Water and Wastewater Treatment Equipment Market Overview

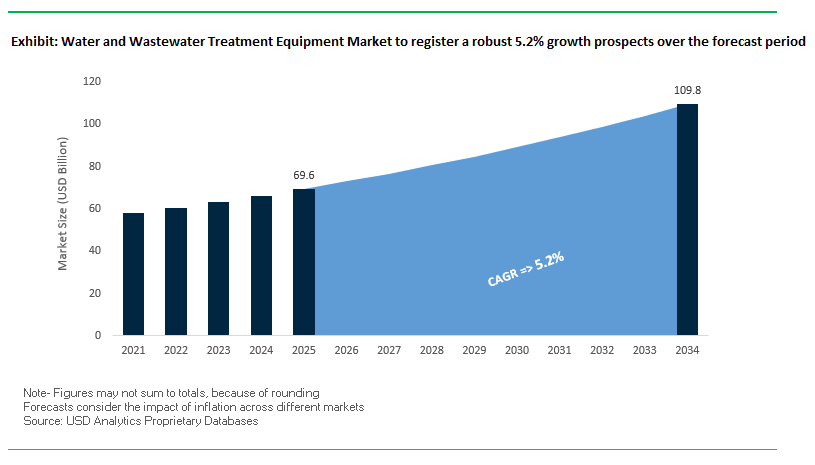

The global water and wastewater treatment equipment market is projected to grow from USD 69.6 billion in 2025 to USD 109.8 billion by 2034, registering a steady CAGR of 5.2%. The growth is driven by a combination of stringent environmental regulations, rapid technological advancements, and heightened awareness of water reuse as a sustainable resource management strategy. Governments and utilities are increasingly prioritizing advanced water treatment solutions to meet regulatory discharge standards, modernize aging infrastructure, and combat water scarcity challenges. For instance, the commissioning of the Thames Tideway Tunnel in early 2025 marks a significant investment in preventing untreated sewage discharge into London’s River Thames, reflecting the market’s role in large-scale infrastructure upgrades. Moreover, the industry is experiencing a paradigm shift from traditional treatment methods to cutting-edge membrane filtration, UV disinfection, and IoT-enabled smart monitoring systems, enabling higher operational efficiency and resource recovery. As climate change accelerates water scarcity and demand intensifies from industrial, municipal, and agricultural sectors, the market outlook for water and wastewater treatment equipment is set to remain robust, with notable growth in water reuse and circular economy applications.

Key Insights for Industry Professionals

- Regulatory Pressure as a Catalyst – Enforcement of strict effluent discharge standards is pushing utilities and industries toward high-efficiency treatment systems.

- Shift to Smart and Sustainable Solutions – Integration of IoT, data analytics, and advanced filtration is driving operational efficiency.

- Aging Infrastructure Driving Capex – Large investments are planned for modernization and expansion in both developed and emerging markets.

- Water Reuse as a Priority – Circular water economy principles are fostering demand for wastewater recycling equipment in agriculture and industrial manufacturing.

In-Depth Market Analysis and Recent Industry Developments

The water and wastewater treatment equipment industry is at the cusp of a great transformation driven by the intersection of environmental stewardship, intelligent technology incorporation, and new business models. Industry leaders are addressing water stress globally by moving their portfolios forward with new treatment technologies, acquisitions, and alliances that bolster strength within municipal, industrial, and domestic segments. Movement from traditional processes to membrane bioreactors, advanced oxidation technologies, and nanotechnology-based filtration technologies is opening up new prospects and room for growth for suppliers, particularly as regulatory commissions continue to increase requirements for treatment of rising contaminants like PFAS. Significant capital projects such as H2O America investing $540 million in July 2025 acquiring Quadvest and upgrading water infrastructure within the city of Houston are testaments of the industry's long-term intention of replacing aged infrastructure based on sustainability and dependability.

Recent acquisitions and mergers are redefining the competitive landscape. Veolia purchased the final 30% of Water Technologies and Solutions (WTS) in July 2025 at $1.75 billion, bringing operational control together for efficiency and cost synergies by 2027. Likewise, Solenis and NCH Corporation merged in June 2025 to form a more diversified global water treatment and hygiene solutions provider with greater penetration of the mid-market. Strategic acknowledgment of innovation is also being seen, such as when Pentair's Everpure PFAS Reduction Systems and Manitowoc Ice NEO ice machine were recognized with Kitchen Innovations Awards in April 2025 and highlighted market interest in addressing "forever chemicals" and end-user efficiency.

Partnerships in technologies and infrastructure contracts are supporting industry growth momentum. In December 2024, SUEZ won a €1.4 billion, 20-year waste-to-energy concession contract at France-based waste management facilities with integrated water and energy recovery concepts. September 2024 witnessed Xylem announcing an anaerobic membrane bioreactor (AnMBR) via a strategic alliance with the objective of resource recovery through biogas production. M&A action is equally robust, with Pentair acquiring Porous Media in October 2024 with the objective of building out filtration and separation technologies and Solenis investing $193 million in February 2024 in the expansion of Virginia polymer facilities. Long-range R&D investment, like Danaher's Beacons program (2022-2023), continues shaping innovation roadmaps, and the sector is better prepared both now and tomorrow to address water quality issues.

Key Market Trends Driving Technological Transformation

Accelerating Adoption of Electrochemical Water and Wastewater Treatment Technologies

The global water and wastewater treatment equipment market is experiencing a watershed movement from conventional chemical-based methodologies toward electrochemical treatment technologies providing precise, sustainable, and chemical-free contaminant removal. Industry growth is initiated based on the technology itself being able to diminish sludge formation, toxic by-product formations, and operational expenditures through automation. Businesses such as Current Water Technologies have moved from prototyping and engineering development toward full-scale commercialization with recent shipments of electrochemical water treatment equipment to industrial end-users within mining, metals, and municipal wastewater. Peer-reviewed articles within the Global NEST Journal validate the popularity of electrochemical methodologies, demonstrating up to 99% turbidity, BOD, and microbial loading removals within hospital wastewater effluent using limited dosing of heavy chemicals. Further incorporation of solar and wind sources of renewables within electrocoagulation and electro-oxidation facilities makes these technologies a cornerstone of future net-zero water infrastructure.

Membrane Bioreactor (MBR) Technology Taking the Lead in Municipal Wastewater Plant Upgrades

MBR technologies are quickly becoming the norm for municipal wastewater treatment facility upgrades, providing high-capability biological treatment and membrane filtration within a small footprint. Higher biomass concentrations are possible than with conventional activated sludge treatment and significantly smaller land use is possible, making it a big advantage where space is at a premium. According to the U.S. EPA, MBRs replace secondary clarifiers and sand filters so both greater treatment capacity and higher effluent quality are possible within the same or smaller space. Because the membranes are a physical barrier, water leaving the system is pathogen-free and solids-free and can go directly into reuse applications like agricultural irrigation and landscape watering. Around the world, high-profile municipal MBR applications ranging from Stockholm city upgrades to Beijing treatment centers with advanced technologies cement growing use of the technology as cities confront tighter water quality controls and water supply issues.

High-Growth Opportunities Shaping the Competitive Landscape

Industrial Zero Liquid Discharge (ZLD) Systems as a Regulatory and ESG Imperative

Zero Liquid Discharge (ZLD) growth in heavy industries is one of the strongest growth prospects within the water treatment space. Governments are increasingly making ZLD mandatory for water-conductive industries like textiles, chemicals, and power plants in water-scarce nations like India, where the Central Pollution Control Board made ZLD norms mandatory within industrial centers like Surat to avoid effluent dumping. Even the economics of ZLD is strong: World Bank case histories show projects where water reuse revenues paid full operating costs and recovered capital expenditures within five years. Innovations are making ZLD feasible on increasingly complex industrial effluents where new and improved RO, electrodialysis (ED), and membrane distillation (MD) are lowering the energy footprint and extending their use to high-saline streams.

Modular and Containerized Treatment Systems for Disaster Response and Infrastructure Resilience

As the impact of climate change and deteriorating infrastructure elevates the need for emergency intervention, demand is growing for modular, containerized water treatment units. Portable, multi-technology water purification with options for alternative power is available with technologies such as the U.S. EPA's Water-on-Wheels (WOW Cart), and water can be safely delivered within hours of flooding or hurricanes or when contaminants are introduced. Beyond the emergency context, modular units are being used as scaleable infrastructure solutions when deployed to remote communities and temporary installations when plants are being refurbished. Current Opinion in Environmental Sustainability has reported industry research promoting modular water systems as a long-term decentralized approach improving urban water security when integrated, variably flexibly, with centralised networks and new developments like atmo-pheric water harvesting.

Water and Wastewater Treatment Equipment Market Share Insights

Market Share by Equipment Type: Water Treatment Equipment Maintains Leadership While Wastewater Gains Momentum

In 2025, water treatment equipment is projected to command nearly 56.3% of the global market share, driven by consistent demand for potable water in both municipal and industrial sectors. The category includes critical infrastructure for purification, desalination, and advanced filtration, underpinning growth in regions facing water stress. However, wastewater treatment equipment, representing about 45% of the market, is forecast to outpace in growth rate due to intensifying environmental regulations, industrial expansion, and water reuse mandates. Within the mix, membrane filters and reverse osmosis systems remain pivotal revenue drivers, particularly as industries such as pharmaceuticals, power generation, and food & beverage depend on ultra-pure water.

.png)

Market Share by Application: Municipal Contracts Dominate While Industrial Wastewater Treatment Expands

The municipal segment is expected to secure around 38.7% of the global market share in 2025, reflecting large-scale contracts for water purification and wastewater infrastructure upgrades across urbanizing regions. These projects are long-term and capital-intensive, forming a stable revenue base for OEMs and EPC contractors. Meanwhile, industrial wastewater treatment accounts for approximately 34.9%, offering higher value per installation due to its complexity. Sub-sectors such as power generation and petrochemicals demand advanced technologies like AOPs, demineralization units, and high-capacity biological treatment, while food and beverage industries rely on robust filtration and biological systems to manage high organic loads. Residential adoption remains a smaller share at 14.9%, yet shows resilience as POU and POE systems gain traction in cities with poor water quality.

Market Share by Technology: Membrane Systems Anchor the Global Water and Wastewater Treatment Market

Membrane technologies are projected to capture about 31.6% of the global market by 2025, cementing their role as the backbone of modern water and wastewater treatment. RO, UF, NF, and MBR solutions have become indispensable for industries requiring high-purity standards and for municipalities adopting advanced reuse strategies. Biological treatment systems, accounting for 26.7%, continue as the most cost-effective method for nutrient and organic waste removal in large-scale plants, with MBR technology seeing rapid adoption. Physical processes such as screening, sedimentation, and sand/carbon filtration remain fundamental with a 17.6% share, while chemical treatment and advanced oxidation processes (AOPs) contribute 15%, critical for meeting emerging micropollutant discharge limits.

Market Share by Sales Channel: Direct B2B Sales Dominate, Supported by Dealers and Online Growth

With nearly 58.7% share in 2025, direct B2B sales remain the dominant channel, particularly for large municipal and industrial projects where engineering design, installation, and after-sales support are critical. The direct engagement also helps equipment manufacturers secure long-term service contracts, which are often as lucrative as the equipment itself. Distributors and dealers, accounting for 31.6%, are essential for expanding regional reach, especially for standardized products and replacement parts where local presence matters. While still modest at 11.4%, e-commerce and online sales are gaining traction for smaller equipment categories such as pumps, UV disinfection units, and replacement cartridges, signaling a shift in how the aftermarket is served.

Market Share by Scale of Operation: Large-Scale Systems Drive Revenue but Medium-Scale Projects Widen Accessibility

In terms of operational scale, large-scale systems dominate with about 51.4% of the global market share, fueled by municipal water treatment plants and major industrial installations with multibillion-dollar contract values. These projects demand high-capacity filtration, sludge handling, and disinfection technologies, making them the most lucrative revenue stream for global OEMs. Medium-scale systems, with a 35% share, represent a highly versatile segment covering mid-sized industries, large commercial complexes, and smaller municipalities, often relying on packaged plant solutions. Meanwhile, small-scale decentralized systems at 15% are emerging as a niche but critical market, addressing rural communities and localized treatment challenges through modular, containerized solutions that align with distributed infrastructure trends.

Country Analysis of the Water and Wastewater Treatment Equipment Market

United States: Expanding Advanced Water Treatment Capabilities

The United States is a vital market for water and wastewater treatment equipment due to high federal investment and innovation. Bipartisan Infrastructure Law invested over $50 billion upgrading national drinking water and wastewater infrastructure and stimulating demand for new treatment technologies and equipment. Key industry leaders are increasingly building up their footprints: A.O. Smith Corporation strengthened its home market via acquisitions of Atlantic Filter of Florida (2022) and Master Water Conditioning Corporation of Pennsylvania (2021), and Xylem Inc. purchased Evoqua to extend its North American and European market positions. R&D projects are remodeling the market; Clemson University has patented a coated carbon nanotube-based saltwater deionization method that enhances salt adsorption and decreases energy consumption and University of North Carolina at Charlotte announced NanoResin materials to optimize organic matter elimination. Industrial developments are improving too, with DuPont announcing new FilmTec™ Fortilife™ membrane grades (CR100, XC70, XC120HR, and XC160), improving brine concentration and energy efficiency within wastewater treatment. This blend of regulatory encouragement, innovation, and corporate growth makes the U.S. a top market for water and wastewater treatment equipment uptake.

China: Regulatory Push and Industrial-Driven Market Growth

China's water and wastewater treatment equipment market is growing tremendously under strict environmental laws and increasing industrialization. Government norms now enforce strong effluent treatment at the municipal and industrial levels, triggering high demand for latest equipment. SUEZ, the global giant, formed a joint venture partnership with Shandong Public to establish and run an industrial wastewater treatment facility at the Jining New Materials Industrial Park, with 100% wastewater recycling using state-of-the-art technology. Moreover, China is investing considerably on bioelectrochemical systems (BES), treating wastewater and producing energy simultaneously and promoting environmental sustainability and operational effectiveness. Fast industrial growth, especially at manufacturing centers, is further boosting use of high-end water treatment solutions and making China a very attractive market offering domestic and foreign equipment suppliers great business prospective.

India: Government Initiatives and Innovation Driving Market Expansion

India’s water and wastewater treatment equipment market is witnessing accelerated growth due to large-scale government programs and innovative technology adoption. Initiatives like the Jal Jeevan Mission and Namami Gange program are major drivers, exemplified by the 14 MLD Sewage Treatment Plant in Baghpat, Uttar Pradesh, and the planned 220 MLD STP in Meerut. Indian companies are leveraging advanced technologies to meet demand: Enviro Infra Engineers secured a ₹395.5 crore project from MIDC to implement Zero Liquid Discharge (ZLD) solutions using RO, UF, and MVR technologies, while Technocraft Ventures manages an order book valued at ₹685.83 crore across AMRUT and Namami Gange projects. Startups like Earthy are pioneering biomimetic membrane technologies, branded as “Aquaporin Inside,” which use aquaporin proteins to efficiently transport water, offering highly sustainable solutions. Larsen & Toubro’s Water Business Group continues to execute large-scale infrastructure projects, including drinking water supply schemes and wastewater management systems. Collectively, these initiatives and technological innovations are expanding India’s market for advanced water and wastewater treatment equipment.

Germany: Sustainability and High-Tech Adoption in the European Market

Germany’s water and wastewater treatment equipment market is among Europe’s most advanced, driven by strict environmental regulations and a strong focus on sustainability. The market is witnessing widespread adoption of advanced technologies, including membrane filtration and energy-efficient treatment systems, particularly in industrial and municipal applications. Germany’s ambitious climate targets, aligned with the Paris Agreement, are prompting investments in solutions that improve water quality and reduce energy consumption in treatment processes. Companies are increasingly focusing on pollutant reduction technologies, positioning Germany as a leader in adopting environmentally responsible and technologically sophisticated water treatment equipment.

Japan: Innovation and Specialized Water Treatment Solutions

Japan’s water and wastewater treatment equipment market emphasizes advanced technological development and innovative solutions. Kurita Water Industries is spearheading initiatives such as a partnership with lunar exploration company ispace to transport a water purification demonstration system to the moon after 2027, showcasing expertise in highly specialized environments. Additionally, Kurita’s collaboration with Imagine H2O, a water innovation accelerator, provides startups access to R&D and pilot facilities at the Kurita Innovation Hub, facilitating the commercialization of advanced water solutions. Opened in 2022, the Kurita Innovation Hub serves as a living laboratory for testing new water treatment technologies, reinforcing Japan’s position at the forefront of water treatment innovation.

Israel: Leadership in Desalination and Efficient Water Reuse

Israel has established itself as a global leader in seawater desalination and innovative water treatment equipment adoption. IDE Water Technologies’ Sorek 2 – Be'er Miriam Desalination Plant, operational in March 2025, is the world’s first large-scale steam-driven seawater reverse osmosis (SWRO) facility, exemplifying technological advancement in energy-efficient desalination. Israel also maintains significant capacity through the Sorek I and Hadera plants, highlighting the nation’s commitment to advanced water treatment and water reuse initiatives. These projects underscore Israel’s role as a key market for high-efficiency and innovative water treatment equipment, serving as a model for sustainable water management globally.

Competitive Landscape of the Global Water and Wastewater Treatment Equipment Market

The competitive landscape of the water and wastewater treatment equipment industry is defined by multinational corporations with diverse product portfolios, strong R&D pipelines, and global operational reach. These companies are leveraging acquisitions, partnerships, and technological innovations to expand capabilities in membrane filtration, digital water management, and advanced disinfection systems. Strategic focus areas include circular water economy adoption, tackling emerging contaminants, and modernizing critical water infrastructure.

Xylem Inc. – Integrating Digital Intelligence into Water Management

The Xylem brand family of Flygt, Sanitaire, and Leopold is known for its knowledge in municipal, industrial, and residential applications within over 150 nations. It extended its next-level treatment expertise with the 2023 purchase of Evoqua Water Technologies. It is pushing data-driven water utility optimization with its Xylem Vue platform and "smart sewer" system that enable lowering operating expenses and bolstering resilience against climate-motivated disruption. It has products ranging from pumps and valves to filtration and disinfection equipment with a special emphasis on smart infrastructure solutions.

Veolia Environnement S.A. – Expanding Ecological Transformation Capabilities

Veolia operates in water, waste, and energy and provides holistic environmental solutions. Veolia's July 2025 acquisition of the WTS residual interest solidifies its control of operations and secures its global water technologies leadership. Veolia's solutions encompass drinking water production, wastewater reuse and industrial water management solutions accompanied by technologies like "BeyondPFAS" applied for contaminant remediation. Veolia's solutions are designed towards cross-functional environmental solutions addressing complex regulatory and sustainability problems.

SUEZ S.A. – Driving Circular Water and Waste Solutions

SUEZ integrates infrastructure development expertise with digital water technologies leadership and addresses both mature and new markets. Through its operations in more than 40 countries, it supplies drinking water to 57 million and sanitation solutions to more than 36 million. Its December 2024 €1.4 billion France concession contract highlights its interest in the water-energy nexus and the recovery of resources. SUEZ invests significantly in R&D and deals with polluters, water protection enhancement, and green energy creation from waste.

Pentair plc – Innovating in Sustainable Residential and Industrial Solutions

Pentair’s purpose-driven strategy focuses on delivering smart, sustainable water solutions to home, commercial, and industrial end customers, Pentair is recognized in April 2025 with its Everpure PFAS Reduction Systems and Manitowoc Ice NEO ice machine. Pentair leads with solutions designed to tackle water contaminants of tomorrow. Through acquisitions of Porous Media in October 2024, it builds out its portfolio of separations and filtration and cements its market leadership. Its end-to-end solutions from pool equipment to industrial valves are driven first by energy efficiency and then networked solutions.

Danaher Corporation – Advancing Precision Water Quality Technologies

Water quality platform is at the core of Danaher mission of advancing science and technology for human health. Subsidiary Hach is at the forefront of chemical and analytical solutions for water and wastewater with its precision instruments and next-generation purification technologies. Beacons program (2022-2023) is Danaher's long-term investment in innovation with research feeding into next-gen water quality breakthroughs. Its solutions are applicable to environmental, municipal, commercial, and industrial use, making it possible to ensure regulatory compliance and protect public health.

Water and Wastewater Treatment Equipment Market Report Scope

Water and Wastewater Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$69.6 Billion

|

|

Market Size (2034)

|

$109.8 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Water Treatment Equipment (Filtration Systems, Reverse Osmosis (RO) Systems, Disinfection Equipment, Water Softeners & Ion Exchange Systems, Distillation Units, Electrodialysis & Electrodeionization (EDI) Systems), By Wastewater Treatment Equipment (Primary Treatment, Secondary Treatment, Tertiary/Advanced Treatment, Sludge Treatment Equipment), By Application (Municipal Water & Wastewater Treatment, Industrial Wastewater Treatment, Residential, Recycling & Reuse Systems), By Technology (Physical Treatment, Chemical Treatment, Biological Treatment, Membrane Technology, Advanced Oxidation Processes (AOPs)), By Sales Channel (Direct Sales, Distributors & Dealers, E-commerce & Online Retail), By Scale of Operation (Small-Scale Systems, Medium-Scale Systems, Large-Scale Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., Ecolab, SUEZ, Pentair, DuPont, Kurita Water Industries, VA Tech WABAG Ltd., Thermax Limited, Aquatech International LLC, Calgon Carbon Corporation, GE Water & Process Technologies (now part of SUEZ and others), Culligan Water, Hindustan Dorr-Oliver Ltd., Grundfos Holding A/S

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water and Wastewater Treatment Equipment Market Segmentation

By Water Treatment Equipment

- Filtration Systems

- Sand Filters

- Activated Carbon Filters

- Membrane Filters

- Reverse Osmosis (RO) Systems

- Disinfection Equipment

- UV Purifiers

- Ozonation Systems

- Chlorination Systems

- Water Softeners & Ion Exchange Systems

- Distillation Units

- Electrodialysis & Electrodeionization (EDI) Systems

By Wastewater Treatment Equipment

- Primary Treatment

- Screens & Grit Chambers

- Sedimentation Tanks

- Secondary Treatment

- Activated Sludge Process (ASP)

- Biological Filters (Trickling Filters, MBBR, MBR)

- Sequencing Batch Reactors (SBR)

- Tertiary/Advanced Treatment

- Membrane Bioreactors (MBR)

- Advanced Oxidation Processes (AOP)

- Chemical Precipitation

- Sludge Treatment Equipment

- Centrifuges

- Belt Filter Presses

- Sludge Dryers

By Application

- Municipal Water & Wastewater Treatment

- Industrial Wastewater Treatment

- Oil & Gas

- Food & Beverage

- Pharmaceuticals

- Chemicals & Petrochemicals

- Power Generation

- Pulp & Paper

- Textiles

- Residential

- Recycling & Reuse Systems

By Technology

- Physical Treatment

- Chemical Treatment

- Biological Treatment

- Membrane Technology

- Advanced Oxidation Processes (AOPs)

By Sales Channel

- Direct Sales (B2B – Industrial Contracts)

- Distributors & Dealers

- E-commerce & Online Retail

By Scale of Operation

- Small-Scale Systems

- Medium-Scale Systems

- Large-Scale Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water and Wastewater Treatment Equipment Market

- Veolia

- Xylem Inc.

- Ecolab

- SUEZ

- Pentair

- DuPont

- Kurita Water Industries

- VA Tech WABAG Ltd.

- Thermax Limited

- Aquatech International LLC

- Calgon Carbon Corporation

- GE Water & Process Technologies (now part of SUEZ and others)

- Culligan Water

- Hindustan Dorr-Oliver Ltd.

- Grundfos Holding A/S

* List Not Exhaustive

Research Coverage

This report investigates the Global Water and Wastewater Treatment Equipment Market, offering comprehensive analysis reviews of industry dynamics, technology breakthroughs, regulatory drivers, and strategic investments shaping the sector. Developed by USDAnalytics, the study highlights how the convergence of environmental compliance, infrastructure modernization, and advanced filtration technologies is transforming municipal, industrial, and residential water systems worldwide. It also tracks mergers, acquisitions, and innovation pipelines that are redefining competitive positioning, from electrochemical systems to membrane bioreactors and IoT-enabled smart monitoring. As utilities, governments, and industries prioritize water reuse and resource recovery, this report is an essential resource for decision-makers, policymakers, engineers, and corporate strategists seeking actionable insights into long-term growth opportunities and risks across global markets.

Scope Includes:

- Segmentation: By Equipment Type (Water Treatment, Wastewater Treatment), Application (Municipal, Industrial, Residential), Technology (Membrane Systems, Biological, Physical, Chemical & AOPs), Sales Channel (Direct, Dealers, Online), and Scale of Operation (Large, Medium, Small)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa

- Timeframe: Historic data from 2021–2024 and forecast data from 2025–2034

- Companies: Competitive profiling and analysis of 15+ leading companies in the market

Methodology

The research methodology applied by USDAnalytics combines primary and secondary research to ensure data accuracy and market reliability. Primary inputs were collected through structured interviews with manufacturers, utilities, EPC contractors, regulators, and technology providers across multiple geographies. Secondary data was sourced from annual reports, regulatory publications, academic research, government databases, and trade journals. Market sizing was developed using top-down and bottom-up modeling approaches, supported by data triangulation, sensitivity analysis, and scenario forecasting. Expert validation further ensured the robustness of projections, making the report a dependable reference for strategic planning, investment decisions, and policy development in the Water and Wastewater Treatment Equipment Market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Water and Wastewater Treatment Equipment Market Landscape & Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $69.6 Billion

2.2.2. Forecasted Market Size (2034): $109.8 Billion at 5.2% CAGR

2.3. Strategic Drivers & Key Insights

2.3.1. Regulatory Pressure as a Catalyst

2.3.2. Shift to Smart and Sustainable Solutions

2.3.3. Aging Infrastructure Driving Capex

2.3.4. Water Reuse as a Priority

3. In-Depth Market Analysis and Recent Industry Developments

3.1. Overview of Market Transformation

3.2. Recent Acquisitions and Mergers

3.2.1. Veolia's Acquisition of Water Technologies and Solutions (WTS)

3.2.2. Solenis's Merger with NCH Corporation

3.3. Strategic Partnerships and Contracts

3.3.1. SUEZ's Waste-to-Energy Concession Contract

3.3.2. Xylem's Anaerobic Membrane Bioreactor (AnMBR) Alliance

3.4. R&D and Capital Investments

3.4.1. H2O America's Infrastructure Upgrades

3.4.2. Pentair's Acquisition of Porous Media

3.4.3. Solenis's Polymer Facility Expansion

4. Key Market Trends Driving Technological Transformation

4.1. Accelerating Adoption of Electrochemical Treatment Technologies

4.1.1. Benefits of Electrochemical Methods

4.1.2. Commercialization by Key Players

4.2. Membrane Bioreactor (MBR) Technology

4.2.1. Advantages in Municipal Wastewater Treatment

4.2.2. Global Municipal Applications

4.3. High-Growth Opportunities

4.3.1. Industrial Zero Liquid Discharge (ZLD) Systems

4.3.2. Modular and Containerized Treatment Systems

5. Market Share and Segmentation Insights

5.1. By Equipment Type

5.1.1. Water Treatment Equipment

5.1.2. Wastewater Treatment Equipment

5.2. By Application

5.2.1. Municipal

5.2.2. Industrial

5.2.3. Residential

5.3. By Technology

5.3.1. Membrane Technology

5.3.2. Biological Treatment

5.3.3. Physical Treatment

5.3.4. Chemical Treatment and AOPs

5.4. By Sales Channel

5.4.1. Direct B2B Sales

5.4.2. Distributors and Dealers

5.4.3. E-commerce and Online Retail

5.5. By Scale of Operation

5.5.1. Large-Scale Systems

5.5.2. Medium-Scale Systems

5.5.3. Small-Scale Systems

6. Country Analysis and Regional Outlook

6.1. United States: Expanding Advanced Water Treatment Capabilities

6.2. China: Regulatory Push and Industrial-Driven Growth

6.3. India: Government Initiatives and Innovation

6.4. Germany: Sustainability and High-Tech Adoption

6.5. Japan: Innovation and Specialized Solutions

6.6. Israel: Leadership in Desalination and Efficient Reuse

6.7. Other Country Analysis (e.g., UK, France, South Korea, etc.)

7. Water and Wastewater Treatment Equipment Market Size Outlook by Region (2025–2034)

7.1. North America Water and Wastewater Treatment Equipment Market Size Outlook to 2034

7.1.1. By Equipment Type

7.1.2. By Application

7.1.3. By Technology

7.1.4. By Sales Channel

7.1.5. By Scale of Operation

7.2. Europe Water and Wastewater Treatment Equipment Market Size Outlook to 2034

7.2.1. By Equipment Type

7.2.2. By Application

7.2.3. By Technology

7.2.4. By Sales Channel

7.2.5. By Scale of Operation

7.3. Asia Pacific Water and Wastewater Treatment Equipment Market Size Outlook to 2034

7.3.1. By Equipment Type

7.3.2. By Application

7.3.3. By Technology

7.3.4. By Sales Channel

7.3.5. By Scale of Operation

7.4. South America Water and Wastewater Treatment Equipment Market Size Outlook to 2034

7.4.1. By Equipment Type

7.4.2. By Application

7.4.3. By Technology

7.4.4. By Sales Channel

7.4.5. By Scale of Operation

7.5. Middle East and Africa Water and Wastewater Treatment Equipment Market Size Outlook to 2034

7.5.1. By Equipment Type

7.5.2. By Application

7.5.3. By Technology

7.5.4. By Sales Channel

7.5.5. By Scale of Operation

8. Company Profiles: Leading Players in Water and Wastewater Treatment Equipment Market

8.1. Veolia

8.2. Xylem Inc.

8.3. Ecolab

8.4. SUEZ

8.5. Pentair

8.6. DuPont

8.7. Kurita Water Industries

8.8. VA Tech WABAG Ltd.

8.9. Thermax Limited

8.10. Aquatech International LLC

8.11. Calgon Carbon Corporation

8.12. GE Water & Process Technologies (now part of SUEZ and others)

8.13. Culligan Water

8.14. Hindustan Dorr-Oliver Ltd.

8.15. Grundfos Holding A/S

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Methodology: Data Collection & Analysis

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations