Ceramic Membranes Market Overview: Growth Outlook and Key Insights

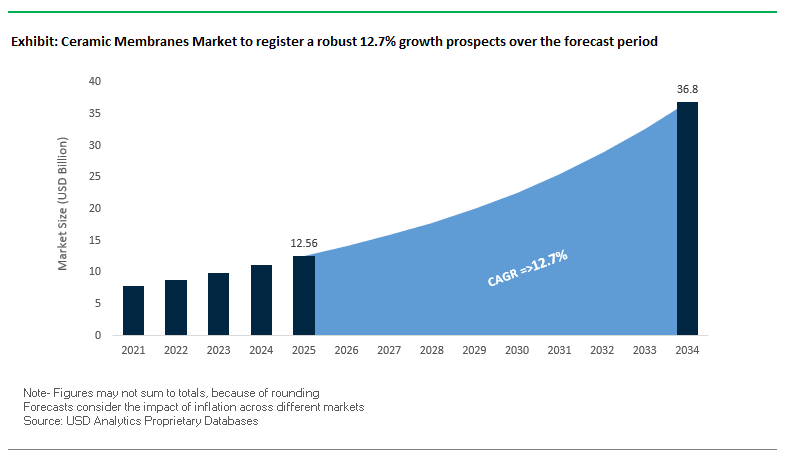

The global ceramic membranes market is projected to expand from USD 12.56 billion in 2025 to USD 36.8 billion by 2034, registering a robust CAGR of 12.7%. This strong growth is driven by the rising adoption of ceramic membranes in industries that demand resilience, cost efficiency, and sustainability. Their unique ability to withstand high temperatures, extreme pH levels, and aggressive chemicals positions ceramic membranes as a superior alternative to polymeric membranes in oil & gas, industrial wastewater, food & beverage, pharmaceuticals, and desalination applications.

For buyers and industry Stakeholders, the value proposition lies in the extended lifespan, lower lifecycle costs, and reduced energy consumption of ceramic membranes. As industries worldwide intensify water reuse and circular economy initiatives, ceramic membranes are emerging as a critical enabler of high-efficiency separation and pre-treatment processes.

Key Market Insights

- Durability in Harsh Environments: Ceramic membranes excel in demanding industries such as oil & gas, chemical processing, and municipal wastewater due to their resistance to high temperature, pressure, and corrosive chemicals.

- Lower Lifecycle Costs: Their lifespan often decades reduces replacement frequency and maintenance, delivering cost advantages compared to polymeric alternatives.

- Superior Fouling Resistance: High hydrophilicity and unique surface structures enable higher flux and lower fouling, minimizing downtime and cleaning cycles.

- Pre-Treatment Role in Reverse Osmosis: Increasingly deployed ahead of RO systems, ceramic membranes safeguard sensitive membranes from suspended solids, oils, and grease.

- Energy Savings: By reducing fouling and cleaning needs, ceramic membranes lower pumping energy demand, making them attractive for desalination and large-scale water reuse projects.

Market Analysis: Recent Developments Driving Ceramic Membrane Adoption

The ceramic membranes industry is experiencing rapid innovation, strategic collaborations, and expanding deployment across critical applications.

In July 2025, Nanostone Water and Solecta merged to form Acuriant Technologies, combining polymeric and ceramic membrane expertise to address complex water and separation challenges. That same month, Veolia advanced water reuse technologies in Brazil, showcasing ceramic membranes as key enablers of circular water economy projects in Latin America.

In June 2025, Meiden Singapore launched a demonstration plant integrating ceramic flat-sheet membranes for seawater reverse osmosis (SWRO) pre-treatment. This large-scale initiative highlights Singapore’s leadership in desalination efficiency. In May 2025, Nanostone Water introduced its CUF|ShieldPlus™ ceramic ultrafiltration module, designed to tackle the toughest wastewater streams in semiconductor manufacturing, a high-growth end-use sector.

March 2025 marked a milestone for TAMI Industries, which announced a partnership to apply ceramic membranes in advanced beer filtration, underscoring the growing use of ceramic technologies in the food & beverage industry. In February 2025, LiqTech International delivered a pilot unit for oily wastewater treatment at a U.S. steel producer, signaling diversification into new end markets.

Looking back to 2024, momentum was already building: in June 2024, Meiden Singapore and PUB (Singapore’s National Water Agency) partnered on energy-efficient ceramic flat-sheet membranes for seawater desalination, while in April 2024, Nanostone Water and ENOWA (Saudi Arabia’s NEOM subsidiary) signed an MoU to apply ceramic ultrafiltration in sustainable brine mining projects. These developments collectively demonstrate how ceramic membranes are not just replacing polymeric systems but also enabling new applications across industries.

Key Trends Transforming the Ceramic Membranes Market

Growing Demand for Industrial Wastewater Treatment and Recycling

A major trend driving the ceramic membranes market is the growing adoption of advanced separation technologies for industrial wastewater treatment and recycling. Industries across oil & gas, chemicals, and heavy manufacturing are under regulatory pressure to reduce effluent discharge and increase water reuse. Ceramic membranes are increasingly preferred due to their ability to withstand high temperatures and manage high solids loading, making them more reliable than polymeric alternatives. For example, Veolia Water Solutions & Technologies presented case studies in 2021 highlighting the successful treatment of oily wastewater in the oil and gas industry using ceramic membranes. The ability to reuse treated water for processes such as oil well reinjection not only supports sustainability goals but also reduces dependence on freshwater sources, a critical factor in water-stressed regions.

Technological Innovations in Low-Cost Manufacturing Processes

Another significant trend is the industry-wide effort to reduce the cost of ceramic membrane manufacturing, traditionally considered a major barrier to adoption. Research efforts are increasingly focused on leveraging alumina, clays, and other abundant raw materials to create cost-effective alternatives. The Council of Scientific and Industrial Research (CSIR) in India has taken major strides by establishing a pre-pilot plant for producing alumina-based ceramic membranes, showcasing water flux rates of 100–200 LMH, a benchmark performance metric. Government-backed initiatives to indigenize production and scale manufacturing are expected to make ceramic membranes economically feasible for price-sensitive markets, expanding adoption in municipal water treatment and mid-scale industries.

Expansion into High-Value Industrial Separation Applications

The scope of ceramic membranes is extending beyond conventional water and wastewater treatment into high-value separations such as solvent recovery, chemical processing, and gas separations. Companies like CoorsTek are pioneering innovations in active ceramic membranes, including technologies enabling the direct conversion of natural gas into liquids, reducing carbon emissions and streamlining processes. Such breakthroughs highlight the transformative potential of ceramic membranes in petrochemical and energy-intensive industries, where process efficiency and carbon reduction are top priorities.

Replacement of Polymeric Membranes in Harsh Environments

Ceramic membranes are also witnessing a rising trend of replacing polymeric membranes in environments characterized by extreme pH, abrasive particulates, and high-temperature operations. Their projected service life of up to 20 years, as highlighted by CERAFILTEC, gives them a clear economic advantage in lifecycle cost. Their proven durability has made them attractive for municipal water treatment, industrial wastewater recovery, and power plant effluent treatment. The trend toward replacing polymeric membranes in legacy systems underlines the long-term shift toward ceramic-based solutions for critical operations requiring higher reliability.

Market Share Analysis of the Ceramic Membranes Market

Market Share by Material- Alumina Dominates the Global Market with 50% Share

Alumina-based membranes remain the cornerstone of the ceramic membranes market, accounting for nearly half of the total share in 2025. Their balance of performance, affordability, and adaptability across applications such as municipal water treatment, food and beverage processing, and pharmaceuticals positions them as the industry’s most widely deployed solution. Titania membranes, holding 20%, are increasingly valued for their photocatalytic properties and resilience in acidic environments, making them ideal for pharmaceuticals and specialty chemicals. Zirconium oxide membranes (15%) dominate high-value industrial separations, given their mechanical strength and resistance to both acidic and alkaline extremes. Meanwhile, niche categories like silica are growing in gas separations due to their tunable pore sizes, while silicon carbide is gaining ground in abrasion-heavy wastewater treatment, highlighting its potential in mining and textile industries.

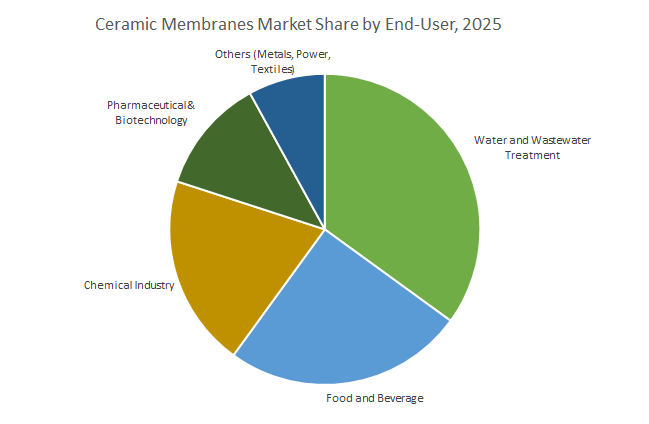

Market Share by End-User Industry- Water and Wastewater Treatment Holds the Largest Share at 35%

End-user analysis reveals that the water and wastewater treatment sector is the largest consumer of ceramic membranes, accounting for approximately 35% of market share. This dominance is attributed to stringent discharge norms, municipal water security goals, and the growing demand for reuse and recycling. The food and beverage sector follows with 25% share, leveraging ceramic membranes’ steam sterilizability and CIP/SIP compatibility for applications such as whey protein concentration, juice clarification, and beer filtration. The chemical industry (20%) is another major segment, using ceramic membranes to manage harsh solvents, extreme temperatures, and catalyst recovery processes that would rapidly degrade polymeric membranes. Pharmaceutical and biotechnology applications (12%) are expanding due to the demand for sterile filtration, reliable cell harvest, and high-value biologics clarification. In addition, the “Others” category (8%) is gaining attention, particularly in metal recovery, textile dye concentration, and flue gas desulfurization wastewater treatment, representing diverse and fast-emerging opportunities across resource-intensive industries.

China: Advanced Ceramic Membranes Driving Industrial Water Reuse

China is a major driver in the global ceramic membranes market, fueled by regulatory mandates and technological innovation. The Ministry of Ecology and Environment (MEE) enforces stringent industrial wastewater discharge standards, compelling companies to invest in advanced on-site treatment systems, including ceramic membranes. Technological advancements in 2024, such as hollow-fiber ultrafiltration membranes with enhanced antifouling properties, are improving long-term operational efficiency and reducing maintenance costs in membrane bioreactors (MBRs). Domestic production expansions and competitive pricing have strengthened China’s position in the global market, while key applications, such as textile wastewater recycling, leverage ceramic membranes to recover over 95% of process water from high-temperature, high-strength effluents.

United States: Government Support and Research-Driven Innovation

The U.S. ceramic membranes market is supported by significant government funding and advanced research initiatives. The Bureau of Reclamation has funded low-pressure ceramic membrane projects to reduce desalination costs, while the NSF promotes R&D in water purification and chemical separations. Major corporate projects, such as the 2023 inauguration of the world’s largest membrane-based carbon capture plant by Membrane Technology and Research, Inc., highlight the broader adoption of advanced membrane solutions, including ceramic membranes, in water and gas treatment applications.

Germany: Industrial Excellence and Global Ceramic Membrane Leadership

Germany leads in industrial wastewater treatment applications of ceramic membranes, driven by environmental compliance and innovation. PWT Wassertechnik delivers industrial-scale ceramic filtration solutions to treat and reuse wastewater, while CERAFILTEC announced in 2024 the deployment of ceramic flat membranes for MBR projects across four continents, covering capacities from 250 m³/d to 10,000 m³/d. Corporate initiatives by MANN+HUMMEL focus on digital solutions and innovative membrane technologies to address global water challenges, with applications spanning industrial process solutions and green energy.

Japan: Cutting-Edge R&D and Widespread MBR Adoption

Japan is at the forefront of ceramic membrane innovation through academic and corporate R&D. In 2025, Toray Industries introduced next-generation hollow fiber membranes with 20% higher permeability and reduced fouling, lowering operational costs in MBR systems. The Ministry of the Environment allocated USD 1.2 billion in 2024 for sustainable wastewater infrastructure, supporting ceramic membrane integration. Japan hosts over 3,000 full-scale MBR installations, with companies like Metawater deploying ceramic membranes to eliminate impurities and turbidity in municipal and industrial water treatment.

Australia: Water Recycling Leadership and Next-Generation Filtration

Australia faces significant water scarcity, making water recycling and advanced membrane systems essential. The Australian Water Recycling Centre of Excellence demonstrated the cost and performance benefits of ceramic membranes for treating secondary effluent with high organic content. Innovative installations, such as the Narromine Shire Council’s submerged flat-sheet ceramic membrane system from Cerafiltec, showcase next-generation technology in regional applications. Academic research at Victoria University’s ISILC focuses on maximizing water recovery from desalination and minimizing membrane fouling and scaling, addressing key challenges in ceramic membrane adoption.

Saudi Arabia: Desalination Investments and Early Ceramic Membrane Adoption

Saudi Arabia, a global desalination leader, invests heavily in advanced water treatment. Projects like the Jubail 3A desalination plant, led by ACWA Power, primarily use reverse osmosis (RO) but offer potential for ceramic membrane integration in harsh operating conditions. Early adoption is evident from orders placed with ItN Nanovation AG for flat ceramic membranes in groundwater treatment projects, demonstrating the region’s willingness to explore ceramic technologies for enhanced durability and performance.

Competitive Landscape: Key Players in the Ceramic Membranes Market

The ceramic membranes market is moderately consolidated, with leading players focusing on material innovation, industry-specific solutions, and global partnerships. Companies are leveraging their strengths to expand into new markets, improve energy efficiency, and align with the circular economy.

LiqTech International: Silicon Carbide Leadership in Extreme Applications

LiqTech International, Inc. specializes in silicon carbide (SiC) ceramic membranes, known for exceptional chemical and thermal stability. The company is expanding into new industries, including a pilot system for oily wastewater treatment for a U.S. steel producer (Feb 2025). With an 11% revenue increase in Q2 2025, LiqTech expects full-year revenues to reach a four-year high, driven by liquid filtration growth. Its diversification strategy positions it strongly in marine, oil & gas, and industrial wastewater markets.

Nanostone Water: Expanding Through Strategic Merger and Product Innovation

In July 2025, Nanostone Water merged with Solecta to create Acuriant Technologies, offering both ceramic and polymeric solutions. Known for desalination pre-treatment, Nanostone’s CUF|ShieldPlus™ module (May 2025) addresses semiconductor wastewater challenges. Partnerships with ENOWA (2024) in Saudi Arabia and approvals such as the UK’s Regulation 31 highlight its credibility in drinking water and industrial reuse markets.

TAMI Industries: Filtration Expertise in Food, Beverage, and Biopharma

TAMI Industries specializes in tangential flow filtration with a broad ceramic product portfolio spanning ultrafiltration to microfiltration. The company is strengthening its position in biopharma and food & beverage, with ceramic membranes applied in whey protein concentration, wine clarification, and most recently, beer filtration (March 2025). Its focus on eco-efficient, industry-specific solutions underlines its competitive edge.

Cembrane A/S: Proven Global Adoption with Ovivo Support

Cembrane A/S, acquired by Ovivo in 2021, is a leader in SiC flat-sheet ceramic membranes. With installations in 450+ sites across 65 countries, Cembrane’s membranes are valued for fouling resistance and durability. Its partnership with Ovivo has expanded applications in municipal wastewater, drinking water, and industrial sectors, while leveraging Ovivo’s global reach to accelerate adoption.

Meidensha Corporation: Pioneering Large-Scale Ceramic Membrane Plants

Meidensha Corporation, through Meiden Singapore, is at the forefront of large-scale ceramic membrane deployment. Its supply of membranes for the Chestnut Avenue Waterworks (CAWW) in Singapore set to be the world’s largest ceramic membrane facility by 2026 demonstrates its scale capabilities. Meidensha’s focus on seawater desalination pre-treatment (June 2025 demo plant) emphasizes energy efficiency and cost reduction for utilities and industrial clients.

aTech Innovations GmbH: Purity and Sustainability through Advanced Manufacturing

aTech Innovations manufactures high-purity ceramic membranes from 100% aluminum oxide, ensuring resistance to caustics, acids, and high temperatures. Its unique binder-free process results in durable membranes designed for long lifespans, energy savings, and cost efficiency. Recently, aTech entered a strategic partnership to expand into stainless steel membranes, diversifying its portfolio and strengthening its position in chemical processing, pharmaceuticals, and water treatment.

Ceramic Membranes Market Report Scope

Ceramic Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.56 Billion

|

|

Market Size (2034)

|

$36.8 Billion

|

|

Market Growth Rate

|

12.7%

|

|

Segments

|

By Material (Alumina, Silica, Titania, Zirconium Oxide, Others), By End-User (Water and Wastewater Treatment, Food and Beverage, Chemical Industry, Pharmaceutical, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Veolia, SUEZ, Toray Industries, Inc., Asahi Kasei Corporation, Pentair plc, LiqTech Holding A/S, TAMI Industries, Kubota Corporation, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, LG Chem, W. L. Gore & Associates, Inc., Mitsubishi Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ceramic Membranes Market Segmentation

By Material

- Alumina

- Silica

- Titania

- Zirconium Oxide

- Others

By End-User

- Water and Wastewater Treatment

- Food and Beverage

- Chemical Industry

- Pharmaceutical

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Ceramic Membranes Industry include-

- DuPont de Nemours, Inc.

- Veolia

- SUEZ

- Toray Industries, Inc.

- Asahi Kasei Corporation

- Pentair plc

- LiqTech Holding A/S

- TAMI Industries

- Kubota Corporation

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- LG Chem

- W. L. Gore & Associates, Inc.

- Mitsubishi Chemical Corporation

*- List not Exhaustive

Research Coverage

This report investigates how ceramic membranes are scaling across high-stress separations, where breakthroughs in materials (alumina, titania, zirconia, SiC) and module engineering are resetting total cost of ownership; our analysis reviews durability economics, pre-treatment performance ahead of RO, and application pivots in industrial wastewater, F&B, pharma, and desalination. It highlights vendor moves, partnerships, and pilot-to-plant learnings that validate longer service life, wider pH/temperature windows, and lower cleaning frequency. Framed by adoption drivers, risk factors, and bankable KPIs, this report is an essential resource for utilities, EPCs, plant owners, and OEMs standardizing rugged filtration. Produced by USDAnalytics, the study benchmarks membrane chemistries, lifecycle energy, and retrofit pathways to support capex/opex decisions without bias. Scope Includes-

- Segmentation: By Material (Alumina, Silica, Titania, Zirconium Oxide, Others), By End-User (Water & Wastewater Treatment, Food & Beverage, Chemical Industry, Pharmaceutical, Others)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic 2021–2024 and forecast 2025–2034.

- Companies (Profiles of 15+ firms): DuPont de Nemours, Inc.; Veolia; SUEZ; Toray Industries, Inc.; Asahi Kasei Corporation; Pentair plc; LiqTech Holding A/S; TAMI Industries; Kubota Corporation; The Dow Chemical Company; MANN+HUMMEL; Evoqua Water Technologies; LG Chem; W. L. Gore & Associates, Inc.; Mitsubishi Chemical Corporation

Methodology

USDAnalytics applied a mixed-method approach: (1) Top-down sizing from installed capacity additions, end-user CAPEX plans, and regulatory timelines; (2) Bottom-up models at material level (alumina/titania/zirconia/SiC), mapping flux (LMH), TMP, recovery, CIP/SIP cadence, and replacement intervals to cost per 1,000 m³; (3) Primary research with utilities, EPCs, and operators to validate duty conditions (oils/grease, high solids, extreme pH, temperature) and pre-RO performance; (4) Competitive benchmarking of vendors on durability, fouling resistance, energy draw, and warranty terms; (5) Scenario analysis for price learning in ceramic manufacturing, supply-chain risk, and retrofit sensitivity; and (6) Quality controls via triangulation with pilot/commissioning data, peer-reviewed studies, and public disclosures to ensure reproducible forecasts through 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Ceramic Membranes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Ceramic Membranes Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $12.56 Billion

2.2.2. Forecasted Market Size (2034): $36.8 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 12.7%

2.3. Key Trends and Opportunities

2.3.1. Growing Demand for Industrial Wastewater Treatment and Recycling

2.3.2. Technological Innovations in Low-Cost Manufacturing Processes

2.3.3. Expansion into High-Value Industrial Separation Applications

2.3.4. Replacement of Polymeric Membranes in Harsh Environments

3. Recent Developments and Strategic Shifts

3.1. Corporate Strategy: Mergers and Partnerships

3.1.1. Nanostone Water and Solecta Merge to Form Acuriant Technologies

3.1.2. Veolia Advances Water Reuse in Brazil

3.1.3. TAMI Industries Partners for Beer Filtration

3.1.4. LiqTech International Delivers Pilot Unit for Oily Wastewater

3.1.5. Nanostone Water and ENOWA Sign MoU for Brine Mining

3.2. Product and Project Milestones

3.2.1. Meiden Singapore Launches Demonstration Plant for Desalination

3.2.2. Nanostone Water Introduces CUF|ShieldPlus™ Module

3.2.3. Meiden Singapore and PUB Partner on Energy-Efficient Membranes

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Material Specialists to Global Solution Providers

4.2. Key Competitive Factors

4.2.1. Material Innovation and Purity

4.2.2. Expertise in Industry-Specific Solutions

4.2.3. Strategic Global Partnerships and Project Execution

4.3. Profiles of Top Players

4.3.1. LiqTech International

4.3.2. Nanostone Water

4.3.3. TAMI Industries

4.3.4. Cembrane A/S

4.3.5. Meidensha Corporation

4.3.6. aTech Innovations GmbH

5. Ceramic Membranes Market – Segmentation Insights

5.1. By Material

5.1.1. Alumina

5.1.2. Silica

5.1.3. Titania

5.1.4. Zirconium Oxide

5.1.5. Others

5.2. By End-User

5.2.1. Water and Wastewater Treatment

5.2.2. Food and Beverage

5.2.3. Chemical Industry

5.2.4. Pharmaceutical

5.2.5. Others

6. Country Analysis and Outlook: Ceramic Membranes Market

6.1. China: Advanced Ceramic Membranes Driving Industrial Water Reuse

6.2. United States: Government Support and Research-Driven Innovation

6.3. Germany: Industrial Excellence and Global Ceramic Membrane Leadership

6.4. Japan: Cutting-Edge R&D and Widespread MBR Adoption

6.5. Australia: Water Recycling Leadership and Next-Generation Filtration

6.6. Saudi Arabia: Desalination Investments and Early Ceramic Membrane Adoption

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Ceramic Membranes Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Material

7.1.2. By End-User

7.2. Europe Market Size Outlook to 2034

7.2.1. By Material

7.2.2. By End-User

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Material

7.3.2. By End-User

7.4. South America Market Size Outlook to 2034

7.4.1. By Material

7.4.2. By End-User

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Material

7.5.2. By End-User

8. Company Profiles: Additional Leading Players

8.1. DuPont de Nemours, Inc.

8.2. Veolia

8.3. SUEZ

8.4. Toray Industries, Inc.

8.5. Asahi Kasei Corporation

8.6. Pentair plc

8.7. LiqTech Holding A/S

8.8. TAMI Industries

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. MANN+HUMMEL

8.12. Evoqua Water Technologies

8.13. LG Chem

8.14. W. L. Gore & Associates, Inc.

8.15. Mitsubishi Chemical Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures