Zero Liquid Discharge Systems Market Overview: Market Value, CAGR, and Key Insights

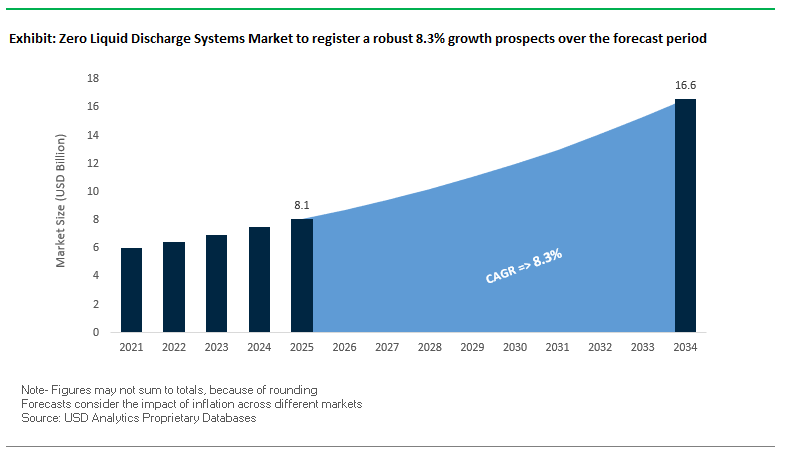

The Zero Liquid Discharge (ZLD) Systems Market is expanding rapidly, driven by global environmental regulations, industrial water scarcity, and the economic advantages of reusing treated water. The global market is projected to grow from USD 8.1 billion in 2025 to USD 16.6 billion by 2034, reflecting a robust CAGR of 8.3%. This trajectory underscores the growing importance of advanced water recycling and industrial wastewater treatment technologies across multiple sectors including power generation, chemicals, textiles, and oil & gas.

Key Insights:

- High Recovery Rates: Over 90% of wastewater can be recovered with integrated ZLD systems, significantly reducing industrial freshwater intake.

- Asia-Pacific Leadership: China and India are the fastest-growing adopters, driven by water-stressed regions and strict discharge regulations.

- Industry Demand: Power generation and chemical industries remain the largest end-users due to high wastewater volumes.

- Membrane Innovation: Adoption of reverse osmosis (RO) and nanofiltration (NF) pretreatment enables up to 80% recovery before energy-intensive evaporation.

Market Analysis: Recent Developments in Zero Liquid Discharge Systems

The ZLD systems industry is evolving through innovation, regulatory pressures, and strategic corporate initiatives. Recent developments highlight how technology providers and industries are responding to global water challenges.

In August 2025, Voltea integrated its Capacitive Deionization (CapDI) systems with IoT infrastructure to minimize brine discharge, introducing a more sustainable and cost-effective ZLD pathway. However, not all sectors welcome strict mandates; in July 2025, textile dyeing units in Ludhiana, India raised concerns that enforced ZLD norms could disrupt small enterprises, emphasizing the balance between sustainability and economic feasibility. Around the same time, Veolia Water Technologies strengthened its portfolio by acquiring full ownership of its Water Technologies and Solutions subsidiary (May 2025), enhancing its ability to deliver integrated ZLD solutions worldwide.

Innovation is also fueled by public and academic initiatives. A European R&D program (August 2025) allocated funding for next-generation anti-fouling membrane coatings, expected to reduce chemical cleaning needs in recycling plants. Similarly, in December 2024, a breakthrough study showcased the use of engineered nanoparticles for efficient in-situ produced water treatment signaling a cost-effective alternative for ZLD deployment.

Strategic partnerships are expanding ZLD’s footprint in heavy industries. SLB’s acquisition of ChampionX (April 2024) enhanced its capacity for produced water management, while Cannon Artes (October 2023) deployed ZLD solutions in West Qurna, Iraq, one of the largest onshore oil fields globally. Additionally, LiqTech International’s collaboration (January 2024) with Razorback Direct Oilfield Solutions advanced ZLD for re-injection, reuse, and lithium harvest, showing that ZLD is no longer just about compliance but about value creation from wastewater.

Key Trends Driving ZLD Market Growth

Stricter Environmental Regulations as a Market Catalyst

Regulatory tightening is a primary driver shaping the ZLD market. Policies such as the European Union's Water Reuse Regulation and India’s mandate for textile plants exceeding 25 m³/day of wastewater are not merely compliance requirements they are shaping investment decisions. Companies are proactively adopting ZLD to avoid regulatory penalties, maintain social licenses, and position themselves as sustainability leaders. The U.S. EPA’s enforcement of strict effluent standards in power generation demonstrates that large-scale industrial projects are increasingly being designed with ZLD as a central component. This trend highlights how regulation is not just a constraint but a key driver for market expansion and technology innovation.

Corporate Investment in Water Reuse and Resource Recovery

ZLD adoption is increasingly motivated by financial and operational efficiency rather than compliance alone. Industries are now recognizing that water recovery and byproduct extraction can offset capital and operating expenditures. For instance, the textile manufacturer in India that achieved a 95% water recycling rate while recovering 1.2 tons of sodium sulfate daily demonstrates the dual economic and environmental value of ZLD. Similarly, a $150 million investment by an oil and gas company to eliminate all liquid waste streams underscores that ZLD is becoming a strategic component of industrial water management. The trend indicates that companies see ZLD as a revenue-generating and cost-saving investment rather than a purely regulatory obligation.

Technological Advancements in Hybrid and Modular ZLD Systems

Technological innovation is accelerating the adoption of ZLD systems. Hybrid systems combining membrane technologies with thermal processes optimize energy consumption and reduce operational costs, making ZLD viable for more industries. Modular designs, such as those implemented by Saltworks, allow rapid deployment and adaptability for sites of varying scales, making ZLD accessible to mid-market industrial plants and remote facilities. By enabling energy efficiency, automation, and process flexibility, technological advancements are removing traditional barriers to ZLD adoption, broadening its market potential.

Zero Liquid Discharge Systems Market Share Insights

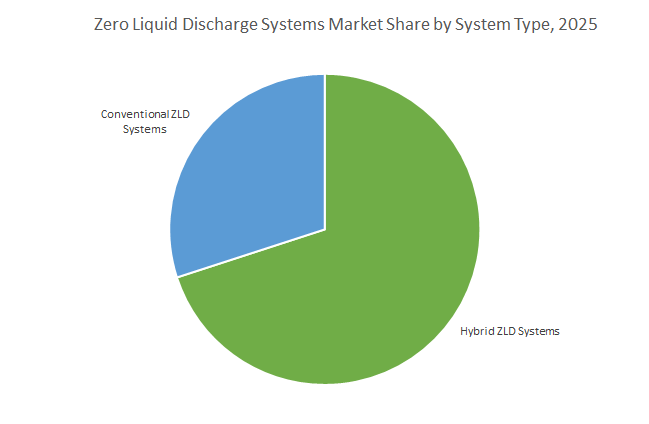

Market Share by System Type: Hybrid Systems Leading the Way

Hybrid ZLD systems are projected to dominate the market (70%) in 2025 due to their superior energy efficiency and cost-effectiveness. By pre-concentrating brine using membranes before thermal crystallization, hybrid systems significantly reduce OPEX, making them economically viable across a broader range of industrial settings. Conventional thermal ZLD systems (30%) are reserved for niche applications with extreme scaling potential or high fouling waste streams, highlighting that cost, energy efficiency, and operational feasibility are key determinants in system selection.

Market Share by Technology: Thermal vs. Membrane Integration

Thermal-based ZLD (60%) remains indispensable for achieving true zero discharge, particularly for high-salinity and challenging effluents. Membrane-based technologies (40%) serve as pre-treatment solutions, recovering a significant portion of water while reducing thermal load. This symbiotic relationship illustrates that technology selection is not a binary choice but a strategic decision to optimize both energy use and water recovery, reflecting how hybrid process trains are redefining efficiency in industrial water management.

Market Share by Plant Capacity: Economies of Scale Drive Adoption

ZLD is most economically viable at large scales, with plants above 1000 m³/day (40%) leading adoption, particularly in power generation, chemical parks, and mining. Mid-sized plants (500–1000 m³/day, 30%) are increasingly adopting ZLD as regulatory pressures rise and modular solutions reduce capital intensity. Smaller units (<500 m³/day) remain niche but strategically important for high-value or high-toxicity waste streams, indicating a market with both scale-driven and specialized growth opportunities.

Market Share by Application: Water-Intensive Industries at the Forefront

Industries with high water consumption and strict regulatory oversight, such as power generation (22%), chemicals & petrochemicals (20%), and textiles (15%), are primary adopters of ZLD systems. Mining and oil & gas (10%) leverage ZLD to address operational constraints in remote locations. Sectors such as food & beverage, semiconductors, and pharmaceuticals adopt ZLD for resource recovery and sustainability, reflecting that both regulatory compliance and strategic water management are shaping market dynamics. The trend underscores how ZLD adoption is increasingly driven by a combination of environmental, operational, and economic factors.

India: Regulatory Push and Corporate Adoption Propel ZLD Deployment

India’s ZLD systems market is witnessing rapid growth due to stringent regulatory policies and proactive corporate initiatives. The Central Pollution Control Board (CPCB) and State Pollution Control Boards (SPCBs) mandate ZLD for industrial sectors such as textiles, dyeing, chemicals, and power generation, especially in water-stressed regions. The National Green Tribunal (NGT) reinforces these requirements, driving adoption among industries. Leading companies like VA Tech Wabag have secured contracts worth ₹46.5 crore for implementing ZLD systems in solar cell manufacturing facilities and are expanding their presence with projects in Dindigul, Tamil Nadu. Technological innovations from players like Arvind Envisol focus on energy efficiency, with patented polymeric film technologies for Mechanical Vapour Recompression Evaporators (MVREs) claiming up to 80% energy savings compared to conventional methods. The National Water Policy further emphasizes sustainable water management, making ZLD systems essential for compliance and environmental protection. Key applications include power generation, textiles, chemicals, and pharmaceuticals in industrial hubs such as Surat, Visakhapatnam, and Chennai, where water scarcity and pollution are critical concerns.

United States: Advanced ZLD Adoption Driven by Regulations and Funding

In the U.S., the ZLD systems market is driven by stringent EPA regulations under the Clean Water Act (CWA), targeting wastewater discharge and emerging contaminants like PFAS. Government funding through the Department of Energy (DOE) supports innovative projects, such as RTI International’s hybrid system combining forward osmosis (FO) with membrane distillation (MD) powered by waste heat, for industrial water reuse. Corporate initiatives by Veolia Water Technologies, Evoqua Water Technologies, and Koch Separation Solutions focus on modular MBR systems integrated into larger ZLD plants for diverse industrial applications. The power generation sector, particularly coal-fired power plants, leads adoption due to strict ash pond discharge rules, while chemical, petrochemical, and refining industries increasingly implement ZLD to minimize wastewater and enhance resource recovery.

China: Government Investment and Local Production Drive ZLD Market Growth

China’s ZLD systems market is expanding due to robust regulatory frameworks, government investments, and high domestic production. The Ministry of Ecology and Environment (MEE) mandates strict wastewater discharge compliance, while policies like the “Guiding Opinions on Promoting the Utilization of Wastewater Resources” aim for a recycled water utilization rate of at least 25% in water-scarce cities by 2025. Heavy investments in wastewater treatment targeting textiles, steel, and pharmaceuticals total $50 billion by 2025. China has achieved approximately 85% self-sufficiency in ZLD system components, fostering competitive advantages over foreign companies and enabling cost-effective solutions. ZLD systems are increasingly adopted in expansion and renovation projects, offering compact footprints and compliance with stringent discharge standards.

Saudi Arabia: Infrastructure Investment and RO Integration Enhance ZLD Implementation

Saudi Arabia is a global leader in ZLD integration within desalination and water reuse projects. Investments include a $4 billion portfolio across 96 initiatives aimed at enhancing water reuse for agriculture, industry, and urban applications. The Saudi Water Partnership Company (SWPC) continues to launch projects under the PPP model, focusing on advanced reverse osmosis (RO) and membrane technologies. Modernization efforts are converting older thermal desalination plants into energy-efficient RO systems integrated with ZLD to manage high-salinity brine. This strategic approach ensures sustainable industrial and municipal water reuse while aligning with the Kingdom’s National Water Strategy.

Germany: Chemical Industry Drives ZLD Market with Regulatory Support

Germany’s ZLD systems market is primarily driven by the chemical sector, which comprises over 2,900 businesses requiring advanced wastewater management. The German Federal Wastewater Charges Act enforces strict discharge fees, promoting ZLD adoption across industrial operations. Leading companies such as H2O GmbH and GEA Group AG are developing innovative and sustainable solutions tailored for industrial wastewater treatment. The focus on industrial compliance, combined with advanced technology implementation, positions Germany as a benchmark for efficient and environmentally responsible ZLD deployment.

Japan: Membrane Innovation and High Water Reuse Demand Propel ZLD Market

Japan’s ZLD systems market benefits from a combination of high population density, water scarcity, and technological leadership. Academic and corporate R&D, led by companies like Toray Industries, has produced high-efficiency separation membrane modules for biopharmaceutical and industrial applications. The government-backed A-JUMP project promotes widespread MBR adoption, ensuring advanced membrane technology penetration in medium- to large-scale sewage treatment plants. ZLD systems are critical in Japan for maximizing water reuse, minimizing wastewater discharge, and optimizing limited freshwater resources, particularly in densely populated industrial zones.

Competitive Landscape: Leading Players in the Zero Liquid Discharge Systems Market

The competitive landscape of the Zero Liquid Discharge Systems Market is shaped by global conglomerates, mid-tier specialists, and innovative startups. Leaders differentiate themselves through technological innovation, geographic reach, and industry partnerships. Below are the top companies defining this space.

DuPont Water Solutions – Pioneering Membrane Technologies for ZLD

DuPont is a global leader in materials science and membrane innovation, with its FilmTec™ RO membranes forming the backbone of many ZLD systems. In 2025, the company won an R&D 100 Award for its FilmTec™ Fortilife™ XC160 Membrane, designed to concentrate wastewater streams more efficiently. Its offerings include reverse osmosis (RO), nanofiltration (NF), ultrafiltration, and ion exchange resins, making it a go-to provider for industries requiring integrated ZLD solutions. DuPont’s strategic focus is on sustainable water reuse and circularity, helping industries reduce both carbon footprints and operational costs.

Veolia Water Technologies – Integrated Solutions Across the ZLD Value Chain

Veolia is a global frontrunner in ecological transformation and industrial water management. Its “GreenUp” plan prioritizes water reuse, desalination, and sustainable ZLD. With over 1,950 RO desalination systems deployed, Veolia has improved energy efficiency by 35% in the past decade. Its portfolio includes falling film evaporators and crystallizers, which allow continuous operations and recovery of valuable by-products from industrial wastewater. Veolia’s strength lies in tailoring integrated ZLD solutions for complex streams, such as cooling tower blowdown and membrane reject, making it a trusted partner for industries under regulatory pressure.

Aquatech International LLC – Specialist in Industrial ZLD Applications

Aquatech is a leading water technology company specializing in ZLD and high-recovery systems. It was named Water Technology Company of the Year (2025 Global Water Awards), underscoring its leadership. Aquatech’s offerings span RO, NF, membrane bioreactors, evaporators, and crystallizers, delivering complete ZLD packages. Recently, it secured a major contract for Kuwait Oil Company’s Lower Fars Heavy Oil Development Project, showcasing its expertise in challenging oil & gas wastewater streams. Aquatech’s focus is on industrial-scale water reuse and helping clients achieve regulatory compliance in resource-scarce environments.

SUEZ – Digital Optimization for Efficient ZLD Systems

SUEZ is a global powerhouse in industrial water and wastewater management, with a strong foothold in Asia. The company recently commissioned an industrial wastewater treatment plant in China (2024) targeting 100% water recycling, a benchmark in ZLD performance. Its offerings include membrane bioreactors, RO membranes, and advanced biological systems, reinforced by predictive analytics platforms to optimize performance. By reducing fouling and chemical consumption, SUEZ ensures ZLD operations are both cost-effective and environmentally sustainable, making it a key player in digitalized water management.

IDE Technologies – High-Efficiency Thermal and Membrane ZLD Solutions

IDE Technologies specializes in desalination and ZLD systems, with a strong reputation in thermal and membrane-based solutions. Its MAXH2O-PFRO technology delivers high recovery rates from tough wastewater streams, minimizing the load on evaporators and crystallizers. IDE’s ZLD portfolio spans ultrafiltration, RO, evaporation, crystallization, and electrodeionization. With a strong focus on oil & gas, power generation, and heavy industry, IDE enables clients to maximize wastewater recovery while meeting strict environmental regulations. Its innovation-led approach positions it as a technology pioneer in the global ZLD landscape.

Zero Liquid Discharge Systems Market Report Scope

Zero Liquid Discharge Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.1 Billion

|

|

Market Size (2034)

|

$16.6 Billion

|

|

Market Growth Rate

|

8.3%

|

|

Segments

|

By System Type (Conventional ZLD Systems, Hybrid ZLD Systems), By Technology (Membrane-Based ZLD, Thermal-Based ZLD), By Plant Capacity (Less than 100 m³/day, 100–500 m³/day, 500–1000 m³/day, Above 1000 m³/day), By Application (Power Generation, Oil & Gas, Chemicals & Petrochemicals, Textile & Dyeing Industry, Food & Beverage, Pharmaceuticals, Metals & Mining, Semiconductor & Electronics, Municipal Wastewater Treatment), By End Use (Industrial ZLD Systems, Municipal ZLD Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Aquatech International, Evoqua Water Technologies, Alfa Laval, Xylem Inc., DuPont de Nemours, Inc., Toray Industries, Inc., GEA Group, Kurita Water Industries Ltd., Thermax Limited, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Aquarion AG, H2O GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Zero Liquid Discharge Systems Market Segmentation

By System Type

- Conventional ZLD Systems

- Hybrid ZLD Systems

By Technology

- Membrane-Based ZLD

- Reverse Osmosis (RO)

- Ultrafiltration (UF)

- Nanofiltration (NF)

- Thermal-Based ZLD

- Multi-Effect Evaporation (MEE)

- Mechanical Vapor Recompression (MVR)

- Crystallizers

By Plant Capacity

- Less than 100 m³/day

- 100–500 m³/day

- 500–1000 m³/day

- Above 1000 m³/day

By Application

- Power Generation

- Oil & Gas

- Chemicals & Petrochemicals

- Textile & Dyeing Industry

- Food & Beverage

- Pharmaceuticals

- Metals & Mining

- Semiconductor & Electronics

- Municipal Wastewater Treatment

By End Use

- Industrial ZLD Systems

- Municipal ZLD Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Zero Liquid Discharge Systems Industry include-

- Veolia

- SUEZ

- Aquatech International

- Evoqua Water Technologies

- Alfa Laval

- Xylem Inc.

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- GEA Group

- Kurita Water Industries Ltd.

- Thermax Limited

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Aquarion AG

- H2O GmbH

*- List not Exhaustive

Research Coverage

This report investigates the Zero Liquid Discharge Systems Market, delivering analysis reviews on adoption drivers, regulatory inflection points, and technology breakthroughs that elevate recovery, shrink energy intensity, and unlock resource valorization. Produced by USDAnalytics, it highlights how hybrid membrane-thermal architectures, modular deployments, and digital optimization reshape lifecycle economics across power, chemicals, textiles, oil & gas, and high-purity manufacturing. With granular sizing and competitively benchmarked upgrade pathways, this report is an essential resource for operators, EPCs, and policymakers planning compliance-ready, high-recovery ZLD programs through 2034. Scope Includes-

- Segmentation

- By System Type: Conventional ZLD Systems; Hybrid ZLD Systems

- By Technology: Membrane-Based (RO, UF, NF); Thermal-Based (MEE, MVR, Crystallizers)

- By Plant Capacity: <100 m³/day; 100–500 m³/day; 500–1000 m³/day; >1000 m³/day

- By Application: Power Generation; Oil & Gas; Chemicals & Petrochemicals; Textile & Dyeing; Food & Beverage; Pharmaceuticals; Metals & Mining; Semiconductor & Electronics; Municipal Wastewater Treatment

- By End Use: Industrial ZLD Systems; Municipal ZLD Systems

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic/Forecast Horizon: Historic data from 2021–2024 and forecasts for 2025–2034.

- Companies (15+ profiles): Veolia; SUEZ; Aquatech International; Evoqua Water Technologies; Alfa Laval; Xylem Inc.; DuPont de Nemours, Inc.; Toray Industries, Inc.; GEA Group; Kurita Water Industries Ltd.; Thermax Limited; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Aquarion AG; H2O GmbH.

Methodology

USDAnalytics applies a mixed top-down/bottom-up approach: country-level sizing by system type, technology, capacity, application, and end use is triangulated with industry water balances, discharge norms, energy tariffs, and project/tender pipelines. Primary research spans structured interviews with plant managers, EPCs, and OEMs to validate CAPEX/OPEX curves, recovery/quality KPIs (TDS, SDI, oil-in-water), and payback for hybrid vs. thermal trains. Secondary sources include regulatory frameworks, environmental permits, vendor specs, and peer-reviewed studies, benchmarking kWh/m³, steam demand, chemical dose, and brine-to-solids conversion. Scenario modeling stress-tests sensitivities to feed salinity, PFAS and sector-specific limits, energy prices, and automation maturity to produce robust 2025–2034 forecasts.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Zero Liquid Discharge (ZLD) Systems Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights: High Recovery, Asia-Pacific Leadership, and Technology

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): USD 8.1 Billion

1.3.2. Projected Market Valuation (2034): USD 16.6 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 8.3%

2. Market Outlook (2025–2034)

2.1. Introduction: Market Value, CAGR, and Growth Drivers

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends Driving ZLD Market Growth

2.3.1. Stricter Environmental Regulations as a Market Catalyst

2.3.2. Corporate Investment in Water Reuse and Resource Recovery

2.3.3. Technological Advancements in Hybrid and Modular ZLD Systems

3. Innovations and Strategic Developments in ZLD Systems

3.1. Market Analysis: Recent Developments

3.1.1. Voltea Integrates IoT with CapDI for Cost-Effective ZLD (August 2025)

3.1.2. Veolia Strengthens Portfolio with Full Ownership of Subsidiary (May 2025)

3.1.3. Strategic Partnerships Expand ZLD’s Footprint in Heavy Industries

3.1.4. Public and Academic Initiatives Drive R&D in ZLD Technologies (August 2025)

3.1.5. India Addresses Economic Feasibility of ZLD for Small Enterprises

4. Competitive Landscape: Leading Players in the ZLD Systems Market

4.1. Competitive Overview: Global Conglomerates and Specialist Providers

4.2. Strategic Profiles of Key Companies

4.2.1. DuPont Water Solutions: Pioneering Membrane Technologies for ZLD

4.2.2. Veolia Water Technologies: Integrated Solutions Across the ZLD Value Chain

4.2.3. Aquatech International LLC: Specialist in Industrial ZLD Applications

4.2.4. SUEZ: Digital Optimization for Efficient ZLD Systems

4.2.5. IDE Technologies: High-Efficiency Thermal and Membrane ZLD Solutions

5. ZLD Systems Market – Segmentation Insights (2025)

5.1. By System Type

5.1.1. Hybrid Systems (70% Market Share)

5.1.2. Conventional Thermal Systems (30% Market Share)

5.2. By Technology

5.2.1. Thermal-Based ZLD (60% Market Share)

5.2.2. Membrane-Based ZLD (40% Market Share)

5.3. By Plant Capacity

5.3.1. Above 1000 m³/day (40% Market Share)

5.3.2. 500–1000 m³/day (30% Market Share)

5.3.3. Less than 500 m³/day (30% Market Share)

5.4. By Application

5.4.1. Power Generation (22% Market Share)

5.4.2. Chemicals & Petrochemicals (20% Market Share)

5.4.3. Textile & Dyeing Industry (15% Market Share)

5.4.4. Metals & Mining and Oil & Gas (20% Market Share)

5.4.5. Other Applications (23% Market Share)

5.5. By End Use

5.5.1. Industrial ZLD Systems

5.5.2. Municipal ZLD Systems

6. Country Analysis: ZLD Systems Market

6.1. India: Regulatory Push and Corporate Adoption Propel ZLD Deployment

6.2. United States: Advanced ZLD Adoption Driven by Regulations and Funding

6.3. China: Government Investment and Local Production Drive Market Growth

6.4. Saudi Arabia: Infrastructure Investment and RO Integration Enhance Implementation

6.5. Germany: Chemical Industry Drives Market with Regulatory Support

6.6. Japan: Membrane Innovation and High Water Reuse Demand Propel Market

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Market Outlook

7.1.1. By System Type

7.1.2. By Application

7.1.3. By End-Use Industry

7.2. Europe Market Outlook

7.2.1. By System Type

7.2.2. By Application

7.2.3. By End-Use Industry

7.3. Asia Pacific Market Outlook

7.3.1. By System Type

7.3.2. By Application

7.3.3. By End-Use Industry

7.4. South America Market Outlook

7.4.1. By System Type

7.4.2. By Application

7.4.3. By End-Use Industry

7.5. Middle East & Africa Market Outlook

7.5.1. By System Type

7.5.2. By Application

7.5.3. By End-Use Industry

8. Company Profiles: Leading Players

8.1. Veolia

8.2. SUEZ

8.3. Aquatech International

8.4. Evoqua Water Technologies

8.5. Alfa Laval

8.6. Xylem Inc.

8.7. DuPont de Nemours, Inc.

8.8. Toray Industries, Inc.

8.9. GEA Group

8.10. Kurita Water Industries Ltd.

8.11. Thermax Limited

8.12. V.A. TECH WABAG Ltd.

8.13. Mitsubishi Chemical Corporation

8.14. Aquarion AG

8.15. H2O GmbH

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures