Electrodeionization Market Overview: Growth Outlook, Size, and Key Insights

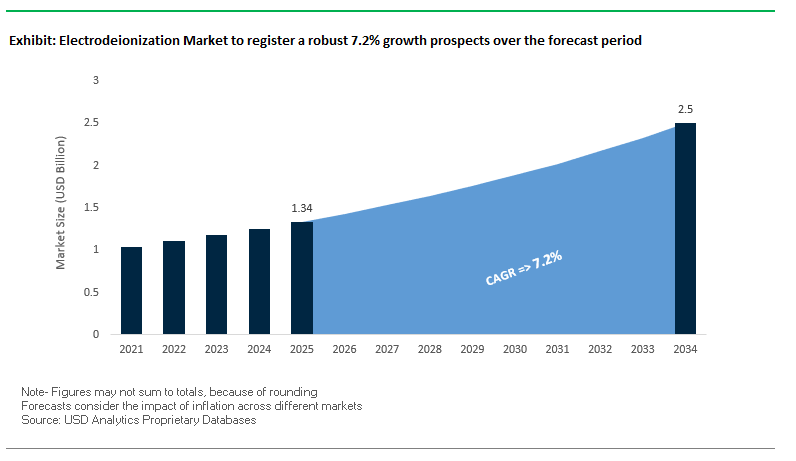

The global electrodeionization (EDI) market is projected to grow from USD 1.34 billion in 2025 to USD 2.5 billion by 2034, expanding at a healthy CAGR of 7.2%. This growth is being propelled by rising demand for ultrapure water systems in semiconductors, pharmaceuticals, and power generation industries, where water quality directly impacts operational efficiency, regulatory compliance, and product integrity.

The electronics and semiconductor sector remains the largest consumer of ultrapure water, with a single 8-inch silicon wafer requiring up to 7,500 liters of water two-thirds of which must be ultrapure. The pharmaceutical industry is also a critical growth driver, where stringent USP water quality standards mandate advanced EDI systems for drug formulation and production. Furthermore, the power generation industry continues to adopt EDI for boiler feedwater, ensuring protection against scaling and corrosion while maintaining long-term plant efficiency.

Unlike conventional ion exchange, EDI technology eliminates hazardous chemical regeneration, lowering operational costs and ensuring safer, sustainable plant operations. This shift toward chemical-free water treatment systems is one of the strongest competitive advantages for end-users across multiple industries.

Key Electrodeionization Market Insights

- Ultrapure water demand in semiconductors is driving large-scale EDI adoption.

- Chemical-free water treatment reduces costs and environmental impact compared to ion exchange.

- Power generation EDI systems ensure high-purity boiler feedwater, enhancing efficiency and equipment life.

- Pharmaceutical-grade EDI water ensures compliance with USP standards for drug manufacturing.

Market Analysis: Recent Developments Shaping the Electrodeionization Industry

The electrodeionization industry is undergoing rapid innovation, with advancements focused on sustainability, high-purity applications, and global market expansion. In August 2025, a new scientific study confirmed that advanced EDI systems can remove emerging contaminants, positioning the technology as essential for industries facing stricter environmental regulations. In the same month, DuPont Water Solutions received a BIG Sustainability Award for breakthroughs in industrial wastewater reuse, where EDI plays a central role in circular water management.

In July 2025, SUEZ entered a renewable energy PPA with RATP Group, showcasing how renewable electricity and advanced water treatment are converging to decarbonize operations. Meanwhile, in June 2025, LG Chem sold its water solutions business to Glenwood Private Equity, signaling a strategic refocus on core materials and pharmaceuticals while shifting EDI market share dynamics. Around the same time, SUEZ announced Xavier Girre as its new CEO, marking a leadership change that aligns with its global water transformation agenda.

Regional demand is also reshaping the EDI market. In May 2025, analysts highlighted that the Asia-Pacific region led by China, India, and Japan will dominate electrodeionization adoption, fueled by electronics and semiconductor manufacturing expansions. Also in May, Veolia launched the TERION™ S, a compact single-skid EDI + RO system, designed for lab and industrial ultrapure water production, signaling a shift toward modular and space-efficient designs. Earlier, in April 2025, DuPont’s FilmTec™ LiNE-XD membranes earned a Bronze Edison Award for their role in lithium brine purification, further cementing DuPont’s leadership in sustainable resource recovery.

Key Trends in the Electrodeionization Market

Growing Demand for Ultrapure Water in High-Tech and Industrial Applications

The increasing dependence on ultrapure water in industries such as pharmaceuticals, semiconductors, and power generation is one of the most defining trends in the electrodeionization market. EDI technology delivers consistent production of ultrapure water with resistivity levels of up to 18 MΩ·cm, meeting the highest standards of wafer rinsing in semiconductor fabs and Water for Injection (WFI) in pharmaceutical manufacturing. Power generation plants also adopt EDI to prevent scaling and corrosion in boilers and turbines, thereby reducing downtime and maintenance costs. Companies like Veolia, through its E-Cell EDI stacks, have already demonstrated successful case studies in both microelectronics and power plants, underscoring the dominance of EDI in high-stakes industrial settings.

Shift Toward Chemical-Free and Sustainable Water Treatment Solutions

Environmental sustainability is pushing industries to adopt water purification methods that minimize hazardous chemical use. Unlike conventional ion exchange processes, electrodeionization eliminates the need for acid and caustic regeneration, making it inherently safer and more eco-friendly. The U.S. Department of Energy (DOE) highlighted a collaborative EDI process by Argonne National Laboratory and EDSEP Inc. that reduces chemical consumption by 90% and waste streams by over 50%. This shift toward green water purification solutions is a key factor propelling EDI adoption in industries under regulatory and environmental scrutiny.

Technological Advancements Driving Efficiency and Lower Energy Consumption

Continuous research and development in EDI technology is delivering groundbreaking innovations such as resin-wafer EDI (RW-EDI) and membrane-free EDI (MF-EDI). Studies published in Water Research X indicate that these advanced systems can operate at energy levels as low as 0.1–0.3 kWh/m³, making them highly competitive compared to traditional deionization methods. Enhanced fouling resistance, modular stack designs, and integration with reverse osmosis systems further improve EDI performance, reducing total cost of ownership and accelerating market penetration across industries that prioritize operational efficiency.

Expansion into New Applications Beyond Ultrapure Water

While EDI is primarily known as a polishing technology in ultrapure water production, its role is expanding into advanced wastewater treatment and niche chemical purification. Case studies from Aarhus University highlight the effectiveness of EDI in removing heavy metals such as chromium, copper, and cesium from industrial wastewater streams, including those from mining and electroplating operations. This demonstrates the versatility of EDI systems, opening new growth avenues in environmental remediation, industrial discharge management, and specialty chemical processing.

Emerging Opportunities Accelerating the Electrodeionization Market

Strong Adoption in Semiconductor and Electronics Manufacturing

The booming global semiconductor and Electronics Manufacturing industry presents the single largest opportunity for electrodeionization. Fabrication plants require ultrapure rinsewater at resistivity levels of 18.2 MΩ·cm, and even minor deviations can result in millions of dollars in losses due to rejected wafers. EDI’s continuous operation and elimination of downtime for regeneration make it the preferred technology for ensuring process reliability. With the ongoing expansion of semiconductor manufacturing capacity worldwide, demand for EDI systems is set to grow exponentially.

Pharmaceutical and Biotechnology Industries Embracing EDI for Compliance and Safety

The pharmaceutical and biotech sector provides significant opportunities for EDI adoption, especially for Water for Injection (WFI) and Purified Water applications that must meet cGMP, USP, and EP standards. By eliminating chemical regeneration, EDI simplifies compliance audits and enhances operator safety. Growing investment in biologics and advanced therapies further accelerates the sector’s reliance on reliable, chemical-free ultrapure water, positioning EDI as a critical enabler of future pharmaceutical manufacturing.

Rising Role of EDI in Power Generation and Energy Efficiency

The power generation sector represents another major opportunity, as high-purity water is critical for high-pressure boilers and turbines. The adoption of EDI minimizes scaling, corrosion, and unplanned shutdowns, directly improving plant efficiency. As utilities worldwide strive to maximize efficiency while meeting stricter environmental regulations, electrodeionization is positioned as a key solution for ensuring both operational reliability and compliance.

Expanding Scope in Wastewater Treatment and Environmental Remediation

A rapidly growing opportunity lies in the use of EDI for industrial wastewater treatment, particularly for industries facing stringent discharge standards. Its ability to selectively remove heavy metals and other contaminants gives it a role beyond ultrapure water, making it a valuable tool for sustainable industrial operations. With governments tightening wastewater discharge norms, EDI adoption is poised to accelerate in sectors such as mining, electroplating, and chemical processing.

Market Share Analysis of the Electrodeionization Market

Market Share by Type: Plate & Frame Dominates the Electrodeionization Industry

By 2025, Plate & Frame EDI devices are projected to capture nearly 85% of the market, while Spiral Wound systems account for the remaining share. Plate & Frame’s dominance is rooted in its unmatched reliability, robustness, and ability to consistently produce high-resistivity ultrapure water (16–18 MΩ·cm). Its scalability and tolerance to variations in feedwater quality make it indispensable for mission-critical applications such as semiconductor fabs and power plants. In contrast, Spiral Wound designs serve a specialized niche where compact form factor and lower initial costs outweigh their limitations in handling high scaling risk, positioning them as suitable for applications using already high-quality feedwater.

Market Share by Resin Type: Mixed-Bed Resin Leads Due to Efficiency

In terms of resin configuration, Mixed-Bed designs command 75% of the market as they deliver the most efficient ion exchange and electro-regeneration performance, closely mimicking the characteristics of a traditional mixed-bed polisher. They enable the production of consistently high-purity water required in sensitive industries. Meanwhile, Separated-Bed resin designs account for 25% of the market, used primarily in applications with unbalanced ion loads or specialized maintenance requirements. Although less common, Separated-Bed systems provide advantages in fouling resistance and targeted ion removal, making them strategically important in niche industrial processes.

Market Share by Application: Ultrapure Water Production is the Core Application

Electrodeionization is overwhelmingly driven by ultrapure water production, accounting for 90% of the market by 2025. Its ability to operate continuously without chemical regeneration has made it synonymous with UPW polishing across industries. Conventional water treatment represents 8% of the market, primarily in partial demineralization for boiler feedwater. However, this segment remains limited due to the higher cost of EDI compared to traditional ion exchange. The remaining 2% is driven by specialized laboratory and chemical applications, where ultrapure and chemical-specific purification requirements create demand for smaller-scale EDI units.

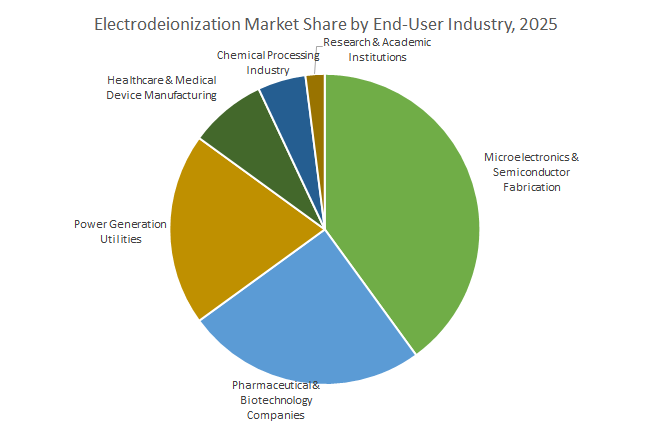

Market Share by End-User Industry: Microelectronics Sets the Benchmark for Adoption

The end-user landscape is dominated by microelectronics and semiconductor manufacturing, accounting for 40% of market share due to their unmatched need for ultrapure rinsewater. Pharmaceutical and biotechnology companies follow with 25%, driven by strict regulatory standards and the need for chemical-free compliance in water purification. Power generation utilities represent 20%, leveraging EDI to prevent scaling in turbines and ensure high operational efficiency. Healthcare and medical device manufacturing contribute 8%, where high-purity water is essential for biocompatibility testing and final rinsing. The chemical processing sector (5%) and research institutions (2%) represent smaller but important niches. Across industries, the unifying demand driver is the transition toward chemical-free, sustainable, and continuous water purification, making EDI a preferred choice for mission-critical operations.

Electrodeionization Market – Country Analysis

China: Regulatory Push and Hydrogen Fuel Cell Applications

China’s electrodeionization (EDI) market is strongly influenced by stringent environmental regulations and rapid industrial adoption. The Ministry of Ecology and Environment (MEE) enforces rigorous wastewater discharge standards, pushing industries to adopt advanced EDI systems to meet emission norms. Technological advancements, such as the 2024 development of hollow-fiber ultrafiltration membranes with enhanced antifouling properties, are improving long-term efficiency and reducing maintenance costs of EDI units. A key growth driver is China’s expanding hydrogen fuel cell sector, where companies are developing ultra-thin reinforced proton exchange membranes to increase power density in stationary and automotive applications. These innovations position China as a leading market for EDI systems in both industrial water treatment and emerging energy applications.

United States: Government Funding and Industry-Led EDI Innovation

The U.S. EDI market benefits from substantial federal support and private sector innovation. The Bipartisan Infrastructure Law provides over $50 billion to the EPA to upgrade water infrastructure, targeting emerging contaminants such as PFAS that require advanced EDI filtration technologies. NSF-funded research centers are at the forefront of developing new membranes for water purification, chemical separations, and biopharmaceutical applications, accelerating innovation in the EDI sector. Leading companies, including DuPont Water Solutions and Evoqua Water Technologies, are developing next-generation perfluorinated ion exchange membranes for chemical processing and the rapidly expanding green hydrogen market, solidifying the U.S. position as a hub for advanced EDI solutions.

India: Government Initiatives and Infrastructure Investments

India’s electrodeionization market is driven by regulatory policies, rural water initiatives, and strategic infrastructure investments. The “Jal Jeevan Mission” aims to provide 55 liters of tap water per rural household daily by 2024, emphasizing the use of advanced filtration technologies like EDI for contaminant removal. The Ghaziabad Nagar Nigam’s issuance of India’s first Certified Green Municipal Bond, raising ₹150 crore for a Tertiary Sewage Treatment Plant (TSTP), illustrates the adoption of EDI and other membrane-based technologies for industrial wastewater reuse. Furthermore, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant in Chennai, valued at INR 415 crores, highlights India’s expanding investment in maintaining and deploying EDI-based water treatment infrastructure.

Saudi Arabia: Desalination Expansion and EDI Polishing Applications

Saudi Arabia is a global leader in membrane-based desalination, and EDI plays a critical role in water polishing. ACWA Power’s Jubail 3A desalination plant, producing 600,000 cubic meters per day, uses RO technology with EDI as a post-treatment step to ensure ultra-pure water quality. The Kingdom’s Saline Water Conversion Corporation (SWCC) employs ion exchange pre-treatment to prevent scaling and enhance operational efficiency, which complements EDI polishing for high-purity water production. Additionally, the Saudi Water Partnership Company (SWPC) continues launching RO-based desalination projects, reinforcing the strategic adoption of membrane technologies, including EDI, across the country’s water infrastructure.

Germany: Industrial EDI Adoption and Green Hydrogen Integration

Germany is at the forefront of EDI applications in industrial wastewater treatment and the green hydrogen economy. Companies such as PWT Wassertechnik integrate EDI and reverse osmosis for industrial water reuse while complying with stringent European environmental regulations. In the hydrogen sector, Enapter is scaling anion exchange membranes for modular electrolyzers, creating significant demand for PFAS-free EDI membranes. Technological advancements by MANN+HUMMEL focus on innovative membrane and digital solutions addressing global water challenges, highlighting Germany’s dual leadership in industrial and energy-related EDI applications.

Japan: Research-Driven EDI Innovation and Global Project Deployment

Japan’s EDI market is heavily influenced by research and innovation. Academic and corporate institutions are developing novel functional membranes, including biomimetic and highly porous designs, to improve water treatment efficiency. Toray Industries continues to play a leading role, providing high-performance RO membranes for large-scale desalination plants, often integrating EDI as a polishing step to achieve ultra-pure water quality. Japan’s expertise in membrane technologies positions it as a key technology provider for global projects requiring advanced EDI applications in industrial and municipal water systems.

Competitive Landscape: Key Players in the Electrodeionization Market

The electrodeionization (EDI) competitive landscape is defined by innovation, mergers, and global project execution. Market leaders such as DuPont Water Solutions, SUEZ (part of Veolia), Veolia Water Technologies, Ovivo, and SnowPure are advancing EDI technologies to meet demands for ultrapure water in electronics, pharmaceuticals, and energy. Each company’s strategy highlights the importance of integrated water treatment portfolios, digital optimization, and sustainability-focused solutions.

DuPont Water Solutions: Innovation in Integrated EDI and Sustainability

DuPont Water Solutions stands out as a global leader in EDI technology with a strong emphasis on integrated ultrapure water systems. Its portfolio spans EDI, ion exchange, reverse osmosis (RO), and ultrafiltration (UF), allowing comprehensive water treatment solutions. Recent innovations include the AmberLite™ P2X110 Resin for green hydrogen production, complementing its EDI business. The launch of WAVE PRO digital modeling tools has strengthened its customer engagement, enabling engineers to optimize UF and RO alongside EDI. DuPont’s recognition as Water Technology Company of the Year (2024) further underscores its leadership in sustainable industrial water treatment.

SUEZ Water Technologies & Solutions: Expanding EDI Through Ecological Transformation

Now part of Veolia, SUEZ Water Technologies & Solutions plays a crucial role in delivering pure and ultrapure water systems for municipal and industrial use. Its EDI portfolio complements large-scale membrane-based desalination and wastewater projects, such as China’s largest desalination plant. The company is actively aligned with circular economy principles, leveraging water reuse, biogas, and renewable energy. The appointment of Xavier Girre as CEO in June 2025 signals renewed strategic direction for global water transformation.

Veolia Water Technologies: Compact TERION™ Systems Driving Growth

Veolia has cemented its reputation as a leader in resource optimization. Its TERION™ series, which integrates reverse osmosis and continuous EDI, has become a flagship offering for high-purity water applications in power generation, pharmaceuticals, and laboratories. Veolia’s Hubgrade™ cloud solutions enhance system monitoring, lowering energy consumption and ensuring performance reliability. With a strategy centered on circular water, energy, and waste solutions, Veolia is aggressively targeting Asia-Pacific and European markets for EDI adoption.

Ovivo: Refocusing Strategy with Divestment and Core Growth

Ovivo has strategically restructured, selling its Electronics division to Ecolab in June 2025 for $2.4 billion. This move allows the company to strengthen focus on municipal, industrial, and energy divisions, where EDI technology remains critical. Ovivo’s long-standing expertise in ultrapure water for semiconductors remains influential, and with operations across 18 countries and 1,500 employees, the company is positioned to pursue new strategic acquisitions while supporting EDI integration globally.

SnowPure: Specialist in High-Purity EDI Technology

SnowPure is a niche player specializing in Electrodeionization (EDI) and Electrodialysis (ED). Its technologies cater to pharmaceuticals, laboratories, food & beverage, and electronics industries. By supplying EDI components like ion exchange membranes and spacers to OEMs, SnowPure has carved out a strong role in the high-purity water supply chain. The company provides technical training and EDICAD design software, ensuring customers can efficiently design and operate EDI systems. This focus on innovation and OEM partnerships makes SnowPure an essential contributor to the global electrodeionization market.

Electrodeionization Market Report Scope

Electrodeionization Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.34 Billion

|

|

Market Size (2034)

|

$2.5 Billion

|

|

Market Growth Rate

|

7.2%

|

|

Segments

|

Type (Plate & Frame Design, Spiral Wound Design), Resin (Mixed-Bed Resin, Separated-Bed Resin), Application (Ultrapure Water (UPW) Production, Conventional Water Treatment, Others), System Integration (Standalone EDI Systems, Post Reverse Osmosis), End-User Industry (Microelectronics & Semiconductor Fabrication, Pharmaceutical & Biotechnology Companies, Power Generation Utilities, Chemical Processing Industry, Healthcare & Medical Device Manufacturing, Research & Academic Institutions)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., SUEZ, Veolia, Pentair plc, Xylem Inc., Toray Industries, Inc., Asahi Kasei Corporation, Kubota Corporation, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, LG Chem, Koch Industries, V.A. TECH WABAG Ltd., Ion Exchange (India) Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Electrodeionization Market Segmentation

By Type

- Plate & Frame Design

- Spiral Wound Design

By Resin

- Mixed-Bed Resin

- Separated-Bed Resin

By Application

- Ultrapure Water (UPW) Production

- Conventional Water Treatment

- Others

By System Integration

- Standalone EDI Systems

- Post Reverse Osmosis

By End-User Industry

- Microelectronics & Semiconductor Fabrication

- Pharmaceutical & Biotechnology Companies

- Power Generation Utilities

- Chemical Processing Industry

- Healthcare & Medical Device Manufacturing

- Research & Academic Institutions

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Electrodeionization Industry include-

- DuPont de Nemours, Inc.

- SUEZ

- Veolia

- Pentair plc

- Xylem Inc.

- Toray Industries, Inc.

- Asahi Kasei Corporation

- Kubota Corporation

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- LG Chem

- Koch Industries

- V.A. TECH WABAG Ltd.

- Ion Exchange (India) Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the global electrodeionization (EDI) market, delivering analysis reviews of demand shifts from ultrapure water (UPW) in fabs and pharma suites to chemical-free polishing for power plants and advanced reuse lines. It highlights breakthroughs in stack architectures (plate-and-frame dominance, spiral niches), resin strategies (mixed-bed vs. separated-bed), and emerging variants (RW-EDI/MF-EDI) that lift resistivity, curb energy per m³, and eliminate hazardous regeneration. The study also highlights how decarbonization, factory expansions in Asia, and modular RO+EDI skids are reshaping procurement, qualification, and lifecycle cost models. With benchmarking on reliability KPIs (ASR, silica/boron leakage, conductivity breakthrough) and system integration pathways, USDAnalytics translates technical performance into bankable outcomes this report is an essential resource for process engineers, EPCs, and buyers standardizing UPW trains across multi-site footprints. Scope Includes-

- Segmentation: By Type (Plate & Frame; Spiral Wound); By Resin (Mixed-Bed; Separated-Bed); By Application (Ultrapure Water Production; Conventional Demineralization; Others); By System Integration (Standalone EDI; Post-RO Integration); By End-User (Microelectronics & Semiconductors; Pharmaceutical & Biotechnology; Power Generation; Chemical Processing; Healthcare & Medical Devices; Research & Academia).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historical assessment 2021–2024 with forecasts 2025–2034.

- Companies: Profiles of 15+ companies (e.g., DuPont, SUEZ/Veolia, Ovivo, SnowPure, Pentair, Xylem, Toray, Asahi Kasei, LG Chem, Dow, Koch, VA TECH WABAG, Ion Exchange (India)).

Methodology

We employ a single, consistent framework: primary interviews (fab UPW leads, pharma QA/validation, power O&M, OEMs/EPCs) combined with secondary research (standards, filings, patents, technical literature). Market sizes fuse top-down demand models (wafer capacity adds, biologics fill-finish growth, MW additions) with bottom-up bill-of-materials for RO+EDI trains (stack area, current density, recovery, conductivity set-points, clean-in-place cadence). Forecasts integrate learning curves, electricity and chemical price scenarios, and policy cadence for green manufacturing. Competitive benchmarking compares stack designs on resistivity stability, silica/boron control, TOC footprint, kWh/m³, uptime, and validated compliance (USP/EP). All outputs undergo cross-checks against commissioning data and announced capacity in APAC, the U.S., and EMEA.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Electrodeionization Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Electrodeionization Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.34 Billion

2.2.2. Forecasted Market Size (2034): $2.5 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 7.2%

2.3. Key Trends and Opportunities

2.3.1. Growing Demand for Ultrapure Water in High-Tech and Industrial Applications

2.3.2. Shift Toward Chemical-Free and Sustainable Water Treatment Solutions

2.3.3. Technological Advancements Driving Efficiency and Lower Energy Consumption

2.3.4. Expansion into New Applications Beyond Ultrapure Water

3. Recent Developments and Strategic Shifts

3.1. Market Trend: Sustainability and Digitalization

3.1.1. DuPont Water Solutions Receives BIG Sustainability Award

3.1.2. SUEZ Enters Renewable Energy PPA for Decarbonization

3.1.3. Veolia Launches Compact EDI + RO System

3.1.4. DuPont's FilmTec™ Membranes Win Edison Award

3.2. Market Opportunity: Global Expansion and Realignment

3.2.1. Asia-Pacific to Dominate EDI Adoption

3.2.2. LG Chem Sells Water Solutions Business

3.2.3. SUEZ Announces New CEO

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Material Science to Integrated Solutions

4.2. Key Competitive Factors

4.2.1. Integrated Water Treatment Portfolios

4.2.2. R&D in New Materials and Digital Tools

4.2.3. Global Project Execution and Aftermarket Support

4.3. Profiles of Top Players

4.3.1. DuPont Water Solutions

4.3.2. SUEZ Water Technologies & Solutions

4.3.3. Veolia Water Technologies

4.3.4. Ovivo

4.3.5. SnowPure

5. Electrodeionization Market – Segmentation Insights

5.1. By Type

5.1.1. Plate & Frame Design

5.1.2. Spiral Wound Design

5.2. By Resin

5.2.1. Mixed-Bed Resin

5.2.2. Separated-Bed Resin

5.3. By Application

5.3.1. Ultrapure Water (UPW) Production

5.3.2. Conventional Water Treatment

5.3.3. Others

5.4. By System Integration

5.4.1. Standalone EDI Systems

5.4.2. Post Reverse Osmosis

5.5. By End-User Industry

5.5.1. Microelectronics & Semiconductor Fabrication

5.5.2. Pharmaceutical & Biotechnology Companies

5.5.3. Power Generation Utilities

5.5.4. Chemical Processing Industry

5.5.5. Healthcare & Medical Device Manufacturing

5.5.6. Research & Academic Institutions

6. Country Analysis and Outlook: Electrodeionization Market

6.1. China: Regulatory Push and Hydrogen Fuel Cell Applications

6.2. United States: Government Funding and Industry-Led EDI Innovation

6.3. India: Government Initiatives and Infrastructure Investments

6.4. Saudi Arabia: Desalination Expansion and EDI Polishing Applications

6.5. Germany: Industrial EDI Adoption and Green Hydrogen Integration

6.6. Japan: Research-Driven EDI Innovation and Global Project Deployment

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Electrodeionization Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Resin

7.1.3. By Application

7.1.4. By System Integration

7.1.5. By End-User Industry

7.2. Europe Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Resin

7.2.3. By Application

7.2.4. By System Integration

7.2.5. By End-User Industry

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Resin

7.3.3. By Application

7.3.4. By System Integration

7.3.5. By End-User Industry

7.4. South America Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Resin

7.4.3. By Application

7.4.4. By System Integration

7.4.5. By End-User Industry

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Resin

7.5.3. By Application

7.5.4. By System Integration

7.5.5. By End-User Industry

8. Company Profiles: Additional Leading Players

8.1. DuPont de Nemours, Inc.

8.2. SUEZ

8.3. Veolia

8.4. Pentair plc

8.5. Xylem Inc.

8.6. Toray Industries, Inc.

8.7. Asahi Kasei Corporation

8.8. Kubota Corporation

8.9. The Dow Chemical Company

8.10. MANN+HUMMEL

8.11. Evoqua Water Technologies

8.12. LG Chem

8.13. Koch Industries

8.14. V.A. TECH WABAG Ltd.

8.15. Ion Exchange (India) Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures