Strong Growth Outlook for the Membranes for Water and Wastewater Market

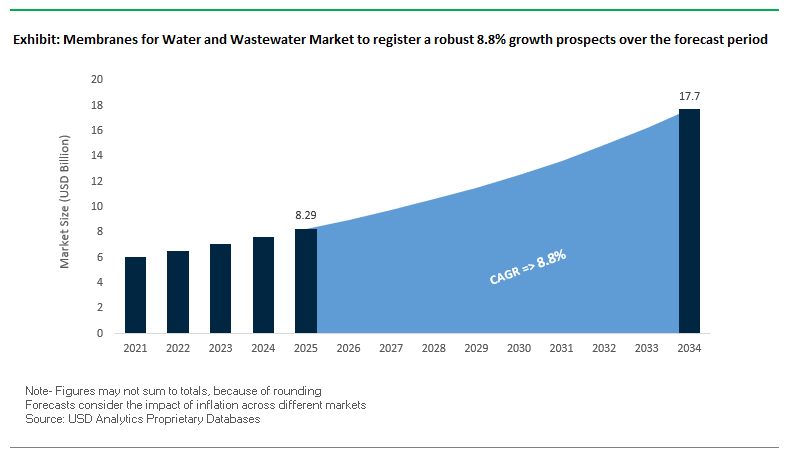

The global membranes for water and wastewater market is projected to grow from USD 8.29 billion in 2025 to USD 17.7 billion by 2034, reflecting a CAGR of 8.8%. This surge is fueled by rising industrial adoption of water reuse, decentralized treatment solutions, and urgent demand for potable water accessibility. Membranes have emerged as a cornerstone of sustainable water management, enabling industries and municipalities to optimize resource efficiency, meet environmental compliance, and lower operating costs.

Industrial adoption is the single largest driver, with industries contributing to almost half of the global water recycle and reuse revenue. Advanced filtration membranes particularly reverse osmosis (RO), ultrafiltration (UF), and membrane bioreactors (MBR) are central to this transformation, ensuring cost-effective treatment of complex effluents. At the same time, municipalities and communities are deploying decentralized modular systems, such as nanofiltration skids and compact membrane bioreactors, that deliver 50–500 cubic meters per day of potable or process water while reducing reliance on large-scale centralized networks.

Technology advancements are significantly reshaping the market. New low-pressure ultrafiltration units and energy-efficient RO stacks are cutting electricity consumption for both industrial and municipal operators. Meanwhile, sustainability is no longer optional as of 2024, 2.2 billion people still lacked access to safely managed drinking water (WHO/UNICEF), highlighting the urgent global need for scalable purification systems. The market is therefore pivoting toward solutions that reduce chemical use, minimize waste, and support long-term water security.

Key Market Insights:

- Industrial leadership in reuse: Industries now account for 50% of water recycle and reuse revenues.

- Decentralized adoption: Growth of “off-grid” treatment with membrane bioreactors and nanofiltration skids.

- Efficiency gains: Energy reductions through low-pressure UF and advanced RO stacks.

- Global water gap: 2.2 billion people remain without safe drinking water, reinforcing demand for advanced membrane solutions.

Market Analysis: Recent Developments Shaping the Membrane Industry

The membranes for water and wastewater market is undergoing rapid transformation, with recent announcements underscoring both technological progress and strategic expansion. In July 2025, SUEZ commissioned China’s largest industrial membrane-based seawater desalination plant at Wanhua Chemical’s Penglai Industrial Park. This landmark project reflects growing industrial reliance on seawater desalination as a reliable and sustainable supply source.

In August 2025, a peer-reviewed scientific study emphasized the effectiveness of membranes in treating radioactive and heavy metal wastewater, showcasing their ability to minimize secondary pollution. That same month, Pentair plc strengthened its municipal water portfolio by acquiring Hydra-Stop, a leader in specialty valve solutions further enhancing its infrastructure-focused water treatment business. Also in July 2025, Asahi Kasei’s Microza® hollow fiber membrane achieved a Gold rating in the EcoVadis sustainability assessment, placing its water division among the top 5% of all evaluated companies worldwide.

Earlier in June 2025, Koch Technology Solutions announced that its membrane-enabled PTA production line reached full capacity, highlighting the integration of membranes in petrochemical processes. In parallel, SUEZ won three new water projects across Asia, including a seawater reverse osmosis (SWRO) plant in the Philippines and a smart water grid platform in Singapore.

Technology innovation remains central to market expansion. In March 2025, DuPont Water Solutions launched WAVE PRO, a digital ultrafiltration modeling tool to help engineers optimize plant designs. Meanwhile, Toray Industries secured a reverse osmosis membrane order in February 2024 for Saudi Arabia’s Yanbu 4 IWP desalination project the first in the Kingdom powered by clean energy under a public-private partnership model. Collectively, these developments reinforce the momentum toward digitalization, sustainable desalination, and industry-driven water security initiatives.

Key Trends and Opportunities in the Membranes for Water and Wastewater Market

Stricter Regulatory Landscape Driving Membrane Adoption

One of the most transformative trends in the membranes for water and wastewater market is the enforcement of increasingly stringent discharge and reuse regulations by global authorities. In India, for example, the Central Pollution Control Board (CPCB) mandates effluent treatment and reuse, with penalties exceeding ₹80,000 crore already imposed by the National Green Tribunal (NGT) for non-compliance. Such regulatory actions are forcing municipalities and industries to invest in membrane-based treatment systems to meet quality norms, minimize liabilities, and ensure sustainable water management practices.

Breakthroughs in High-Performance Membrane Materials

Technological innovation is rapidly reshaping the market, with next-generation membranes being designed for higher efficiency, reduced fouling, and extended operational lifespans. Research from Imperial College London, for instance, showcased a PVDF-based membrane that is 15 times more efficient than existing standards while maintaining pore size integrity. This breakthrough overcomes the traditional trade-off between permeance and separation quality, opening new avenues for cost-effective, high-performance solutions that can address both municipal and industrial challenges.

Expanding Industrial Investments in Water Reuse Systems

Corporate strategies increasingly center around water sustainability, with industries prioritizing on-site wastewater treatment and reuse to mitigate risks associated with scarcity and regulatory pressures. A global filtration technology leader recently announced a large-scale membrane manufacturing facility in India to meet rising demand, while LG Water Solutions launched new ultrafiltration and membrane bioreactor products engineered for higher durability. These investments highlight a clear opportunity for membrane suppliers to capitalize on the surge of industrial and commercial adoption.

Rising Role of Desalination in Securing Water Supply

With freshwater resources under growing strain, desalination projects represent a critical growth avenue for membrane adoption. Reverse osmosis membranes dominate this trend, particularly in arid and coastal regions. A large-scale plant upgrade in Morocco exemplifies this shift, designed to increase desalination capacity and combat water scarcity. Similar initiatives across the Middle East, North Africa, and parts of Asia underscore desalination as a strategic opportunity for membrane manufacturers to scale operations and secure long-term contracts with governments and utilities.

Market Share Analysis of the Membranes for Water and Wastewater Market

Market Share by Technology

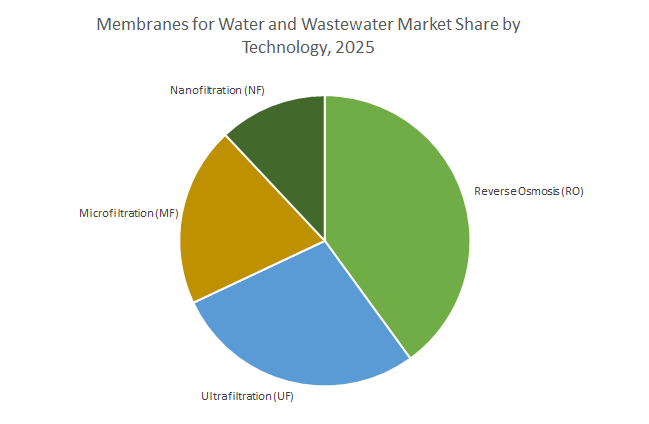

Reverse Osmosis (RO) is projected to lead the technology landscape with a 40% share in 2025, driven by its indispensable role in desalination and industrial process water treatment. Its ability to remove dissolved salts and ions makes it the ultimate choice for high-purity water production. Ultrafiltration (UF), holding about 28% share, serves as the backbone for municipal potable water and membrane bioreactor (MBR) systems, also acting as the preferred pre-treatment for RO plants. Microfiltration (MF) accounts for 20%, widely applied in turbidity removal and wastewater clarification, while Nanofiltration (NF), with 12%, is gaining ground as a sustainable alternative to chemical softening, offering selective removal of divalent ions and organic contaminants.

Market Share by Application

Wastewater Treatment & Reuse will dominate with 38% market share by 2025, reflecting the growing emphasis on circular water economies, industrial water recycling, and zero-liquid discharge (ZLD) systems. Potable Water Production follows closely at 35%, driven by population growth, infrastructure modernization, and the need to replace conventional sand filtration plants with more compact and reliable membrane systems. Pre-treatment for Industrial Processes, projected at 27%, holds strong value importance, particularly in sectors such as microelectronics, pharmaceuticals, and power generation, where ultra-pure water is critical to operational integrity and product quality.

Market Share by Material

Polymeric membranes will overwhelmingly dominate the market, representing around 92% share by 2025, due to their cost-effectiveness, scalability, and wide applicability across all water treatment processes. Continuous improvements in polymeric formulations such as PVDF, PES, and PA enhance fouling resistance and operational durability, reinforcing their stronghold. Ceramic membranes, though at 8%, represent the fastest-growing niche, particularly in extreme industrial wastewater environments where polymers underperform. Their resistance to high temperatures, aggressive chemicals, and abrasive conditions positions them as the preferred choice for heavy-duty operations with long-term lifecycle value.

Membranes for Water and Wastewater Market – Country Analysis

China: Regulatory Policies and Infrastructure Investment Driving Membrane Adoption

China’s membranes for water and wastewater market is largely shaped by stringent environmental regulations and strategic government investments. The Ministry of Ecology and Environment (MEE) mandates strict compliance for industrial wastewater discharge, compelling companies to implement advanced membrane filtration systems. In 2024, researchers introduced hollow-fiber ultrafiltration membranes with enhanced antifouling properties, aiming to improve long-term efficiency and reduce maintenance costs of membrane bioreactors (MBRs). Further, China’s 14th Five-Year Plan (2021-2025) emphasizes expanding natural gas production and storage infrastructure, which is expected to increase the adoption of nanofiltration and other membrane technologies in the oil and gas sector, reinforcing China’s position as a critical market for water and wastewater membrane solutions.

Saudi Arabia: Desalination Projects and Technological Advancements Fueling Market Growth

Saudi Arabia is a global leader in desalination, driving strong demand for advanced membranes for water and wastewater treatment. ACWA Power’s Jubail 3A desalination plant, an independent water project (IWP), uses reverse osmosis (RO) membranes to produce 600,000 cubic meters of freshwater per day, highlighting large-scale industrial adoption. The Saline Water Conversion Corporation (SWCC) is advancing energy-efficient RO membranes, such as those at the Yanbu 4 desalination plant producing 450,000 cubic meters per day, supporting the Kingdom’s sustainable development goals. Government initiatives led by the Saudi Water Partnership Company (SWPC), including projects like Rabigh 4, focus on reverse osmosis-based membrane solutions, establishing a strategic shift toward membrane-driven water management infrastructure.

United States: Government Funding and Academic Research Accelerating Membrane Innovation

The United States membranes for water and wastewater market is bolstered by substantial government funding, academic research, and corporate initiatives addressing emerging water contaminants. The Bipartisan Infrastructure Law provides over $50 billion to the Environmental Protection Agency (EPA) to enhance water infrastructure, including addressing PFAS and other emerging contaminants through advanced membrane filtration technologies. NSF-funded research centers focus on developing innovative membranes for water purification, chemical separations, and biopharmaceutical processes, further advancing the market. Corporations such as Veolia Water Technologies have deployed treatment capacities using advanced membrane systems to deliver PFAS-compliant water to over 140,000 Americans, underscoring the combined impact of public and private sector initiatives on market growth.

India: Government Programs and Strategic Infrastructure Investments Driving Adoption

India’s membranes for water and wastewater market is growing rapidly due to government initiatives, urban infrastructure investments, and industrial adoption. The Jal Jeevan Mission and the Department of Science & Technology’s Water Technology Initiative promote R&D in filtration technologies to provide safe and affordable water in rural regions. The Ghaziabad Nagar Nigam successfully raised ₹150 crore via India’s first Certified Green Municipal Bond to develop a Tertiary Sewage Treatment Plant (TSTP) utilizing advanced membrane filtration, including ultrafiltration, for industrial wastewater reuse. Additionally, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant in Chennai, valued at INR 415 crores, highlights large-scale adoption of membrane technologies, emphasizing India’s commitment to sustainable water management.

Japan: Academic Excellence and Corporate Innovation Strengthening Market Position

Japan’s membranes for water and wastewater market is driven by advanced academic research and corporate innovation. A 2024 study from Kobe University’s Membrane Engineering Group demonstrated development of biomimetic and highly porous membranes for water and atmospheric applications, highlighting Japan’s focus on functional and efficient membrane technologies. Toray Industries continues to provide high-performance RO membranes for large-scale desalination projects, such as those in Saudi Arabia, where hollow-fiber ultrafiltration and other membranes serve as critical pretreatment solutions. Japan’s dual focus on research excellence and global project deployment positions it as a key technology provider in the membranes market.

Germany: Industrial Wastewater Treatment and Technological Leadership

Germany is a prominent market for membranes in water and wastewater treatment, driven by industrial applications and technological innovation. PWT Wassertechnik specializes in membrane processes for industrial water reuse, ensuring compliance with strict European environmental regulations. Multinational MANN+HUMMEL focuses on developing innovative membrane, filtration, and digital solutions to address global water challenges, with applications in industrial processes and green energy. Germany’s combination of regulatory adherence, industrial expertise, and technological advancement underscores its leadership in the global membranes market.

Australia: Water Recycling Initiatives and Academic Research Promoting Sustainability

Australia, a country facing chronic water scarcity, has positioned itself as a leader in water recycling and reuse, driving demand for membranes for water and wastewater treatment. The Sydney Water Wollongong Water Resource Recovery Facility employs a combination of microfiltration, ultrafiltration, and reverse osmosis membranes to treat wastewater for irrigation and industrial use. Academic research at Victoria University’s Institute for Sustainable Industries and Liveable Cities (ISILC) focuses on increasing water recovery from desalination and reducing membrane fouling and scaling, critical challenges in sustainable water management. These efforts highlight Australia’s strategic adoption of membrane solutions to enhance water security and efficiency.

Competitive Landscape: Key Players Driving Global Growth

The competitive landscape in the membranes for water and wastewater market is defined by leading multinationals with strong portfolios in RO, UF, nanofiltration (NF), and MBR technologies. These companies are pursuing strategic investments, sustainability initiatives, and partnerships to capture share in both industrial and municipal segments. Their focus is not only on membrane performance but also on enabling low-energy operations, resource recovery, and digital optimization of treatment processes.

DuPont Water Solutions strengthens market leadership with integrated portfolio

DuPont offers one of the most comprehensive technology portfolios, including RO, UF, ion exchange, and MBR systems. Its Water Solutions Sustainability Navigator enables customers to measure and compare environmental impacts such as carbon footprint and chemical use, reinforcing its leadership in sustainable innovation. Recognition as the 2024 Water Technology Company of the Year underscores its R&D capabilities. A recent textile industry pilot in India achieved 75% lower cleaning costs and 10% energy savings using DuPont’s minimal liquid discharge approach.

SUEZ delivers large-scale desalination and digital water platforms

SUEZ is renowned for executing complex projects, such as China’s largest membrane-based desalination plant. Its expertise in public-private partnerships is evidenced by its collaboration with the Senegalese government to expand access to safe water. The company’s AQUADVANCED® Water Networks platform is reshaping digital water management, driving operational efficiency and resilience. As part of the Veolia group, SUEZ is expanding integrated water reuse and resource recovery solutions globally.

Toray Industries drives high-performance RO membranes in the Middle East

Toray has a strong reputation for reverse osmosis membranes in large-scale desalination projects, with installations at Yanbu 4 and Shuaibah 3 in Saudi Arabia. Its membranes are projected to cut CO₂ emissions by 45 million tons annually and reduce crude oil consumption by 22 million barrels through eco-friendly conversion of conventional plants. With a broad portfolio spanning RO, UF, and MBR, and the establishment of a Water Technology Center in Saudi Arabia, Toray continues to solidify its Middle East presence.

Koch Separation Solutions rebrands as Kovalus with innovation-driven focus

Koch Separation Solutions (KSS), now Kovalus Separation Solutions, is advancing with its PURON® reinforced hollow fiber membranes, recognized for durability, low fouling, and cost efficiency. The company is also realigning operations, closing a U.S. plant while investing $20 million in a new Mexican facility to boost production by 50%. With tailored applications across food, beverage, life sciences, and textiles, Kovalus demonstrates flexibility in meeting industry-specific water challenges.

Pentair expands municipal water solutions through acquisitions

Pentair has been consolidating its infrastructure portfolio, most notably with the August 2025 acquisition of Hydra-Stop, reinforcing its solutions for municipalities. With $4.1 billion in 2024 revenues, Pentair combines scale with a focus on smart, sustainable water solutions for both residential and commercial markets. Its strategy of targeted acquisitions enhances its ability to grow in municipal and industrial water treatment infrastructure.

Asahi Kasei advances sustainable membranes and green hydrogen integration

Asahi Kasei is aligning water treatment with clean energy transitions. Its Microza® membrane technology earned a Gold sustainability rating from EcoVadis, while ongoing investments of ¥35 billion in electrolyzer membrane production position the company at the forefront of green hydrogen supply chains. Asahi Kasei’s containerized Aqualyzer™-C3 electrolyzer system in Finland demonstrates its integration of membranes into renewable energy projects. In April 2024, it also launched an energy-efficient membrane-based WFI production system, reducing reliance on distillation.

Membranes for Water and Wastewater Market Report Scope

Membranes for Water and Wastewater Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.29 Billion

|

|

Market Size (2034)

|

$17.7 Billion

|

|

Market Growth Rate

|

8.8%

|

|

Segments

|

By Technology (Microfiltration, Ultrafiltration, Nanofiltration, Reverse Osmosis), By Application (Potable Water Production, Wastewater Treatment & Reuse, Pre-treatment for Industrial Processes), By Material (Polymeric Membranes, Ceramic Membranes), By Module Design (Spiral Wound, Hollow Fiber, Plate & Frame, Tubular), By End-Users (Municipalities, Industrial Users, Power Generation, Oil & Gas, Food & Beverage, Chemicals & Pharmaceuticals, Mining & Metals, Microelectronics, EPC Companies)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., SUEZ, Veolia, Xylem Inc., Pentair plc, Toray Industries, Inc., Asahi Kasei Corporation, Kubota Corporation, LG Chem, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, Hydranautics (a Nitto Group Company), Koch Industries, V.A. TECH WABAG Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Membranes for Water and Wastewater Market Segmentation

By Technology

- Microfiltration (MF)

- Ultrafiltration (UF)

- Nanofiltration (NF)

- Reverse Osmosis (RO)

By Application

- Potable Water Production

- Wastewater Treatment & Reuse

- Pre-treatment for Industrial Processes

By Material

- Polymeric Membranes

- Ceramic Membranes

By Module Design

- Spiral Wound

- Hollow Fiber

- Plate & Frame

- Tubular

By End-Users

- Municipalities

- Industrial Users

- Power Generation

- Oil & Gas

- Food & Beverage

- Chemicals & Pharmaceuticals

- Mining & Metals

- Microelectronics

- EPC Companies

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Membranes for Water and Wastewater Industry include-

- DuPont de Nemours, Inc.

- SUEZ

- Veolia

- Xylem Inc.

- Pentair plc

- Toray Industries, Inc.

- Asahi Kasei Corporation

- Kubota Corporation

- LG Chem

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- Hydranautics (a Nitto Group Company)

- Koch Industries

- V.A. TECH WABAG Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the global membranes for water and wastewater market, delivering analysis reviews on how industrial reuse mandates, decentralized treatment models, and digitalized plant design are accelerating deployment across utilities and process industries. It highlights breakthroughs that compress energy use and cleaning frequency, advances in module engineering that stabilize RO pretreatment and MBR operations, and policy tailwinds that prioritize resilient potable supply in water-stressed regions. The study further highlights the shift from chemical-intensive flowsheets to low-waste, membrane-centric operations, mapping procurement drivers, reliability KPIs, and country-level implementation pathways. With clear linkages to circular-economy goals and emerging contaminant control, this report is an essential resource for engineers, EPCs, asset owners, and investors planning scalable, regulation-ready projects. Developed by USDAnalytics, it converts technical performance into bankable outcomes for decision-makers. Scope Includes-

- Segmentation: By Technology (Microfiltration (MF), Ultrafiltration (UF), Nanofiltration (NF), Reverse Osmosis (RO)), By Application (Potable Water Production; Wastewater Treatment & Reuse; Pre-treatment for Industrial Processes), By Material (Polymeric Membranes; Ceramic Membranes), By Module Design: Spiral Wound; Hollow Fiber; Plate & Frame; Tubular), By End-Users: Municipalities; Industrial Users; Power Generation; Oil & Gas; Food & Beverage; Chemicals & Pharmaceuticals; Mining & Metals; Microelectronics; EPC Companies)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

- Companies: Profiles of 15+ companies (e.g., DuPont, SUEZ, Veolia, Xylem, Pentair, Toray, Asahi Kasei, Kubota, LG Chem, Dow, MANN+HUMMEL, Evoqua, Hydranautics, Koch, VA TECH WABAG).

Methodology

We apply a mixed-methods approach: primary interviews with utilities, industrial users, OEMs/EPCs, and regulators, combined with secondary research (standards, patents, filings, and peer-reviewed studies). Market sizes are derived via top-down triangulation (end-market capex, installed base, retrofit cycles, reuse mandates) and bottom-up bill-of-materials models by technology (MF/UF/NF/RO), normalizing for flux (LMH), TMP, fouling factors, cleaning regimes, and membrane replacement intervals. Forecasts incorporate technology learning curves, energy-price sensitivity, brine/effluent chemistry, and regulatory thresholds for potable quality and discharge/reuse. Competitive benchmarking evaluates lifecycle cost per 1,000 m³, SDI/turbidity guarantees, PFAS/readily-removable organics protection strategies, and digital O&M maturity. All outputs undergo cross-validation against commissioning data, project announcements, and country policy cadence.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Membranes for Water and Wastewater Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Membranes for Water and Wastewater Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $8.29 Billion

2.2.2. Forecasted Market Size (2034): $17.7 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 8.8%

2.3. Key Market Insights

2.3.1. Industrial Leadership in Reuse

2.3.2. Decentralized Treatment Solutions

2.3.3. Efficiency Gains through Technology

2.3.4. The Global Water Gap as a Market Driver

3. Recent Developments and Strategic Shifts

3.1. Market Trend: Mega-Scale Industrial Projects

3.1.1. SUEZ Commissions China’s Largest Desalination Plant

3.1.2. SUEZ Wins Three New Asia Water Projects

3.2. Market Trend: Sustainability and Digitalization

3.2.1. Asahi Kasei’s Microza® Receives Gold EcoVadis Rating

3.2.2. DuPont Water Solutions Launches WAVE PRO Modeling Tool

3.3. Market Opportunity: Diversification and Innovation

3.3.1. Membranes for Radioactive and Heavy Metal Wastewater

3.3.2. Pentair Acquires Hydra-Stop to Strengthen Municipal Portfolio

3.3.3. Toray Industries Secures Order for Clean Energy-Powered Desalination

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Membrane Suppliers to Integrated Solution Providers

4.2. Key Competitive Factors

4.2.1. Integrated Technology Portfolios

4.2.2. Sustainability and ESG Credentials

4.2.3. Global Project Execution and Service Networks

4.3. Profiles of Top Players

4.3.1. DuPont Water Solutions

4.3.2. SUEZ (Veolia)

4.3.3. Toray Industries, Inc.

4.3.4. Kovalus Separation Solutions (formerly Koch Separation Solutions)

4.3.5. Pentair plc

4.3.6. Asahi Kasei Corporation

5. Membranes for Water and Wastewater Market – Segmentation Insights

5.1. By Technology

5.1.1. Reverse Osmosis (RO)

5.1.2. Ultrafiltration (UF)

5.1.3. Microfiltration (MF)

5.1.4. Nanofiltration (NF)

5.2. By Application

5.2.1. Wastewater Treatment & Reuse

5.2.2. Potable Water Production

5.2.3. Pre-treatment for Industrial Processes

5.3. By Material

5.3.1. Polymeric Membranes

5.3.2. Ceramic Membranes

6. Country Analysis and Outlook: Membranes for Water and Wastewater Market

6.1. China: Regulatory Policies and Infrastructure Investment

6.2. Saudi Arabia: Desalination Projects and Technological Advancements

6.3. United States: Government Funding and Academic Research

6.4. India: Government Programs and Strategic Infrastructure Investments

6.5. Japan: Academic Excellence and Corporate Innovation

6.6. Germany: Industrial Wastewater Treatment and Technological Leadership

6.7. Australia: Water Recycling and Academic Research

6.8. Other Key Countries

6.8.1. North America (Canada, Mexico)

6.8.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.8.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.8.4. South America (Brazil, Argentina, Rest of South America)

6.8.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Membranes for Water and Wastewater Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Technology

7.1.2. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Technology

7.2.2. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Technology

7.3.2. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Technology

7.4.2. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Technology

7.5.2. By Application

8. Company Profiles: Additional Leading Players

8.1. Veolia

8.2. DuPont de Nemours, Inc.

8.3. SUEZ

8.4. Xylem Inc.

8.5. Pentair plc

8.6. Toray Industries, Inc.

8.7. Asahi Kasei Corporation

8.8. Kubota Corporation

8.9. LG Chem

8.10. The Dow Chemical Company

8.11. MANN+HUMMEL

8.12. Evoqua Water Technologies

8.13. Hydranautics (a Nitto Group Company)

8.14. Koch Industries

8.15. V.A. TECH WABAG Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures