Textile Wastewater Treatment Equipment Market Overview

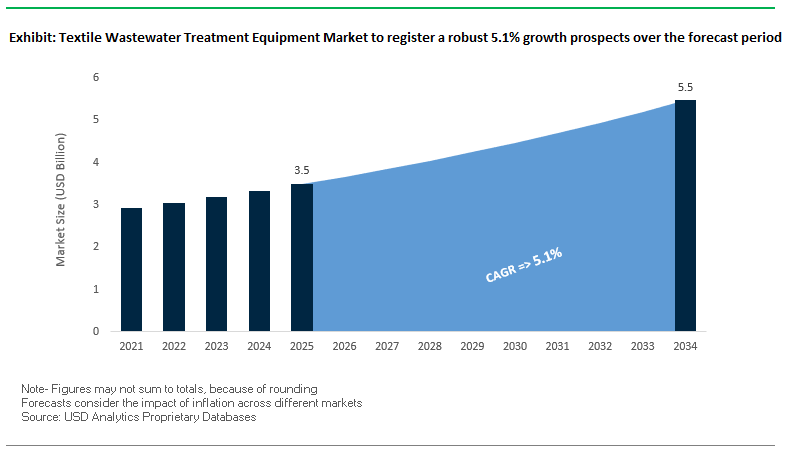

The global textile wastewater treatment equipment market is projected to grow from $3.5 billion in 2025 to $5.5 billion by 2034, reflecting a steady CAGR of 5.1%. This growth highlights the increasing urgency for textile manufacturers to adopt advanced water treatment technologies in order to meet strict environmental regulations, reduce reliance on freshwater, and achieve sustainability goals. Industry Stakeholders are seeking solutions that not only meet compliance but also provide cost efficiencies, high recovery rates, and energy optimization.

Key Insights for Industry Stakeholders

- Industrial dominance: The industrial sector, particularly textiles, is one of the largest consumers of wastewater treatment systems due to the complex chemical loads in dyeing and finishing processes.

- Water reuse success stories: In Tamil Nadu, India, textile mills using Minimum Liquid Discharge (MLD) systems have achieved over 70% water recovery through technologies like reverse osmosis, significantly reducing freshwater dependency.

- Resource intensity: A single textile mill can consume 100 liters of water per kilogram of fabric produced, underscoring the scale of the challenge and the importance of efficient wastewater management.

- Regional leadership: Asia-Pacific dominates the market due to its vast textile production hubs and increasingly stringent government regulations on effluent discharge.

Market Analysis: Recent News and Developments in Textile Wastewater Treatment

The textile wastewater treatment equipment industry is rapidly evolving, driven by sustainability mandates, energy recovery goals, and advancements in ZLD and MLD technologies. Companies are actively pursuing acquisitions, strategic partnerships, and breakthrough innovations to strengthen their market position and address the rising demand for water reuse and resource recovery solutions in textiles.

In August 2025, DuPont Water Solutions received recognition in the BIG Sustainability Awards for its leadership in industrial wastewater reuse and minimal liquid discharge systems, cementing its reputation as a key sustainability partner for textile manufacturers. Similarly, in July 2025, SUEZ inaugurated France’s largest biogas unit at the Seine Aval wastewater treatment plant, showcasing how wastewater can be transformed into an energy resource. That same month, Veolia Water Technologies was chosen to equip France’s largest treated wastewater reuse project in Argelès-sur-Mer, a milestone highlighting the company’s large-scale capabilities in circular water solutions.

Strategic consolidations and technological milestones have also defined the market. In May 2025, Veolia completed the acquisition of full ownership of its Water Technologies and Solutions subsidiary, streamlining its offerings to better serve industrial clients, including textile plants. Meanwhile, Kurita Water Industries achieved a breakthrough in April 2025 by validating microbial fuel cell technology capable of generating electricity directly from wastewater, a major step toward energy-positive wastewater management. Looking back, the October 2024 launch of an MLD wastewater plant in Foshan, China, treating 160,000 m³/day for textile manufacturers, demonstrated how large-scale adoption of water recovery is reshaping the industry. Additionally, in December 2024, researchers published findings on engineered nanoparticles for in-situ wastewater treatment, opening potential pathways for lower-cost and more efficient solutions. In August 2024, H2O America expanded its footprint with a $540 million acquisition of Quadvest, earmarking over $500 million in infrastructure modernization, signaling continued capital flows into wastewater-related utilities.

Key Trends Driving Growth in Textile Wastewater Treatment Equipment Industry

Stricter Regulations and the Push for Zero Liquid Discharge (ZLD)

Government initiatives are shaping the market by making advanced treatment technologies mandatory. In India, ZLD policies compel textile units to upgrade their effluent systems, with states like Gujarat actively promoting modern technologies to ensure global competitiveness. Globally, large-scale implementations such as the Da Tang Industrial Park ZLD plant in Foshan, China, which treats 160,000 cubic meters of wastewater per day using nanofiltration, RO, and electrodialysis, demonstrate a significant shift toward sustainable manufacturing. These regulations drive continuous investment in high-capacity, technologically sophisticated systems that can meet stringent effluent quality standards.

Emergence of Advanced and Hybrid Treatment Technologies

Technological innovation is a critical trend in this market. Advanced membrane filtration techniques, Membrane Bioreactors (MBR), electrochemical treatment, and advanced oxidation processes (AOPs) are increasingly replacing conventional methods to handle complex textile effluent, especially color, salts, and residual COD. Studies from IIT Madras and MDPI’s Membranes journal highlight that hybrid and electrochemical methodologies reduce RO unit requirements, lowering both capital and operational costs by up to 25%. These technologies enable mills to achieve high-efficiency treatment, reduce energy consumption, and maintain compliance in a cost-effective manner.

Corporate Investment in Resource Recovery and Circularity

Textile manufacturers are leveraging wastewater treatment not only for compliance but also as a strategic avenue for resource recovery. Leading players like Aquarelle India exemplify corporate commitment to sustainability through onsite treatment, water recycling, and zero-waste initiatives. Academic research indicates that sophisticated treatment systems can recover water, salts, and other chemicals, creating additional revenue opportunities. This integration of circular economy principles is becoming an essential aspect of ESG strategies, providing a dual benefit of environmental responsibility and financial incentive.

Textile Wastewater Treatment Equipment Market Share Insights

Market Share by Type: Tertiary/Advanced Systems Dominate

Tertiary/Advanced Treatment Equipment (45%) is the largest segment due to the textile industry's need to remove complex pollutants such as dyes, salts, and residual COD. Technologies like ultrafiltration (UF), nanofiltration (NF), reverse osmosis (RO), advanced oxidation processes (AOPs), ozonation, and activated carbon adsorption are central to this segment. Secondary Treatment, including activated sludge, SBR, MBBR, and anaerobic reactors (UASB), remains critical for reducing biodegradable organic load and generating biogas where feasible. Primary Treatment (20%), incorporating screens, grit chambers, equalization tanks, and coagulation-flocculation, serves as an essential first step for removing coarse solids and reducing downstream load. The predominance of advanced systems underscores the market’s shift toward high-performance, regulatory-compliant solutions.

Market Share by Process Integration: Customization Rules the Market

Custom-Engineered Systems (70%) dominate due to the high variability of textile effluent. Each mill requires tailored solutions based on fabric type, dye chemistry, and production processes. Packaged Systems (30%), pre-designed modular units, cater to smaller facilities or specific treatment steps, such as tertiary polishing with ozone or UV. The high share of custom systems reflects the market’s emphasis on effective, plant-specific designs that minimize compliance risk and optimize operational efficiency. Packaged solutions are limited to add-on units or small workshops, emphasizing that engineering expertise is highly valued.

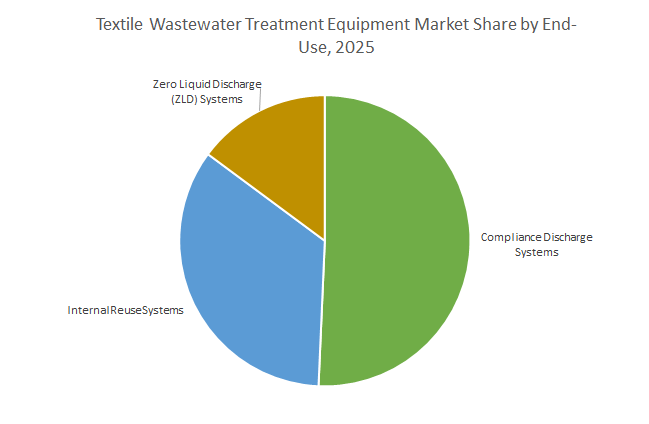

Market Share by End-Use: Reuse and ZLD Gain Strategic Importance

Compliance Discharge Systems (50%) remain the baseline segment, as all mills must meet regulatory requirements for COD, color, and toxicity using a full treatment train. Internal Reuse Systems (35%) are rapidly growing, driven by water scarcity, cost reduction, and sustainability goals; MBR followed by RO is increasingly standard for producing high-quality recycled water. Zero Liquid Discharge (ZLD) Systems (15%) are the most technologically advanced, often mandated in highly polluted textile clusters in India and China. ZLD eliminates environmental discharge, allows salt recovery, and represents the pinnacle of sustainable textile effluent management, albeit with higher capital and operational expenditure.

China: Regulatory Mandates and Cutting-Edge RO Membrane Technologies Drive Market Expansion

China's textile wastewater treatment equipment market is witnessing significant growth due to stringent regulatory enforcement and government-backed investments. The Ministry of Ecology and Environment (MEE) has set rigorous industrial wastewater discharge standards, particularly targeting the textile sector, a major water consumer and polluter. Aligned with the 14th Five-Year Plan, the country aims to achieve 95% wastewater treatment coverage in all county-level cities, emphasizing water reuse. The Chinese government is investing $50 billion by 2025 to upgrade wastewater infrastructure across heavy-polluting industries, including textiles and dyeing. Technological advancements include the development of dual-functional reverse osmosis (RO) membranes with enhanced antibacterial and anti-adhesion properties, improving the efficiency of RO systems in textile wastewater treatment. Biological membrane bioreactors (MBRs) are increasingly adopted in municipal and industrial projects to meet stringent discharge standards while minimizing physical footprint requirements.

India: ZLD Mandates and Academic Innovations Enhance Textile Wastewater Management

India’s textile wastewater treatment equipment market is largely driven by regulatory mandates and technological innovations. The Central Pollution Control Board (CPCB) and State Pollution Control Boards (SPCBs) have mandated Zero Liquid Discharge (ZLD) for textile and dyeing industries in water-scarce regions. Pilot projects developed by institutions such as IIT Madras have demonstrated 96% color removal and 60% COD reduction in dyebath effluent at common effluent treatment plants (CETPs). Additionally, the Department of Science & Technology (DST) supports low-cost, energy-efficient treatment solutions using biosurfactants and membrane technology, converting toxic wastewater into irrigation sources, as implemented at Kakatiya Mega Textile Park, Telangana. Infrastructure initiatives under the "Namami Gange Mission" and "Smart Cities Mission" are accelerating the modernization and deployment of wastewater treatment plants, directly benefiting textile clusters along major rivers.

United States: EPA Regulations and Modular MBR Systems Boost Industry Compliance

The U.S. textile wastewater treatment market is shaped by regulatory oversight, corporate initiatives, and technological innovation. The EPA continues to evaluate opportunities to limit PFAS discharges from textile and other industrial sectors, with the 2026 industrial stormwater multisector general permit (MSGP) introducing PFAS monitoring requirements. Technological advancements include modular MBR systems, such as those launched by Koch Separation Solutions in 2024, which integrate with larger ZLD systems to meet environmental compliance standards. Companies like Veolia Water Technologies and Evoqua Water Technologies have deployed biological treatment capacities to supply water with PFAS levels below regulatory thresholds. The market is increasingly leveraging resource recovery and bioenergy generation, with applications extending to food and beverage sectors, enhancing the overall adoption of advanced treatment equipment in textiles.

Germany: EU Directives and Circular Economy Initiatives Propel Equipment Demand

Germany’s textile wastewater treatment equipment market is influenced by the revised EU Urban Wastewater Treatment Directive, which took effect in January 2025. The directive enforces deeper treatment levels and wider coverage, prompting adoption of advanced oxidation processes and membrane filtration technologies to remove micropollutants. HUBER SE’s "Wastewater Symposium 2025" highlighted water reuse applications for agriculture and urban irrigation, directly relevant to textile effluent management. Startups like Rebirth Studios promote circularity through rebirthOS, upcycling pre-consumer textile waste, which increases demand for specialized wastewater treatment equipment capable of handling complex chemical streams. The presence of over 2,900 chemical businesses further amplifies the need for advanced treatment solutions to comply with stringent regulations in Germany.

Japan: Membrane Bioreactor Innovation Supports Textile Industry Sustainability

Japan’s textile wastewater treatment equipment market is driven by government policies and corporate R&D. The MLIT’s "Advance of Japan Ultimate Membrane bioreactor technology Project (A-JUMP)" promotes MBR-based membrane technologies for medium- to large-scale sewage treatment plants. Japanese corporations and academic institutions, including Toray Industries Inc., are at the forefront of developing advanced membrane technologies, widely applied in textile wastewater treatment. The textile industry focuses on nutrient recovery and water reuse for irrigation, making MBR technologies essential for sustainable operations in Japan’s water-constrained environment.

Brazil: Legal Reforms and Infrastructure Investments Expand Textile Wastewater Solutions

Brazil’s textile wastewater treatment equipment market is propelled by legal reforms and significant infrastructure investment. The new water framework encourages private sector participation, setting targets for 2033 to achieve 99% water coverage and 90% treated sewage coverage, providing regulatory certainty and attracting investment. Projects worth approximately BRL 105 billion across 43 privatization initiatives will include services for industrial customers, such as textile manufacturers. Textile production hubs in São Paulo and Santa Catarina rely heavily on these initiatives to manage wastewater efficiently and mitigate water resource conflicts, driving demand for advanced treatment equipment tailored for textile effluents.

Competitive Landscape: Leading Companies in Textile Wastewater Treatment Equipment

The competitive landscape of the textile wastewater treatment equipment market is defined by global water technology leaders, specialized ZLD solution providers, and innovative chemical treatment companies. These players compete on technology innovation, project scale, sustainability goals, and digital integration capabilities, making this a highly competitive yet opportunity-rich industry.

DuPont Water Solutions

DuPont Water Solutions leverages its expertise in advanced membranes, particularly through its FilmTec™ brand, which is a gold standard in reverse osmosis for textile wastewater treatment. In 2025, DuPont won an R&D 100 Award for its FilmTec™ Fortilife™ XC160 Membrane, specifically engineered to handle high-strength textile effluents for MLD and ZLD systems. Its integrated portfolio spans RO, NF, UF, and ion exchange resins, delivering end-to-end solutions for sustainable water reuse. DuPont’s strategic focus remains on enabling water circularity and cost reduction, currently helping purify more than 50 million gallons of water every minute across 112 countries.

Veolia Water Technologies

Veolia is a pioneer in ecological transformation and large-scale wastewater treatment infrastructure. In July 2025, the company was chosen to deliver France’s largest wastewater reuse project, reaffirming its ability to scale complex projects. Veolia’s portfolio includes biological systems, advanced membranes, thermal evaporators, and crystallizers, all essential for ZLD in textiles. Its GreenUp strategy emphasizes climate-focused innovation and resource recovery, directly aligning with the textile sector’s push toward sustainability and compliance.

Aquatech International LLC

Aquatech is a leader in ZLD and high-recovery solutions for industries like textiles. Its RecovOAR™ technology, which uses osmotically assisted RO, allows for up to 75% reduction in thermal evaporation costs, making ZLD more cost-effective. The company’s offerings include RO, NF, membrane bioreactors, and thermal crystallizers, designed specifically for textile wastewater reuse. Aquatech’s strong application focus ensures textile manufacturers can reduce freshwater dependency and meet stringent discharge norms while maintaining cost efficiency.

SUEZ – Water Technologies & Solutions

SUEZ brings a legacy of expertise in industrial wastewater treatment, delivering tailored solutions for sectors with highly polluted effluents, including textiles. The company recently secured contracts in China for plants designed to achieve 100% wastewater recycling, reinforcing its leadership in ZLD systems. SUEZ combines biological systems, membranes, and predictive analytics to optimize treatment performance, reduce chemical use, and extend asset life. This integration of digital platforms with core water technologies enhances cost efficiency and operational resilience for textile manufacturers.

Kurita Water Industries Ltd.

Kurita stands out for its hybrid approach of chemical and equipment-based water solutions. In June 2024, Kurita expanded in India through its joint venture Kurita AquaChemie India Private Limited, targeting one of the world’s largest textile hubs. Its offerings range from membrane cleaning agents to innovative technologies such as microbial fuel cells that generate electricity from wastewater. Kurita’s sustainability-driven strategy emphasizes reducing discharges to near-zero levels while maximizing water reuse efficiency, making it a trusted partner for environmentally conscious textile producers.

Textile Wastewater Treatment Equipment Market Report Scope

Textile Wastewater Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.5 Billion

|

|

Market Size (2034)

|

$5.5 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Type (Primary Treatment Equipment, Secondary Treatment Equipment, Tertiary/Advanced Treatment Equipment), By Process Integration (Packaged Systems, Custom-Engineered Systems), By End-Use (Compliance Discharge Systems, Internal Reuse Systems, Zero Liquid Discharge Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, Pentair plc, DuPont de Nemours, Inc., Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kuraray Co., Ltd., Nalco Water (An Ecolab Company), Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Textile Wastewater Treatment Equipment Market Segmentation

By Type

- Primary Treatment Equipment

- Secondary Treatment Equipment

- Tertiary/Advanced Treatment Equipment

By Process Integration

- Packaged Systems

- Custom-Engineered Systems

By End-Use

- Compliance Discharge Systems

- Internal Reuse Systems

- Zero Liquid Discharge Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Textile Wastewater Treatment Equipment Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- Pentair plc

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kuraray Co., Ltd.

- Nalco Water (An Ecolab Company)

- Thermax Limited

*- List not Exhaustive

Research Coverage

This report investigates the Textile Wastewater Treatment Equipment Market with deep analysis reviews of demand drivers, regulatory catalysts, and plant-level economics, and it highlights technology breakthroughs in advanced oxidation, electrochemical polishing, and membrane-enabled reuse/ZLD trains. Produced by USDAnalytics, the study benchmarks CAPEX/OPEX across treatment trains, quantifies recovery rates and energy intensity, and maps procurement patterns from packaged modules to fully engineered plants. It also sizes replacement cycles, retrofit opportunities, and digital optimization levers, aligning equipment choice with discharge, reuse, and ZLD outcomes. By combining evidence-led market modeling with case-based performance metrics, this report is an essential resource for textile mills, CETP operators, OEMs/EPCs, and investors seeking compliant, cost-efficient, and circular water strategies through 2034. Scope Includes-

- Segmentation

- By Type: Primary Treatment Equipment; Secondary Treatment Equipment; Tertiary/Advanced Treatment Equipment

- By Process Integration: Packaged Systems; Custom-Engineered Systems

- By End-Use: Compliance Discharge Systems; Internal Reuse Systems; Zero Liquid Discharge Systems

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

- Companies (analysis/profiles of 15+ firms): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; Pentair plc; DuPont de Nemours, Inc.; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kuraray Co., Ltd.; Nalco Water (An Ecolab Company); Thermax Limited.

Methodology

USDAnalytics applies a triangulated approach that fuses bottom-up equipment shipments and installed base audits with top-down spending benchmarks by cluster, fiber type, and finishing process. Primary interviews with mill utilities heads, CETP operators, OEMs/EPCs, and regulators validate real-world removal efficiencies (color/COD/salts), recovery rates, kWh·m⁻³, chemical dose, membrane cleaning intervals, and sludge handling costs. Secondary intelligence spans permits, tender awards, tariff orders, and peer-reviewed trials for MBR, NF/RO, EDR, AOPs, ozonation, and electrochemical units. We convert plant-level data into regional curves for CAPEX, OPEX, and LCC, then run scenarios for ZLD mandates, freshwater pricing, and energy trends to produce defensible 2025–2034 market forecasts and vendor share estimates.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Textile Wastewater Treatment Equipment Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights: Industrial Dominance, Water Reuse, and Regional Leadership

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): $3.5 Billion

1.3.2. Projected Market Valuation (2034): $5.5 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 5.1%

2. Market Outlook (2025–2034)

2.1. Introduction: Market Drivers and Growth Forecast

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends Driving Growth in the Textile Wastewater Treatment Equipment Industry

2.3.1. Stricter Regulations and the Push for Zero Liquid Discharge (ZLD)

2.3.2. Emergence of Advanced and Hybrid Treatment Technologies

2.3.3. Corporate Investment in Resource Recovery and Circularity

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent News and Developments

3.1.1. DuPont Water Solutions Recognized for Industrial Water Reuse Leadership (August 2025)

3.1.2. Veolia and SUEZ Secure Major Contracts for Circular Water Solutions (July 2025)

3.1.3. Strategic Consolidation and Technological Milestones

3.1.4. Large-Scale Project Deployments in Key Regions

3.1.5. Breakthroughs in Energy-Positive Wastewater Management

4. Competitive Landscape: Leading Companies

4.1. Competitive Overview: Global Leaders and Specialized Providers

4.2. Strategic Profiles of Key Companies

4.2.1. DuPont Water Solutions: Pioneering Membrane Technologies for ZLD

4.2.2. Veolia Water Technologies: Global Leader in Large-Scale Water Infrastructure

4.2.3. Aquatech International LLC: Specialist in Industrial ZLD Applications

4.2.4. SUEZ – Water Technologies & Solutions: Focused on Digital Optimization and ZLD

4.2.5. Kurita Water Industries Ltd.: Hybrid Chemical and Equipment Solutions

5. Textile Wastewater Treatment Equipment Market – Segmentation Insights

5.1. By Type

5.1.1. Tertiary/Advanced Treatment Equipment (45% Market Share)

5.1.2. Secondary Treatment Equipment (35% Market Share)

5.1.3. Primary Treatment Equipment (20% Market Share)

5.2. By Process Integration

5.2.1. Custom-Engineered Systems (70% Market Share)

5.2.2. Packaged Systems (30% Market Share)

5.3. By End-Use

5.3.1. Compliance Discharge Systems (50% Market Share)

5.3.2. Internal Reuse Systems (35% Market Share)

5.3.3. Zero Liquid Discharge (ZLD) Systems (15% Market Share)

6. Country Analysis: Textile Wastewater Treatment Equipment Market

6.1. China: Regulatory Mandates and Cutting-Edge RO Membrane Technologies

6.2. India: ZLD Mandates and Academic Innovations

6.3. United States: EPA Regulations and Modular MBR Systems

6.4. Germany: EU Directives and Circular Economy Initiatives

6.5. Japan: Membrane Bioreactor Innovation Supports Sustainability

6.6. Brazil: Legal Reforms and Infrastructure Investments Expand Market

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Market Outlook

7.1.1. By Type

7.1.2. By Process Integration

7.1.3. By End-Use

7.2. Europe Market Outlook

7.2.1. By Type

7.2.2. By Process Integration

7.2.3. By End-Use

7.3. Asia Pacific Market Outlook

7.3.1. By Type

7.3.2. By Process Integration

7.3.3. By End-Use

7.4. South America Market Outlook

7.4.1. By Type

7.4.2. By Process Integration

7.4.3. By End-Use

7.5. Middle East & Africa Market Outlook

7.5.1. By Type

7.5.2. By Process Integration

7.5.3. By End-Use

8. Company Profiles: Leading Players

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. Pentair plc

8.6. DuPont de Nemours, Inc.

8.7. Toray Industries, Inc.

8.8. Aquatech International

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. V.A. TECH WABAG Ltd.

8.12. Mitsubishi Chemical Corporation

8.13. Kuraray Co., Ltd.

8.14. Nalco Water (An Ecolab Company)

8.15. Thermax Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures