Flue Gas Desulfurization Market Outlook 2025–2034: Growth Trajectory, Regulatory Push, and Strategic Imperatives

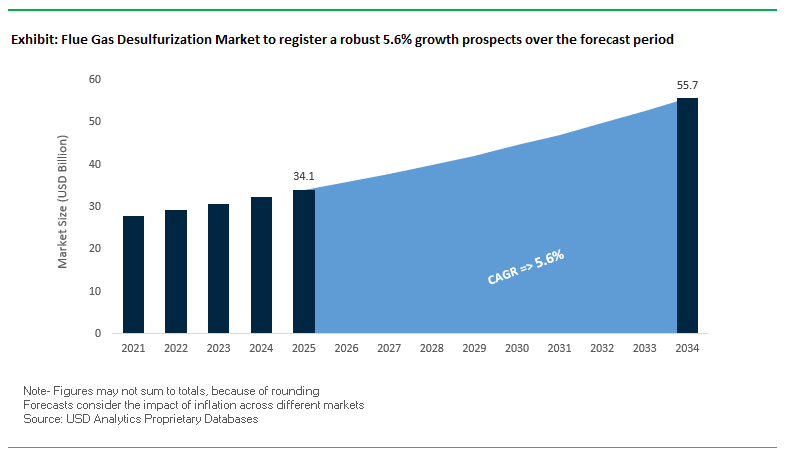

The Flue Gas Desulfurization (FGD) market is projected to reach USD 34.1 billion in 2025 and expand to USD 55.7 billion by 2034, reflecting a CAGR of 5.6% over the forecast period. The sustained growth is anchored in the global tightening of emission control regulations, particularly targeting sulfur dioxide (SO₂) emissions from coal-fired power plants and heavy industries.

Industry-leading Wet Flue Gas Desulfurization (WFGD) technology will remain predominant in high-capacity coal-fired power plants due to long-term capability to achieve above 95% SO₂ removal efficiency. It will remain the largest end-user market because coal-fired power plants continue to produce the largest portion of global SO₂ emissions. In addition, there is a strong trend toward utilization of byproduct gypsum, conversion of calcium sulfite to high-grade synthetic gypsum for use in wallboard and building materials constitutes a possible secondary source of incomes to plant personnel.

Regulatory environment is a key growth factor, and the stringent regulations in places like India, China, and Europe hasten installation. India's changing emission requirements for coal-based power stations, for example, have triggered large-scale use of FGD, but recent exemptions (July 2025) have changed the near-term installation scenario.

Strategic Imperatives for Industry Stakeholders:

- Prioritize dual-technology portfolios (wet, dry, and hybrid) to address varying regional regulatory demands.

- Leverage gypsum byproduct commercialization to improve ROI on FGD investments.

- Focus on retrofit market opportunities in Asia and Europe, where existing plants face strict compliance deadlines.

- Invest in technology upgrades to achieve >99% SO₂ removal with lower operational costs.

- Build strategic partnerships with EPC contractors for competitive advantage in large-scale project bidding.

Global Flue Gas Desulfurization Market Analysis: Regulatory Shifts, Major Contracts, and Regional Momentum

The global FGD industry is navigating a dual-force environment where stringent environmental compliance requirements continue to fuel demand, but policy relaxations in certain regions create localized slowdowns. For example, in July 2025, India’s Environment Ministry exempted nearly 78% of the nation’s coal-fired thermal plants from installing FGD systems, marking a sharp departure from earlier mandates. However, before the shift, the Ministry of Power confirmed in August 2025 that 57 thermal units had already installed FGDs, reflecting tangible progress under the earlier regulatory regime.

China remains the single largest FGD market due to the massive installed base of coal-fired plants, with R&D efforts aimed at efficiency improvements and byproduct valorization into fertilizers. In developed markets, compliance upgrades are still active as GE Vernova recently completed a major European FGD installation, ensuring the facility met strict EU SO₂ emission standards. These developments underscore that, while regional policy changes affect the pace of deployment, the global trajectory remains firmly growth-oriented, driven by both environmental policy and long-term decarbonization strategies.

Trends and Opportunities in Flue Gas Desulfurization Market

Trend 1: Transition to Dry Sorbent Injection (DSI) for Flexible Compliance

Flue gas desulfurization (FGD) market is experiencing a significant trend shift toward Dry Sorbent Injection (DSI) systems as a flexible, economical alternative to conventional wet limestone or seawater FGD technology. Power plants and industrially driven facilities increasingly adopt DSI systems due to their compact nature, fast installation, and effectiveness in retrofitting existing units. Research emphasizes that DSI systems, such as sodium bicarbonate-based systems employing a sorbent, can reach SO2 capture efficiencies of at least 50% in mid-capacity units and hence apply ideally to plants having broader emission targets. Alongside sulfur dioxide, other acid gases such as HCl and SO3 alongside heavy metals such as mercury can be targeted in DSI technology allowing multi-pollutant control within a singular flexible solution. Deployment at rates faster than 12–14 months versus conventional wet system deployments running past two years facilitate fast compliance due to changing environmental regulations and henceforth a growing trend within industrial emission control.

Trend 2: Waste-to-Byproduct Conversion in Wet FGD Systems

The FGD sector is becoming progressively receptive to the concepts of a circular economy by turning waste streams into beneficial byproducts. Wet limestone FGD systems, in fact, are designed to maximize the production of high-purity synthetic gypsum that can be utilized in wallboarding and other structural applications, creating a financially appealing alternative to landfill disposal. Furthermore, some FGD byproducts, which contain valuable sulfur and alkaline materials, can be utilized in agriculture and boost crop yields and soil quality. Advanced resource recovery methods are further appearing on the scene like oxalic acid-based separation to recover elemental sulfur at a level up to 97%, while recycling still-liquid streams back into industrial acids. Resource recovery efforts aim not only to offset operating costs but integrate FGD systems into sustainable industrial practice and ESG-compatible strategies.

Opportunity 1: Emerging Market Coal Plant Retrofits

Rapidly growing Asian and African economies are creating a major opportunity for suppliers of FGD equipment on a large number of coal-fired power plant retrofits. India, a high-emitting SO2 country, has begun a large program to install FGD on 537 coal-based thermal units, with several hundred units contracted or tendered. Staggered compliance dates between December 2024 and December 2026 provide powerful motivations to use FGD and meet environmental regulation rather than pay penalties. Retrofits have achieved impressive emission reductions with state, central, and privately owned plants cutting SO2 emission levels by 65%, 69%, and 60%, respectively. Such retrofits create large demand levels for modular, scalable FGD technology solutions that this growth is boosting demand in the global emission control technology market.

Opportunity 2: Hydrogen-Ready FGD for Ammonia and Chemical Plants

As part of global efforts toward decarbonization, hydrogen and ammonia production plants increasingly need FGD systems to achieve low-carbon status. Ammonia-based FGD technology is highly effective in removing SO2 while generating high-value byproducts such as ammonium sulfate that can recover above 50% operating costs. These systems provide high removal efficiencies above 99%, which remain vital to safeguarding downstream catalysts and stringent environmental regulations in chemical production and low-carbon hydrogen production. Addition of FGD in hydrogen and ammonia plants serves both compliance with low-carbon standards and a secondary revenues stream from byproducts, making it a sound investment toward sustainable operation in the industry.

Flue Gas Desulfurization Market Share Insights

Market Share by Technology Type: Wet FGD Systems as the Industry Workhorse

Wet flue gas desulfurization systems are projected to command nearly 65% of the global FGD market share by 2025, establishing themselves as the dominant technology. Their ability to achieve over 95% SO₂ removal efficiency makes them the preferred choice for large coal-fired power plants and energy-intensive industrial facilities. The segment’s growth is closely tied to strict environmental regulations such as the EPA’s Mercury and Air Toxics Standards (MATS) in the U.S. and the EU Industrial Emissions Directive, which mandate deep sulfur reduction. In contrast, dry and semi-dry systems remain relevant in smaller plants, regions with limited water availability, and retrofit applications due to their lower capital intensity and dry waste output. Emerging technologies, although only 5% of the market, are garnering attention for their potential to recover saleable byproducts and minimize water use, indicating a gradual shift toward sustainability-driven adoption.

Market By Technology Type (2025).png)

Market Share by Absorbent Type: Alkaline-Based Sorbents Leading with Cost Efficiency

Alkaline-based sorbents, primarily limestone and lime, account for nearly 80% of the global FGD market share, cementing their role as the industry standard. Limestone remains dominant due to its abundance, low cost, and compatibility with wet scrubbing processes, while lime is widely used in both wet and dry systems for flexibility and efficiency. The segment benefits from reliable global supply chains and predictable operating costs, which are critical for large-scale, long-term utility operations. Alternative sorbents, representing about 20% of the market, provide niche advantages in specific contexts such as ammonia-based systems that generate marketable fertilizers or sodium-based solutions that deliver very high removal rates. However, their adoption is largely situational, depending on local raw material availability and waste-handling economics, ensuring limestone’s continued supremacy in mainstream applications.

Market Share by System Capacity: Large Utility-Scale Plants Driving High-Value Contracts

The >500 MW system capacity segment represents around 50% of the global FGD market in 2025, making it the most valuable and impactful category. These large-scale systems are tailored for utility-grade coal-fired power plants, where custom engineering, complex integration, and massive capital investment define project scope. Mid-range systems (100–500 MW), with 34.3% share, are widely deployed in industrial sectors like steel and cement, representing a balanced market of new installations and retrofits. Smaller systems (<100 MW), about 15% of the total, serve waste-to-energy plants and compact industrial boilers, often with dry FGD technology. The distribution illustrates how the market is heavily weighted toward large, utility-driven projects, with smaller systems forming a secondary but essential layer that supports compliance in decentralized industries.

Market Share by Installation Configuration: Brownfield Retrofits as the Compliance Backbone

Brownfield retrofits are projected to capture around 55% of the global FGD market share in 2025, underscoring their role as the primary compliance driver in developed regions. Power and industrial plants across North America and Europe are under constant pressure to upgrade existing assets with desulfurization systems to meet tightening emissions standards. Greenfield installations are most prominent in Asia-Pacific, where new coal-fired capacity continues to be added to meet energy demand, particularly in China, India, and Southeast Asia. Meanwhile, modular and pre-fabricated units are gaining visibility as fast-track solutions for smaller industrial facilities and for operators seeking predictable installation costs. The breakdown highlights how the global FGD market reflects both retrofit-led environmental compliance in mature markets and growth-driven adoption in emerging economies.

Market Share by End-User Industry: Energy & Utilities Dominating with Coal Dependence

The energy and utilities sector is forecast to hold approximately 70% of the FGD market share by 2025, firmly positioning coal-fired power generation as the central demand source. The scale of sulfur emissions from the sector makes it the largest contributor to global desulfurization technology adoption, with policies like China’s ultra-low emission mandates reinforcing its dominance. Cement manufacturing follows as a major industrial emitter, where FGD systems are increasingly deployed to manage kiln-related emissions. The iron and steel industry also contributes significantly, particularly through sinter plants and coke ovens that require customized solutions. Chemicals and petrochemicals and waste incineration plus other industries account for the remaining share, reflecting the widening application of FGD technologies beyond power into diversified heavy industries.

Country Analysis of the Flue Gas Desulfurization Market

United States: Modular and Multi-Pollutant FGD Systems Drive Market Growth

The United States flue gas desulfurization market is largely driven by the Bipartisan Infrastructure Law and stringent enforcement by the EPA using the Clean Air Act. Power plant and boiler modernization is generating keen demand for advanced FGD systems that can achieve 99% SO2 removal efficiency. Products such as LDX Solutions' Dustex® circulating dry scrubbers (CDS) lead the charge in minimizing water and reagent consumption while targeting multiple pollutants such as SO3, HCl, and heavy metals. Modular and compact units for FGD continue a growth trend that serves to simplify installation and decrease operational complexity in smaller applications within industry. Retrofit work throughout existing facilities further escalates demand, a reflection of a need for compliance-motivated, energy-efficient desulfurization technology.

China: Coal-Dependent Energy Consumption Drives Wet and Semi-Dry FGD Technologies

China continues to be a key market for flue gas desulfurization technology due to coal-based energy consumption and vigorous governmental efforts toward environmental protection. Wet limestone-gypsum FGD systems are widely utilized in the country due to high SO2 removal efficiency. Concurrently, studies on new semi-dry desulfurization technology, such as powder-particle spouted bed system technology, aim to obtain high removal efficiency while generating minimal wastewater. Mega-projects, such as the Shandong Power Plant FGD Project, indicate governmental efforts toward cutting emissions and ensuring better industrial compliance. Such efforts make China a model follower in Asian countries of new desulfurization and denitration technology.

India: Policy-Driven Adoption Focused on Critical Pollution Zones

In India, the FGD market is driven by recent policy updates issued by India's Ministry of Environment, Forest and Climate Change requiring flue gas desulfurization systems mostly in critically polluted cities and around large cities. Approximately 78% of thermal power station units remain exempted from mandatory installation due to low levels of sulfur in Indian coal and overall tolerable ambient SO2 levels. For remaining plants covered under the mandate, compliance dates reach December 2027 and 2028, finding a balance between environmental targets and economical viability. India's Central Pollution Control Board continues to maintain air quality monitoring to ensure continued demand for highly efficient FGD solutions in remaining high-precedence installations.

South Korea: Retrofitting and Advanced Emission Monitoring Expand Market Opportunities

South Korea's flue gas desulfurization market is bolstered by governmental master plans to decrease fine dust concentration by more than 35% by 2030. Retrofitting existing coal-fired power stations with FGD systems is a key activity within the updated Clean Air Conservation Act. Opportunities exist within this market for dry sorbent injections technology and ongoing emissions monitoring systems, with regulatory compliance extending to 11 key air pollutants and 32 hazardous chemicals. Switching coal plants to natural gas-fired power stations has a further impetus to use energy-efficient and low-maintenance desulfurization technology, making sustainability and regulatory compliance a priority.

Japan: Pioneering Semi-Dry and Lime-Gypsum Recovery FGD Technologies

Japan has long been a pioneer in flue gas desulfurization systems, integrating technologies such as lime-gypsum recovery processes and seawater desulfurization to handle diverse exhaust gases. Companies like Tsukishima Kikai Co., Ltd. focus on innovations that reduce operational costs while enhancing pollutant removal efficiency. Academic research, including semi-dry FGD development at Gunma University using powder-particle spouted beds, highlights Japan’s leadership in high-efficiency, low-waste desulfurization methods. Rising demand for Japanese FGD technologies overseas reflects their strong reputation in industrial emissions control and sustainable air pollution solutions.

Saudi Arabia: Aramco-Led Projects Emphasize Zero-Discharge and Energy Efficiency

Saudi Arabia’s FGD market is heavily influenced by Aramco, with projects such as the Fadhili Gas Plant achieving sulfur recovery rates above 99.9%. The country has embraced advanced zero-discharge FGD technologies, demonstrated by earlier deployments like the Ducon seawater system at the Jeddah power plant. Energy efficiency and CO2 reduction are key focuses, with turbocharger integration and renewable energy considerations supporting broader environmental goals. Under Vision 2030, the shift from oil to cleaner natural gas for power generation further drives adoption of state-of-the-art FGD systems, highlighting Saudi Arabia’s commitment to sustainable emissions management.

Competitive Landscape: Global Leaders Driving Technological and Regulatory Compliance

The flue gas desulfurization market is characterized by a mix of established multinational technology providers and regionally strong players. The leaders in the space differentiate themselves through technology breadth, retrofit expertise, and global service networks, enabling them to serve both mature and emerging markets under diverse environmental mandates.

Mitsubishi Heavy Industries (MHI) – Setting the Benchmark for Ultra-High SO₂ Removal

MHI is the global leader in wet technology for FGD, and its CT-121 process can reach a desulfurization efficiency level of up to 99.5%. Advanced gas-gas heaters are integrated into the product for better energy efficiency, and MHI provides complete turnkey services ranging from engineering to maintenance. Supported by a history of successful global installation spanning decades, MHI's strategy still lies in ongoing innovation to drive down operating costs while satisfying the highest level of environmental controls.

Babcock & Wilcox Enterprises (B&W) – Comprehensive Solutions for Every Plant Type

B&W has one of the most comprehensive FGD product portfolios available in the market, ranging from WFGD, circulating dry scrubbers (CDS) to dry sorbent injection (DSI) systems. With this range, it can serve mixed plant capacity and SO₂ removal applications. Recognized as a leader in boiler and environmental technology heritage, B&W accompanies installation with a strong aftermarket business supplies parts, maintenance, and upgrade services to achieve long-term operational excellence.

GE Vernova – Leveraging Power Sector Expertise for Integrated Compliance

GE Vernova combines wet, semi-dry and dry FGD technology and long power generation heritage to offer integrated air quality control solutions. Its recent India wins, including large deals within India's state-owned utility NTPC, reflect ability to perform large-capacity work within high-growth markets. Its global presence, engineering capability and strong brand equity make GE Vernova a utility-scale emission control project preferred partner.

Thermax Limited – Custom-Built Solutions for Emerging Market Needs

Thermax is a leading force in India's FGD market with WFGD, spray dryer absorber (SDA), and DSI systems designed especially for domestic conditions and pollution control regulations. Thermax provides turnkey solutions from engineering to commissioning with strong engineering and manufacturing capabilities. Its intimate knowledge of India's industrial scene coupled with continued order wins solidifies Thermax's position as a preferred vendor of affordable yet high-capacity-FGD installation.

Flue Gas Desulfurization Market Report Scope

Flue Gas Desulfurization Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$34.1 Billion

|

|

Market Size (2034)

|

$55.7 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Technology Type (Wet FGD Systems, Dry & Semi-Dry FGD Systems, Emerging Technologies), By Absorbent Type (Alkaline-Based, Alternative Sorbents), By System Capacity (<100 MW, 100–500 MW, >500 MW), By Installation Configuration (Greenfield Installations, Brownfield Retrofits, Modular/Pre-fabricated Units), By End-User Industry (Energy & Utilities, Iron and Steel, Cement, Chemicals & Petrochemicals, Waste Management, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mitsubishi Heavy Industries, General Electric Company, Babcock & Wilcox Enterprises, Inc., Andritz AG, Doosan Lentjes GmbH, Thermax Limited, FLSmidth & Co. A/S, Hamon Group, Chiyoda Corporation, Kawasaki Heavy Industries, John Wood Group, Siemens AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flue Gas Desulfurization Market Segmentation

By Technology Type

- Wet FGD Systems

- Limestone-Based Wet Scrubbing

- Seawater FGD

- Ammonia-Based FGD

- Dry & Semi-Dry FGD Systems

- Spray Dry Absorbers (SDA)

- Circulating Dry Scrubbers (CDS)

- Dry Sorbent Injection (DSI)

- Emerging Technologies

- Membrane-Based FGD

- Electrochemical FGD

- Bio-FGD (Microbial treatment)

By Absorbent Type

- Alkaline-Based

- Alternative Sorbents

By System Capacity

- <100 MW

- 100–500 MW

- >500 MW

By Installation Configuration

- Greenfield Installations

- Brownfield Retrofits

- Modular/Pre-fabricated Units

By End-User Industry

- Energy & Utilities

- Iron and Steel

- Cement

- Chemicals & Petrochemicals

- Waste Management

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Flue Gas Desulfurization Market

- Mitsubishi Heavy Industries

- General Electric Company

- Babcock & Wilcox Enterprises, Inc.

- Andritz AG

- Doosan Lentjes GmbH

- Thermax Limited

- FLSmidth & Co. A/S

- Hamon Group

- Chiyoda Corporation

- Kawasaki Heavy Industries

- John Wood Group

- Siemens AG

* List Not Exhaustive

Research Coverage

This report investigates the Global Flue Gas Desulfurization (FGD) Market, presenting analysis reviews of regulatory enforcement, large-scale retrofit demand, and technological breakthroughs transforming industrial air quality control. Published by USDAnalytics, it highlights how tightening sulfur dioxide (SO₂) emission standards in China, India, Europe, and the U.S. are accelerating adoption of wet, dry, and hybrid FGD technologies. The study further explores gypsum byproduct commercialization, waste-to-value conversion, and next-generation hydrogen-ready systems, alongside industry contracts, EPC collaborations, and regional policy shifts. By evaluating market drivers, country-level policies, technology share, and competitive positioning, this report is an essential resource for utility operators, regulators, EPC contractors, and investors seeking clarity on compliance trends and long-term opportunities in the FGD industry.

Scope Includes:

- Segmentation: By Technology (Wet FGD, Dry FGD, Semi-Dry FGD, Dry Sorbent Injection), By Absorbent (Limestone, Lime, Ammonia, Sodium-Based, Others), By System Capacity (<100 MW, 100–500 MW, >500 MW), By Installation (Brownfield Retrofit, Greenfield, Modular/Prefabricated), and By End-User (Energy & Utilities, Cement, Iron & Steel, Chemicals & Petrochemicals, Waste-to-Energy, Others).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic & Forecast: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Profiles and competitive analysis of 15+ leading companies in the global FGD market.

Methodology

The research methodology employed by USDAnalytics integrates both primary and secondary research to deliver a comprehensive view of the FGD market. Primary research included direct interviews with power utilities, industrial operators, technology providers, and regulatory agencies to validate adoption patterns, compliance strategies, and regional dynamics. Secondary research incorporated industry reports, government regulations, company disclosures, technical journals, and global emissions data. Market sizing was derived using both top-down and bottom-up approaches, further refined with triangulation to ensure accuracy across regions, segments, and capacities. Scenario modeling for regulatory enforcement timelines, retrofit cycles, and technology substitution trends was also applied, ensuring that the findings present a reliable and forward-looking perspective for industry stakeholders.

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Flue Gas Desulfurization Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Stakeholders

1.3. Global Market Snapshot

2. Flue Gas Desulfurization Market Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $34.1 Billion

2.2.2. Forecasted Market Size (2034): $55.7 Billion at 5.6% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Global Tightening of Emission Regulations

2.3.2. Dominance of Wet FGD Technology

2.3.3. Gypsum Byproduct Utilization

3. Global FGD Market Analysis: Regulatory Shifts, Major Contracts, and Regional Momentum

3.1. Overview of the Dual-Force Environment

3.2. Regulatory Policy Changes

3.2.1. India's July 2025 Exemptions

3.2.2. China's Continued Regulatory Momentum

3.3. Major Contracts and Project Developments

3.3.1. GE Vernova's European Installation

3.3.2. India's FGD Installation Progress

4. Trends and Opportunities in Flue Gas Desulfurization Market

4.1. Trend 1: Transition to Dry Sorbent Injection (DSI)

4.1.1. Flexible and Economical Alternative

4.1.2. Multi-Pollutant Control and Fast Installation

4.2. Trend 2: Waste-to-Byproduct Conversion

4.2.1. Synthetic Gypsum Production and Agricultural Use

4.2.2. Elemental Sulfur and Acid Recovery

4.3. Opportunity 1: Emerging Market Coal Plant Retrofits

4.3.1. Large-Scale Retrofit Programs in India and Asia

4.3.2. Staggered Compliance Dates Driving Demand

4.4. Opportunity 2: Hydrogen-Ready FGD for Ammonia and Chemical Plants

4.4.1. High-Efficiency Systems for Low-Carbon Production

4.4.2. Byproduct Recovery for Revenue Streams

5. Flue Gas Desulfurization Market Share Insights

5.1. By Technology Type

5.1.1. Wet FGD Systems

5.1.2. Dry & Semi-Dry Systems

5.1.3. Emerging Technologies

5.2. By Absorbent Type

5.2.1. Alkaline-Based Sorbents

5.2.2. Alternative Sorbents

5.3. By System Capacity

5.3.1. Large Utility-Scale Plants (>500 MW)

5.3.2. Mid-Range Systems (100–500 MW)

5.3.3. Smaller Systems (<100 MW)

5.4. By Installation Configuration

5.4.1. Brownfield Retrofits

5.4.2. Greenfield Installations

5.4.3. Modular/Pre-fabricated Units

5.5. By End-User Industry

5.5.1. Energy & Utilities Sector

5.5.2. Cement Manufacturing

5.5.3. Iron and Steel Industry

5.5.4. Other Industrial Sectors

6. Country Analysis of the Flue Gas Desulfurization Market

6.1. United States: Regulations and Multi-Pollutant Systems

6.2. China: Wet and Semi-Dry FGD Technologies

6.3. India: Policy-Driven Adoption and Critical Pollution Zones

6.4. South Korea: Retrofitting and Advanced Monitoring

6.5. Japan: Semi-Dry and Lime-Gypsum Recovery Innovations

6.6. Saudi Arabia: Zero-Discharge and Energy Efficiency Projects

6.7. Other Country Analysis

7. Flue Gas Desulfurization Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Technology, Absorbent, Capacity, Installation, and End-User

7.2. Europe Market Size Outlook to 2034

7.2.1. By Technology, Absorbent, Capacity, Installation, and End-User

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Technology, Absorbent, Capacity, Installation, and End-User

7.4. South America Market Size Outlook to 2034

7.4.1. By Technology, Absorbent, Capacity, Installation, and End-User

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Technology, Absorbent, Capacity, Installation, and End-User

8. Company Profiles: Top Companies in Flue Gas Desulfurization Market

8.1. Mitsubishi Heavy Industries (MHI)

8.2. Babcock & Wilcox Enterprises (B&W)

8.3. GE Vernova

8.4. Thermax Limited

8.5. Andritz AG

8.6. Doosan Lentjes GmbH

8.7. FLSmidth & Co. A/S

8.8. Hamon Group

8.9. Chiyoda Corporation

8.10. Kawasaki Heavy Industries

8.11. John Wood Group

8.12. Siemens AG

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations