Market Overview: Rising Demand for Sustainable Produced Water Treatment Solutions

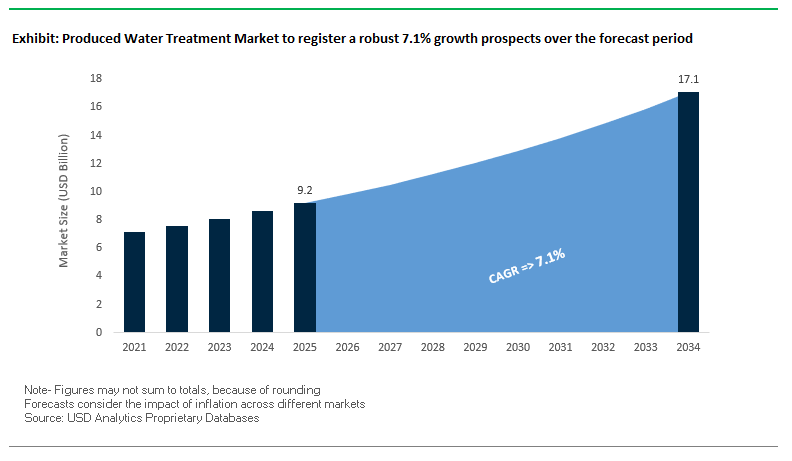

The Produced Water Treatment Market is witnessing strong growth, driven by stringent environmental regulations, sustainability goals in the oil and gas sector, and the need for cost-efficient water management. The market is valued at USD 9.2 billion in 2025 and is projected to reach USD 17.1 billion by 2034, growing at a CAGR of 7.1%.

Industry Stakeholders view produced water treatment as critical, given that over 21 billion barrels of produced water are generated annually, requiring effective separation, disposal, or reuse solutions. The industry’s momentum is further fueled by advanced treatment technologies such as membrane filtration, flotation systems, and chemical treatment, which are becoming mainstream across onshore and offshore projects.

Key Insights for Industry Stakeholders

- Onshore dominance: Onshore operations accounted for 72% of revenue in 2024, largely driven by shale oil and gas production in North America.

- Physical treatment leadership: Physical methods such as membrane filtration and flotation captured 48% of market revenue in 2024, reinforcing their importance in primary and secondary treatment stages.

- Regional strength: The Middle East & Africa commands 43.4% of the global market, underscoring the region’s reliance on produced water treatment for large-scale oil and gas activities.

- Sustainability impact: Technologies supporting water reuse and circularity are gaining traction as producers look to reduce environmental impact and optimize resources.

Market Analysis: Recent Developments Driving Innovation and Expansion

The produced water treatment market has been highly active, with recent strategic alliances, product launches, and technology advancements shaping its trajectory. In April 2024, SLB announced its agreement to acquire ChampionX Corporation, significantly expanding its capabilities in chemical solutions and artificial lift systems both critical in produced water management. This move positions SLB to offer integrated water treatment solutions across global operations.

In January 2024, Adaptive Process Solutions (APS) launched its Microbubble Infusion Unit (MiFU), a breakthrough designed to enhance contaminant removal efficiency, addressing one of the industry’s most pressing challenges high operational costs. Similarly, LiqTech International’s February 2024 partnership with Razorback Direct Oilfield Solutions marked a step forward in deploying advanced filtration systems for re-injection, reuse, and lithium harvesting across the U.S., reflecting the market’s diversification into secondary value creation.

The emphasis on sustainability is evident in Baker Hughes’ October 2023 introduction of H2prO, a solution aimed at the beneficial reuse of produced water, supporting industry-wide circularity goals. Regional advancements include Cannon Artes’ October 2023 project in West Qurna, Iraq, providing large-scale treatment for one of the world’s largest oil fields. Technological progress also plays a pivotal role: in January 2024, published research demonstrated the use of engineered nanoparticles for in-situ treatment, highlighting innovation in reducing costs while improving efficiency.

Emerging Trends Shaping the Produced Water Treatment Market

Advanced Technologies for Water Reuse and Resource Recovery

Technological innovation is at the forefront of market growth, enabling operators to transform produced water into a reusable resource. A recent study in the Journal of Water Process Engineering demonstrates that hybrid treatment systems combining advanced oxidation processes (AOPs) with membrane filtration can remove 99.8% of hydrocarbons and 95% of dissolved solids, producing water suitable for industrial reuse in boilers or cooling towers. Globally, large-scale projects, such as a 100,000 barrels/day facility in the Middle East, showcase how treated water is reinjected into reservoirs for enhanced oil recovery (EOR), increasing production while conserving freshwater a model increasingly replicated worldwide.

Rising Investment in Digitalization and Automation

The shift towards digitally integrated produced water management is accelerating efficiency and compliance. Schlumberger’s digital platform for produced water leverages real-time sensors and predictive analytics, reportedly improving operational efficiency by up to 15% through optimized treatment and predictive maintenance. In addition, the U.S. EPA notes growing interest in using treated produced water for agriculture and wildlife propagation in arid regions, emphasizing the need for automated monitoring to meet stringent quality standards. Digital solutions are thus becoming a differentiator for companies aiming to reduce operational costs while maintaining environmental compliance.

Growing Focus on Zero Liquid Discharge (ZLD) Systems

Sustainability-driven initiatives are pushing the adoption of Zero Liquid Discharge (ZLD) technologies, which allow operators to recover almost all water from effluents. A major oil and gas company invested $150 million in a ZLD facility at its refinery to achieve full water recovery and internal reuse. Additionally, Veolia Water Technologies recently implemented a modular produced water treatment system in the North Sea designed for high total dissolved solids and variable flow rates, exemplifying how ZLD systems are critical in offshore operations to comply with strict environmental regulations and reduce marine pollution.

Strategic Opportunities in the Produced Water Treatment Market

The produced water treatment market presents multiple growth avenues tied to resource efficiency, sustainability, and technological sophistication. The increasing deployment of advanced treatment and ZLD systems opens opportunities for high-value projects in both onshore and offshore segments. The water-as-a-service model is gaining traction, allowing independent operators and service providers to offer modular, mobile treatment solutions that reduce upfront CAPEX while providing operational flexibility. Furthermore, digital and automated solutions for monitoring and control enable better regulatory compliance and optimization of complex treatment trains. Companies investing in hybrid technologies, advanced membranes, and full-scale automation are well-positioned to capitalize on regulatory mandates, water scarcity challenges, and the global push towards sustainable oilfield operations.

Produced Water Treatment Market Share Insights

Market Share by Treatment Type (2025)

Primary treatment dominates with a 40% market share, forming the foundation of all treatment trains by removing free oil, grease, and suspended solids. Its universal application is critical to protect downstream equipment and ensure compliance with basic discharge criteria. Secondary treatment, accounting for 35%, addresses dissolved and emulsified hydrocarbons, enabling compliance for surface discharge and water reuse in operations such as hydraulic fracturing. Tertiary/advanced treatment, with 25% share, is the fastest-growing segment, driven by ZLD mandates, aquifer recharge projects, and high-value reuse applications. This segment relies on technologies like reverse osmosis (RO), nanofiltration (NF), and advanced oxidation, reflecting the increasing sophistication of produced water management strategies globally.

Market Share by System Configuration (2025)

Onshore systems account for 75% of the market, reflecting the dominance of land-based oil and gas operations. These systems offer flexibility through centralized plants, modular units, or mobile skids, making them ideal for variable well output and evolving production needs. Offshore systems hold 25% share but represent a high-value segment due to space, weight, and reliability constraints on platforms and FPSOs. The complexity and critical nature of offshore operations drive significant investment in compact, automated, and robust treatment solutions, highlighting the technological advancement in this segment despite its smaller volume.

Market Share by Technology (2025)

Physical treatment technologies lead with 40%, forming the backbone of treatment systems with equipment such as gravity separators, hydrocyclones, and induced gas flotation units, valued for simplicity and reliability. Membrane-based separation technologies hold 25% share, critical for secondary polishing, desalination, and high-quality reuse, with ultrafiltration (UF), microfiltration (MF), and RO being widely adopted. Chemical treatment technologies (20%) enhance oil-water separation, prevent scaling, and control biofouling, complementing physical systems. Hybrid and integrated systems (15%) combine multiple treatment approaches into optimized trains, addressing variable feed quality and achieving stringent water quality targets. The rise of hybrid systems reflects the increasing complexity of produced water streams and the demand for customized, high-efficiency treatment solutions.

Market Share by End-User (2025)

Oil & gas operators, including majors and NOCs, dominate with 50% share, driving major capital projects for centralized onshore and offshore treatment facilities. Independent E&P companies (20%) favor flexibility, often outsourcing treatment solutions to manage costs and operations efficiently. Oilfield service companies (20%) provide modular, mobile “water-as-a-service” offerings, converting capital-intensive equipment into operational expenditures. Finally, water treatment service providers (10%) address the increasing complexity of produced water, offering specialized expertise from design to operation and disposal. The distribution highlights a trend toward outsourcing and service-based models, enabling operators to focus on core production while leveraging advanced treatment solutions and sustainable water management practices.

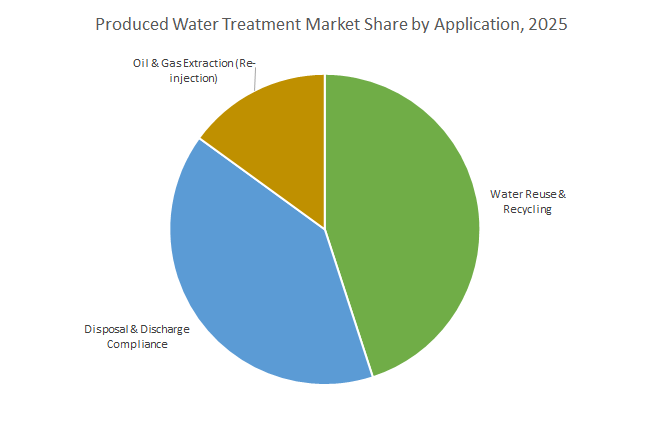

Market Share by Application

Country Analysis of Produced Water Treatment Market

Saudi Arabia: Strategic Investments in RO Membrane Infrastructure

Saudi Arabia is a pivotal market for produced water treatment, driven by its position as a global oil and gas leader. The Kingdom is constructing the first reverse osmosis (RO) membrane plant in the Middle East, with an annual production capacity of 254,000 membranes, scheduled to commence in 2025. This infrastructure supports the treatment of produced water for safe disposal and reuse, bolstering sustainability goals. The Saline Water Conversion Corporation (SWCC) is deploying energy-efficient RO membranes at facilities like the Yanbu 4 desalination plant, producing 450,000 cubic meters of freshwater per day. The Saudi Water Partnership Company (SWPC) continues to launch new desalination and wastewater treatment projects, predominantly leveraging RO technology, reflecting a strategic transition from energy-intensive thermal methods to advanced membrane-based solutions.

United States: Regulatory Compliance and Hybrid Membrane Innovations

The U.S. produced water treatment market is propelled by strict federal regulations and innovative membrane technologies. The Environmental Protection Agency (EPA) enforces the Clean Water Act and Safe Drinking Water Act, including new PFAS Maximum Contaminant Levels, which are driving retrofitting investments in existing treatment facilities. The Department of Energy (DOE) funds hybrid projects combining forward osmosis (FO) with membrane distillation (MD) powered by waste heat, enhancing industrial water reuse. Corporations like Veolia Water Technologies, Evoqua Water Technologies, and Koch Separation Solutions are deploying modular systems suitable for retrofits, addressing both PFAS compliance and industrial water reuse needs. This focus on hybrid technologies and regulatory alignment positions the U.S. as a leading adopter of advanced produced water treatment solutions.

China: Large-Scale Investments and Localized Production Capacity

China’s produced water treatment market is influenced by stringent industrial wastewater regulations and government-driven infrastructure programs. The Ministry of Ecology and Environment (MEE) mandates strict emission standards, while the 14th Five-Year Plan emphasizes water reuse, targeting 95% wastewater treatment for county-level cities. Researchers from the Chinese Academy of Sciences developed dual-functional RO membranes with antibacterial and anti-adhesion properties for use downstream of biological treatment, improving system efficiency. China’s government plans $50 billion in investment for wastewater treatment by 2025, particularly in high-pollution industries such as textiles, steel, and pharmaceuticals. Domestic production is highly localized, with self-sufficiency reaching approximately 85%, enabling cost-effective deployment of produced water treatment systems.

Canada: Provincial Standards and First Nation Water Infrastructure Initiatives

Canada’s produced water treatment market is governed by provincial and territorial regulations, ensuring compliance with environmental standards. Health Canada is reviewing and establishing objectives for water quality and treatment, particularly in regions like Ontario. The federal government is focusing on establishing minimum standards for water services and infrastructure on First Nation lands, which is expected to drive substantial investments in water and wastewater treatment, including produced water. Technological adoption includes water safety planning approaches and integration of advanced treatment systems to ensure safe and sustainable water management across industrial and municipal sectors.

Russia: Academic Innovations and Photocatalyst-Based Treatment

Russia is enhancing its produced water treatment capabilities through research and technological innovations. In 2021, Russian scientists patented a thermostable microporous photocatalyst material suitable for industrial and produced water treatment. While municipal wastewater projects, such as a 2024 initiative in Moscow, have primarily tested this technology, its industrial applicability is significant. South Ural State University, under the guidance of Vyacheslav Avdin, is conducting advanced research on photocatalysts, aiming to develop high-efficiency water treatment systems for the oil, gas, and industrial sectors, positioning Russia as an emerging market for innovative produced water solutions.

Brazil: Private Sector Participation and Oil & Gas-Driven Demand

Brazil is witnessing a transformation in its water treatment market, driven by new legal frameworks promoting private sector participation. The regulatory framework sets ambitious targets for 2033, including 99% water coverage and 90% treated sewage coverage, creating a predictable environment for investment. Approximately BRL 105 billion is expected to be invested across 43 privatization projects, representing one of Latin America’s largest infrastructure financing initiatives. The country’s growing oil and gas sector is a key driver for produced water treatment systems, with increased exploration and production activities fueling the demand for advanced treatment solutions, ensuring compliance and sustainable water management practices.

Competitive Landscape: Key Players Shaping the Produced Water Treatment Market

The competitive environment is defined by oilfield service giants, specialized technology providers, and ecological solution leaders, all contributing with advanced treatment portfolios, digital integration, and global project execution capabilities.

Schlumberger (SLB) – Expanding Capabilities Through Strategic Acquisitions

SLB brings unmatched global reach and technological expertise in integrated oilfield services. Its strength in produced water treatment lies in combining chemical and physical separation technologies with digital platforms. The acquisition of ChampionX (April 2024) enhances its solutions in chemistry and artificial lift, fortifying its leadership in water management. SLB’s offerings include AI-driven optimization tools, enabling efficient operations and reduced treatment costs.

Baker Hughes – Driving Sustainability with H2prO Technology

Baker Hughes leverages its global energy technology leadership to address complex water challenges. Its H2prO solution, launched in October 2023, highlights the company’s commitment to water reuse and circularity. With a robust mix of separation, chemical, and digital monitoring solutions, Baker Hughes positions itself as a sustainability-focused partner. Its strategy revolves around delivering integrated systems that improve both operational efficiency and environmental compliance.

Veolia Group – Global Leader in Ecological Transformation

Veolia’s strengths lie in providing full-cycle water treatment solutions, including membrane filtration, thermal distillation, and biological treatment. In May 2025, Veolia completed the acquisition of full ownership of its Water Technologies and Solutions subsidiary, streamlining operations and expanding capabilities in produced water treatment. With proven expertise in large-scale projects, Veolia continues to be a go-to partner for oil and gas producers tackling high-volume, complex treatment needs.

SUEZ Group – Customized Industrial Produced Water Solutions

SUEZ is recognized for delivering customized treatment systems tailored to industrial and oilfield environments. While its China seawater desalination project (2023) highlights broader industrial capabilities, its core offerings for produced water include hydrocyclones, flotation systems, and advanced membranes. SUEZ’s focus on reuse and recycling aligns with industry trends, ensuring it remains a competitive force in oilfield water management.

DuPont – Advanced Membrane Technologies for Produced Water

DuPont, through its Water Solutions division, is a leader in high-performance membranes. Its FilmTec™ Fortilife™ membranes, awarded for sustainability, are particularly well-suited for harsh industrial wastewater conditions, including produced water. With a portfolio covering reverse osmosis (RO) and nanofiltration (NF) membranes, DuPont enables high-purity water recovery and supports circular water use strategies. Its innovation-driven approach keeps it at the forefront of produced water treatment technologies.

Produced Water Treatment Market Report Scope

Produced Water Treatment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.2 Billion

|

|

Market Size (2034)

|

$17.1 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Treatment Type (Primary Treatment, Secondary Treatment, Tertiary / Advanced Treatment), By System Configuration (Onshore Systems, Offshore Systems), By Technology (Physical Treatment Technologies, Chemical Treatment Technologies, Membrane-Based Separation Technologies, Hybrid & Integrated Systems), By Application (Oil & Gas Extraction, Water Reuse & Recycling, Disposal & Discharge Compliance), By End-User (Oil & Gas Operators, Oilfield Service Companies, Independent E&P Companies, Refineries & Petrochemical Plants, Water Treatment Service Providers)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, Pentair plc, DuPont de Nemours, Inc., Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kuraray Co., Ltd., Nalco Water (An Ecolab Company), Schlumberger Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Produced Water Treatment Market Segmentation

By Treatment Type

- Primary Treatment

- Gravity Separation

- Corrugated Plate Interceptors

- Hydrocyclones

- Secondary Treatment

- Induced Gas Flotation (IGF)

- Dissolved Air Flotation (DAF)

- Membrane Separation (UF, NF, RO)

- Biological Treatment

- Tertiary / Advanced Treatment

- Advanced Oxidation Processes (AOPs)

- Ion Exchange

- Adsorption (activated carbon, media filters)

- Electrocoagulation & Electrochemical Treatment

- Thermal Treatment & Distillation

By System Configuration

- Onshore Systems

- Modular Containerized Units

- Centralized Facilities

- Offshore Systems

- Compact Skid-Mounted Units

- Floating Production Storage & Offloading (FPSO) Systems

By Technology

- Physical Treatment Technologies

- Chemical Treatment Technologies

- Membrane-Based Separation Technologies

- Hybrid & Integrated Systems

By Application

- Oil & Gas Extraction

- Upstream

- Midstream

- Downstream

- Water Reuse & Recycling

- Enhanced Oil Recovery (EOR)

- Irrigation & Agricultural Use

- Industrial Utilities

- Disposal & Discharge Compliance

- Deep Well Injection

- Surface Discharge

By End-User

- Oil & Gas Operators

- Oilfield Service Companies

- Independent E&P Companies

- Refineries & Petrochemical Plants

- Water Treatment Service Providers

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Produced Water Treatment Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- Pentair plc

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kuraray Co., Ltd.

- Nalco Water (An Ecolab Company)

- Schlumberger Limited

*- List not Exhaustive

Research Coverage

This report investigates the global Produced Water Treatment Market, delivering analysis reviews on demand drivers, breakthrough technologies, and strategic highlights shaping reuse, disposal, and compliance outcomes through 2034. Produced by USDAnalytics, this report is an essential resource for operators, oilfield service firms, EPCs, and policymakers seeking to align decarbonization, water stewardship, and field economics. It explains how integrated trains spanning primary separation, secondary polishing, and advanced/tertiary steps are being retrofitted into onshore and offshore assets; how digital monitoring and modular systems compress OPEX and downtime; and how water-as-a-service models and ZLD pathways convert a liability into a resource across shale, conventional, and petrochemical value chains. Scope Includes-

- Segmentation:

- By Treatment Type: Primary (Gravity Separation, Corrugated Plate Interceptors, Hydrocyclones); Secondary (Induced Gas Flotation, Dissolved Air Flotation, Membrane Separation UF/NF/RO, Biological Treatment); Tertiary/Advanced (AOPs, Ion Exchange, Adsorption, Electrocoagulation/Electrochemical, Thermal/Distillation)

- By System Configuration: Onshore (Modular Containerized Units, Centralized Facilities); Offshore (Compact Skid-Mounted Units, FPSO Systems)

- By Technology: Physical; Chemical; Membrane-Based Separation; Hybrid & Integrated Systems

- By Application: Oil & Gas Extraction (Upstream, Midstream, Downstream); Water Reuse & Recycling (EOR, Irrigation & Agricultural Use, Industrial Utilities); Disposal & Discharge Compliance (Deep Well Injection, Surface Discharge)

- By End-User: Oil & Gas Operators; Oilfield Service Companies; Independent E&P Companies; Refineries & Petrochemical Plants; Water Treatment Service Providers

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Analysis/ profiles of 15+ companies): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; Pentair plc; DuPont de Nemours, Inc.; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kuraray Co., Ltd.; Nalco Water (An Ecolab Company); Schlumberger Limited.

Methodology

USDAnalytics applies a mixed top-down/bottom-up approach: market sizing by treatment type, configuration, technology, application, and end-user at the country level is triangulated with E&P capex, rig counts, produced-water-to-oil ratios, decline curves, and disposal/reuse penetration. Primary research includes structured interviews with operators, OFS providers, EPCs, and technology OEMs to confirm cost curves (CAPEX/OPEX), performance deltas (oil-in-water, TDS/TSS, SDI), and payback for modular and ZLD projects. Secondary inputs comprise regulatory frameworks, tender databases, project trackers, corporate disclosures, and technical literature, benchmarked to KPIs such as kWh/m³, chemical dose, uptime, and water recovery. Scenario analysis stress-tests sensitivities to commodity prices, PFAS and discharge limits, brine salinity, and automation maturity to produce robust 2025–2034 forecasts.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Produced Water Treatment Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): USD 9.2 Billion

1.3.2. Projected Market Valuation (2034): USD 17.1 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 7.1%

2. Market Outlook (2025–2034)

2.1. Introduction: Rising Demand for Sustainable Produced Water Solutions

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Emerging Trends Shaping the Market

2.3.1. Advanced Technologies for Water Reuse and Resource Recovery

2.3.2. Rising Investment in Digitalization and Automation

2.3.3. Growing Focus on Zero Liquid Discharge (ZLD) Systems

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent Developments Driving Innovation and Expansion

3.1.1. SLB Completes Acquisition of ChampionX Corporation (July 2025)

3.1.2. Adaptive Process Solutions (APS) Launches Microbubble Infusion Unit (MiFU) (January 2024)

3.1.3. LiqTech International Partners with Razorback Direct Oilfield Solutions (February 2024)

3.1.4. Baker Hughes Introduces H2prO for Beneficial Water Reuse (October 2023)

3.1.5. Cannon Artes Delivers Large-Scale Treatment Project in Iraq (October 2023)

4. Competitive Landscape: Produced Water Treatment Market

4.1. Market Overview: Global Leaders and Innovators

4.2. Key Players Shaping the Market

4.2.1. Schlumberger (SLB): Expanding Capabilities Through Strategic Acquisitions

4.2.2. Baker Hughes: Driving Sustainability with H2prO Technology

4.2.3. Veolia Group: Global Leader in Ecological Transformation

4.2.4. SUEZ Group: Customized Industrial Produced Water Solutions

4.2.5. DuPont: Advanced Membrane Technologies for Produced Water

5. Produced Water Treatment Market – Segmentation Insights (2025)

5.1. By Treatment Type

5.1.1. Primary Treatment (40% Market Share)

5.1.2. Secondary Treatment (35% Market Share)

5.1.3. Tertiary / Advanced Treatment (25% Market Share)

5.2. By System Configuration

5.2.1. Onshore Systems (75% Market Share)

5.2.2. Offshore Systems (25% Market Share)

5.3. By Technology

5.3.1. Physical Treatment Technologies (40% Market Share)

5.3.2. Membrane-Based Separation Technologies (25% Market Share)

5.3.3. Chemical Treatment Technologies (20% Market Share)

5.3.4. Hybrid & Integrated Systems (15% Market Share)

5.4. By Application

5.4.1. Oil & Gas Extraction (Upstream, Midstream, Downstream)

5.4.2. Water Reuse & Recycling (EOR, Industrial Utilities, etc.)

5.4.3. Disposal & Discharge Compliance

5.5. By End-User

5.5.1. Oil & Gas Operators (50% Market Share)

5.5.2. Independent E&P Companies (20% Market Share)

5.5.3. Oilfield Service Companies (20% Market Share)

5.5.4. Water Treatment Service Providers (10% Market Share)

6. Country Analysis and Outlook: Produced Water Treatment Market

6.1. Saudi Arabia: Strategic Investments in RO Membrane Infrastructure

6.2. United States: Regulatory Compliance and Hybrid Membrane Innovations

6.3. China: Large-Scale Investments and Localized Production Capacity

6.4. Canada: Provincial Standards and First Nation Water Infrastructure Initiatives

6.5. Russia: Academic Innovations and Photocatalyst-Based Treatment

6.6. Brazil: Private Sector Participation and Oil & Gas-Driven Demand

6.7. Other Countries Analyzed

6.7.1. North America (Mexico)

6.7.2. Europe (Germany, UK, France, Spain, Italy, Rest of Europe)

6.7.3. Asia Pacific (India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Produced Water Treatment Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Treatment Type

7.1.2. By System Configuration

7.1.3. By Technology

7.2. Europe Market Size Outlook to 2034

7.2.1. By Treatment Type

7.2.2. By System Configuration

7.2.3. By Technology

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Treatment Type

7.3.2. By System Configuration

7.3.3. By Technology

7.4. South America Market Size Outlook to 2034

7.4.1. By Treatment Type

7.4.2. By System Configuration

7.4.3. By Technology

7.5. Middle East & Africa Market Size Outlook to 2034

7.5.1. By Treatment Type

7.5.2. By System Configuration

7.5.3. By Technology

8. Company Profiles: Leading Players in Produced Water Treatment Industry

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. Pentair plc

8.6. DuPont de Nemours, Inc.

8.7. Toray Industries, Inc.

8.8. Aquatech International

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. V.A. TECH WABAG Ltd.

8.12. Mitsubishi Chemical Corporation

8.13. Kuraray Co., Ltd.

8.14. Nalco Water (An Ecolab Company)

8.15. Schlumberger Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures