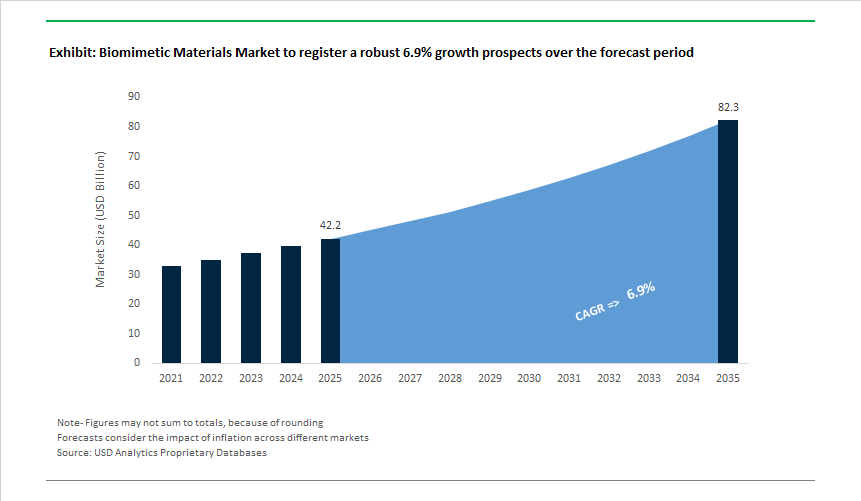

Market Overview: High-Performance Biomimetic Engineering Driving Usd 42.2 Bn Market Growth

The Global Biomimetic Materials Market, valued at USD 42.2 billion in 2025, is projected to reach USD 82.2 billion by 2035, expanding at a 6.9% CAGR, as bio-inspired material design moves decisively from academic research into repeatable, industrial-scale manufacturing. Growth is being driven by quantifiable performance gains in fatigue life, surface functionality, adhesion under extreme conditions, and weight reduction-metrics that directly affect lifecycle cost, safety margins, and system efficiency in aerospace, medical devices, robotics, coatings, and advanced manufacturing.

Across manufacturing industries, biomimetic materials are increasingly specified where conventional polymers, metals, and coatings reach performance ceilings. Aerospace and defense OEMs are adopting bone-inspired lattice alloys and nacre-mimetic composites to achieve higher damage tolerance at lower mass, supporting structural weight reductions of 10-18% while extending fatigue life by over 40% in cyclic loading environments. These architectures are being enabled by advances in additive manufacturing and precision casting, allowing controlled micro- and meso-scale structures that were previously impractical at volume.

In medical and life-science manufacturing, mussel-inspired catechol chemistries and gecko-mimetic surface structures are moving into regulated production pipelines. Surgical adhesive systems based on these principles demonstrate wet-tissue adhesion improvements approaching 45-50%, while maintaining elasticity and biocompatibility under dynamic physiological conditions. Implant manufacturers are also scaling bone-mimicking surface topographies, which show measurable improvements in osseointegration rates and load transfer efficiency compared to smooth or plasma-sprayed surfaces-reducing revision risk in orthopedic and dental applications.

Polymer producers are commercializing spider-silk-inspired molecular architectures, delivering ~30% higher tensile strength and >30% improvement in fatigue resistance versus conventional engineering plastics at comparable densities. These materials are increasingly evaluated for lightweight composite matrices, soft robotics actuators, and high-durability fibers, where energy absorption and crack-arrest behavior are critical. Importantly, these polymers are now being produced via melt-processable and solution-processable routes compatible with existing extrusion and molding infrastructure, lowering adoption barriers.

From a manufacturing perspective, buyer evaluation criteria are shifting toward process repeatability, design-for-manufacture compatibility, and long-term performance stability, rather than purely bio-inspired functionality. Suppliers that can demonstrate controlled microstructure tolerances, consistent batch-to-batch performance, and integration with digital design workflows (CAD-to-print or CAD-to-mold) are gaining preference over research-focused solution providers.

Market Analysis: Key Scientific, Regulatory & Commercial Developments

The biomimetic materials industry experienced accelerated innovation and commercialization, driven by new investment agreements, sustainability initiatives, medical breakthroughs, and European regulatory funding. In Jan 2025, Sanara MedTech entered into an exclusive licensing and minority investment agreement with Biomimetic Innovations Ltd., advancing the clinical rollout of bio-inspired wound management technologies based on polymer structures that mimic natural tissue mechanics. Shortly afterward, Dec 2025 saw ASPECT Biosystems achieve a major R&D milestone by successfully 3D-bioprinting complex prosthetic tissue using proprietary biomimetic hydrogels, spotlighting the increasing convergence of advanced manufacturing and bio-inspired materials.

European regulatory and funding momentum strengthened the sector’s growth trajectory. In Nov 2025, the European Commission allocated €15 million to develop scalable self-healing biomimetic materials for high-criticality infrastructure including bridges, pipelines, and structural reinforcements. Similarly, Oct 2025 marked the introduction of Kyocera’s nacre-inspired ceramic coatings for surgical tools and dental implants, improving wear resistance and boosting osseointegration rates. Innovations continued into Sep 2025, when BASF reaffirmed its R&D commitment to bio-based, water-resistant polymers engineered after natural shell structures, signaling directional push toward sustainable coatings for automotive and architectural markets.

The market also witnessed commercialization expansion in packaging and vascular devices, emphasizing biomimetic design’s versatility. In Mar 2024, Ecovative Design partnered with a major food delivery company to scale mycelium-based packaging systems, reducing reliance on petrochemical plastics through biological growth processes. In Jan 2024, Veryan Medical secured a new purchasing agreement in the UK for its BioMimics 3D Vascular Stent System-an innovation that leverages swirling, helical blood-flow patterns to reduce restenosis risk. R&D momentum persisted into Dec 2024, when the U.S. National Science Foundation funded research into scalable manufacturing of gecko-inspired adhesives, enabling high-load gripping systems for robotics and heavy-duty industrial handling applications.

Biomimetic Materials Market: Trends and Opportunities

Commercial-Scale Structural Composites Inspired by Nacre and Bone Architectures

Biomimetic materials are transitioning from laboratory curiosity to commercially deployable structural solutions, driven by sectors that demand simultaneous gains in strength, toughness, and weight efficiency. Aerospace, defense, and biomedical manufacturers are increasingly adopting nacre-inspired “brick-and-mortar” architectures, where hard inorganic platelets are bonded by softer organic phases to dissipate energy and arrest crack propagation. Unlike isotropic ceramics or metals, these hierarchically structured composites deliver damage tolerance without sacrificing stiffness, unlocking new design envelopes for load-bearing applications.

Between late 2024 and 2025, peer-reviewed advances demonstrated trabeculae-like biomimetic (TBM) materials that replicate the porous hierarchy of natural bone. These materials are capable of embedding osteogenic cells while maintaining mechanical integrity under cyclic load, enabling simultaneous structural support and biological function. In orthopedic and trauma implants, this dual capability is redefining expectations—moving from inert replacements to living, load-sharing scaffolds with controlled drug-release functionality.

In aerospace and defense, nacre-mimetic ceramic–metal composites developed in 2025 showed pronounced micro-crack deflection at engineered interfaces, preventing catastrophic brittle failure. This has opened the door for lightweight ceramics in ballistic protection, hypersonic components, and fatigue-critical structures, where conventional ceramics historically failed qualification. Parallel research programs—including bio-inspired morphing concepts advanced by NASA—are translating avian feather slotting and bat-wing elasticity into adaptive aerostructures. Early 2025 surveys cataloged 290+ biological archetypes under evaluation for drag reduction, maneuverability, and fuel efficiency, underscoring biomimetics as a systems-level performance lever.

Dynamic, Responsive Surfaces Modeled on Marine and Cephalopod Biology

A second major inflection point lies in responsive biomimetic surfaces that change properties in real time. Inspired by cephalopod camouflage, sea-cucumber stiffness modulation, and insect micro-cilia, these materials are being engineered to dynamically alter wettability, stiffness, color, and surface energy. The strategic value is highest in environments where static coatings fail—marine infrastructure, subsea equipment, and defense platforms.

In 2025, magnetic-responsive antifouling surfaces incorporating Fe₃O₄ nanoparticles demonstrated contact angles approaching 157°, enabling continuous shedding of biofouling through controlled oscillation—without toxic biocides. This represents a step-change for offshore energy and naval assets, where biofouling can increase hydrodynamic drag by up to 40% and accelerate corrosion-related failures.

Defense and security programs have also accelerated electrochromic and thermochromic “stealth skins” inspired by octopus chromatophores. By mid-2025, disclosures confirmed millisecond-scale color and texture changes suitable for drones and maritime vessels, enabling adaptive camouflage across thermal and visible spectra. Complementing this, self-healing biomimetic coatings—modeled on vascularized tissue repair—are extending service life of subsea and military hardware by autonomously sealing micro-cracks before they propagate. Collectively, these innovations signal a shift from passive protection to active surface intelligence.

Bio-Inspired Barrier Coatings Replace PFAS in Sustainable Packaging

Regulation is catalyzing one of the fastest-moving opportunity spaces for biomimetic materials: PFAS-free barrier systems for packaging. The EU Packaging and Packaging Waste Regulation (PPWR), in force from February 2025, effectively bans PFAS in food-contact materials by August 2026, forcing brands to replace legacy fluorochemical barriers at scale.

In response, silicon-based and bio-inspired coatings that replicate plant cuticles and insect exoskeleton nanostructures are moving rapidly from pilot to commercialization. Initiatives launched in late 2025—such as Spain’s PLASRECO program—are validating moisture- and grease-resistant coatings that achieve regulatory compliance without compromising recyclability. Major brand owners, including Inditex, are actively testing these solutions to future-proof packaging portfolios.

The broader “paperization” trend is amplifying demand. With EU rules requiring all packaging to be recyclable by 2030, biomimetic coatings that allow paper and fiber substrates to reach plastic-like gas barrier performance are becoming essential. These coatings enable brands to approach Grade-A recyclability thresholds (≈95%) while maintaining shelf-life protection—positioning biomimetic barriers as a cornerstone of circular packaging strategies.

Biomimetic Hydrogels Enable Organoids and Precision Drug Discovery

In life sciences, biomimetic materials are reshaping drug discovery and regenerative medicine through advanced hydrogel scaffolds that emulate the human extracellular matrix (ECM). Pharmaceutical R&D is rapidly adopting organoid-based models to reduce animal testing and improve translational accuracy, creating a premium market for hydrogels with precise mechanical, biochemical, and pH-buffering properties.

Between 2024 and 2025, the integration of microfluidics with bio-inspired hydrogels enabled long-term culture of physiologically relevant organoids, supporting complex tissue differentiation and dynamic nutrient exchange. In oncology, histidine-modified fibrous hydrogels introduced in late 2025 demonstrated intrinsic pH buffering—mirroring tumor microenvironments and allowing patient-derived cancer organoids to maintain structural stability far beyond the limits of conventional synthetic matrices.

Early 2025 research also confirmed the successful creation of immune and bone organoids using biomimetic scaffolds derived from mesenchymal stem cell cues. These “osteo-organoids” provide new platforms for studying bone regeneration, immune response, and neurodevelopmental disorders, reinforcing biomimetic hydrogels as enabling infrastructure for personalized medicine rather than niche research tools.

Market Share Analysis: Biomimetic Materials Market

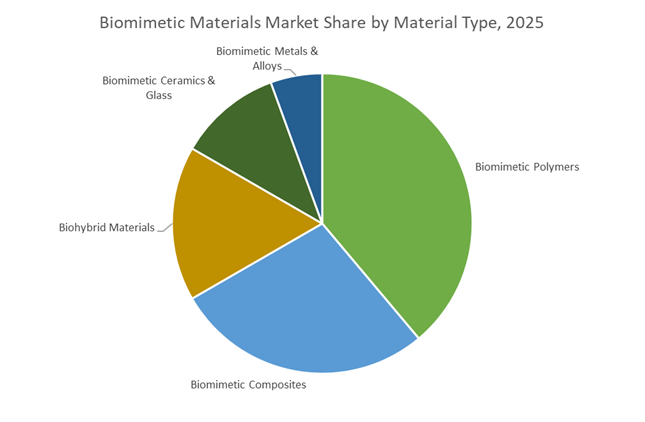

Market Share by Material Type: Biomimetic Polymers Lead Clinical Adoption and Commercial Scale

Biomimetic polymers account for approximately 35% of the global Biomimetic Materials Market, reflecting their unmatched ability to replicate biological functions while remaining manufacturable at scale. This segment dominates because advanced polymers can be precisely engineered to match the mechanical, chemical, and biological behavior of human tissues, solving one of the most persistent challenges in medical device design: compatibility with living systems. High-performance biomimetic polymers deliver bone-like elasticity, reducing stress shielding in orthopedic implants and improving long-term clinical outcomes compared to rigid metallic alternatives. Market share is further reinforced by the tunability of degradation profiles, as resorbable polymers can be programmed to maintain strength for defined periods before safely dissolving, eliminating the need for secondary removal surgeries and lowering total treatment costs. Infection control is another decisive driver, with biomimetic polymer surfaces significantly reducing bacterial adhesion and helping hospitals address costly hospital-acquired infections. The segment’s dominance is also supported by its proven clinical scale and regulatory acceptance, as tens of millions of polymer-based biomimetic implants are already in use globally. Together, these performance, cost, and scalability advantages position biomimetic polymers as the material backbone of the biomimetic materials market, securing their leading share.

Market Share by Application: Medical and Healthcare Anchor High-Value Demand

The medical and healthcare segment represents approximately 40% of total demand in the Biomimetic Materials Market, making it the largest and most value-intensive application area. This leadership is driven by the sector’s need to overcome the body’s natural foreign-body response, which remains one of the most expensive and failure-prone challenges in modern medicine. Biomimetic materials enable implants, scaffolds, and drug delivery systems that behave more like native tissue, improving acceptance rates and reducing complications. Market share is further strengthened by high-volume regenerative manufacturing, which has lowered unit costs and expanded access to advanced biomimetic therapies across public and private healthcare systems. The rise of patient-specific solutions, particularly in 3D-printed orthopedic and cranial implants, has accelerated adoption by reducing surgical time and improving fit and recovery outcomes. In parallel, biomimetic polymer-based controlled drug delivery systems are transforming chronic disease management by replacing frequent dosing with long-acting implants, dramatically improving patient compliance. As healthcare systems increasingly prioritize outcomes, efficiency, and long-term cost reduction, medical and healthcare applications remain the primary demand engine for biomimetic materials, sustaining their dominant share in the global market.

Competitive Landscape: Leading Innovators in Biomimetic Ceramics, Polymers, Coatings & Medical Devices

Global competition in the biomimetic materials market is defined by leadership in advanced ceramics, bio-inspired polymers, nano-structured coatings, self-healing composites, and medical devices designed around physiological biomechanics. Companies compete through breakthroughs in osseointegration, friction reduction, bio-adhesion, tissue emulation, and sustainability. Across healthcare, aerospace, robotics, and energy, suppliers differentiate through proprietary processing technologies, regulatory compliance excellence, and scalable biomimetic architectures.

Kyocera Corporation - Biomimetic Ceramics For Implants & Robotics

Kyocera leverages decades of advanced ceramics expertise to deliver biomimetic solutions for orthopedic and dental implants, designing materials that mimic the microstructure and density of natural bone to enhance biocompatibility and stability. Its medical-grade materials deliver up to 36% lower inflammation rates, significantly reducing post-operative complications. Kyocera also integrates piezoelectric ceramics-mirroring biological charge generation-into sensors and actuators for next-generation robotics and bio-sensing devices. The company’s R&D efforts focus on creating surface-engineered ceramic structures that accelerate osseointegration and improve long-term implant performance.

Ceramtec Gmbh - Global Leader in Biomimetic Joint Replacement Ceramics

CeramTec dominates the orthopedic implant market with its BIOLOX® ceramic technology, recognized for extreme wear resistance and low friction behavior in hip and knee replacements. Its femoral heads exhibit significantly lower friction coefficients compared to metal-on-polyethylene systems, improving implant longevity and patient mobility. CeramTec’s strategic focus on the premium biomedical segment ensures compliance with strict FDA and ISO implant standards. Ongoing investment in expanding BIOLOX production capacity supports the rise in large-diameter ceramic heads, which improve joint stability and reflect modern surgical preferences.

Basf Se - Bio-Inspired Polymers & Self-Healing Functional Materials

BASF utilizes its world-leading chemical innovation capabilities to develop advanced, bio-inspired polymers featuring self-healing, stimuli-responsive, and hydrophobic properties derived from natural systems such as lotus leaves and mussel adhesion. Its investment strategy emphasizes sustainability and circularity, engineering materials that feature closed-loop design principles. BASF’s biomimetic coatings deliver enhanced water repellency and self-cleaning behavior for automotive and architectural applications, while mussel-inspired adhesion chemistries improve underwater bonding for marine repair and industrial sealing. The company works closely with OEMs to integrate bio-based chemistries into large-scale industrial processes.

Lord Corporation (Parker Hannifin) - Biomimetic Adhesives & Adaptive Materials

Lord Corporation designs biomimetic adhesives, vibration-dampening systems, and adaptive materials derived from biological muscle and tendon behavior. Its lightweight coatings and adhesive systems enable aerospace structures to achieve up to 12% weight savings, contributing to lower fuel consumption and improved structural efficiency. The company’s magneto-rheological elastomers mimic natural adaptive responses, supporting applications ranging from advanced robotics actuators to prosthetic devices. Lord’s biomimetic adhesives, including Chemlok®, provide superior environmental resistance and high-strength bonding across automotive, aerospace, and industrial composite components.

Veryan Medical Limited (Otsuka Medical Devices) - Bio-Inspired Vascular Stents

Veryan Medical leads the vascular implant sector with its BioMimics 3D Vascular Stent System, which leverages natural helical artery geometry to induce swirling blood flow, thereby reducing wall shear stress and lowering restenosis risk in Peripheral Artery Disease (PAD). Its design represents a shift from conventional linear stents toward biomechanically optimized solutions that support targeted blood flow dynamics. Backed by Otsuka Medical Devices, the company benefits from robust investment resources to expand clinical validation, scale manufacturing, and enhance global market penetration of its biomimetic cardiovascular technologies.

The United States biomimetic materials market is defined by its ability to convert federally funded research into venture-backed industrial platforms, particularly in medical biomimetics and high-performance structural materials. In 2025, bio-inspired design has been formally embedded into funding priorities across the U.S. Department of Energy (DOE) and National Science Foundation (NSF), accelerating the translation of bone-mimetic hierarchical structures into lightweight aerospace alloys and regenerative medical devices. This policy alignment has strengthened the domestic ecosystem for self-healing composites, where biomimetic vascular networks are being integrated into carbon-fiber structures to enable autonomous crack repair, extending lifecycle performance in defense and aerospace applications. Venture-backed commercialization is equally strong, with companies such as Tidal Vision scaling chitosan-based polymers for water purification and textiles, and inSoma Bio advancing fractional polymer platforms for reconstructive surgery. Collectively, these developments position the U.S. as the global anchor market for high-value, clinically validated biomimetic materials.

China: Dual-Carbon Mandates and Industrial-Scale Biomimicry

China’s biomimetic materials strategy is anchored in scale, speed, and policy-driven substitution of fossil-based materials. Under the dual-carbon framework and the 14th Five-Year Plan, China has rapidly transitioned biomimetic plastics and coatings from pilot concepts into mass production. By 2025, more than 150 pilot lines and over 100 academic laboratories were operational, supporting high-volume deployment of biodegradable and functional films. Industrial leaders such as Changsu Industrial have commercialized BOPLA films that replicate natural membrane barrier properties, directly addressing sustainability requirements in packaging and electronics. China also dominates lotus-effect surface deployment, using superhydrophobic biomimetic coatings to improve efficiency in solar panels and reduce fouling in maritime assets. This combination of industrial scale and policy enforcement makes China the largest volume market for biomimetic coatings and plastics globally.

Germany: Circular Economy Integration and Bionic Engineering Excellence

Germany leads Europe’s biomimetic materials market through deep integration of bionic engineering, Industry 4.0, and circular economy principles. With more than 60 active pilot sites, Germany has the highest concentration of biomimetic testing infrastructure in Europe, focusing on self-healing polymers for automotive applications and natural-fiber composites for transport interiors. Corporate innovation is strongly aligned with applied research, exemplified by Festo AG & Co. KG and its globally recognized Bionic Learning initiatives, which translate biological motion principles into industrial automation. In parallel, bio-inspired adaptive building skins are gaining traction in Germany’s construction sector, supported by EU energy performance regulations. Germany’s competitive strength lies not in volume, but in high-precision, regulation-compliant biomimetic systems designed for long service life and recyclability.

Japan: AI-Driven Biomimetic Design and Marine-Safe Materials

Japan’s biomimetic materials market is differentiated by its heavy reliance on AI-driven materials discovery and a strategic focus on environmentally safe solutions. Japanese firms and research institutes are using artificial intelligence to simulate complex natural phenomena such as butterfly-wing structural coloration, enabling the development of interference-based pigments that eliminate toxic dyes. Electronics leaders including TDK Corporation and Kyocera are embedding these biomimetic principles into consumer electronics and sensors. At the same time, Japan has prioritized marine-biodegradable plastics inspired by enzymes and shell structures to address ocean pollution. With more than 80 dedicated R&D centers, Japan remains a global innovation hub for precision biomimetic materials used in robotics, electronics, and marine-safe applications.

Singapore: Clinical Translation and Bio-Printed Orthopedic Scaffolds

Singapore occupies a unique position as the Asia-Pacific gateway for clinically approved biomimetic medical materials. The country’s regulatory efficiency and hospital–industry collaboration model have enabled rapid commercialization of bioresorbable scaffolds and orthopedic implants. A notable milestone was achieved by Osteopore, which secured regulatory clearance for its aXOpore® biomimetic bone scaffolds and expanded collaborations with major hospitals to address complex conditions such as avascular necrosis. Singapore’s Smart Nation framework further supports the deployment of biomimetic sensors in urban water systems, reinforcing its role as a testbed for high-value, clinically validated biomimetic technologies.

United Kingdom: Luxury Biomaterials and Resorbable Medical Devices

The United Kingdom biomimetic materials market is characterized by strong crossover between luxury goods, sustainability, and advanced healthcare. Venture capital activity has accelerated the scaling of collagen-based and bioresorbable materials that replicate natural fiber architectures. Startups such as PACT are commercializing collagen-based alternatives to leather for luxury fashion, while 4D Medicine is advancing degradable biomaterials for 3D-printed implants that safely resorb as tissue heals. In parallel, packaging innovators are piloting seaweed-derived films to address marine pollution in FMCG supply chains. The UK’s strength lies in design-led biomimetic innovation with strong sustainability credentials.

Comparative Snapshot: Biomimetic Materials Market by Country

Biomimetic Materials Market Development Matrix by Country

|

Country

|

Strategic Focus

|

Industrial Strength

|

Key Application Areas

|

|

United States

|

Advanced manufacturing & regenerative medicine

|

Venture-backed scale-up, defense R&D

|

MedTech, aerospace, self-healing composites

|

|

China

|

Dual-carbon industrialization

|

High-volume pilot-to-mass production

|

Coatings, biodegradable plastics

|

|

Germany

|

Circular economy & bionics

|

Precision engineering, automotive pilots

|

Automotive, adaptive buildings

|

|

Japan

|

AI-driven materials DX

|

High-purity, marine-safe innovation

|

Electronics, robotics, marine materials

|

|

Singapore

|

Clinical translation

|

Fast regulatory approval

|

Orthopedics, bio-printed scaffolds

|

|

United Kingdom

|

Design-led biomaterials

|

Luxury and healthcare crossover

|

Fashion, resorbable implants

|

Biomimetic Materials Market Report Scope

Biomimetic Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$42.2 Billion

|

|

Market Size (2035)

|

$82.2 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Material Type (Biomimetic Polymers, Biomimetic Ceramics & Glass, Biomimetic Metals & Alloys, Biohybrid Materials, Biomimetic Composites), By Technology Type (Surface Engineering, Self-Healing Systems, Sensors & Actuators, Structural Biomimicry, Molecular Self-Assembly), By Application (Medical & Healthcare, Aerospace & Defense, Automotive, Construction & Architecture, Textiles & Wearables, Electronics, Environmental Protection)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, BASF SE, DuPont de Nemours Inc., Stryker Corporation, Evonik Industries AG, Festo SE & Co. KG, Kyocera Corporation, TDK Corporation, Koninklijke DSM N.V., Boston Scientific Corporation, Medtronic plc, Zimmer Biomet Holdings Inc., CeramTec GmbH, Ecovative Design LLC, Veryan Medical Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biomimetic Materials Market Segmentation

By Material Type

- Biomimetic Polymers

- Biomimetic Ceramics and Glass

- Biomimetic Metals and Alloys

- Biohybrid Materials

- Biomimetic Composites

By Technology Type

- Surface Engineering

- Self-Healing Systems

- Sensors and Actuators

- Structural Biomimicry

- Molecular Self-Assembly

By Application

- Medical and Healthcare

- Aerospace and Defense

- Automotive

- Construction and Architecture

- Textiles and Wearables

- Electronics

- Environmental Protection

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Biomimetic Materials Market

- 3M Company

- BASF SE

- DuPont de Nemours, Inc.

- Stryker Corporation

- Evonik Industries AG

- Festo SE & Co. KG

- Kyocera Corporation

- TDK Corporation

- Koninklijke DSM N.V.

- Boston Scientific Corporation

- Medtronic plc

- Zimmer Biomet Holdings, Inc.

- CeramTec GmbH

- Ecovative Design LLC

- Veryan Medical Limited

*- List not Exhaustive