Brackish Water Desalination Systems Market Outlook 2025–2034: Size, Growth, and Strategic Insights

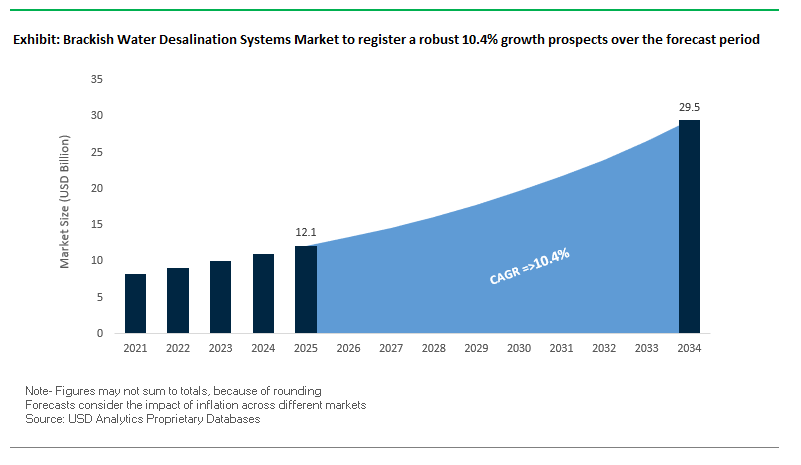

The brackish water desalination systems market is projected to expand from USD 12.1 billion in 2025 to USD 29.5 billion by 2034, reflecting a robust CAGR of 10.4% over the forecast period. The sustained growth is fueled by intensifying urban and agricultural water scarcity, particularly in water-stressed geographies like the southwestern United States, coastal India, and parts of the Middle East. As freshwater resources become increasingly constrained, brackish water reverse osmosis (BWRO) and advanced membrane technologies are emerging as cost-effective and sustainable alternatives to traditional freshwater sourcing.

In California, the state’s Water Supply Strategy targets a capacity increase to 84,000 acre-feet of brackish desalination by 2040, signaling aggressive infrastructure commitments. At the same time, electrically active membranes and hybrid-batch RO systems are improving water output by 20–30% while halving electricity consumption, creating a new performance benchmark. Public-private partnerships, such as the City of Alice–Seven Seas Water Group collaboration, demonstrate scalable financing and deployment models without significant upfront capital burden on municipalities.

Strategic Imperatives for Market Stakeholders

- Capitalize on high-growth regions like India, Texas, and California with rising municipal and agricultural water demand.

- Invest in next-gen membrane R&D to stay ahead in efficiency, fouling resistance, and lifecycle performance.

- Pursue PPPs as a risk-sharing, capital-efficient pathway to scale brackish desalination capacity.

- Integrate energy recovery devices to meet competitive cost-per-liter benchmarks and sustainability requirements.

- Diversify end-user portfolios to include industrial, municipal, and emergency response applications for revenue resilience.

Market Analysis: Policy, Technology, and Infrastructure Shaping Growth

The market is witnessing significant advancements in both technology deployment and policy-backed infrastructure investment. In July 2025, Seven Seas Water Group commissioned Texas’ first public-private brackish water RO desalination facility in the City of Alice, delivering up to 2.7 million gallons per day under a Water-as-a-Service® model. The milestone underscores a critical shift toward decentralized, partnership-driven water supply solutions that bypass traditional capital barriers for municipalities.

Membrane innovation remains a critical driver. In March 2025, DuPont launched its Multibore™ PRO ultrafiltration membranes, designed for pretreatment in brackish water desalination. These systems require fewer modules, reduce footprint, and protect downstream RO processes, enabling lower total cost of ownership.

Global water treatment leaders are also broadening their market footprint through specialized, high-value contracts. In September 2025, Veolia secured a multi-million-dollar agreement with Petrobras to supply seawater desalination systems for two FPSOs in Brazil’s offshore energy sector highlights the demand for space-efficient, high-reliability solutions in industrial applications.

Policy momentum is also reshaping demand. California’s February 2024 Water Supply Strategy lays out concrete targets at 28,000 acre-feet by 2030 and 84,000 acre-feet by 2040, which cements brackish desalination’s role in long-term water security. Meanwhile, municipal expansions like the Ahmedabad Municipal Corporation’s August 2025 Jaspur plant upgrade signal strong urban adoption in emerging economies. The sector’s adaptive capacity is further exemplified by U.S. EPA’s Water-on-Wheels emergency systems, enabling rapid deployment in disaster-affected zones.

Trends and Opportunities in Brackish Water Desalination Systems Market

Trend 1: Brackish Water Desalination Expands in Agriculture to Combat Water Scarcity

The global water crisis is intensifying the adoption of brackish water desalination systems in agriculture, especially in arid and semi-arid regions. Farmers are increasingly turning to desalinated brackish groundwater to supplement diminishing freshwater resources, ensuring stable crop yields and mitigating soil salinization risks. In Spain, over 22% of total desalinated water is allocated to agricultural applications, highlighting its significance in sustaining water-stressed farming operations. Advanced technologies, including solar-powered nanofiltration, have demonstrated improved crop yields and efficient use of water and fertilizers, as shown in pilot projects in Israel and Jordan. Moreover, brackish water desalination is approximately 35% more cost-effective than seawater desalination, making it an economically viable solution for large-scale irrigation while reducing long-term risks of soil degradation.

Trend 2: Decentralized Brackish Water Treatment for Rural Communities

In developing countries and rural areas, the absence of centralized water infrastructure and the presence of brackish groundwater are fueling the growth of small-scale, decentralized brackish water treatment systems. Modular units provide an accessible source of clean drinking water for communities in water-stressed regions, addressing critical public health needs. Globally, over 1.6 billion people reside in rural areas lacking sufficient water supply, making solar-powered desalination an ideal solution. Successful case studies, such as low-pressure reverse osmosis (RO) systems in rural Mexico producing 1.8 cubic meters of freshwater per day, have demonstrated feasibility and reliability. Technologies like Electrodialysis Reversal (EDR) enhance water recovery while reducing energy consumption, offering an effective decentralized solution for regions with limited grid access.

Opportunity 1: Low-Cost Electrodialysis Systems for Brackish Water in Emerging Markets

Electrodialysis (ED) is emerging as a cost-efficient alternative to reverse osmosis for brackish water, particularly in low-salinity regions and emerging markets. ED systems are more economical for feed salinities up to 3 g/L, making them suitable for slightly saline water sources without the high-pressure requirements of RO. Additionally, ED systems achieve higher water recovery ratios at 60% compared to 25–50% for RO to reduce water wastage. Lower operational costs stem from the absence of high-pressure pumps and reduced pre-treatment needs, while anticipated reductions in ion-exchange membrane costs could make ED a preferred technology across broader salinity ranges in the near future.

Opportunity 2: Brackish Desalination Coupled with Solar Microgrids in Off-Grid Areas

The growing affordability and reliability of solar power present significant opportunities for integrating brackish water desalination with solar microgrids. Solar-powered brackish water RO systems provide cost-effective and autonomous water solutions for off-grid and remote regions, reducing reliance on conventional energy and ensuring a secure water supply. Case studies indicate capital costs can be 10% lower, with freshwater production costs up to 50% lower than alternative energy-powered systems. High solar energy potential in arid regions, such as Chihuahua, Mexico (5.07–7.31 kWh/m²/day), further supports feasibility. Modular designs allow scalable production ranging from 10 to 2,000 cubic meters per day, enabling communities to install precisely sized systems and expand capacity as needed, while companies like OSMOSUN have successfully implemented battery-free solar desalination plants in Cape Verde and Namibia.

Brackish Water Desalination Systems Market Share Insights

Brackish Water Reverse Osmosis (BWRO) Commands 71.3% Market Dominance

Membrane-based systems, led by Brackish Water Reverse Osmosis (BWRO), are projected to capture nearly 71.3% of the global brackish water desalination systems market by 2025. Their dominance reflects the lower energy requirements compared to seawater desalination, coupled with reduced operating pressures and scalable designs. While electrodialysis reversal (ED/EDR) retains 13.9% share in niche low-salinity applications and nanofiltration is widely used for selective hardness removal, BWRO remains the go-to choice for cost-efficient, high-recovery operations across municipal and industrial sectors.

.png)

Modular Skid-Mounted Units Secure Half of System Installations

Skid-mounted and modular systems account for approximately 48.7% of the global market, making them the backbone of both industrial and municipal deployments. Their appeal lies in pre-engineered, standardized assembly that reduces installation costs and accelerates deployment, offering scalability from small municipalities to industrial clusters. By contrast, large-scale fixed installations, with 31.2% market share, dominate in municipal water projects where capital-intensive, permanent facilities are justified. Containerized systems and mobile trailers serve remote or emergency water needs, highlighting the growing importance of portability and rapid response capabilities in desalination infrastructure.

Municipal and Industrial Sectors Drive 75% of End-Use Demand

Municipal water utilities remain the primary end-user, holding about 40.3% of total market share. Cities in water-stressed inland regions are adopting BWRO to tap brackish aquifers and diversify supply amid droughts and groundwater salinity challenges. At the same time, industrial demand spanning food & beverage, power generation, mining, and oil & gas accounts for 28.7% of the market, making it the most diverse and innovation-driven segment. Agriculture follows with 14.3%, primarily in greenhouse irrigation and hydroponics for high-value crops, while the commercial and military sectors rely on brackish desalination for secure, off-grid supply in remote or strategic locations.

Medium-Salinity Feedwater Represents the Economic Sweet Spot

Feedwater in the medium salinity range of 5,000–15,000 ppm TDS represents 44.3% of the global market, marking the most commercially viable operating range for BWRO. Systems in the range deliver significant water quality improvements while maintaining competitive energy costs. Low-salinity sources (1,000–5,000 ppm) hold 36.7% market share, where electrodialysis often competes effectively with RO, particularly in scaling-prone waters. By contrast, high-salinity brackish sources (15,000–30,000 ppm) account for 20% but demand higher-pressure RO and advanced pre-treatment, making them a cost-intensive choice typically reserved for critical industrial or municipal supply projects.

Brine Management Dominated by Deep Well Injection at 40%

Deep well injection remains the preferred brine disposal strategy, representing 40.3% of global market share, particularly in regions with suitable geological formations. Surface discharge, at 31.4%, persists but faces tightening environmental regulations, while evaporation ponds account for 20%, mainly in arid zones with abundant land availability. Increasingly, brine concentration technologies such as electrodialysis metathesis (EDM) and vibratory shear enhanced processing (VSEP) are gaining adoption, reducing waste volume and pushing operations toward Zero Liquid Discharge (ZLD) models. The shift aligns with global sustainability goals and growing regulatory pressure on water-intensive industries.

Country Analysis of the Brackish Water Desalination Systems Market

Saudi Arabia: Pioneering Hybrid and Advanced BWRO Desalination for Water Security

Saudi Arabia is a global leader in brackish water desalination systems, driven by its Vision 2030 initiatives aimed at sustainable water security. The Saline Water Conversion Corporation (SWCC) commissioned the technologically advanced Shuqaiq 3 plant, recognized as one of the most sustainable desalination facilities worldwide. Hybrid projects like the Ras Al Khair plant, which combines thermal multi-stage flash (MSF) and reverse osmosis (RO) technologies, exemplify the country’s commitment to energy-efficient and high-capacity desalination. The Kingdom maintains an extensive network of desalination plants along the Red Sea and Arabian Gulf, supplying more than 70% of its freshwater demand, establishing Saudi Arabia as a hub for innovative water supply solutions.

United States: Expanding BWRO Facilities to Address Water Scarcity

The U.S. brackish water desalination market is growing to meet increasing water demand in arid regions, with key hubs in Florida and Texas. Texas plans to expand numerous brackish water reverse osmosis (BWRO) facilities, supplementing the hundreds of municipal membrane treatment plants already in operation. California’s reliance on large-scale seawater and brackish water desalination, such as the Claude “Bud” Lewis Carlsbad plant, delivers over 190 million liters of potable water daily, reducing dependence on imported water sources. These projects emphasize the U.S. focus on energy-efficient desalination technologies and smart water management solutions.

Spain: Leading European Desalination Through RO Upgrades

Spain is the largest desalination market in Europe, with more than 1,900 active facilities addressing drought resilience and agricultural needs. Investments have been made to upgrade legacy multi-stage flash units to high-pressure reverse osmosis (RO) systems, achieving significant energy savings. Spanish desalination infrastructure is critical for the agricultural sector, supporting water-intensive crops such as fruits, vegetables, and grapes. The European Union’s Blue Economy Observatory recognizes Spain’s desalination capabilities as essential for mitigating annual drought-related losses exceeding €1.5 billion, highlighting the country’s role in sustainable water supply and energy-efficient desalination technologies.

United Arab Emirates: Integrating Renewable Energy in BWRO Systems

The UAE is a global leader in brackish water and RO desalination systems, producing around 90% of its drinking water from desalination plants. The Taweelah power and water complex, with a capacity exceeding 900,000 cubic meters per day, represents a flagship RO project enhancing municipal water supply. The UAE is also pioneering renewable energy integration, with gigawatt-scale photovoltaic (PV)-RO hybrid plants aimed at lowering operational costs and carbon emissions. The positions the country at the forefront of energy-efficient and sustainable desalination solutions in water-scarce regions.

Israel: World Leader in Advanced BWRO and Desalination Research

Israel meets approximately 70% of its freshwater demand through desalination, combining reverse osmosis technologies with cutting-edge research. The Sorek plant supplies 20% of municipal water demand, while the Sorek 2 – Be'er Miriam plant represents the world’s first steam-driven seawater RO system, demonstrating innovation in energy-efficient desalination and smart water infrastructure. Israel’s technology-driven approach ensures water supply not only for residential use but also for agricultural irrigation, showcasing its expertise in sustainable and high-performance BWRO systems.

Morocco: Expanding Desalination to Combat Drought

Morocco is rapidly scaling its brackish water desalination capabilities to address historic droughts. By 2030, the country aims to source 50% of its drinking water from desalination, with 15 plants under development. Africa’s largest desalination plant near Rabat, a collaboration with Veolia, will produce 822,000 cubic meters per day, providing water to an estimated 9.3 million residents. These initiatives position Morocco as a growing market for energy-efficient brackish water and RO desalination solutions, emphasizing resilience against water scarcity.

Competitive Landscape: Leading Innovators and Market Movers

The brackish water desalination systems market is dominated by a mix of global technology providers and specialized infrastructure developers, each leveraging unique competitive advantages. The leaders are innovating in membrane performance, energy efficiency, and financing models while pursuing high-profile municipal and industrial contracts worldwide.

DuPont Water Solutions: Advancing High-Performance Membranes

DuPont focuses on separation and purification technologies, offering FilmTec™ RO/NF membranes and the Multibore™ PRO ultrafiltration line. Recognized with a 2025 BIG Innovation Award, DuPont’s solutions are designed for longer lifecycles and superior fouling resistance. Its Sustainability Navigator digital tool enables clients to assess environmental impacts, aligning with the industry’s decarbonization goals.

Veolia Environnement S.A.: Full-Cycle Ecological Transformation

Veolia applies a lifecycle approach to water management, integrating mobile RO units, advanced pre-treatment, and digital optimization platforms like Hubgrade. Recent wins include the Petrobras FPSO desalination contract in Brazil, cementing Veolia’s position in offshore industrial water solutions. Its PoIaris™ systems cater to high-purity industrial sectors, particularly pharmaceuticals.

SUEZ S.A.: Circular and Energy-Efficient Water Solutions

SUEZ delivers membrane filtration, MBR, and advanced oxidation technologies, targeting large-scale municipal and industrial needs. Landmark projects include the 500 MLD Mumbai wastewater facility under a €700 million contract. The company is notable for securing high-value PPPs and partnering with CNRS to address micropollutants.

IDE Technologies: Pioneers in Large-Scale Desalination

IDE specializes in large-scale RO, NF, and thermal desalination systems, including MED and MVC technologies. Flagship projects like the Carlsbad Plant (USA) and Sorek I & II (Israel) position IDE as a leader in high-performance, energy-efficient plants with proven municipal and industrial applications.

Seven Seas Water Group: Scaling Water-as-a-Service®

Seven Seas champions the Water-as-a-Service® model, delivering fully financed, designed, owned, and operated desalination systems. The July 2025 City of Alice plant is a landmark for U.S. brackish water infrastructure, demonstrating scalability and speed-to-market in water-stressed regions.

Brackish Water Desalination Systems Market Report Scope

Brackish Water Desalination Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.1 Billion

|

|

Market Size (2034)

|

$29.5 Billion

|

|

Market Growth Rate

|

10.4%

|

|

Segments

|

By Technology Type (Membrane-Based Systems, Electrodialysis/Electrodialysis Reversal (ED/EDR), Nanofiltration (NF) Systems, Emerging Technologies, Hybrid Systems), By System Configuration (Skid-Mounted/Modular Units, Containerized Systems, Fixed-Plant Installations, Mobile Trailers), By End-Use Sector (Municipal & Public Water supply, Industrial Applications, Agricultural Use, Commercial, Military & Remote Sites), By Feedwater Characteristics (Low Salinity (1,000–5,000 ppm TDS), Medium Salinity (5,000–15,000 ppm TDS), High Salinity (15,000–30,000 ppm TDS)), By Brine Management (Surface Discharge, Deep Well Injection, Evaporation Ponds, Brine Concentration)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., DuPont, IDE Technologies, ACCIONA, Aquatech International LLC, Toray Industries, Inc., SUEZ, Kurita Water Industries, Evoqua Water Technologies (now part of Xylem), Thermax Limited, VA Tech Wabag, Biwater Holdings Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Brackish Water Desalination Systems Market Segmentation

By Technology Type

- Membrane-Based Systems

- Reverse Osmosis (BWRO)

- Standard BWRO

- High-Recovery BWRO

- Low-Energy BWRO

- Electrodialysis/Electrodialysis Reversal (ED/EDR)

- Nanofiltration (NF) Systems

- Emerging Technologies

- Hybrid Systems

By System Configuration

- Skid-Mounted/Modular Units

- Containerized Systems

- Fixed-Plant Installations

- Mobile Trailers

By End-Use Sector

- Municipal & Public Water Supply

- Industrial Applications

- Food & Beverage

- Textiles

- Mining

- Power Plants

- Others

- Agricultural Use

- Commercial

- Military & Remote Sites

By Feedwater Characteristics

- Low Salinity (1,000–5,000 ppm TDS)

- Medium Salinity (5,000–15,000 ppm TDS)

- High Salinity (15,000–30,000 ppm TDS)

By Brine Management

- Surface Discharge

- Deep Well Injection

- Evaporation Ponds

- Brine Concentration

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Brackish Water Desalination Systems Market

- Veolia

- Xylem Inc.

- DuPont

- IDE Technologies

- ACCIONA

- Aquatech International LLC

- Toray Industries, Inc.

- SUEZ

- Kurita Water Industries

- Evoqua Water Technologies (now part of Xylem)

- Thermax Limited

- VA Tech Wabag

- Biwater Holdings Limited

* List Not Exhaustive

Research Coverage

This report investigates the Global Brackish Water Desalination Systems Market, providing comprehensive analysis reviews of growth drivers, technology adoption, and regulatory initiatives shaping the industry through 2034. Published by USDAnalytics, the study highlights key breakthroughs such as hybrid-batch RO, electrically active membranes, and PPP-based Water-as-a-Service® models that are redefining brackish water treatment economics. The report also highlights how escalating municipal and agricultural water scarcity in regions like California, India, and the Middle East is accelerating demand for BWRO and electrodialysis systems. With strategic insights into market share, infrastructure investments, and competitive strategies, this report is an essential resource for utilities, policymakers, EPC contractors, and technology providers navigating the global brackish desalination market.

Scope Includes:

- Segmentation: By Technology (BWRO, Electrodialysis, Nanofiltration, Hybrid Systems), By Plant Configuration (Skid-Mounted, Containerized, Fixed, Mobile), By End-Use Sector (Municipal, Industrial, Agriculture, Commercial, Military), By Feedwater Salinity (Low, Medium, High), and By Brine Management (Deep Well Injection, Surface Discharge, Evaporation Ponds, ZLD).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021–2024, and Forecast Data: 2025–2034.

- Companies: Profiles and analysis of 15+ leading players including DuPont, Veolia, SUEZ, IDE Technologies, and Seven Seas Water Group.

Methodology

The research methodology applied by USDAnalytics integrates primary interviews and secondary research to ensure reliability and actionable insights. Primary research involved discussions with plant operators, technology developers, regulators, and financial institutions to validate market assumptions and adoption trends. Secondary research leveraged industry publications, desalination project databases, company reports, and policy frameworks. Market sizing was performed using top-down and bottom-up approaches, triangulated across technology adoption rates, regional deployments, and investment pipelines. Scenario modeling incorporated energy costs, regulatory targets, financing models, and membrane R&D trajectories to produce robust forecasts that reflect the real-world evolution of the brackish desalination market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Brackish Water Desalination Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Market Stakeholders

1.3. Global Market Snapshot

2. Brackish Water Desalination Systems Market Outlook (2025–2034)

2.1. Introduction to the Brackish Water Desalination Systems Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $12.1 Billion

2.2.2. Forecasted Market Size (2034): $29.5 Billion at 10.4% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Intensifying Urban and Agricultural Water Scarcity

2.3.2. Advancements in Brackish Water Reverse Osmosis (BWRO) and Membrane Technologies

2.3.3. Public-Private Partnerships and Cost-Effective Deployment

3. Market Analysis: Policy, Technology, and Infrastructure Shaping Growth

3.1. Overview of Technology and Infrastructure Investment

3.2. Strategic Developments of Key Players

3.2.1. Seven Seas Water Group's Public-Private Partnership in Texas (July 2025)

3.2.2. DuPont's Multibore™ PRO Ultrafiltration Membranes (March 2025)

3.2.3. Veolia's Agreement with Petrobras for Offshore Systems (September 2025)

3.3. Policy Momentum and Municipal Expansions

3.3.1. California's Water Supply Strategy Targets (February 2024)

3.3.2. U.S. EPA's Water-on-Wheels Emergency Systems

4. Trends and Opportunities in Brackish Water Desalination Systems

4.1. Trend 1: Expansion in Agriculture to Combat Water Scarcity

4.1.1. Supplementing Diminishing Freshwater Resources

4.1.2. Cost-Effectiveness Compared to Seawater Desalination

4.2. Trend 2: Decentralized Treatment for Rural Communities

4.2.1. Addressing Critical Public Health Needs in Developing Countries

4.2.2. Feasibility of Small-Scale, Solar-Powered Systems

4.3. Opportunity 1: Low-Cost Electrodialysis Systems

4.3.1. A Cost-Efficient Alternative to Reverse Osmosis

4.3.2. Higher Water Recovery Ratios and Lower Operational Costs

4.4. Opportunity 2: Desalination Coupled with Solar Microgrids

4.4.1. Autonomous Water Solutions for Off-Grid Areas

4.4.2. Lower Capital and Production Costs

5. Competitive Landscape: Leading Innovators and Market Movers

5.1. DuPont Water Solutions: Advancing High-Performance Membranes

5.2. Veolia Environnement S.A.: Full-Cycle Ecological Transformation

5.3. SUEZ S.A.: Circular and Energy-Efficient Water Solutions

5.4. IDE Technologies: Pioneers in Large-Scale Desalination

5.5. Seven Seas Water Group: Scaling Water-as-a-Service®

5.6. Other Key Players

6. Market Share and Segmentation Insights: Brackish Water Desalination Systems Market

6.1. By Technology Type

6.1.1. BWRO Commands 70% Market Dominance

6.1.2. Electrodialysis (ED/EDR) and Nanofiltration (NF) Shares

6.2. By System Configuration

6.2.1. Modular Skid-Mounted Units Secure 50% of Installations

6.2.2. Fixed Installations, Containerized Systems, and Mobile Trailers

6.3. By End-Use Sector

6.3.1. Municipal and Industrial Sectors Drive 75% of Demand

6.3.2. Agricultural, Commercial, and Military Segments

6.4. By Feedwater Characteristics

6.4.1. Medium-Salinity Feedwater Represents the Economic Sweet Spot (45%)

6.4.2. Low- and High-Salinity Sources

6.5. By Brine Management

6.5.1. Deep Well Injection Dominates (40%)

6.5.2. Surface Discharge, Evaporation Ponds, and Brine Concentration

7. Country Analysis and Outlook of the Brackish Water Desalination Systems Market

7.1. Saudi Arabia: Pioneering Hybrid and Advanced BWRO Desalination

7.2. United States: Expanding BWRO Facilities to Address Scarcity

7.3. Spain: Leading European Desalination Through RO Upgrades

7.4. United Arab Emirates: Integrating Renewable Energy in BWRO Systems

7.5. Israel: World Leader in Advanced BWRO and Research

7.6. Morocco: Expanding Desalination to Combat Drought

7.7. Other Country Analysis

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. By Technology Type

8.1.2. By System Configuration

8.1.3. By End-Use Sector

8.1.4. By Feedwater Characteristics

8.1.5. By Brine Management

8.2. Europe Market Size Outlook to 2034

8.2.1. By Technology Type

8.2.2. By System Configuration

8.2.3. By End-Use Sector

8.2.4. By Feedwater Characteristics

8.2.5. By Brine Management

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. By Technology Type

8.3.2. By System Configuration

8.3.3. By End-Use Sector

8.3.4. By Feedwater Characteristics

8.3.5. By Brine Management

8.4. South America Market Size Outlook to 2034

8.4.1. By Technology Type

8.4.2. By System Configuration

8.4.3. By End-Use Sector

8.4.4. By Feedwater Characteristics

8.4.5. By Brine Management

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. By Technology Type

8.5.2. By System Configuration

8.5.3. By End-Use Sector

8.5.4. By Feedwater Characteristics

8.5.5. By Brine Management

9. Methodology

9.1. Research Scope

9.1.1. Geographic Scope

9.1.2. Historic & Forecast Data

9.1.3. Companies Covered

9.2. Market Research Approach

9.2.1. Primary Interviews

9.2.2. Secondary Data Analysis

9.3. Market Sizing and Forecasting Model

9.3.1. Top-Down Approach

9.3.2. Bottom-Up Approach

9.3.3. Data Triangulation and Scenario Modeling

9.4. Research Coverage

9.5. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures