems, and the shift toward ceramic and reinforced polymer membranes for industrial applications. Unlike spiral-wound or hollow-fiber membranes, tubular membranes are engineered to handle high concentrations of suspended solids, oils, and grease, making them indispensable in industries such as food & beverage, textiles, oil & gas, and chemicals. Their robust design, high resistance to chemical and thermal stress, and long operational lifespan further strengthen their value proposition in sectors where downtime and frequent replacements lead to operational inefficiencies.

Key Insights for Industry Stakeholders

- Handling High-Solids Feed: Tubular membranes are optimized for high fouling feeds such as oils, greases, and viscous fluids, ensuring superior operational reliability in complex wastewater streams.

- Extended Lifespan: Constructed with ceramics or reinforced polymers, tubular membranes provide higher durability compared to conventional membrane technologies, reducing replacement frequency.

- Chemical & Thermal Stability: Their resilience against harsh cleaning agents and elevated temperatures makes them suitable for high-demand industrial applications.

- Enabler of ZLD Systems: Tubular membranes are a core technology for ZLD, helping industries comply with strict environmental mandates while enabling water reuse and resource recovery.

Market Analysis: Recent Developments Reshaping Industrial Water Treatment

The tubular membranes industry has entered a new growth phase, marked by innovations in ceramic and polymeric materials, mergers, and integration with advanced water treatment systems. A clear trend is the use of tubular membranes in emerging contaminant removal, as highlighted in August 2025, where new research demonstrated their effectiveness in filtering micro-pollutants a critical capability as governments enforce stricter discharge and reuse standards. Similarly, July 2025 saw Meiden Singapore, a subsidiary of Meidensha Corporation, deploy large-scale ceramic flat-sheet membranes in seawater reverse osmosis pre-treatment, reinforcing Singapore’s role as a leader in desalination efficiency.

Corporate consolidations are also shaping the market. In June 2025, Nanostone Water and Solecta merged to form Acuriant Technologies, combining ceramic and polymer expertise to tackle advanced separation challenges. Just a month earlier, in May 2025, Memsift Innovations, backed by India’s Murugappa Group, launched the GOSEP™ Ultrafiltration Membrane, a tubular membrane engineered for aggressive chemical resistance and longer life, representing a breakthrough for industries needing durability under extreme process conditions.

Further research-driven enhancements are improving the efficiency and stability of tubular membranes. An April 2025 scientific study introduced electrostatic air spray deposition to improve nanofiltration composite membranes, offering higher flux and stability. Meanwhile, LiqTech International, in February 2025, supplied a new pilot unit to a U.S. steel producer for oily wastewater treatment opening a new end-market opportunity for SiC-based tubular membranes. Looking back, Meiden Singapore’s collaboration with PUB in June 2024 to enhance desalination efficiency and Saint-Gobain’s April 2024 launch of upgraded SiC membranes with 15% higher flux are key milestones that continue to set industry benchmarks. These developments collectively reflect a market transitioning from traditional wastewater management toward high-performance, sustainable, and regulation-compliant solutions.

Key Trends Shaping the Tubular Membranes Market

Specialization in High-Solids and Oily Wastewater Treatment

One of the most significant trends driving the tubular membranes market is their specialization in treating complex wastewater streams that contain high levels of suspended solids, oils, and greases. Unlike conventional spiral-wound or hollow-fiber membranes, tubular membranes feature wide channels and cross-flow operation that resist fouling and maintain long-term performance even under extreme loading conditions. This makes them a preferred choice in industries such as metal finishing, food processing, and textiles, where effluents are particularly challenging. A case study by Berghof Membranes demonstrated that a tubular ultrafiltration system deployed at a metal finishing plant achieved recoveries of more than 95%, while successfully reducing heavy metal concentrations to below 0.1 mg/L and achieving turbidity levels under 1 NTU. Such results underscore the growing reliance on tubular membranes as industries face mounting regulatory pressure to manage highly polluted effluents. This trend not only positions tubular membranes as a technology of last resort for complex streams but also strengthens their role in industries prioritizing compliance with stricter discharge norms.

Advancements in Materials and Module Design for Durability

Another defining trend is the rapid technological innovation in membrane materials and designs, aimed at extending operational life and lowering total cost of ownership. Manufacturers are increasingly investing in ceramic tubular membranes, which offer unparalleled chemical, thermal, and mechanical resistance, making them suitable for aggressive chemical effluents and high-temperature operations. At the same time, polymeric tubular membranes made from PVDF, PES, and PTFE are being enhanced with nanomaterials and anti-fouling coatings to minimize cleaning frequency and reduce maintenance costs. Research published in ACS Applied Materials & Interfaces highlights the potential of nanostructured surfaces to create self-cleaning and fouling-resistant properties. Furthermore, pilot-scale studies in automotive and car wash wastewater treatment show that polymeric tubular ultrafiltration membranes can be cyclically cleaned without significant long-term degradation, demonstrating their resilience. These advancements are reshaping the market by making tubular membranes not only robust for extreme conditions but also more economically viable, widening their adoption in industries that were previously hesitant due to high upfront costs.

Essential Role in Zero Liquid Discharge (ZLD) Systems

One of the most promising opportunities lies in the integration of tubular membranes into Zero Liquid Discharge (ZLD) systems, which are becoming increasingly common in water-stressed regions and industries with strict effluent mandates. Tubular membranes act as a pre-concentration step, significantly reducing the wastewater volume that must be processed by more energy-intensive thermal evaporators. This not only lowers operating costs but also makes ZLD systems economically feasible for a broader range of industries. The U.S. Environmental Protection Agency (EPA) has been tightening effluent guidelines for sectors such as power generation and chemicals, effectively forcing companies to adopt ZLD practices. Tubular membranes, by enabling high recovery rates in streams containing oils, greases, and high solids, are emerging as a cornerstone technology for regulatory compliance and water reuse. With global water scarcity driving stricter governance, the opportunity for tubular membranes in ZLD applications is expected to expand sharply.

Resource Recovery and the Circular Economy

Another major opportunity comes from the increasing focus on resource recovery and circular economy initiatives. Tubular membranes are uniquely suited to reclaim valuable metals, nutrients, and chemicals from process streams that would otherwise be discarded. For instance, in the mining and metal finishing industries, tubular ultrafiltration and nanofiltration systems are being used to recover precious metals from effluents, reducing both environmental impact and raw material costs. In the food and beverage sector, tubular membranes enable the recovery of proteins and sugars from by-product streams, creating additional revenue opportunities. A growing number of companies are aligning with global sustainability frameworks by investing in circular economy projects, and tubular membranes are positioned as an enabling technology. This creates a high-value opportunity for suppliers to market tubular membranes not only as a compliance tool but also as a profit-generating asset that transforms waste into reusable inputs.

Market Share Analysis of the Tubular Membranes Market

Market Share by Type

Ceramic tubular membranes are projected to dominate the market with about 60% share by 2025, reflecting their unmatched resistance to extreme pH, thermal shocks, and aggressive cleaning chemicals. Their durability makes them indispensable in industries like chemicals, petrochemicals, and mining, where conditions would rapidly degrade polymeric alternatives. Despite the higher capital cost, their long operational life provides favorable lifecycle economics. On the other hand, polymeric tubular membranes will hold a substantial 40% share, particularly in food & beverage and textile wastewater treatment, where the operating conditions are less aggressive and cost sensitivity is higher. Polymeric variants made from PVDF, PES, or PTFE remain an attractive choice due to lower upfront costs and their effectiveness in handling oily, fatty, and organic-laden streams.

Market Share by Technology

Ultrafiltration (UF) will account for the largest share at about 65% of the market, establishing itself as the workhorse technology for tubular membranes. Its pore size makes it highly effective for removing emulsified oils, viruses, and colloids, enabling industries to meet stringent discharge norms and achieve product recovery. Microfiltration (MF), with an estimated 25% share, plays a complementary role in clarification and pre-treatment, removing larger particles and bacteria ahead of UF or reverse osmosis processes. Although smaller in share at around 10%, nanofiltration (NF) holds a niche yet growing position. It is increasingly used in divalent ion and organic molecule removal from highly fouling streams, where spiral-wound NF membranes are not feasible. This diversity across technologies highlights the adaptability of tubular membranes across a spectrum of industrial needs.

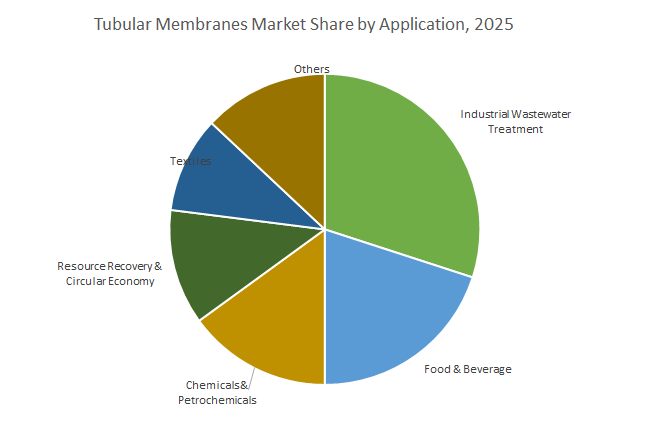

Market Share by Application

Industrial wastewater treatment is the largest application segment, expected to contribute 30% of market share by 2025. The increasing need to comply with stricter effluent discharge norms and ZLD mandates makes tubular membranes essential for treating high-strength, high-solids industrial wastewater. The food & beverage sector follows with a 20% share, leveraging tubular membranes for protein recovery from whey, juice clarification, and wastewater treatment, where cleanability and hygiene are critical. Chemicals and petrochemicals will represent around 15% share, heavily relying on ceramic membranes for catalyst recovery and aggressive solvent purification.

A particularly fast-growing application is resource recovery and circular economy initiatives, contributing 12% share. Tubular membranes play a transformative role in recovering metals, chemicals, and reusable water, aligning with global sustainability agendas. The textiles industry holds 10% share, employing tubular UF and NF membranes for dye and chemical removal, enabling water reuse and reducing environmental footprint. The remaining 13% of applications span energy, pharma, and leather industries, where tubular membranes support specialized uses like flue gas desulfurization wastewater treatment, viscous process stream handling, and tanning solution recovery, further demonstrating the wide applicability of this technology across industries.

China: Driving Industrial ZLD Systems with Advanced Tubular Membranes

China’s tubular membranes market is experiencing rapid growth due to stringent environmental regulations and a strong focus on industrial wastewater management. The Ministry of Ecology and Environment (MEE) enforces strict wastewater discharge standards, compelling industries to adopt tubular membrane systems to comply with emission norms. In 2024, Chinese researchers developed hollow-fiber ultrafiltration membranes with enhanced antifouling properties, which are integrated into multi-stage treatment systems that include tubular membranes to ensure high-quality water output. Key applications are in zero-liquid discharge (ZLD) systems for textiles and petrochemicals, where tubular membranes are valued for their robustness and ability to handle high-solids-content wastewater, driving adoption in both industrial and municipal wastewater treatment sectors.

United States: Government-Funded Innovation and Corporate Initiatives

The U.S. tubular membranes market benefits from substantial government funding and advanced R&D initiatives. Under the Bipartisan Infrastructure Law, over $50 billion is allocated to the EPA to enhance water infrastructure and address emerging contaminants like PFAS, emphasizing the need for high-performance tubular membrane filtration technologies. NSF-funded research centers are advancing water purification, chemical separations, and biopharmaceutical membrane technologies, creating a strong innovation ecosystem. Industry leaders like Pentair and Koch Separation Solutions are developing next-generation tubular membranes, such as the INDU-COR HD high-density tubular membrane, providing space-saving solutions and improved filtration efficiency for industrial and biopharmaceutical applications.

India: Green Bonds and Expanding Tubular Membrane Infrastructure

India’s tubular membranes market is gaining momentum through government initiatives and infrastructure investments. Programs like the “Jal Jeevan Mission” and the Department of Science & Technology’s Water Technology Initiative promote research in nano-material and filtration technologies to provide safe drinking water in rural areas. The Ghaziabad Nagar Nigam’s issuance of India’s first Certified Green Municipal Bond raised ₹150 crore for a Tertiary Sewage Treatment Plant (TSTP) utilizing tubular membranes for industrial wastewater reuse. Additionally, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant, valued at INR 415 crores, highlights significant investments in tubular membrane-based water treatment infrastructure.

Germany: Industrial Expertise and Global Tubular Membrane Projects

Germany remains a global leader in tubular membrane applications for industrial wastewater treatment. PWT Wassertechnik specializes in tubular membrane processes to treat and reuse water for industrial applications, ensuring compliance with European environmental regulations. In 2024, Berghof Membranes announced the deployment of ceramic tubular membranes for MBR projects across multiple continents, ranging from 250 m³/d industrial to 10,000 m³/d municipal systems. Companies like MANN+HUMMEL are developing innovative membrane and digital solutions for industrial processes and green energy applications, further strengthening Germany’s position as a hub for advanced tubular membrane technologies.

Japan: Academic Research and Large-Scale MBR Applications

Japan is at the forefront of tubular membrane innovation, combining academic research with corporate expertise. Studies by Kobe University’s Membrane Engineering Group in 2024 focus on developing novel functional membranes, including biomimetic and highly porous designs. Toray Industries has contributed high-performance reverse osmosis (RO) membranes for large-scale desalination projects in Saudi Arabia, while Metawater’s ceramic tubular membrane systems are deployed across over 3,000 full-scale MBR applications, ranging from industrial/household wastewater to municipal treatment plants. These deployments highlight Japan’s role in driving both technological innovation and global market adoption of tubular membranes.

Saudi Arabia: Expanding Desalination with Tubular Membrane Technology

Saudi Arabia is a global leader in desalination, heavily investing in reverse osmosis (RO) technology with a strategic focus on tubular membrane systems. The ACWA Power-led Jubail 3A desalination plant, an independent water project (IWP), produces 600,000 cubic meters of freshwater per day using RO technology. The Saline Water Conversion Corporation (SWCC) is pioneering energy-efficient RO membranes, exemplified by the Yanbu 4 desalination plant producing 450,000 cubic meters of freshwater per day. With the Saudi Water Partnership Company (SWPC) continuously launching new membrane-based desalination projects, tubular membranes are strategically positioned to support the Kingdom’s sustainable water development goals.

Competitive Landscape: Leading Companies Driving Tubular Membrane Innovation

The global tubular membranes market is highly competitive, with innovation driven by both established leaders and specialized technology providers. The competitive environment is characterized by a mix of ceramic specialists, polymer membrane manufacturers, and integrated water treatment solution providers, each leveraging material science expertise, project execution capabilities, and global reach to strengthen market presence.

Saint-Gobain – Leadership in Silicon Carbide Tubular Membranes

Saint-Gobain leverages its unmatched expertise in advanced ceramics to dominate the SiC tubular membrane segment. Its products are renowned for high fouling resistance, superior chemical durability, and robust performance in extreme industrial environments. In April 2024, the company introduced an upgraded SiC membrane line with a 15% improved flux rate, reflecting its ongoing commitment to performance improvements. Widely used in semiconductors, pharmaceuticals, and food & beverage industries, Saint-Gobain’s products are supported by a distribution network spanning over 70 countries, reinforcing its global leadership.

LiqTech International – Expanding End-Market Opportunities with SiC Solutions

LiqTech International is a recognized innovator specializing in silicon carbide membrane technologies. Its SiC tubular membranes are valued for unmatched chemical and thermal resistance, enabling effective treatment of oily wastewater, marine discharges, and harsh industrial effluents. In February 2025, the company delivered a new pilot unit for a U.S. steel producer, showcasing its diversification into new industrial markets. LiqTech reported an 11% revenue increase in Q2 2025, highlighting its operational momentum and strong growth trajectory as it expands beyond traditional markets into steel and heavy industries.

Koch Separation Solutions (KSS) – Engineering Custom High-Density Tubular Membranes

Now operating as Kovalus Separation Solutions, Koch Separation Solutions continues to expand its portfolio of tubular membranes with its INDU-COR HD technology launched in April 2021. This innovation increased membrane packing density, delivering cost and space savings for industrial users. Known for customized solutions, KSS serves industries such as food & beverage, automotive, and life sciences, where complex wastewater and process challenges demand precision-engineered separation. Its high-purity water applications and long-lifetime membranes reinforce Koch’s positioning as a technology-driven player in advanced separation systems.

Berghof Membrane Technology GmbH – Industrial Wastewater Specialist

Berghof, a German leader in industrial wastewater treatment membranes, has carved its niche with tubular modules capable of managing high solids and oil-laden effluents. Its solutions are widely adopted in automotive, food & beverage, and chemical sectors, thanks to decades of proven expertise. Berghof emphasizes sustainability and water reuse, aligning its products with global sustainability mandates. Its strong international footprint underpins its reputation as a reliable provider of robust and eco-conscious tubular membrane systems.

Ovivo – Strengthening Position through Strategic Acquisitions

Ovivo, with operations across 18 countries and over 1,500 water treatment experts, is a prominent player with an integrated global platform. The company’s 2021 acquisition of Cembrane, a SiC flat-sheet membrane specialist, strengthened its position in the broader membrane market. While Ovivo’s focus extends beyond tubular membranes, its strong industrial wastewater, semiconductor, and mining applications demonstrate its versatility. By integrating proprietary technologies with advanced system engineering, Ovivo continues to deliver holistic water treatment solutions, ensuring its competitiveness in the tubular membranes sector.

Tubular Membranes Market Report Scope

Tubular Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.28 Billion

|

|

Market Size (2034)

|

$2.6 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By Type (Ceramic Tubular Membranes, Polymeric Tubular Membranes), By Technology (Microfiltration, Ultrafiltration, Nanofiltration), By Application (Industrial Wastewater Treatment, Energy & Power, Chemicals & Petrochemicals, Pharmaceuticals, Textiles, Leather, Food & Beverage, Resource Recovery & Circular Economy)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., SUEZ, Veolia, Toray Industries, Inc., Pentair plc, Xylem Inc., Asahi Kasei Corporation, Kubota Corporation, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, LG Chem, Koch Industries, Berghof Membranes, V.A. TECH WABAG Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tubular Membranes Market Segmentation

By Type

- Ceramic Tubular Membranes

- Polymeric Tubular Membranes

By Technology

- Microfiltration

- Ultrafiltration

- Nanofiltration

By Application

- Industrial Wastewater Treatment

- Energy & Power

- Chemicals & Petrochemicals

- Pharmaceuticals

- Textiles

- Leather

- Food & Beverage

- Resource Recovery & Circular Economy

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Tubular Membranes Industry include-

- DuPont de Nemours, Inc.

- SUEZ

- Veolia

- Toray Industries, Inc.

- Pentair plc

- Xylem Inc.

- Asahi Kasei Corporation

- Kubota Corporation

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- LG Chem

- Koch Industries

- Berghof Membranes

- V.A. TECH WABAG Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the global Tubular Membranes Market across high-solids industrial wastewater, ZLD pre-concentration, and resource-recovery use cases; the analysis reviews duty-condition performance (oils/grease/viscous feeds), compares ceramic versus reinforced-polymer economics, and highlights supplier moves in packing density, anti-fouling surfaces, and cassette/module redesign that shift lifetime OPEX. Developed by USDAnalytics, it maps adoption inflection points by industry, pressure class, and effluent complexity, quantifies retrofit pathways for space-constrained plants, and benchmarks KPIs that matter to operators (flux stability, CIP windows, kWh/m³, recovery). With granular sizing, risk scoring, and scenario tests, this report is an essential resource for utilities, EPCs, plant owners, and OEMs that need defensible forecasts and procurement guidance across 2025–2034. Scope Includes-

- Segmentation – By Type: Ceramic Tubular Membranes; Polymeric Tubular Membranes | By Technology: Microfiltration; Ultrafiltration; Nanofiltration | By Application: Industrial Wastewater Treatment; Energy & Power; Chemicals & Petrochemicals; Pharmaceuticals; Textiles; Leather; Food & Beverage; Resource Recovery & Circular Economy

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic 2021–2024; Forecast 2025–2034.

- Companies (Profiles of 15+ firms): DuPont de Nemours, Inc.; SUEZ; Veolia; Toray Industries, Inc.; Pentair plc; Xylem Inc.; Asahi Kasei Corporation; Kubota Corporation; The Dow Chemical Company; MANN+HUMMEL; Evoqua Water Technologies; LG Chem; Koch Industries; Berghof Membranes; V.A. TECH WABAG Ltd.

Methodology

USDAnalytics applies a hybrid top-down/bottom-up approach: top-down TAM by end-market capex and regulatory drivers; bottom-up plant-level models built from installed base, module counts, membrane area, flux/TMP curves, cleaning frequency, chemical/energy usage, and replacement cycles to derive $/1,000 m³ and TCO. We triangulate vendor disclosures, tender databases, pilot/commissioning data, and 60+ expert interviews (operators, OEMs, EPCs) to validate duty conditions for oily/high-TSS feeds. Competitive benchmarking normalizes ceramics vs. polymers on permeability recovery, chemical/thermal tolerance, warranty terms, and packing density. Scenario analysis covers ceramic cost-learning, ZLD mandates, and consumables inflation; sensitivity testing quantifies impacts of fouling load, CIP set-points, and recovery targets on EBITDA/NPV to 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Tubular Membranes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

2. Tubular Membranes Market Outlook (2025–2034)

2.1. Market Overview: Growth Driven by Industrial Wastewater, ZLD, and Advanced Materials

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): USD 1.28 Billion

2.2.2. Forecasted Market Size (2034): USD 2.6 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 8.3%

2.3. Key Trends and Opportunities

2.3.1. Specialization in High-Solids and Oily Wastewater Treatment

2.3.2. Advancements in Materials and Module Design for Durability

2.3.3. Essential Role in Zero Liquid Discharge (ZLD) Systems

2.3.4. Resource Recovery and the Circular Economy

3. Recent Developments Reshaping the Market

3.1. Market Analysis: Recent Innovations and Strategic Activities

3.1.1. Nanostone Water and Solecta Merge to Form Acuriant Technologies (June 2025)

3.1.2. Memsift Innovations Launches GOSEP™ Ultrafiltration Membrane (May 2025)

3.1.3. LiqTech International Supplies Pilot Unit for U.S. Steel Producer (February 2025)

3.1.4. Meiden Singapore Collaborates with PUB to Enhance Desalination Efficiency (June 2024)

3.1.5. Saint-Gobain Launches Upgraded SiC Membranes (April 2024)

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Material Specialists to Integrated Solution Providers

4.2. Key Competitive Factors

4.2.1. Expertise in Material Science and Application-Specific Solutions

4.2.2. Project Execution and Global Reach

4.2.3. Focus on Durability and Lower Total Cost of Ownership

4.3. Profiles of Leading Players

4.3.1. Saint-Gobain

4.3.2. LiqTech International

4.3.3. Koch Separation Solutions (KSS)

4.3.4. Berghof Membrane Technology GmbH

4.3.5. Ovivo

5. Tubular Membranes Market – Segmentation Insights

5.1. By Type

5.1.1. Ceramic Tubular Membranes

5.1.2. Polymeric Tubular Membranes

5.2. By Technology

5.2.1. Ultrafiltration (UF)

5.2.2. Microfiltration (MF)

5.2.3. Nanofiltration (NF)

5.3. By Application

5.3.1. Industrial Wastewater Treatment

5.3.2. Food & Beverage

5.3.3. Chemicals & Petrochemicals

5.3.4. Resource Recovery & Circular Economy

5.3.5. Textiles, Leather, and Other Industrial Applications

6. Country Analysis and Outlook: Tubular Membranes Market

6.1. China: Driving Industrial ZLD Systems with Advanced Membranes

6.2. United States: Government-Funded Innovation and Corporate Initiatives

6.3. India: Green Bonds and Expanding Membrane Infrastructure

6.4. Germany: Industrial Expertise and Global Projects

6.5. Japan: Academic Research and Large-Scale Applications

6.6. Saudi Arabia: Expanding Desalination with Tubular Membrane Technology

6.7. Other Key Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Tubular Membranes Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Technology

7.1.3. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Technology

7.2.3. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Technology

7.3.3. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Technology

7.4.3. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Technology

7.5.3. By Application

8. Company Profiles: Additional Leading Players

8.1. DuPont de Nemours, Inc.

8.2. SUEZ

8.3. Veolia

8.4. Toray Industries, Inc.

8.5. Pentair plc

8.6. Xylem Inc.

8.7. Asahi Kasei Corporation

8.8. Kubota Corporation

8.9. The Dow Chemical Company

8.10. MANN+HUMMEL

8.11. Evoqua Water Technologies

8.12. LG Chem

8.13. Koch Industries

8.14. Berghof Membranes

8.15. V.A. TECH WABAG Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures