Smart Water Treatment Systems Market Outlook

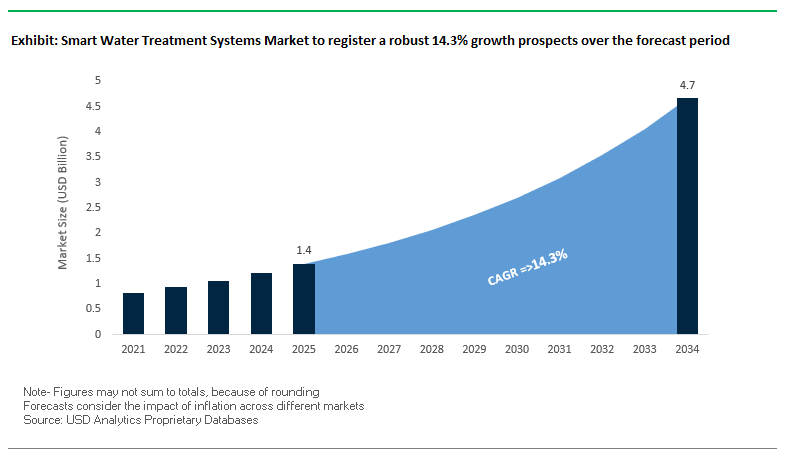

The smart water treatment systems market is projected to surge from $1.4 billion in 2025 to $4.7 billion by 2034, expanding at a robust CAGR of 14.3%. The rapid growth is underpinned by the rising adoption of AI-driven operational intelligence, IoT-enabled smart sensors, and digital twin technology to optimize municipal and industrial water operations.

At the heart of the transformation, artificial intelligence integrates data streams from IoT sensors and SCADA systems, enabling utilities to predict maintenance needs, optimize resource allocation, and improve service reliability. The proliferation of real-time smart sensors is delivering continuous monitoring of water quality, flow, and pressure. The supports early leak detection, which can cut water loss by up to 15%, while ensuring rapid containment of contamination events.

Digital twin technology is emerging as a predictive powerhouse, creating virtual replicas of water treatment assets to simulate operational scenarios, test risk mitigation strategies, and reduce energy usage. However, the increasing digitalization heightens cybersecurity risks, prompting utilities to invest heavily in network segmentation, multi-factor authentication, and real-time threat monitoring to safeguard critical infrastructure.

Strategic Imperatives for Stakeholders:

- Prioritize AI-powered operational intelligence platforms to boost efficiency and service resilience.

- Expand IoT-enabled sensor networks for real-time monitoring and early leak detection.

- Integrate digital twin simulations to predict failures and optimize energy consumption.

- Implement cybersecurity frameworks that address the vulnerabilities of connected water infrastructure.

Market Analysis: Strategic Moves, Investments, and Technological Shifts

The smart water treatment systems market is witnessing accelerated innovation, driven by high-value partnerships, acquisitions, and product launches that are reshaping competitive positioning.

In July 2025, H2O America completed a $540 million acquisition of Quadvest, a Texas-based utility, alongside a $500 million infrastructure modernization plan over the next five years. The initiative will integrate advanced modular water treatment systems to meet the needs of rapidly expanding service areas. Similarly, in March 2024, SUEZ and Vodafone formed a global alliance to deploy over two million smart meters by 2030, using Vodafone’s NB-IoT connectivity to reduce non-revenue water losses by up to 15%.

The digitalization trend is also evident in Veolia’s November 2023 launch of Hubgrade, an AI-powered platform connecting over 10,000 sites worldwide, which has already demonstrated a 15% reduction in municipal water leakage in Prague. Xylem, in December 2024, expanded its digital reach by acquiring a majority stake in Idrica, enhancing its Xylem Vue platform with AI-powered leak detection. Just months earlier, in August 2024, Xylem introduced the Rivo™ I modular control system for municipal drinking water offers real-time chemical dosing and scalable monitoring capabilities.

Consolidation is also shaping market dynamics. Pentair’s October 2024 acquisition of Porous Media for $225 million expanded its high-performance filtration portfolio, adding smart monitoring features for industrial and municipal clients. On the infrastructure front, the City of DuPont, WA recently completed two GAC filtration plants to eliminate PFAS contamination, backed by $7.3 million in grants and outfitted with advanced monitoring technology. Long-term strategic contracts are also emerging such as SUEZ’s September 2023 agreement with Chongqing Water Group to construct and operate a smart water treatment plant serving over 3.3 million residents in China.

Trends and Opportunities in Smart Water Treatment Systems Market

Trend 1: AI-Powered Predictive Maintenance for Treatment Plants

The smart water treatment industry is undergoing a profound transformation with AI and machine learning, particularly in predictive maintenance applications. Unlike traditional reactive approaches, AI analyzes real-time data from sensors and historical maintenance records to anticipate equipment failures, optimize operations, and reduce energy consumption. Case studies indicate that AI-driven optimization in wastewater treatment plants can reduce energy consumption by up to 19%, particularly in aeration processes that typically account for 60% of total plant energy use. Predictive failure detection frameworks have demonstrated a 26% reduction in system inefficiencies, significantly increasing asset availability and minimizing downtime. Furthermore, AI enables dynamic process control, adjusting biological treatment phases, aeration rates, and nutrient dosing in real time to maintain consistent water quality while conserving energy. The trend positions AI as a critical tool for cost reduction, operational efficiency, and sustainability in municipal, industrial, and commercial water systems.

Trend 2: Blockchain-Enabled Water Quality Monitoring

Blockchain technology is emerging as a transformative trend for secure, transparent, and traceable water quality management. By creating decentralized, tamper-proof ledgers, blockchain ensures data integrity from source to tap, addressing public concerns about water safety. Tamper-proof encryption and timestamping of sensor data prevent unauthorized modifications, making the data highly reliable for regulators and stakeholders. Integration with smart contracts allows automated alerts and regulatory compliance enforcement when water quality parameters fall below safe thresholds, eliminating delays associated with manual oversight. The level of transparency also builds public trust, allowing communities and authorities to independently verify water quality data. Municipalities, utilities, and industrial facilities adopting blockchain-enabled monitoring can strengthen accountability, improve regulatory compliance, and enhance overall water safety.

Opportunity 1: Edge Computing for Real-Time Contaminant Detection

Edge computing is creating significant opportunities for smart water systems by decentralizing data processing to the device level. The approach reduces latency, enabling instant detection and response to contaminants. Comparative studies show edge computing can achieve latency as low as 20.33 ms versus over 100 ms for cloud-based systems, while maintaining a high packet delivery ratio (97.47%). AI algorithms embedded in edge devices can autonomously detect harmful chemicals and trigger immediate localized actions, such as activating filtration systems or shutting off pumps, ensuring rapid mitigation of water threats. Decentralization also enhances network resilience, as individual edge devices continue operating independently even during central system or internet outages. The innovation improves safety, responsiveness, and operational reliability for municipal, industrial, and agricultural water networks.

Opportunity 2: 5G-Enabled Smart Metering for Leak Prevention

The deployment of 5G networks presents a transformative opportunity for smart water metering and leak detection. Ultra-low latency and high bandwidth enable real-time monitoring of water flow, pressure, and consumption across extensive distribution networks. Utilities employing 5G-enabled smart meters, such as a case study in France, have successfully identified and repaired over 1,200 leaks in four years, significantly reducing water losses. Smart metering reduces “non-revenue water,” with documented savings ranging from 7% to 22% and, in some cases, up to 46% of total customer water usage. Additionally, 5G facilitates enhanced network management by allowing real-time collection and analysis of data from thousands of meters, supporting demand forecasting, operational efficiency, and long-term infrastructure planning. The trend positions 5G-enabled smart metering as a key driver for sustainable and efficient water management.

Smart Water Treatment Systems Market Share Insights

IoT-Enabled Monitoring & AI Driving Smart Water Management

IoT-enabled monitoring and control (40.4%) continues as the largest technology segment in 2025, forming the foundational layer for smart water treatment systems. These solutions provide real-time data acquisition from sensors and meters, enabling utilities and industries to monitor water quality, flow, pressure, and chemical dosing across extensive networks. AI & Machine Learning solutions are the fastest-growing segment, turning raw operational data into actionable insights for predictive maintenance, anomaly detection, and optimization of chemical dosing, thus reducing operational costs and minimizing water loss. The integration of IoT with AI is accelerating the shift toward intelligent, data-driven water management systems.

.png)

Smart Sensors, SCADA, and AI Software Platforms as System Enablers

Smart sensors and meters (31.6%) remain critical for data collection, including monitoring of pH, chlorine, turbidity, and acoustic leak detection. These feed into centralized SCADA systems, which serve as the nerve center for water treatment operations, now evolving to integrate AI platforms for analytics and visualization. Edge computing devices enhance real-time responsiveness at key points like pump stations, ensuring rapid corrective action. This ecosystem of sensors, software, and control devices is central to achieving efficiency, predictive capabilities, and compliance in modern water networks.

Water Quality Management and Demand Optimization Lead Applications

Water quality management (34.8%) is the core application, enabling continuous monitoring from source to tap and ensuring compliance with stringent regulatory standards. Smart systems allow rapid detection of contamination events, optimize chemical dosing, and enhance operational efficiency. Demand and supply optimization is also a major driver, leveraging network data and AI to balance reservoir levels, pump schedules, and reduce non-revenue water (NRW). Distribution network management complements these efforts, focusing on leak detection, pressure control, and extension of infrastructure life in municipal and industrial networks.

Process Control and Distribution Network Management as Key Treatment Stages

Process control in treatment plants (35.6%) represents the largest treatment-stage segment, where AI-driven chemical dosing and energy optimization significantly reduce operating expenses while maintaining consistent output quality. Distribution network management addresses the largest and most vulnerable asset, employing smart systems to monitor pressure, detect leaks, and manage water age. Wastewater treatment optimization and raw water intake monitoring further enhance efficiency and compliance, particularly for energy-intensive treatment processes and early warning for contamination events.

Municipal Utilities and Industrial Facilities as Primary End-Users

Municipal water utilities (60%) are the dominant end-users, pressured to modernize infrastructure, reduce non-revenue water, and improve operational efficiency. Industrial facilities represent a high-value market, investing in smart systems for process water optimization, chemical cost reduction, and sustainability metrics. Commercial buildings and large-scale agricultural operations are emerging segments, adopting smart water solutions for leak detection, cooling system optimization, and precision irrigation.

Cloud-Based Deployment Leading the Smart Water Solutions Market

Cloud-based solutions (54.5%) dominate deployment models, offering scalability, lower upfront costs, and seamless integration across a utility’s footprint. On-premise deployments are preferred for utilities and industries with stringent data security requirements, while hybrid deployments combine cloud analytics with on-site control for flexibility. The trend toward cloud adoption is enhancing real-time decision-making, predictive maintenance, and overall system resilience in the smart water treatment sector.

Country Analysis of the Smart Water Treatment Systems Market

United States: AI-Driven Smart Water Monitoring and Infrastructure Modernization

The U.S. smart water treatment systems market is witnessing strong growth fueled by the Bipartisan Infrastructure Law, which provides significant funding for drinking water and wastewater infrastructure upgrades. The investment is creating a substantial market for IoT-enabled and AI-driven water treatment technologies that enhance operational efficiency, monitor water quality, and manage aging infrastructure. The EPA’s tightening of regulations on emerging contaminants like PFAS is accelerating the adoption of sensor-based monitoring systems and advanced treatment solutions. Companies such as Innovyze (Autodesk) and Bentley Systems are offering integrated software solutions for predictive maintenance, water demand forecasting, and operational optimization. Sensus, a Xylem brand, provides remotely managed platforms that enable utilities, cooperatives, and municipalities to make data-driven decisions, while smart water meters are being increasingly deployed to reduce non-revenue water, detect leaks, and provide real-time consumption data to customers.

China: Policy-Driven Smart Water Infrastructure and Urban Water Management

China’s government initiatives, including the Water Ten Plan and Dual Carbon goals, are central to the adoption of smart water treatment systems. Policies promoting IoT-enabled and AI-powered water infrastructure are creating opportunities for real-time monitoring, water reuse, and urban runoff management. Veolia’s operations in Shenzhen, with a combined wastewater treatment capacity of 1.41 million cubic meters per day, utilize integrated smart systems for water quality management. The development of sponge cities, alongside significant investment in water infrastructure modernization, is driving demand for cloud-based water monitoring platforms and portable sensors. Chinese water technology companies are rapidly expanding both domestically and internationally, exporting smart solutions to Belt and Road countries, and implementing solar-powered water quality sensors in rural and disaster-prone areas.

India: IoT-Enabled Rural Water Monitoring and Smart Urban Water Initiatives

India’s smart water treatment systems market is propelled by the Jal Jeevan Mission, which deploys IoT and sensor-based technologies across six lakh villages to monitor rural drinking water supply and create a smart water ecosystem. A Technical Expert Committee has prepared a roadmap for measurement and monitoring of water service delivery, ensuring real-time oversight. Startups like KarIoT and WEGoT Utility Solutions are developing IoT-based smart meters and management solutions for residential and commercial buildings, while DigitalPaani offers a platform to monitor and optimize water infrastructure, targeting 175 plants and 4,000 buildings by 2026. The government’s Smart Cities Mission further drives adoption of digital water management solutions for sustainable urban water supply and service delivery efficiency.

Singapore: National Smart Water Network and Water Security Leadership

Singapore’s Public Utilities Board (PUB) has established a nationwide smart water network, leveraging sensors to monitor water quality, flow, and pressure in real-time. The country’s emphasis on water security and conservation has led to smart water treatment and reuse systems, which are critical for its long-term water strategy. Singapore’s ecosystem of water technology companies, research institutions, and public-private collaborations fosters the development of cutting-edge digital water infrastructure. Ongoing R&D and government-led initiatives make Singapore a hub for smart water technologies that integrate automation, IoT, and AI for operational efficiency and sustainable urban water management.

Germany: Integrated Smart Water Systems and Circular Economy Solutions

Germany’s smart water treatment market is strengthened by projects like InDigWa, a collaboration between Fraunhofer institutes, municipalities, and businesses to consolidate isolated innovations into efficient, consumer-centric systems. The German Association for Gas and Water (DVGW) is promoting energy-efficient, resource-recovering solutions, supporting the circular economy through modular and mobile smart water systems. Germany’s commitment to energy efficiency, coupled with EU regulatory frameworks and climate goals, is driving widespread adoption of AI-enabled water management solutions, IoT monitoring platforms, and decentralized water infrastructure to optimize urban and rural water supply operations.

United Arab Emirates: Smart Water Management in a Water-Scarce Region

The UAE is a leading adopter of smart water treatment systems due to high water demand and scarcity challenges. The government invests in large-scale desalination and wastewater treatment projects that integrate smart technologies for monitoring and operational efficiency. The Dubai Electricity and Water Authority (DEWA) is at the forefront, deploying smart grids, IoT-based water meters, and real-time water management platforms for industrial, commercial, and residential applications. The UAE market is seeing a rapid increase in digital water infrastructure, AI-driven monitoring, and real-time quality assessment solutions to optimize supply and ensure sustainability in urban and industrial water systems.

Competitive Landscape: Technology Leaders Shaping the Smart Water Future

The smart water treatment systems market is defined by a mix of multinational leaders and specialized technology providers, all vying for dominance through digital innovation, AI integration, and strategic acquisitions. These companies are not only expanding their solution portfolios but also embedding intelligence and connectivity into every aspect of water management.

Veolia Environnement S.A.: AI-Driven Ecological Transformation

Veolia is positioning itself as a full-lifecycle water solutions leader, with a strategic focus on digital optimization and energy-efficient smart grids. Its flagship Hubgrade platform leverages AI and operational intelligence to monitor and enhance water, energy, and waste systems in real time helping clients cut leakage rates and reduce operational costs. The company’s $1.75 billion acquisition of the remaining stake in Water Technologies and Solutions underscores its commitment to scaling its technology segment under the “GreenUp” roadmap. With a vast installed base of connected assets, Veolia enjoys deep data-driven insights that strengthen predictive maintenance and resilience planning.

SUEZ S.A.: Global Connectivity and Circular Water Solutions

SUEZ focuses on delivering IoT-powered water infrastructure, combining its AQUADVANCED® performance optimization platform with the ON’Connect™ smart metering solution to enhance efficiency and sustainability. The March 2024 partnership with Vodafone marks a significant leap toward global smart meter deployment, leveraging NB-IoT for cost-effective and reliable connectivity. Known for its robust infrastructure expertise, SUEZ integrates digital capabilities into turnkey water and wastewater projects, ensuring both municipal and industrial clients meet their sustainability targets.

Xylem Inc.: Interconnected Smart Water Ecosystems

Xylem’s strategy revolves around building integrated digital ecosystems for water utilities through its Xylem Vue platform, which unifies data from diverse sources for leak detection, non-revenue water management, and predictive maintenance. The December 2024 acquisition of Idrica added AI-driven analytics to its portfolio, complementing the August 2024 launch of the modular Rivo™ I analyzer-control system. Xylem’s vendor-agnostic approach enables utilities to integrate legacy systems, giving it a competitive edge in real-time telemetry and asset optimization.

Smart Water Treatment Systems Market Report Scope

Smart Water Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$4.7 Billion

|

|

Market Growth Rate

|

14.3%

|

|

Segments

|

By Technology (IoT-Enabled Monitoring & Control, AI & Machine Learning Solutions, Automation & Robotics, Digital Twin Systems), By System Component (Smart Sensors & Meters, Edge Computing Devices, Control Valves & Actuators, Centralized SCADA Systems, AI Software Platforms), By Application (Water Quality Management, Demand & Supply Optimization, Customer Engagement), By Treatment Stage (Raw Water Intake Monitoring, Process Control in Treatment Plants, Distribution Network Management, Wastewater Treatment Optimization), By End-User (Municipal Water Utilities, Industrial Facilities, Commercial Buildings, Agricultural Operations), By Deployment (Cloud-Based Solutions, On-Premise Systems, Hybrid Deployments)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., SUEZ, Pentair, Evoqua Water Technologies (now part of Xylem), IBM, Siemens, Trimble Inc., Itron Inc., Badger Meter, Honeywell International Inc., Schneider Electric, Oracle

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Smart Water Treatment Systems Market Segmentation

By Technology

- IoT-Enabled Monitoring & Control

- Real-time Sensors

- Wireless Data Transmission

- Cloud-Based Analytics Platforms

- AI & Machine Learning Solutions

- Predictive Maintenance Algorithms

- Anomaly Detection for Leaks/Contamination

- Optimization Models for Chemical Dosing

- Automation & Robotics

- Autonomous Sampling Drones

- Self-Cleaning Membrane Systems

- Robotic Pipe Inspectors

- D. Digital Twin Systems

By System Component

- Smart Sensors & Meters

- Edge Computing Devices

- Control Valves & Actuators

- Centralized SCADA Systems

- AI Software Platforms

By Application

- Water Quality Management

- Demand & Supply Optimization

- Customer Engagement

By Treatment Stage

- Raw Water Intake Monitoring

- Process Control in Treatment Plants

- Distribution Network Management

- Wastewater Treatment Optimization

By End-User

- Municipal Water Utilities

- Industrial Facilities

- Commercial Buildings

- Agricultural Operations

By Deployment

- Cloud-Based Solutions

- On-Premise Systems

- Hybrid Deployments

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Smart Water Treatment Systems Market

- Veolia

- Xylem Inc.

- SUEZ

- Pentair

- Evoqua Water Technologies (now part of Xylem)

- IBM

- Siemens

- Trimble Inc.

- Itron Inc.

- Badger Meter

- Honeywell International Inc.

- Schneider Electric

- Oracle

* List Not Exhaustive

Research Coverage

This report investigates the Global Smart Water Treatment Systems Market, providing in-depth analysis reviews of technological breakthroughs, regulatory shifts, and competitive strategies shaping the sector between 2025 and 2034. Published by USDAnalytics, the study highlights how AI-driven operational intelligence, IoT-enabled monitoring, and digital twin simulations are revolutionizing water management for utilities and industries. It further explores strategic imperatives such as cybersecurity frameworks, blockchain-enabled monitoring, and 5G-enabled smart metering. Supported by detailed insights into strategic acquisitions, product innovations, and infrastructure modernization initiatives worldwide, this report is an essential resource for water utilities, industrial operators, investors, and policymakers seeking to navigate the fast-evolving digital water landscape.

Scope Includes:

- Segmentation: By Technology (IoT & Monitoring, AI & Machine Learning, Blockchain, Edge Computing, Smart Sensors, SCADA, Cloud/On-Premise Deployment); By System Enablers (Smart Sensors, SCADA, AI Platforms, Edge Devices); By Applications (Water Quality Management, Demand Optimization, Distribution Management); By Treatment Stage (Process Control, Network Management, Wastewater Optimization, Raw Water Monitoring); By End-Use (Municipal, Industrial, Commercial, Agricultural).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021 to 2024 and Forecast Data: 2025 to 2034.

- Companies: Profiles and competitive analysis of 15+ leading players including Veolia, SUEZ, Xylem, Pentair, Innovyze (Autodesk), Bentley Systems, and others.

Methodology

The methodology adopted by USDAnalytics combines primary interviews with industry stakeholders—including utilities, technology developers, regulators, and industrial end-users—with secondary research drawn from government policies, scientific publications, corporate disclosures, and international water projects. Market sizing was calculated using both top-down and bottom-up approaches, with triangulation based on adoption rates of IoT devices, AI platforms, and smart metering deployments. Forecast models were stress-tested across multiple scenarios, including accelerated smart city initiatives, stricter PFAS and non-revenue water regulations, and the rollout of 5G-enabled water infrastructure. This rigorous approach ensures robust, actionable intelligence for decision-makers across the water treatment ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Smart Water Treatment Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Stakeholders

1.3. Global Market Snapshot

2. Market Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.4 Billion

2.2.2. Forecasted Market Size (2034): $4.7 Billion at 14.3% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Rising Adoption of AI-driven Operational Intelligence

2.3.2. Proliferation of IoT-enabled Smart Sensors

2.3.3. Integration of Digital Twin Technology for Predictive Analysis

2.3.4. Cybersecurity Risks and Mitigation Strategies

3. Market Analysis: Strategic Moves, Investments, and Technological Shifts

3.1. Overview of Accelerated Innovation and Market Consolidation

3.2. Strategic Developments of Key Players

3.2.1. H2O America's Acquisition and Infrastructure Modernization Plan

3.2.2. SUEZ and Vodafone's Global Alliance for Smart Metering

3.2.3. Veolia's AI-Powered Hubgrade Platform

3.2.4. Xylem's Acquisition of Idrica and Rivo™ I System Launch

3.3. Key Infrastructure Projects and Long-Term Contracts

4. Trends and Opportunities in Smart Water Treatment Systems

4.1. Trend 1: AI-Powered Predictive Maintenance

4.1.1. Anticipating Equipment Failures and Reducing Downtime

4.1.2. Optimizing Energy Consumption and Operational Efficiency

4.2. Trend 2: Blockchain-Enabled Water Quality Monitoring

4.2.1. Ensuring Secure and Transparent Data for Public Trust

4.2.2. Automated Compliance and Regulatory Enforcement via Smart Contracts

4.3. Opportunity 1: Edge Computing for Real-Time Contaminant Detection

4.3.1. Low-Latency Data Processing for Rapid Response

4.3.2. Enhanced Network Resilience and Operational Reliability

4.4. Opportunity 2: 5G-Enabled Smart Metering for Leak Prevention

4.4.1. Ultra-Low Latency for Real-Time Monitoring

4.4.2. Significant Reduction in Non-Revenue Water (NRW) Losses

5. Smart Water Treatment Systems Market Share Insights

5.1. By Technology

5.1.1. IoT-Enabled Monitoring & AI

5.1.2. Automation & Robotics

5.1.3. Digital Twin Systems

5.2. By System Component

5.2.1. Smart Sensors & Meters, SCADA Systems, and AI Software Platforms

5.3. By Application

5.3.1. Water Quality Management and Demand & Supply Optimization

5.4. By Treatment Stage

5.4.1. Process Control and Distribution Network Management

5.5. By End-User

5.5.1. Municipal Water Utilities and Industrial Facilities

5.6. By Deployment

5.6.1. Cloud-Based vs. On-Premise vs. Hybrid Solutions

6. Country Analysis of the Smart Water Treatment Systems Market

6.1. United States: AI-Driven Infrastructure Modernization

6.2. China: Policy-Driven Urban Water Management

6.3. India: IoT-Enabled Rural and Urban Initiatives

6.4. Singapore: National Smart Water Network and Security

6.5. Germany: Integrated Smart Systems and Circular Economy

6.6. United Arab Emirates: Smart Water Management in a Water-Scarce Region

6.7. Other Country Analysis

7. Competitive Landscape: Technology Leaders Shaping the Smart Water Future

7.1. Veolia Environnement S.A.

7.2. SUEZ S.A.

7.3. Xylem Inc.

7.4. Pentair

7.5. Evoqua Water Technologies (now part of Xylem)

7.6. IBM

7.7. Siemens

7.8. Trimble Inc.

7.9. Itron Inc.

7.10. Badger Meter

7.11. Honeywell International Inc.

7.12. Schneider Electric

7.13. Oracle

7.14. Other Key Companies

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. By Technology

8.1.2. By System Component

8.1.3. By Application

8.1.4. By Treatment Stage

8.1.5. By End-User

8.1.6. By Deployment

8.2. Europe Market Size Outlook to 2034

8.2.1. By Technology

8.2.2. By System Component

8.2.3. By Application

8.2.4. By Treatment Stage

8.2.5. By End-User

8.2.6. By Deployment

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. By Technology

8.3.2. By System Component

8.3.3. By Application

8.3.4. By Treatment Stage

8.3.5. By End-User

8.3.6. By Deployment

8.4. South America Market Size Outlook to 2034

8.4.1. By Technology

8.4.2. By System Component

8.4.3. By Application

8.4.4. By Treatment Stage

8.4.5. By End-User

8.4.6. By Deployment

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. By Technology

8.5.2. By System Component

8.5.3. By Application

8.5.4. By Treatment Stage

8.5.5. By End-User

8.5.6. By Deployment

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations