Market Overview: Expanding Role of Membrane Desalination in Global Water Security

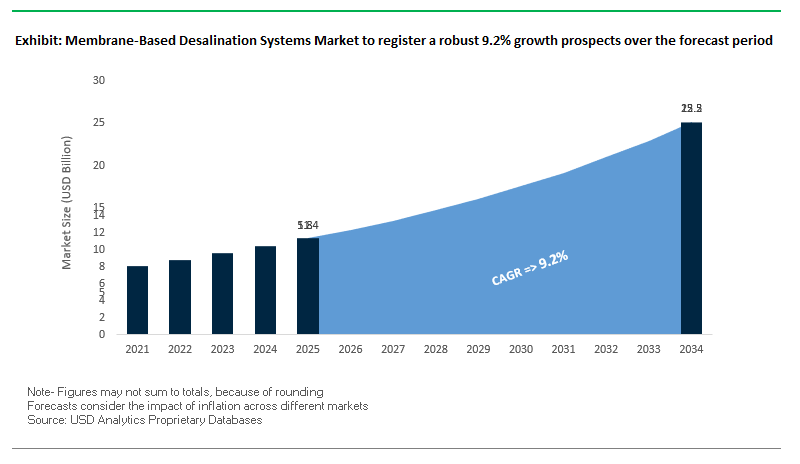

The Membrane-Based Desalination Systems Market is witnessing robust growth, projected to expand from $11.4 billion in 2025 to $25.2 billion by 2034, registering a CAGR of 9.2%. This growth reflects the increasing dependence on seawater and brackish water desalination technologies as a sustainable response to climate change-driven water scarcity, population growth, and urbanization.

The industry’s core lies in reverse osmosis (RO) desalination systems, which dominate due to superior energy efficiency compared to thermal processes. Governments, utilities, and industrial players are scaling investments to secure long-term freshwater supplies, with the Middle East & Africa leading in installed desalination capacity.

Key Market Insights for Stakeholders:

- Seawater desalination dominates installed capacity, followed by brackish water treatment.

- Reverse Osmosis technology commands over 60% market share, making it the most widely adopted desalination process.

- Middle East & Africa leads globally, with Saudi Arabia and UAE driving large-scale seawater desalination investments.

- As of February 2020, more than 21,000 desalination plants worldwide were in operation or under construction, producing 114.9 million m³/day of freshwater.

Market Analysis: Recent News and Strategic Developments in Membrane Desalination

The membrane desalination industry has entered a new phase defined by sustainability, large-scale capacity expansion, and digital integration. Recent developments demonstrate strong momentum across the Middle East, Asia-Pacific, and Latin America.

In July 2025, VA Tech Wabag secured a landmark $280 million contract from the Saudi Water Authority to construct a 300 MLD seawater desalination plant at Yanbu, reinforcing its dominance in the Middle Eastern water infrastructure market. During the same month, Toray Industries supplied its advanced RO membranes for the Shuaibah 3 IWP desalination plant in Saudi Arabia. This project, powered by solar energy, represents one of the largest eco-friendly desalination plants globally, with 600,000 m³/day capacity.

The innovation wave extends to offshore energy and industrial sectors. In June 2025, Veolia Water Technologies won a multi-million dollar contract from Seatrium to provide desalination systems for two FPSO platforms in Brazil’s Santos Basin, showcasing the adoption of membrane desalination in offshore oil & gas. In the same month, Toray established a Water Treatment Technology Center in Saudi Arabia to strengthen technical support and expand market share across the Middle East and Africa.

Earlier, in April 2025, Veolia announced plans to double its operated desalination capacity by 2030, reinforcing its position as a leader in sustainable desalination solutions. Meanwhile, SUEZ expanded its footprint in Asia-Pacific, with two projects in 2024: a SWRO plant in Metro Iloilo, Philippines (October 2024) and the largest industrial membrane desalination plant in China (August 2024), designed to supply Wanhua Chemical. Additionally, in October 2024, Veolia partnered with the Kingdom of Morocco to build a renewable-powered 822,000 m³/day plant near Rabat.

Key Trends Shaping the Membrane-Based Desalination Systems Market

Surge of Mega-Projects in Water-Stressed Regions

The membrane-based desalination systems market is being redefined by the rapid rise of large-scale projects in the Middle East and North Africa (MENA), the most water-stressed region globally. According to the World Bank, by 2050, 100% of the MENA population will face extreme water stress, driving governments to commit over $100 billion in desalination investments by 2030. For example, the Saudi Water Authority (SWA) recently awarded two strategic projects, underscoring the Kingdom’s long-term reliance on desalination to secure water supply. Such mega-projects not only expand installed capacity but also reinforce desalination’s role as the backbone of national water security strategies in arid regions.

Rising Corporate Investments and Technological Advancements

Another critical trend is the influx of corporate investment in next-generation membrane technologies aimed at enhancing efficiency and cutting operational costs. Companies like ACWA Power reported record growth in 2025, signing two Water Purchase Agreements (WPAs) that will add 700,000 m³/day of new capacity while raising over SAR 7 billion in capital, reflecting investor confidence in desalination growth. These investments directly fuel advancements such as high-recovery RO membranes, optimized pre-treatment modules, and energy-efficient system configurations, making desalination more cost-competitive and scalable.

Transition Toward Renewable-Energy Powered Desalination

With traditional desalination consuming 3–5 kWh/m³, energy use has long been its Achilles’ heel. The market is now witnessing a decisive shift toward solar-powered desalination systems, integrating renewable energy with advanced reverse osmosis (RO). A landmark example is Veolia’s $320 million Hassyan desalination plant in Dubai, which will be the world’s largest solar-powered desalination facility. With an energy demand of just 2.9 kWh/m³ 35% lower than the industry average from the last decade this project highlights how renewable-powered desalination is becoming integral to sustainable water infrastructure worldwide.

Breakthrough Innovations in Anti-Fouling and Self-Cleaning Membranes

Fouling remains one of the costliest challenges in reverse osmosis desalination, leading to higher chemical usage and downtime. To counter this, manufacturers are commercializing nanocomposite membranes enhanced with graphene and carbon nanotubes. Research published in Water Research and ResearchGate shows these membranes exhibit superior permeability and anti-fouling resistance, extending lifespan and reducing operating costs. Additionally, startups such as Active Membranes are pioneering electrically conducting membranes that actively prevent scaling an innovation that earned global recognition from the Kingdom of Saudi Arabia. Such technological advances are pivotal in lowering lifecycle costs and expanding the adoption of membrane-based desalination systems.

Opportunities Accelerating the Membrane-Based Desalination Systems Market

Expansion of Industrial Wastewater Reuse

The industrial wastewater reuse segment presents one of the most lucrative opportunities for membrane-based desalination systems. Increasing enforcement of Zero Liquid Discharge (ZLD) and Minimal Liquid Discharge (MLD) regulations is compelling industries such as chemicals, oil & gas, and power generation to integrate RO and hybrid membranes into their treatment facilities. By recycling process water, industries not only cut freshwater withdrawals but also reduce discharge penalties, turning compliance into a cost-saving strategy.

Growth of Modular and Decentralized Desalination Plants

Beyond mega-projects, there is growing demand for modular, containerized membrane desalination systems in remote locations, resorts, and off-grid industries. These decentralized solutions are gaining traction due to their lower upfront investment, scalability, and rapid deployment, making them highly attractive in regions where infrastructure development lags behind demand. As technology costs decline, modular RO systems are expected to play a central role in expanding water access globally.

Market Share Analysis of the Membrane-Based Desalination Systems Market

Market Share by Technology

Reverse Osmosis (RO) continues to dominate the membrane-based desalination systems market, accounting for an estimated 75% share by 2025. RO remains the only membrane process capable of large-scale seawater desalination, supported by ongoing breakthroughs in energy recovery devices and advanced membrane chemistry. Hybrid membrane systems hold 12%, largely as UF/MF + RO or NF + RO combinations, which improve RO efficiency by mitigating fouling. Ultrafiltration (UF) and Microfiltration (MF), while unable to desalinate independently, represent 8%, reflecting their essential role in pre-treatment. Nanofiltration (NF), with a smaller 5% share, remains valuable for brackish water softening and selective ion separation where energy efficiency is critical.

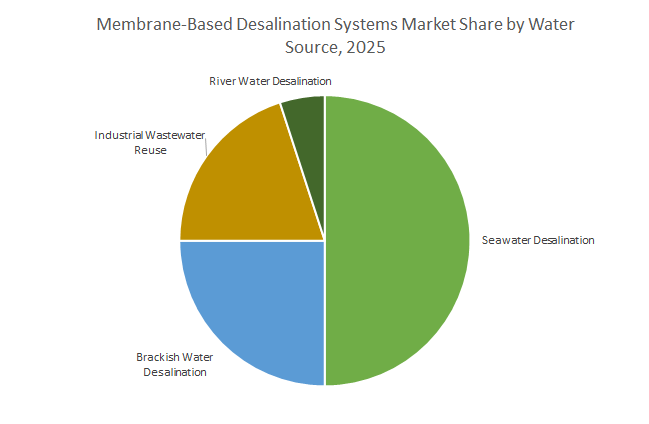

Market Share by Water Source

By feedwater source, seawater desalination represents the largest segment with 50% of the market in 2025, primarily concentrated in arid coastal regions such as the Middle East, California, and Australia. Brackish water desalination follows with 25%, benefiting from lower salinity and energy requirements, making it more widespread for inland municipalities and agriculture. Industrial wastewater reuse is projected to capture 20%, driven by the circular economy and ZLD adoption, making it the fastest-growing segment. Meanwhile, river water desalination holds a smaller 5% share, used mainly in rivers impacted by saltwater intrusion or high natural salinity.

Market Share by Application

From an application perspective, municipal water supply dominates with an estimated 60% share in 2025, as governments and utilities prioritize desalination to meet population growth and urban water security needs. Industrial process water accounts for 30%, serving power plants, chemical refineries, and food & beverage industries that demand uninterrupted access to high-purity water. The remaining 10% includes specialized applications such as agriculture (high-value crops), power generation cooling, military bases, and hospitality, where desalination ensures resilience against freshwater scarcity.

Saudi Arabia: Strategic Investments Positioning the Kingdom as a Global RO Leader

Saudi Arabia continues to strengthen its position as a global leader in membrane-based desalination, largely driven by substantial infrastructure investments and a government-backed shift from thermal to energy-efficient reverse osmosis (RO) technologies. ACWA Power’s Jubail 3A desalination plant, an independent water project (IWP), exemplifies this trend by producing 600,000 cubic meters of freshwater daily using advanced RO membranes. The Saline Water Conversion Corporation (SWCC) has also pioneered energy-efficient RO solutions, with the Yanbu 4 plant delivering 450,000 cubic meters per day while reducing operational energy consumption. Government policy through the Saudi Water Partnership Company (SWPC) emphasizes the construction of new RO membrane production facilities, including the Middle East’s first plant with a capacity of 254,000 membranes per year, set to start in 2025. Beyond municipal water supply, RO membranes are increasingly used for industrial applications and to meet the high water demand during Hajj and Umrah seasons, showcasing Saudi Arabia’s strategic focus on sustainable, membrane-based desalination solutions.

China: Regulatory Support and Technological Innovations Driving Membrane Desalination Growth

China is rapidly expanding its membrane-based desalination capacity, guided by regulatory initiatives and technological advancements. The government’s “14th Five-Year Plan” (2021–2025) targets seawater desalination as a key strategy to mitigate water scarcity, aiming for 3.5 million cubic meters per day by 2025. Technological innovations such as AI-driven RO membranes at the Qingdao Baifa Desalination Facility optimize pressure settings and predict membrane fouling, cutting operational costs by 15%. Significant industrial projects are also underway, including SUEZ’s membrane-based seawater desalination plant in Shandong Province for Wanhua Chemical, which leverages thermal drainage from adjacent power plants to reduce energy usage. While these projects primarily support industrial applications in coastal provinces, the government is promoting desalinated water integration into municipal supplies, demonstrating a dual focus on industrial efficiency and urban water sustainability.

United States: Government and Corporate Initiatives Advancing Energy-Efficient Desalination

The United States maintains a competitive edge in membrane-based desalination through strong government funding, academic research, and corporate deployment of advanced RO technologies. The Bureau of Reclamation’s Desalination and Water Purification Research program allocated over $1.9 million in 2024 to eight projects focused on energy-efficient and cost-effective desalination solutions. Public-private partnerships such as the National Alliance for Water Innovation (NAWI) are pioneering innovations in membranes for waste-brine treatment and renewable-powered desalination systems. Corporations in the U.S. are deploying advanced RO membrane systems to tackle emerging contaminants like PFAS, in alignment with the government’s Bipartisan Infrastructure Law. These initiatives collectively accelerate the adoption of membrane-based desalination technologies for municipal and industrial water applications while emphasizing sustainability and operational efficiency.

Japan: Technological Expertise Supporting Global Membrane Desalination Projects

Japan is recognized as a global technology provider in membrane-based desalination, driven by corporate innovation and government support. Toray Industries, a leader in membrane technology, supplies advanced RO membranes for next-generation desalination plants, including projects in Saudi Arabia converting conventional evaporation facilities into eco-friendly setups. The Japanese government’s 2024 allocation of USD 1.2 billion promotes sustainable infrastructure, including wastewater treatment systems integral to membrane technology. Japan’s extensive use of RO membranes spans both drinking water production and industrial process water, highlighting the versatility of its membrane solutions and the country’s continued influence on global desalination practices.

India: Infrastructure Expansion and Industrial Desalination Driving Market Growth

India is expanding its membrane-based desalination infrastructure through strategic investments and international collaborations. The Ghaziabad Nagar Nigam’s issuance of India’s first Certified Green Municipal Bond raised ₹150 crore to develop a Tertiary Sewage Treatment Plant (TSTP) that utilizes advanced membrane filtration for wastewater reuse in industrial applications. The Perur Desalination Plant in Chennai, funded by JICA and executed by Metito and VA TECH WABAG, is set to become Southeast Asia’s largest, employing reverse osmosis and complementary technologies for efficient water production. Additionally, Kakinada SEZ announced a ₹1,310 crore investment for a 3x50 MLD desalination plant to supply industrial water and reduce freshwater dependence. These projects underscore India’s commitment to sustainable water management through membrane-based technologies.

Australia: Innovative Research and Hybrid Technologies Enhancing Membrane Desalination

Australia addresses water scarcity challenges through cutting-edge infrastructure, government support, and academic research in membrane desalination. The Alkimos Seawater Desalination Plant, under construction in Western Australia, will produce 50 billion liters annually using RO technology with net-zero greenhouse gas emissions. Government initiatives such as the National Water Grid Fund are piloting “iFORO” (integrated Forward Osmosis – Reverse Osmosis) technology to increase water yield and minimize brine waste. Research by the Australian National University (ANU), published in Nature Communications in 2024, explores new thermal desalination methods that could complement or replace traditional membrane-based systems in specific applications. Collectively, these initiatives position Australia as a leader in sustainable, high-efficiency desalination solutions tailored to arid regions.

Competitive Landscape: Key Players Driving the Membrane Desalination Market

The global membrane desalination systems market is consolidated, with leading players holding significant market shares through advanced RO technologies, large project execution capabilities, and sustainable water treatment innovations. Below are detailed profiles of the top companies shaping the industry.

SUEZ – Driving Large-Scale Seawater RO Projects Globally

SUEZ remains a global leader in membrane desalination, offering advanced RO and nanofiltration technologies with applications in both municipal and industrial water sectors. The company strengthened its position following the acquisition of GE Water & Process Technologies in 2017, significantly expanding its global footprint. Its SeaDAF™ Filter technology is widely adopted in compact desalination plants. In recent years, SUEZ has delivered large-scale RO plants in Philippines (October 2024) and China (August 2024), positioning itself as a frontrunner in Asia-Pacific desalination expansion.

Veolia Water Technologies – Leading Sustainable and Renewable-Powered Desalination

Veolia is a benchmark in ecological transformation, with its technologies responsible for 18% of the world’s installed desalination capacity. Its recent Morocco project (October 2024) and Brazil FPSO contract (June 2025) highlight diversification across municipal and industrial markets. Veolia’s ambition to double capacity by 2030 aligns with its sustainability roadmap, ensuring growth in renewable-powered desalination plants. Its portfolio covers thermal, RO, and hybrid desalination solutions, catering to both municipal utilities and industrial customers.

Toray Industries, Inc. – Innovating High-Performance RO Membranes

Toray is a world-renowned RO and NF membrane manufacturer, leveraging its polymer chemistry expertise for innovation. In July 2025, Toray supplied membranes to the solar-powered Shuaibah 3 plant in Saudi Arabia, reinforcing its role in green desalination. The establishment of its Water Treatment Technology Center in Saudi Arabia (June 2025) further strengthens its technical presence in the Middle East. Toray’s product range spans from municipal drinking water membranes to industrial wastewater reuse membranes, making it a diversified market leader.

Dow Water & Process Solutions (DuPont) – High-Performance RO Membranes for Large-Scale Projects

Dow, now part of DuPont, is a global leader in advanced RO membranes, with its DOW FILMTEC™ elements setting benchmarks for efficiency. Its technology powers some of the largest desalination plants worldwide, including the Barka IWP project in Oman. Dow focuses on reducing energy consumption and operating costs in large-scale desalination, catering to municipal, industrial, and agricultural water needs. Its strategy remains centered on scalable, high-efficiency RO membranes for global demand.

Evoqua Water Technologies LLC – Expanding Global Presence with Mission-Critical Solutions

Evoqua specializes in mission-critical water treatment solutions, serving municipal and industrial markets with membrane desalination and advanced filtration systems. The company has strengthened its market position through acquisitions and facility expansions, including its new Singapore manufacturing plant and the India Technology Center. Evoqua’s desalination solutions are widely adopted in industrial applications, where customized, reliable water supply systems are essential. Its continuous expansion ensures a strong global presence across North America, Asia, and Europe.

Membrane-Based Desalination Systems Market Report Scope

Membrane-Based Desalination Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.4 Billion

|

|

Market Size (2034)

|

$25.2 Billion

|

|

Market Growth Rate

|

9.2%

|

|

Segments

|

By Technology (Reverse Osmosis (RO), Nanofiltration (NF), Ultrafiltration (UF), Microfiltration (MF), Hybrid Membrane Systems), By Water Source (Seawater Desalination, Brackish Water Desalination, River Water Desalination, Industrial Wastewater Reuse), By Application (Municipal Water Supply, Industrial Process Water, Power Generation Cooling Water, Agriculture & Irrigation, Military & Defense, Hospitality & Real Estate), By End-User Industry (Oil & Gas, Chemicals & Petrochemicals, Pharmaceuticals, Food & Beverage, Mining & Metals, Textile Industry, Electronics & Semiconductors), By Plant Capacity (Small-Scale (Up to 10,000 m³/day), Medium-Scale (10,000–100,000 m³/day), Large-Scale (Above 100,000 m³/day)), By Operation Mode (Mobile / Containerized Systems, Permanent / Fixed Installations)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Toray Industries, Inc., SUEZ, Veolia, Pentair plc, Xylem Inc., The Dow Chemical Company, Koch Industries, LG Chem, IDE Technologies Ltd., Aquatech International, Mitsubishi Chemical Corporation, V.A. TECH WABAG Ltd., ACWA Power, Abengoa

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Membrane-Based Desalination Systems Market Segmentation

By Technology

- Reverse Osmosis (RO)

- Nanofiltration (NF)

- Ultrafiltration (UF)

- Microfiltration (MF)

- Hybrid Membrane Systems

By Water Source

- Seawater Desalination

- Brackish Water Desalination

- River Water Desalination

- Industrial Wastewater Reuse

By Application

- Municipal Water Supply

- Industrial Process Water

- Power Generation Cooling Water

- Agriculture & Irrigation

- Military & Defense

- Hospitality & Real Estate

By End-User Industry

- Oil & Gas

- Chemicals & Petrochemicals

- Pharmaceuticals

- Food & Beverage

- Mining & Metals

- Textile Industry

- Electronics & Semiconductors

By Plant Capacity

- Small-Scale (Up to 10,000 m³/day)

- Medium-Scale (10,000–100,000 m³/day)

- Large-Scale (Above 100,000 m³/day)

By Operation Mode

- Mobile / Containerized Systems

- Permanent / Fixed Installations

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Membrane-Based Desalination Systems Industry include-

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- SUEZ

- Veolia

- Pentair plc

- Xylem Inc.

- The Dow Chemical Company

- Koch Industries

- LG Chem

- IDE Technologies Ltd.

- Aquatech International

- Mitsubishi Chemical Corporation

- V.A. TECH WABAG Ltd.

- ACWA Power

- Abengoa

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Membrane-Based Desalination Systems opportunity end-to-end market size and growth through 2034, procurement drivers, project pipelines, capex/opex benchmarks, and policy tailwinds. Our analysis reviews technology stacks (RO, NF, UF/MF, hybrids), plant capacity tiers, operating modes, and sectoral demand; it highlights breakthroughs in high-recovery RO, energy recovery devices, renewable-powered plants, and anti-fouling chemistries that compress kWh/m³ and lifecycle cost. With scenario modeling and competitive scorecards, this report is an essential resource for utilities, EPCs, OEMs, and investors seeking bankable specifications, risk-adjusted returns, and vendor shortlists across municipal and industrial deployments. Scope Includes-

- Segmentation: By Technology (Reverse Osmosis (RO), Nanofiltration (NF), Ultrafiltration (UF), Microfiltration (MF), Hybrid Membrane Systems); By Water Source (Seawater Desalination, Brackish Water Desalination, River Water Desalination, Industrial Wastewater Reuse); By Application (Municipal Water Supply, Industrial Process Water, Power Generation Cooling Water, Agriculture & Irrigation, Military & Defense, Hospitality & Real Estate); By End-User Industry (Oil & Gas, Chemicals & Petrochemicals, Pharmaceuticals, Food & Beverage, Mining & Metals, Textile Industry, Electronics & Semiconductors); By Plant Capacity (Small-Scale (Up to 10,000 m³/day), Medium-Scale (10,000–100,000 m³/day), Large-Scale (Above 100,000 m³/day)); By Operation Mode (Mobile / Containerized Systems, Permanent / Fixed Installations).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): DuPont de Nemours, Inc.; Toray Industries, Inc.; SUEZ; Veolia; Pentair plc; Xylem Inc.; The Dow Chemical Company; Koch Industries; LG Chem; IDE Technologies Ltd.; Aquatech International; Mitsubishi Chemical Corporation; V.A. TECH WABAG Ltd.; ACWA Power; Abengoa.

Methodology

USDAnalytics applied a triangulated approach: bottom-up sizing from announced/operational plants (capacity, energy intensity, recovery, ERD type) and awarded EPC contracts; top-down reconciliation with national water strategies, tariff frameworks, and public budgets; and expert validation via interviews with utilities, EPCs, membrane OEMs, and lenders. Techno-economic models normalize LCOE-water (kWh/m³), chemical and cleaning cycles, brine management routes (outfall, ZLD/MLD), and renewable coupling (PPA, behind-the-meter). Sensitivities cover energy prices, intake quality (Silt Density Index), anti-fouling advancements, and carbon pricing. Competitive benchmarking scores vendors on flux/pressure performance, durability, ERD integration, digital O&M, and delivery track record.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Membrane-Based Desalination Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Market Insights for Stakeholders

1.3. Global Market Snapshot

2. Membrane-Based Desalination Systems Market Outlook (2025–2034)

2.1. Market Overview: Expanding Role in Global Water Security

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $11.4 Billion

2.2.2. Forecasted Market Size (2034): $25.2 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 9.2%

2.3. Key Trends Shaping the Market

2.3.1. Surge of Mega-Projects in Water-Stressed Regions

2.3.2. Rising Corporate Investments and Technological Advancements

2.3.3. Transition Toward Renewable-Energy Powered Desalination

2.3.4. Breakthrough Innovations in Anti-Fouling and Self-Cleaning Membranes

2.4. Key Opportunities Accelerating Market Growth

2.4.1. Expansion of Industrial Wastewater Reuse

2.4.2. Growth of Modular and Decentralized Desalination Plants

3. Recent Developments and Strategic Activities

3.1. Market Analysis: Recent News and Strategic Developments

3.1.1. VA Tech Wabag Secures Landmark Contract in Saudi Arabia (July 2025)

3.1.2. Toray Supplies Membranes for Solar-Powered Shuaibah 3 Plant (July 2025)

3.1.3. Veolia Wins Contracts for Brazilian FPSO Platforms (June 2025)

3.1.4. Toray Establishes Water Treatment Technology Center in Saudi Arabia (June 2025)

3.1.5. Veolia Announces Plan to Double Desalination Capacity by 2030 (April 2025)

3.1.6. SUEZ Expands Footprint with Projects in Philippines and China (August-October 2024)

3.1.7. Veolia Partners with Morocco for Large-Scale Plant (October 2024)

4. Competitive Landscape: Key Players

4.1. Market Overview: Consolidated Market Driven by Innovation

4.2. Profiles of Leading Players

4.2.1. SUEZ

4.2.2. Veolia Water Technologies

4.2.3. Toray Industries, Inc.

4.2.4. Dow Water & Process Solutions (DuPont)

4.2.5. Evoqua Water Technologies LLC

5. Market Share Analysis by Segment

5.1. Market Share by Technology

5.1.1. Reverse Osmosis (RO)

5.1.2. Hybrid Membrane Systems

5.1.3. Ultrafiltration (UF) and Microfiltration (MF)

5.1.4. Nanofiltration (NF)

5.2. Market Share by Water Source

5.2.1. Seawater Desalination

5.2.2. Brackish Water Desalination

5.2.3. Industrial Wastewater Reuse

5.2.4. River Water Desalination

5.3. Market Share by Application

5.3.1. Municipal Water Supply

5.3.2. Industrial Process Water

5.3.3. Specialized Applications

6. Country Analysis and Outlook

6.1. Saudi Arabia: Strategic Investments in RO Technology

6.2. China: Regulatory Support and Technological Innovations

6.3. United States: Government and Corporate Initiatives

6.4. Japan: Technological Expertise Supporting Global Projects

6.5. India: Infrastructure Expansion and Industrial Desalination

6.6. Australia: Innovative Research and Hybrid Technologies

6.7. Other Key Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Membrane-Based Desalination Systems Market Segmentation

7.1. By Technology

7.2. By Water Source

7.3. By Application

7.4. By End-User Industry

7.5. By Plant Capacity

7.6. By Operation Mode

8. Market Size Outlook by Region (2025-2034)

8.1. North America Market Size Outlook

8.2. Europe Market Size Outlook

8.3. Asia Pacific Market Size Outlook

8.4. South America Market Size Outlook

8.5. Middle East and Africa Market Size Outlook

9. Company Profiles: Top Players

9.1. DuPont de Nemours, Inc.

9.2. Toray Industries, Inc.

9.3. SUEZ

9.4. Veolia

9.5. Pentair plc

9.6. Xylem Inc.

9.7. The Dow Chemical Company

9.8. Koch Industries

9.9. LG Chem

9.10. IDE Technologies Ltd.

9.11. Aquatech International

9.12. Mitsubishi Chemical Corporation

9.13. V.A. TECH WABAG Ltd.

9.14. ACWA Power

9.15. Abengoa

10. Methodology and Appendix

10.1. Research Scope

10.2. Market Research Approach

10.3. Market Sizing and Forecasting Model

10.4. Research Coverage

10.5. Data Horizon

10.6. Deliverables