Market Overview: Driving Expansion in the Global Tertiary Water & Wastewater Treatment Equipment Market

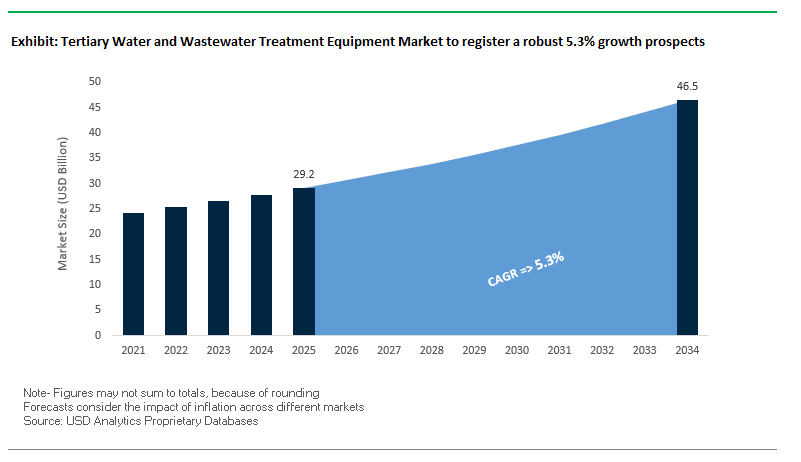

Global tertiary water and wastewater treatment equipment stands at about USD 29.2 billion in 2025 and is anticipated to reach around USD 46.5 billion in 2034 at a solid CAGR of 5.3%. Advanced environmental regulations and stringent mandates for water reuse are pushing cities and industries into implementing state-of-the-art tertiary treatment technology. For example, in Coimbatore, India, a public-private partnership has been initiated to install a tertiary ultrafiltration plant capable of treating and supplying 25 million liters a day of treated water to industries, exemplifying realistic schemes of regulatory compliance integrated with local water reuse aspirations. However, in France, Veolia has been commissioned to equip the largest scheme of treated wastewater reuse in the country in Argelès-sur-Mer and exemplifies surging demand for tertiary systems by locations focusing on mitigation measures against water stress and industrial frameworks on reuse.

Key Strategic Insights for Industry Stakeholders

- Emerging Regulatory Pressure: Intensifying mandates for effluent quality and water reuse, especially concerning micropollutants like PFAS, pharmaceuticals, and pesticides are setting new performance benchmarks.

- Rise of High-Purity Membrane Technologies: Ultrafiltration (UF), nanofiltration (NF), and reverse osmosis (RO) are quickly becoming core to tertiary treatment, enabling pathogen removal, dissolved solids elimination, and potable reuse.

- Membrane-Centric Technological Transition: Increasing reliance on membrane filtration systems not only ensures compliance but also supports efficient removal of contaminants, aligning with sustainability goals.

- Scalable, Modular Deployment Trend: Whether in rapidly urbanizing zones or remote communities, modular and decentralized tertiary systems offer cost-effective, high-performance solutions.

Market Analysis – Regulatory Mandates and Strategic Investments Shift the Tertiary Treatment Sector

Coimbatore completed its tertiary ultrafiltration plant project in August 2025, a milestone in harnessing membrane-based tertiary treatment to provide industrial-grade recycled water. Local initiatives parallel worldwide industry trends, such as in July 2025, when Veolia was awarded a contact to provide tertiary treatment infrastructures for mass-water reuse at Argelès-sur-Mer, France highlight a growing trend in municipal-industrial partnership toward sustainability.

Within the same period, Veolia also completed the acquisition of the remaining 30% of its Water Technologies & Solutions subsidiary, bolstering its integrated treatment capabilities and streamlining access to advanced technologies across its tertiary solutions portfolio. Simultaneously, SUEZ partnered with AgriTech startup Seabex to experiment with biochar applications in agriculture are tying tertiary system byproducts to circular economy practices. Further emphasizing resource recovery, July 2025 witnessed SUEZ inaugurate a biogas unit at Paris’s massive Seine Aval plant, transforming sludge into renewable energy to serve over 6 million residents.

Aside from pure water recovery, Xylem's September 2024 collaboration on a sophisticated anaerobic membrane bioreactor (AnMBR) exemplifies high-grade effluent out of secondary systems supporting tertiary processes such as RO, concluding industry convergence on integrated, resource-efficient chains of treatment. Further, October 2024 witnessed Pentair acquiring Porous Media in a development meant to accelerate advanced filtration solutions critical to stringent tertiary requirements. Modern advances such as membrane integration, energy recovery, and ancillary utilization of byproducts direct the sector's development toward high-performing closed-loop tertiary treatment ecosystems.

Trends and Opportunities in Tertiary Water and Wastewater Treatment Equipment Market

Rapid Adoption of PFAS Destruction Technologies

The tertiary water and wastewater treatment market is undergoing transformative growth due to PFAS's intense regulatory spotlight. Federal authorities have enacted enforceable limits for six PFAS chemicals, such as PFOA and PFOS, at a level of 4.0 parts per trillion, and this has driven municipal and industrial water system investments in advanced treatment strategies by 2029. Spending on PFAS destruction technology has grown briskly, and commercial deployment has begun. One such validation has been made on the "PFAS Annihilator" by Revive Environmental which employs supercritical water oxidation (SCWO) to reach a 99.99% destruction level across all PFAS chemicals. EPA investment of $1 billion under the Infrastructure Investment and Jobs Act has further hastened deployment and testing such that municipalities and commercial operators can achieve stringent compliance levels. SCWO has been accompanied in gaining traction by advanced electrochemical oxidation, plasma treatment technology, and other destruction technology such that a wide range of solutions tailored for use in certain matrices or concentrations of contaminants is available. This market is gaining tremendous strength such that conventional removal methodologies are now supplanted in preference by permanent PFAS mitigation methodologies and hence great marketing opportunities exist for technology providers and system integrators.

Direct Potable Reuse (DPR) Goes Mainstream

Direct Potable Reuse (DPR) is gaining traction as a realistic and increasingly mainstream response to water-scarce areas. DPR consists of treating highly wastewater and injecting it directly into the potable supply system, depending on multi-barrier treatment plants involving microfiltration, reverse osmosis, and advanced oxidation processes (AOPs). Urban centers such as El Paso, Texas, lead DPR efforts within the United States in running pilot and full-scale applications to supplement water supplies sustainably. Internationally, Windhoek, Namibia, has proved DPR's safety and reliability since 1968 by directly blending reclaimed water into potable pipeline streams without inducing reported negative healthcare effects. Economic analysis shows that DPR can be anywhere up to 40% cheaper compared to seawater desalination, especially in desertic locations, while generating economic and sustainability benefits. Multi-barrier treatment facilities provide regulatory compliance and build public trust, boosting wider use within cities, industrial centers, and commercial establishments requiring secure, resilient supplies of water.

Industrial Zero Liquid Discharge (ZLD) Boom

Industrial Zero Liquid Discharge (ZLD) technology is going mainstream thanks to regulatory imperatives and corporate ESG efforts pushing heavy industry to end wastewater discharge. In locations such as Tamil Nadu, India, court rulings and stringent environmental regulations have driven textile dyeing mills to recover in excess of 98% of their waters, illustrating ZLD's transformative ability. Advanced ZLD technology utilizes membrane filtration, evaporation, and crystallization such that not only can waters be recycled but valuable salts and byproducts be recovered and turn streams of waste into streams of revenue. System operating data from Colorado's R.D. Nixon Power Plant demonstrates how deploying ZLD can decrease water-related operating costs up to 50%, illustrating long-term sustainability and economics benefits. Applications around the world continue to utilize ZLD as a compliance and cost-optimization solution, particularly applications high in water usage such as chemicals, textiles, pharmaceuticals, and power.

Ceramic Membranes Displacing Polymers

Ceramic membranes continue to displace polymeric membranes in tertiary treatment, ever more often in high-end industrial applications. Such membranes, constructed out of materials such as silicon carbide (SiC), provide higher strength, chemical stability, and lifespans of operational life between cleaning periods of 10–20 years versus a shorter life cycle of common polymeric equivalents. High-flux and anti-fouling capabilities reduce operational pressures, energy consumption, and cleaning frequencies, ensuring long-term cost-effectiveness. Industrial deployment can be seen in a German xAI data center application of ceramic MBR membranes to treat effluent waters, highlighting a technology's reliability in high-stakes deployments. Adoption of ceramic membranes is part of a wider market trend toward long-life, high-performing tertiary treatment applications that serve both regulatory requirements and operational efficiency objectives.

Tertiary Water & Wastewater Treatment Market Share Insights

Market Share by Type: Filtration Systems Anchor the Market While Reverse Osmosis Drives Strategic Growth

In 2025, filtration systems are projected to capture around 30% of the tertiary water and wastewater treatment equipment market, reinforcing their role as the critical polishing stage in treatment trains. Sand filters, cartridge filters, and especially membrane filtration (MF/UF) remain indispensable in preparing effluent for disinfection or reverse osmosis. Alongside the, advanced treatment technologies such as reverse osmosis (RO) and nanofiltration (NF) account for nearly 28%, representing the strategic growth core of the sector. RO continues to dominate desalination and ultrapure water production, making it a cornerstone for water reuse projects across industrial and municipal markets.

.png)

Market Share by Application: Industrial Sector Dominates While Municipal Demand Surges with Water Reuse

The industrial applications segment leads with an estimated 45% share in 2025, reflecting the high-value demand for ultrapure process water, direct discharge compliance, and in-plant recycling across sectors such as microelectronics, pharmaceuticals, and food & beverage. Customized tertiary systems ften built around RO, ion exchange, and AOPs are essential to meet stringent water quality requirements. On the other side, municipal applications represent about 40% of the market, expanding rapidly due to global water scarcity and growing adoption of water reuse for irrigation and indirect potable supply. The surge is supported by stricter nutrient removal regulations and investments in advanced filtration and disinfection systems for urban utilities.

Market Share by Treatment Objective: Desalination and Pathogen Removal Lead While Micropollutant Control Gains Momentum

Desalination represents roughly 25% of the tertiary treatment market in 2025, cementing its position as a water security driver in arid regions and coastal cities. Reverse osmosis dominates the segment, transforming seawater and brackish sources into reliable freshwater. Meanwhile, pathogen removal, accounting for 20%, remains a non-negotiable pillar of tertiary treatment, with UV disinfection increasingly displacing chlorine due to its chemical-free safety and effectiveness in water reuse. Emerging regulatory pressures are also accelerating growth in organic and micropollutant removal, estimated at 17%, where advanced oxidation processes (AOPs) and granular activated carbon (GAC) are gaining traction to eliminate pharmaceuticals, pesticides, and trace industrial chemicals.

Market Share by End-User: Industrial Sector Generates Highest Revenues While Municipal Investments Accelerate

The industrial sector leads with about 50% of global market revenues, reflecting its reliance on advanced tertiary systems for both compliance and production efficiency. Industries such as power generation, pharmaceuticals, and semiconductors demand high-performance systems tailored for ultrapure water and regulatory discharge standards. The municipal sector, accounting for 40%, is the fastest-growing end-user, fueled by investments in wastewater recycling, nutrient removal upgrades, and large-scale desalination plants. In contrast, the commercial sector, holding around 10%, remains a niche but rising market, with demand driven by large facilities such as resorts, data centers, and hospitals that increasingly install on-site water recycling systems to reduce water consumption and operational costs.

Market Share by System Configuration: Integrated Multi-Technology Trains Dominate While Modular Units Retain Niche Relevance

Integrated tertiary systems are projected to command nearly 70% of the market in 2025, as most advanced treatment facilities rely on multi-stage, fully controlled treatment trains (e.g., MF → RO → UV) to ensure reliability, efficiency, and compliance with stringent discharge or reuse standards. These configurations are especially dominant in large-scale municipal utilities and industrial plants where water reuse and desalination are prioritized. By contrast, stand-alone systems represent about 30%, serving modular or point-of-use needs such as UV disinfection units for wells, small RO systems for process lines, or cartridge filters for particle polishing. The segment remains attractive for niche, decentralized, and cost-sensitive applications.

Country Analysis of the Tertiary Water and Wastewater Treatment Equipment Market

United States: Innovation and Sustainability Driving Tertiary Treatment Adoption

United States is a large market for tertiary water and wastewater treatment solutions due to federal initiatives, innovation in technology, and sustainability targets. The Bipartisan Infrastructure Law has invested more than $50 billion to modernize national drinking water and sewer systems, directly boosting demand for tertiary treatment technologies. Xylem Inc.'s purchase of Evoqua bolsters its portfolio in tertiary wastewater treatment in North America and Europe, while DuPont Water Solutions has been awarded the 2025 BIG Innovation Award due to innovation in membranes and ion exchange resins for sustainable tertiary treatment. DuPont's FilmTec™ nanofiltration membranes was declared "Sustainable Technology of the Year" at the Global Sustainability & ESG Awards due to their application in advanced water reuse applications. Federal Energy Management Program (FEMP) has listed on-site wastewater treatment systems, with tertiary treatment being an essential step in non-potable reuse. Furthermore, A.O. Smith Corporation expanded its local footprint due to key purchases of Atlantic Filter in Florida (2022) and Master Water Conditioning Corporation in Pennsylvania (2021), solidifying the nation's leadership in tertiary water treatment solutions.

India: Government Initiatives and ZLD Projects Fuel Tertiary Treatment Market

India’s tertiary water and wastewater treatment equipment market is growing rapidly, supported by large-scale government programs and technological advancements. The Namami Gange program has sanctioned 488 projects worth over ₹39,730 crore, including a 20 MLD Tertiary Treatment and Reverse Osmosis (TTRO) plant commissioned in Masani, Mathura. Enviro Infra Engineers has secured a ₹395.5 crore Zero Liquid Discharge (ZLD) project in Maharashtra, incorporating tertiary treatment stages for industrial and municipal wastewater. The Central Pollution Control Board (CPCB) has issued new guidelines to expand treated wastewater reuse in agriculture, thermal power, and industrial cooling, boosting demand for tertiary treatment equipment. Larsen & Toubro’s Water Business Group is actively executing large-scale water infrastructure projects, including drinking water supply and wastewater management systems, further strengthening India’s tertiary treatment market and promoting sustainable water reuse.

Israel: Pioneering Water Reuse Through Tertiary Treatment Technology

Israel is a global leader in water reuse, and almost 90% of effluent treated is reused for irrigation. Emphasis has fueled the use of state-of-the-art tertiary water treatment equipment throughout the nation. Israel's largest such installation, the Shafdan Water Recycling Facility, makes use of saturated tertiary treatment in an aquifer and is a research and development site for new water reuse technology. IDE Technologies' Sorek I and Hadera desalination plants include tertiary treatment units to provide assurance in seawater quality prior to desalination. National policy and regulatory encouragement provided by the Israel Water Authority (IWA) solidify the nation's resolve to desalt and reuse waters and provide a powerful domestic market for state-of-the-art tertiary water treatment technology and a strong export market opportunity for new innovative equipment.

China: Policy-Driven Wastewater Recycling and Advanced Tertiary Treatment

China’s tertiary water and wastewater treatment equipment market is expanding under strong government policies and wastewater recycling initiatives. The government aims for 95% coverage for wastewater treatment in county-level cities and promotes the reuse of treated municipal and industrial wastewater. SUEZ, through a joint venture with Shandong Public, is building and operating an industrial wastewater treatment plant in the Jining New Materials Industrial Park, achieving 100% wastewater recycling through tertiary treatment processes. The country is investing heavily in bioelectrochemical systems (BES), which treat wastewater while generating energy, and is emphasizing environmental impact assessments, including greenhouse gas evaluation. These initiatives create significant demand for advanced tertiary treatment equipment capable of supporting energy-efficient and sustainable wastewater management.

Japan: Advanced Tertiary Treatment for Extreme and Resource-Constrained Environments

Japan’s tertiary water and wastewater treatment equipment market emphasizes advanced and specialized solutions, including portable and resource-efficient systems. Kurita Water Industries has partnered with ispace to transport a water purification demonstration system to the moon after 2027, highlighting the use of tertiary treatment technology in extreme environments. Kurita also expanded collaboration with Imagine H2O, a water innovation accelerator, providing startups access to R&D and pilot facilities at the Kurita Innovation Hub to commercialize tertiary treatment solutions. The Ministry of Land, Infrastructure, Transport, and Tourism (MLIT) is promoting resource recycling, converting sewage sludge into fertilizer and energy, applications that rely on tertiary treatment equipment. Japan’s focus on decentralized, resilient, and advanced tertiary treatment systems ensures sustainable water reuse and supports disaster preparedness initiatives.

United Arab Emirates (UAE): Large-Scale Infrastructure Projects Promote Tertiary Treatment

The UAE’s tertiary water and wastewater treatment equipment market is growing due to massive investments in water infrastructure and desalination projects. Veolia is engineering and supplying key technologies for the Hassyan seawater desalination plant in Dubai, integrating tertiary treatment for pretreatment processes. Veolia Water Technologies also delivered the largest Treated Sewage Effluent (TSE) Polishing Plant at Qatar’s Katara Cultural Village, reducing freshwater dependence through advanced tertiary treatment. The Taweelah Desalination Plant, with a capacity of 909,000 m³/day, is among the world’s largest, showcasing the UAE’s commitment to adopting advanced filtration and purification technologies in tertiary water treatment applications. These projects reflect the country’s strategic focus on sustainable water reuse and desalination infrastructure.

Competitive Landscape – Industry Leaders Shaping the Tertiary Water Treatment Frontier

The tertiary water and wastewater treatment equipment arena is characterized by specialized offerings, strategic vertical integration, and a clear pivot toward smart, sustainable treatment models. The market is anchored by industry giants delivering membrane-based disinfection and purification systems, advanced units for micropollutant removal, and modular technologies suitable for localized applications.

Xylem Inc. – Digitalized Tertiary Treatment for Real-Time Optimization

Xylem's tertiary suite from UV and ozone disinfection to AOPs and membrane filtration across its Wedeco and Leopold brands has everything between removal of fine contaminations and control of pathogens. Its use of digital technologies like Xylem Vue allows real-time process control to optimise use of chemicals, energy use, and regulatory compliance. With global reach across municipal and industrial applications, Xylem makes it possible to integrate seamlessly across the cascade of treatment.

Veolia Environnement S.A. – End-to-End Tertiary Ecosystems for Reuse Initiatives

Deriving from such initiatives as the Argelès-sur-MerReuse Centre, Veolia's tertiary treatment range comprises Actiflo®, Spidflow®, membrane solutions, ozonation, and activated carbon technology. Its integrated solution has been boosted by acquiring full ownership of WTS in July 2025. Veolia thrives in optimally designing tertiary systems that operate within larger schemes of reuse and sustainability produce quality water while operating in an energy-efficient manner.

SUEZ S.A. – Circular Tertiary Systems with Resource Recovery

SUEZ brings strong membrane and disinfection capabilities (UF, RO, UV, ozonation) to urban and industrial clients, with digital platforms optimizing tertiary operations. Its stronghold on infrastructure and turnkey project delivery pairs well with innovations like biochar experimentation and city-scale biogas recovery showcases tertiary treatment being fed back into agricultural and energy cycles.

Pentair plc – Advanced Filtration for Clean, Compact Tertiary Solutions

Pentair's tertiary offerings include multimedia, carbon, and ultrafiltration systems within Everpure and Pentek brands. Its acquisition of Porous Media improved filtration expertise, making it highly qualified to meet changing tertiary purity requirements of waters. Its systems include energy-efficient and compact designs and function optimally within decentralized applications or locations where spaces are constrained.

DuPont Water Solutions – High-Purity Membrane Tech for Reuse-Sensitive Functions

DuPont's tertiary strengths consist of new contaminant removal membrane technologies RO (FilmTec ™), NF (Fortilife ™), UF (IntegraTec ™) and ion exchange resins specifically developed for new contaminant removal. State-of-the-art membrane research and development is underway at DuPont's Global Water Technology Center to advance removal and foulability resistance. DuPont engages with utilities and industrial users in implementing integrated high-purity tertiary systems from semiconductor facilities to municipal applications.

Tertiary Water and Wastewater Treatment Equipment Market Report Scope

Tertiary Water and Wastewater Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$29.2 Billion

|

|

Market Size (2034)

|

$46.5 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

Type (Filtration Systems, Advanced Treatment Technologies, Disinfection Systems, Specialized Removal Systems), By Application (Municipal Applications, Industrial Applications, Special Applications), By Treatment Objective (Pathogen Removal, Nutrient Removal, Desalination, Organic Removal, Heavy Metal Removal), By End-User Segment (Municipal Sector, Industrial Sector, Commercial Sector), By System Configuration (Stand-Alone Systems, Integrated Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., Ecolab, DuPont, Pentair, SUEZ, Kurita Water Industries, Calgon Carbon Corporation, Aquatech International LLC, Evoqua Water Technologies (now part of Xylem), 3M, GE Water & Process Technologies (now part of SUEZ and others), Toshiba Water Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Tertiary Water and Wastewater Treatment Equipment Market Segmentation

By Type

- Filtration Systems

- Sand Filters

- Activated Carbon Filters

- Membrane Filtration

- Advanced Treatment Technologies

- Membrane Bioreactors (MBR)

- Electrodialysis Reversal (EDR)

- Ion Exchange Systems

- Disinfection Systems

- UV Irradiation

- Ozonation

- Advanced Oxidation Processes (AOPs)

- Chlorination/Dechlorination

- Specialized Removal Systems

- Nutrient Removal (Nitrogen/Phosphorus)

- Trace Contaminant Removal (Pharmaceuticals, PFAS)

- Color/ODOR Removal

By Application

- Municipal Applications

- Potable water production

- Wastewater reuse (irrigation, industrial)

- Environmental discharge compliance

- Industrial Applications

- Food & Beverage

- Pharmaceuticals

- Microelectronics

- Power Generation

- Mining

- Special Applications

- Aquaculture

- Swimming pool water treatment

- Ballast water treatment

By Treatment Objective

- Pathogen Removal

- Nutrient Removal

- Desalination

- Organic Removal

- Heavy Metal Removal

By End-User

- Municipal Sector

- Industrial Sector

- Manufacturing facilities

- Process industries

- Energy sector

- Commercial Sector

- Hospitals

- Large commercial buildings

- Resorts and hotels

By System Configuration

- Stand-Alone Systems

- Integrated Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Tertiary Water and Wastewater Treatment Equipment Market

- Veolia

- Xylem Inc.

- Ecolab

- DuPont

- Pentair

- SUEZ

- Kurita Water Industries

- Calgon Carbon Corporation

- Aquatech International LLC

- Evoqua Water Technologies (now part of Xylem)

- 3M

- GE Water & Process Technologies (now part of SUEZ and others)

- Toshiba Water Solutions

* List Not Exhaustive

Research Coverage

This report investigates the Tertiary Water & Wastewater Treatment Equipment Market, providing breakthroughs in technology adoption, analysis reviews of regulatory frameworks, highlights of strategic investments, and competitive benchmarking across industrial and municipal segments. It explores the rapid transition toward advanced membrane technologies, PFAS destruction systems, direct potable reuse, and industrial zero liquid discharge, all of which are redefining compliance and sustainability standards. By covering mergers, acquisitions, pilot projects, and cross-sector collaborations, this report highlights how global leaders are driving innovation, efficiency, and resilience in tertiary treatment ecosystems. Produced by USDAnalytics, this report is an essential resource for industry professionals, policy makers, and investors seeking actionable intelligence on high-growth opportunities and regulatory trends shaping the future of tertiary treatment worldwide.

Scope Highlights:

- Segmentation: By Type (Filtration Systems, Membrane Filtration, Advanced Treatment Technologies, Disinfection Systems, Specialized Removal Systems), By Application (Municipal, Industrial, Special Applications), By Treatment Objective (Pathogen Removal, Nutrient Removal, Desalination, Organic Removal, Heavy Metal Removal), By End-User (Municipal, Industrial, Commercial), By System Configuration (Stand-Alone, Integrated Systems)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic & Forecast Data: Covers historical trends from 2021–2024 and forecasts from 2025–2034.

- Companies: Includes analysis and profiles of 15+ leading companies such as Veolia, Xylem Inc., SUEZ, Pentair, DuPont, Kurita Water Industries, and others.

Methodology

The methodology for this market study integrates a blend of primary research (in-depth interviews with industry experts, regulators, utility managers, and technology providers) and secondary research (analysis of company reports, government mandates, regulatory databases, and peer-reviewed journals). Advanced data modeling was employed to forecast market size and growth trends across regions, segments, and technologies. Comparative benchmarking was applied to assess adoption rates of membrane filtration, PFAS destruction, and zero liquid discharge systems, while scenario analysis was conducted to evaluate the impact of regulatory shifts, water scarcity, and investment policies. Triangulation techniques ensured validation of data points and projections, making the findings robust, actionable, and tailored for industry professionals.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Tertiary Water & Wastewater Treatment Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Strategic Insights for Industry Stakeholders

1.3. Global Market Snapshot

2. Tertiary Water & Wastewater Treatment Equipment Market Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $29.2 Billion

2.2.2. Forecasted Market Size (2034): $46.5 Billion at 5.3% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Emerging Regulatory Pressure and Micropollutants

2.3.2. Rise of High-Purity Membrane Technologies

2.3.3. Membrane-Centric Technological Transition

2.3.4. Scalable, Modular Deployment Trend

3. Market Analysis: Regulatory Mandates and Strategic Investments

3.1. Overview of the Tertiary Treatment Sector

3.2. Recent Developments and Strategic Investments

3.2.1. Veolia's Argelès-sur-Mer Project and Acquisition of WTS

3.2.2. SUEZ's Partnerships with Seabex and Biogas Unit

3.2.3. Xylem's Anaerobic Membrane Bioreactor (AnMBR) Collaboration

3.2.4. Pentair's Acquisition of Porous Media

4. Trends and Opportunities in Tertiary Water and Wastewater Treatment Equipment Market

4.1. Rapid Adoption of PFAS Destruction Technologies

4.1.1. Regulatory Drivers and Commercial Deployment

4.1.2. Examples of PFAS Destruction Technologies

4.2. Direct Potable Reuse (DPR) Goes Mainstream

4.2.1. Multi-Barrier Treatment Plants

4.2.2. Global Examples of DPR Implementation

4.3. Industrial Zero Liquid Discharge (ZLD) Boom

4.3.1. Regulatory and ESG Drivers

4.3.2. Case Studies and Economic Benefits

4.4. Ceramic Membranes Displacing Polymers

4.4.1. Advantages of Ceramic Membranes

4.4.2. Industrial Deployment Examples

5. Tertiary Water & Wastewater Treatment Market Share Insights

5.1. By Type

5.1.1. Filtration Systems

5.1.2. Advanced Treatment Technologies

5.1.3. Disinfection Systems

5.1.4. Specialized Removal Systems

5.2. By Application

5.2.1. Industrial Applications

5.2.2. Municipal Applications

5.2.3. Special Applications

5.3. By Treatment Objective

5.3.1. Desalination

5.3.2. Pathogen Removal

5.3.3. Organic and Micropollutant Removal

5.3.4. Nutrient Removal

5.4. By End-User

5.4.1. Industrial Sector

5.4.2. Municipal Sector

5.4.3. Commercial Sector

5.5. By System Configuration

5.5.1. Integrated Multi-Technology Trains

5.5.2. Stand-Alone Systems

6. Country Analysis of the Tertiary Water and Wastewater Treatment Equipment Market

6.1. United States: Innovation and Sustainability Driving Adoption

6.2. India: Government Initiatives and ZLD Projects

6.3. Israel: Pioneering Water Reuse

6.4. China: Policy-Driven Wastewater Recycling

6.5. Japan: Advanced Tertiary Treatment for Extreme Environments

6.6. United Arab Emirates (UAE): Large-Scale Infrastructure Projects

6.7. Other Country Analysis (e.g., UK, France, Saudi Arabia)

7. Tertiary Water & Wastewater Treatment Equipment Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Application

7.1.3. By Treatment Objective

7.1.4. By End-User

7.1.5. By System Configuration

7.2. Europe Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Application

7.2.3. By Treatment Objective

7.2.4. By End-User

7.2.5. By System Configuration

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Application

7.3.3. By Treatment Objective

7.3.4. By End-User

7.3.5. By System Configuration

7.4. South America Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Application

7.4.3. By Treatment Objective

7.4.4. By End-User

7.4.5. By System Configuration

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Application

7.5.3. By Treatment Objective

7.5.4. By End-User

7.5.5. By System Configuration

8. Company Profiles: Leading Players in Tertiary Water and Wastewater Treatment Equipment Market

8.1. Veolia

8.2. Xylem Inc.

8.3. Ecolab

8.4. DuPont

8.5. Pentair

8.6. SUEZ

8.7. Kurita Water Industries

8.8. Calgon Carbon Corporation

8.9. Aquatech International LLC

8.10. Evoqua Water Technologies (now part of Xylem)

8.11. 3M

8.12. GE Water & Process Technologies (now part of SUEZ and others)

8.13. Toshiba Water Solutions

8.14. VA Tech Wabag

8.15. Thermax Limited

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations