Market Overview: Expanding Role of Polymeric Membranes in Global Filtration

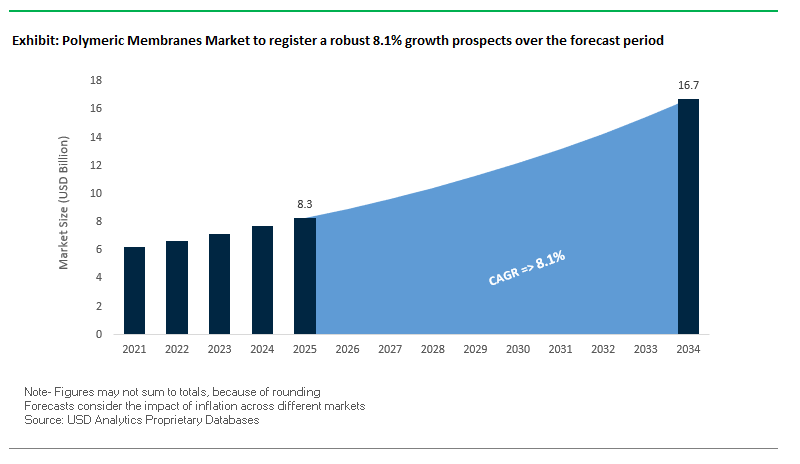

The global polymeric membranes market is projected to reach USD 16.7 billion by 2034 from USD 8.3 billion in 2025, advancing at a strong CAGR of 8.1%. Polymeric membranes have become indispensable in modern separation and purification processes, owing to their cost-effectiveness, chemical resistance, and adaptability across multiple applications. From municipal water treatment to industrial wastewater reuse and biopharmaceutical processing, these membranes are positioned as a sustainable, scalable, and performance-driven solution. For industry Stakeholders, critical considerations revolve around which polymeric materials dominate market share, how these membranes are evolving to address biofouling, and what role regulatory frameworks are playing in adoption. The answers reveal a market that is accelerating due to sustainability pressures, innovation in material science, and integration into both traditional and emerging industries.

Key Insights Driving Market Dynamics

- PVDF and PES membranes dominate due to durability, cost-efficiency, and compatibility with advanced filtration methods like ultrafiltration (UF) and reverse osmosis (RO).

- Municipal and industrial treatment facilities are rapidly shifting toward polymeric ultrafiltration to enhance pathogen removal and meet drinking water quality standards.

- Single-use polymeric membranes are gaining traction in life sciences and pharmaceuticals, driven by high-purity requirements and regulatory compliance.

- Tightening global environmental regulations are accelerating adoption of polymeric membranes in industrial water reuse and zero liquid discharge (ZLD) projects.

- RO and FO technologies based on polymeric membranes continue to lead desalination and high-purity water markets, underpinning large-scale global projects.

Market Analysis: Recent Developments Shaping Growth Trajectories

The polymeric membranes market is entering a new phase of innovation where sustainability, efficiency, and application diversity are defining competitive advantages. DuPont’s recognition in August 2025 with the BIG Sustainability Award for its FilmTec™ Fortilife™ membranes illustrates how industrial wastewater reuse has become a central pillar of global water management strategies. This recognition highlights the shift in customer expectations toward membranes that not only perform reliably but also contribute to circular water systems and lower energy footprints.

In July and June 2025, SUEZ expanded its innovation footprint by collaborating with Seabex to integrate advanced filtration with agricultural practices and by inaugurating Europe’s largest biogas facility at Seine Aval in Paris. Both projects underscore the trend of linking polymeric membrane technology to broader sustainability goals, including energy independence, agriculture, and waste-to-value transitions. Such developments indicate that membranes are no longer confined to water treatment but are enablers of decarbonization strategies and cross-sector integration.

Product innovation remains a defining trend, exemplified by Toray’s March 2025 launch of a new RO membrane designed with double chemical resistance and extended service life. By reducing replacement frequency and CO₂ emissions, the company reinforced its leadership in sustainable desalination technologies. Meanwhile, Koch Separation Solutions’ February 2025 $20 million investment in Mexico to expand spiral membrane capacity reflects the rising global demand for robust, large-scale solutions in food, beverage, and industrial water reuse.

The scope of polymeric membranes continues to widen with companies like Nitto Denko Corporation showcasing carbon-negative solutions at COP29 in November 2024, where membranes were applied for CO₂ separation from industrial exhaust streams. Coupled with European government funding in July 2024 for next-generation anti-fouling membrane coatings, the industry is signaling a shift toward high-performance products with reduced maintenance requirements. Earlier in March 2024, DuPont’s launch of a seawater RO membrane designed to cut energy use in desalination added momentum to the global push for efficiency. Collectively, these innovations demonstrate how polymeric membranes are evolving from traditional water purification into climate-focused technologies, underpinning their importance in future environmental and industrial strategies.

Key Trends and Emerging Opportunities Driving the Polymeric Membranes Market

Breakthroughs in Anti-Fouling and High-Performance Polymeric Membranes

A defining trend in the polymeric membranes market is the shift toward advanced anti-fouling materials and nanocomposite designs that enhance durability, chlorine resistance, and operational stability. Research published in ACS Applied Materials & Interfaces shows that embedding nanomaterials like graphene oxide into polyamide membranes significantly improves hydrophilicity, reducing bacterial and organic fouling. These innovations are extending the life of reverse osmosis membranes and lowering operating costs for water and wastewater treatment plants, making next-generation anti-fouling membranes a cornerstone of future adoption.

Strategic Corporate Investments and Academic-Industry Collaborations

Another major trend is the rise of R&D investments and cross-sector collaborations, which are accelerating commercialization of high-performance polymeric membranes. DuPont’s launch of its new surface-modified, anti-fouling polymeric membranes exemplifies this shift, targeting industrial water treatment operators who face high maintenance burdens. Parallel to this, academic collaborations are pioneering low-cost phase inversion manufacturing techniques, creating opportunities to scale advanced membranes at reduced production costs. These partnerships highlight how corporate innovation and academic research are converging to push membrane performance and affordability forward.

Expansion of Polymeric Membranes into Gas Separation, Biopharma, and Energy

The market is no longer confined to water treatment polymeric membranes are expanding into high-value applications such as carbon capture, gas separation, and biopharmaceutical processing. In the energy sector, highly selective polymeric membranes are being developed to separate CO₂ from flue gases, offering an energy-efficient alternative to chemical scrubbing methods. In pharmaceuticals, single-use sterile filtration membranes are becoming standard due to their role in ensuring contamination-free drug manufacturing. This shift underscores how new end-use industries are transforming polymeric membranes into multi-sector enablers of sustainability and precision processing.

Government Regulations and Infrastructure Investments Accelerating Adoption

Stringent water quality regulations and government-backed infrastructure spending are fueling large-scale adoption of polymeric membranes. For example, the U.S. Bipartisan Infrastructure Law (BIL) allocates billions toward upgrading municipal and industrial water treatment systems, many of which rely heavily on polymeric membrane technology. These policy-driven investments create stable demand pipelines for advanced membranes, particularly in microfiltration, ultrafiltration, and reverse osmosis applications. Regulations addressing industrial wastewater discharge and water reuse further cement polymeric membranes as the most cost-effective and scalable technology to meet environmental compliance standards.

Opportunities in Carbon Capture, Hydrogen Recovery, and Pharmaceutical Sterile Filtration

Looking ahead, some of the most promising opportunities lie in specialized, high-value applications. Carbon capture is emerging as a multi-billion-dollar field where polymeric gas separation membranes offer a sustainable, energy-efficient solution. Similarly, hydrogen recovery membranes are being positioned as critical to the global clean energy transition. In pharmaceuticals, the rapid adoption of single-use sterile filtration membranes opens new revenue streams for companies capable of supplying contamination-free, regulatory-compliant solutions. Coupled with large-scale government investments in water reuse and desalination, these opportunities position polymeric membranes at the center of both environmental sustainability and industrial efficiency.

Polymeric Membranes Market Share Insights

Market Share by Type: Reverse Osmosis Leads in Value, UF/MF Dominate in Volume

The polymeric membranes market exhibits strong segmentation by type, with reverse osmosis (RO) membranes commanding 30% of revenue share in 2025. RO membranes remain indispensable in desalination and high-purity water production, where reliability and multi-layer complexity justify their premium pricing. In contrast, ultrafiltration (UF) and microfiltration (MF) membranes collectively dominate in terms of installed volume, serving as critical pre-treatment stages in municipal and industrial systems. Nanofiltration (NF) membranes represent a fast-growing segment, offering sustainable alternatives for water softening and selective separations. Meanwhile, gas separation membranes and niche types like forward osmosis and pervaporation are carving out high-value opportunities in hydrogen recovery, carbon capture, and solvent separation, positioning themselves as growth engines for the coming decade.

Market Share by Configuration: Spiral Wound and Hollow Fiber Dominate Industrial Use

When analyzed by configuration, the market is overwhelmingly led by spiral wound membranes, with a 60% market share in 2025, due to their unmatched packing density and efficiency in RO, NF, and gas separation applications. Hollow fiber membranes hold 30% of the market, primarily serving UF and MF systems where high surface area and scalability are critical. Though smaller in share, flat sheet/plate-and-frame membranes remain important in food, dairy, and pulp applications where fouling is a major challenge and cleanability outweighs density efficiency. Tubular membranes, at just 2%, cater to highly viscous or solids-laden feeds, particularly in sludge and wastewater processing, highlighting a robustness-over-efficiency tradeoff. This configuration split underlines how application dictates design, with each type optimized for balancing efficiency, durability, and fouling resistance.

Market Share by Application: Water and Wastewater Anchors, Desalination and Industrial Uses Drive Growth

By application, water and wastewater treatment holds the largest share at 55%, underscoring its role as the anchor of the polymeric membranes market. Municipal water reuse and wastewater recycling initiatives are major demand drivers, especially in regions facing water stress. Desalination accounts for 15% of the market, playing a strategic role in arid regions and commanding premium RO membranes tailored for seawater treatment. Meanwhile, industrial processing including food & beverage, pharmaceuticals, and chemicals accounts for 20%, reflecting the shift toward high-value separation and purification processes that demand specialized and compliant membranes. Gas separation membranes, with 7% share, are emerging as critical technologies in the energy transition, enabling biogas upgrading, hydrogen recovery, and CO2 capture. Other applications, though smaller at 3%, include medical and laboratory uses, where polymeric membranes are indispensable for precision and sterility. This segmentation highlights how traditional water applications anchor the market while industrial and energy-transition sectors provide the most promising growth avenues.

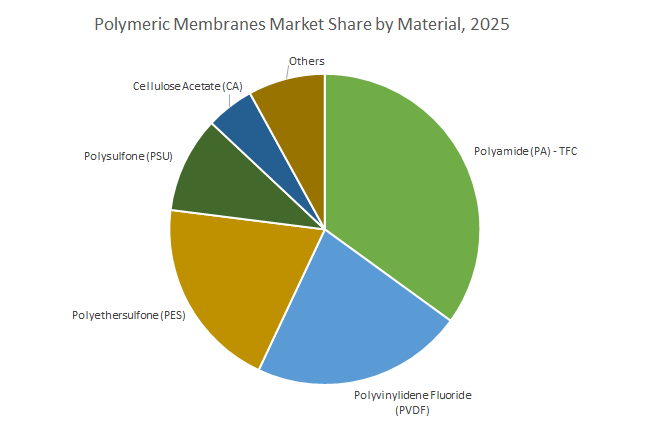

Market Share by Material: Polyamide (PA)-TFC Dominates

China: Regulatory Mandates and Biofouling-Resistant Polymeric Membranes Driving Growth

China’s polymeric membranes market is propelled by stringent regulatory frameworks and technological advancements. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge regulations, encouraging companies to adopt advanced polymeric membrane systems to comply with emission standards. The 14th Five-Year Plan prioritizes water reuse, positioning polymeric membranes as a key technology for municipal and industrial applications. In 2024, researchers at the Institute of Process Engineering (IPE) of the Chinese Academy of Sciences developed a dual-functional RO polymeric membrane with enhanced antibacterial and anti-adhesion properties, targeting biofouling, which accounts for over 45% of operational fouling in RO systems. China’s rapid expansion in membrane production, with competitive pricing and high localization rates, allows domestic players to capture industrial wastewater treatment replacement projects while supporting the growing adoption of polymeric MBR systems for municipal wastewater reuse and renovation projects.

United States: Government Funding and Advanced Polymeric Membranes for Critical Water Applications

The United States market for polymeric membranes is significantly supported by government funding, R&D initiatives, and corporate innovations. Under the Bipartisan Infrastructure Law, over $50 billion is allocated to the EPA for upgrading water infrastructure, including technologies that address emerging contaminants such as PFAS, which necessitate advanced polymeric membranes. The National Alliance for Water Innovation (NAWI), a Department of Energy-funded public-private partnership, is focused on reducing desalination costs and energy use while developing polymeric membranes for waste-brine treatment and renewable-powered plants. Companies like ZwitterCo are expanding their portfolios with biofouling-resistant polymeric membranes leveraging zwitterionic chemistry for industrial water treatment and food processing applications. Key applications in the U.S. include dialysis centers and biologics manufacturing, including monoclonal antibodies, cell and gene therapies, and mRNA-based drugs, driving market growth in high-performance polymeric membrane solutions.

India: Government Initiatives and Large-Scale Infrastructure Projects Fueling Market Expansion

India’s polymeric membranes market benefits from strong government initiatives and strategic infrastructure investments. The “Jal Jeevan Mission” drives membrane technology adoption in rural areas, while the Department of Science & Technology’s Water Technology Initiative supports R&D in nano-material and filtration technologies. The Defence Research and Development Organisation (DRDO) has also developed a high-pressure polymeric membrane for seawater desalination, highlighting India’s focus on indigenous solutions. The Ghaziabad Nagar Nigam raised ₹150 crore through India’s first Certified Green Municipal Bond to establish a Tertiary Sewage Treatment Plant (TSTP) utilizing advanced polymeric membranes for industrial water reuse. Further expansions include the Perur Desalination Plant in Chennai, a 400 MLD facility funded by JICA and executed by Metito and VA TECH WABAG, and the Kakinada SEZ project in Andhra Pradesh, investing ₹1,310 crore in a 3x50 MLD desalination plant to supply industrial water and reduce reliance on freshwater sources.

Germany: Industrial Wastewater Treatment and Technological Innovation Driving Market Leadership

Germany leads in industrial adoption of polymeric membranes, supported by regulatory incentives like the Federal Wastewater Charges Act, which imposes charges on entities discharging untreated wastewater. This has fueled investments in advanced polymeric membrane solutions for industrial wastewater treatment. Technological advancements include CERAFILTEC’s 2024 announcement to provide ceramic flat membranes for MBR projects globally, with capacities ranging from 250 m³/d industrial units to 10,000 m³/d municipal systems. Companies like MANN+HUMMEL focus on innovative membrane and digital solutions that integrate polymeric membranes into industrial processes and green energy initiatives, reinforcing Germany’s leadership in high-efficiency, durable, and environmentally compliant membrane systems.

Japan: Academic Research and High-Efficiency Polymeric Membrane Modules for Biopharmaceuticals

Japan’s polymeric membranes market is supported by robust academic research, corporate R&D, and strategic collaborations. In 2025, Toray Industries developed a high-efficiency separation membrane module for biopharmaceutical manufacturing, offering over twice the filtration performance of conventional systems by minimizing clogging. The Ministry of the Environment allocated USD 1.2 billion in 2024 to promote sustainable infrastructure, including wastewater treatment systems integral to MBR technology. Strategic collaborations, such as the joint development by Siemens Energy and Toray Industries of multi-megawatt class Polymer Electrolyte Membrane (PEM) electrolysis systems, underscore Japan’s commitment to advancing polymeric membrane technologies for both water treatment and industrial energy applications.

Saudi Arabia: Strategic RO Investments and Localized Polymeric Membrane Production

Saudi Arabia remains a pivotal market for polymeric membranes, driven by large-scale reverse osmosis (RO) desalination projects and domestic production initiatives. ACWA Power is leading the Jubail 3A desalination plant, an independent water project producing 600,000 cubic meters of freshwater per day using polymeric RO membranes. The Saline Water Conversion Corporation (SWCC) is advancing highly energy-efficient polymeric RO membranes at the Yanbu 4 plant, producing 450,000 cubic meters per day. Government support through the Saudi Water Partnership Company (SWPC) continues to promote membrane-based desalination projects, with the construction of the Middle East’s first RO membrane plant, producing 254,000 membranes annually starting in 2025, reinforcing Saudi Arabia’s strategic shift from thermal to energy-efficient polymeric membrane desalination technologies.

Competitive Landscape: Leading Innovators in Polymeric Membranes

The competitive landscape of the polymeric membranes market is driven by companies that combine deep expertise in polymer chemistry with strong application portfolios across water, industrial, and environmental sectors. These players differentiate themselves through material innovation, sustainability initiatives, and investments in global production capacity.

DuPont Water Solutions – Global Leader in Sustainable Filtration

DuPont maintains a strong position through its FilmTec™ and IntegraTec™ product lines, which are widely adopted across desalination, water reuse, and industrial processing. The company has recently prioritized membranes engineered for high-biofouling environments, aligning with industries facing water scarcity challenges. Its sustainability-centered strategy focuses on enabling water circularity and operational cost reduction, ensuring relevance in global regulatory landscapes.

Toray Industries, Inc. – Advancing High-Performance RO Membranes

Toray’s vertically integrated model allows full control over polymer development and final product innovation. Its new RO membranes launched in March 2025 stand out for durability and reduced carbon impact. With a Water Treatment Technology Center in Saudi Arabia, Toray is expanding support for large desalination projects while also positioning itself as a partner for sustainable water supply solutions in water-stressed regions.

SUEZ – Integrating Membrane Technology with Circular Economy Goals

SUEZ continues to dominate in municipal and industrial markets through RO, UF, and MBR systems, often integrated with advanced digital platforms. Its recent projects in Brazil and China, alongside European biogas initiatives, highlight how the company leverages membranes not only for water purification but also for resource recovery and energy generation, reinforcing its role in ecological transformation.

Nitto Denko Corporation (Hydranautics) – Pioneering ESG-Focused Membrane Solutions

Nitto Denko, through Hydranautics, has strengthened its reputation with low-fouling and CO₂ separation membranes. Its innovations showcased at COP29 in 2024 reflect its alignment with global decarbonization efforts. The company’s HYDRACAP™ UF and LFC™ RO membranes remain key offerings, enabling both high-performance water purification and environmental remediation applications.

Koch Separation Solutions (Kovalus Separation Solutions) – Expanding Global Capacity

Kovalus is scaling aggressively, marked by its $20 million capacity expansion in Mexico in February 2025 to meet rising demand across dairy, food & beverage, and wastewater reuse markets. Its PURON® MBR and FLUID SYSTEMS® RO/NF products are trusted for reliability in demanding applications. Strategically, the company focuses on enabling higher yield, water reuse, and operational sustainability, making it a rising force in industrial separation solutions.

Polymeric Membranes Market Report Scope

Polymeric Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.3 Billion

|

|

Market Size (2034)

|

$16.7 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Type (Reverse Osmosis (RO) Membranes, Nanofiltration (NF) Membranes, Ultrafiltration (UF) Membranes, Microfiltration (MF) Membranes, Gas Separation Membranes, Pervaporation Membranes, Forward Osmosis (FO) Membranes), By Material (Polyamide (PA), Polysulfone (PSU), Polyethersulfone (PES), Polyvinylidene Fluoride (PVDF), Polypropylene (PP), Cellulose Acetate (CA), Polyacrylonitrile (PAN), Others), By Configuration (Spiral Wound Membranes, Hollow Fiber Membranes, Tubular Membranes, Flat Sheet Membranes, Plate & Frame Modules), By Application (Water & Wastewater Treatment, Desalination, Gas Separation, Food & Beverage Processing , Pharmaceutical & Biotechnology, Chemical & Petrochemical Processing, Power Generation, Oil & Gas), By End-Use Industry (Municipal Sector, Industrial Sector, Residential & Commercial Sector)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Toray Industries, Inc., SUEZ, Veolia, Pentair plc, Xylem Inc., The Dow Chemical Company, Koch Industries, LG Chem, Evoqua Water Technologies, MANN+HUMMEL, Asahi Kasei Corporation, Kubota Corporation, Kuraray Co., Ltd., Mitsubishi Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polymeric Membranes Market Segmentation

By Type

- Reverse Osmosis (RO) Membranes

- Nanofiltration (NF) Membranes

- Ultrafiltration (UF) Membranes

- Microfiltration (MF) Membranes

- Gas Separation Membranes

- Pervaporation Membranes

- Forward Osmosis (FO) Membranes

By Material

- Polyamide (PA)

- Polysulfone (PSU)

- Polyethersulfone (PES)

- Polyvinylidene Fluoride (PVDF)

- Polypropylene (PP)

- Cellulose Acetate (CA)

- Polyacrylonitrile (PAN)

- Others

By Configuration

- Spiral Wound Membranes

- Hollow Fiber Membranes

- Tubular Membranes

- Flat Sheet Membranes

- Plate & Frame Modules

By Application

- Water & Wastewater Treatment

- Desalination

- Gas Separation

- Food & Beverage Processing

- Pharmaceutical & Biotechnology

- Chemical & Petrochemical Processing

- Power Generation

- Oil & Gas

By End-Use Industry

- Municipal Sector

- Industrial Sector

- Food & Beverage

- Pharmaceuticals & Biotech

- Chemicals & Petrochemicals

- Power & Energy

- Oil & Gas

- Pulp & Paper

- Electronics & Semiconductors

- Residential & Commercial Sector

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Polymeric Membranes Industry include-

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- SUEZ

- Veolia

- Pentair plc

- Xylem Inc.

- The Dow Chemical Company

- Koch Industries

- LG Chem

- Evoqua Water Technologies

- MANN+HUMMEL

- Asahi Kasei Corporation

- Kubota Corporation

- Kuraray Co., Ltd.

- Mitsubishi Chemical Corporation

*- List not Exhaustive

Research Coverage

This report investigates the Polymeric Membranes Market, offering detailed analysis reviews, technological breakthroughs, and highlights of the global competitive landscape. Produced by USDAnalytics, this report is an essential resource for industry professionals, policymakers, and technology providers seeking to understand the future of separation and purification technologies. It examines how polymeric membranes, including RO, UF, NF, MF, and gas separation variants, are evolving to meet rising demands in municipal water treatment, desalination, pharmaceuticals, and industrial processing. By exploring advances in anti-fouling coatings, single-use systems for life sciences, and regulatory-driven adoption in zero liquid discharge (ZLD) projects, the study provides actionable insights into sustainability-led growth and innovation shaping the decade ahead. Scope Includes-

- Segmentation: By Type (RO, NF, UF, MF, Gas Separation, Pervaporation, FO), By Material (PA, PSU, PES, PVDF, PP, CA, PAN, Others), By Configuration (Spiral Wound, Hollow Fiber, Tubular, Flat Sheet, Plate & Frame), By Application (Water & Wastewater, Desalination, Gas Separation, Food & Beverage, Pharmaceutical & Biotechnology, Chemical & Petrochemical, Power Generation, Oil & Gas), By End-Use (Municipal, Industrial, Residential & Commercial).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies Covered: Analysis and profiles of 15+ companies including DuPont de Nemours, Toray Industries, SUEZ, Veolia, Pentair, Xylem, Dow Chemical, Koch Industries, LG Chem, Evoqua Water Technologies, MANN+HUMMEL, Asahi Kasei, Kubota, Kuraray, and Mitsubishi Chemical Corporation.

Methodology

The research methodology integrates both primary and secondary approaches to deliver accurate and actionable insights. Primary research involved structured interviews and surveys with executives, engineers, and procurement managers across industries such as water treatment, pharmaceuticals, energy, and food & beverage. Secondary research drew from company filings, scientific journals, regulatory databases, and international trade publications to validate market movements. Quantitative sizing employed bottom-up analysis by segment, triangulated with top-down macroeconomic and infrastructure investment trends, while qualitative insights assessed regulatory drivers, technological innovations, and competitive strategies. This multi-layered methodology ensures a balanced view of current performance and reliable forecasts through 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Polymeric Membranes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

1.3.1. Current Market Size (2025): USD 8.3 Billion

1.3.2. Forecasted Market Size (2034): USD 16.7 Billion

1.3.3. Projected Compound Annual Growth Rate (CAGR): 8.1%

2. Polymeric Membranes Market Outlook (2025–2034)

2.1. Introduction: Role in Global Filtration and Key Drivers

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Recent Developments Shaping Growth Trajectories

2.3.1. DuPont’s Sustainability Award for FilmTec™ Fortilife™ Membranes (August 2025)

2.3.2. SUEZ’s Collaborations in Agriculture and Biogas (July & June 2025)

2.3.3. Toray Industries Launches New RO Membrane with Extended Service Life (March 2025)

2.3.4. Koch Separation Solutions Expands Capacity in Mexico (February 2025)

2.3.5. Nitto Denko Showcases Carbon-Negative Solutions at COP29 (November 2024)

3. Strategic Trends and Opportunities Redefining the Market

3.1. Key Trends Driving Market Growth

3.1.1. Breakthroughs in Anti-Fouling and High-Performance Polymeric Membranes

3.1.2. Strategic Corporate Investments and Academic-Industry Collaborations

3.1.3. Expansion of Polymeric Membranes into Gas Separation, Biopharma, and Energy

3.1.4. Government Regulations and Infrastructure Investments Accelerating Adoption

3.2. Emerging Opportunities

3.2.1. Carbon Capture and Hydrogen Recovery

3.2.2. Pharmaceutical Sterile Filtration

4. Competitive Landscape: Polymeric Membranes Market

4.1. Market Overview: Leaders Driving Innovation and Global Adoption

4.2. Profiles of Top Players

4.2.1. DuPont Water Solutions

4.2.2. Toray Industries, Inc.

4.2.3. SUEZ

4.2.4. Nitto Denko Corporation (Hydranautics)

4.2.5. Koch Separation Solutions (Kovalus Separation Solutions)

5. Polymeric Membranes Market – Segmentation Insights (2025–2034)

5.1. By Type

5.1.1. Reverse Osmosis (RO) Membranes: Largest Segment (30% in 2025)

5.1.2. Ultrafiltration (UF) and Microfiltration (MF) Membranes

5.1.3. Nanofiltration (NF) Membranes

5.1.4. Other Types (Gas Separation, Pervaporation, Forward Osmosis)

5.2. By Configuration

5.2.1. Spiral Wound Membranes: Largest Segment (60% in 2025)

5.2.2. Hollow Fiber Membranes

5.2.3. Flat Sheet/Plate & Frame Membranes

5.2.4. Tubular Membranes

5.3. By Application

5.3.1. Water & Wastewater Treatment: Largest Segment (55% in 2025)

5.3.2. Industrial Processing

5.3.3. Desalination

5.3.4. Gas Separation

5.3.5. Other Applications

6. Country Analysis and Outlook: Polymeric Membranes Market

6.1. China: Regulatory Mandates and Biofouling-Resistant Polymeric Membranes Driving Growth

6.2. United States: Government Funding and Advanced Polymeric Membranes for Critical Water Applications

6.3. India: Government Initiatives and Large-Scale Infrastructure Projects Fueling Market Expansion

6.4. Germany: Industrial Wastewater Treatment and Technological Innovation Driving Market Leadership

6.5. Japan: Academic Research and High-Efficiency Polymeric Membrane Modules for Biopharmaceuticals

6.6. Saudi Arabia: Strategic RO Investments and Localized Polymeric Membrane Production

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Polymeric Membranes Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Configuration

7.1.3. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Configuration

7.2.3. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Configuration

7.3.3. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Configuration

7.4.3. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Configuration

7.5.3. By Application

8. Company Profiles: Leading Players in Polymeric Membranes Market

8.1. DuPont de Nemours, Inc.

8.2. Toray Industries, Inc.

8.3. SUEZ

8.4. Veolia

8.5. Pentair plc

8.6. Xylem Inc.

8.7. The Dow Chemical Company

8.8. Koch Industries

8.9. LG Chem

8.10. Evoqua Water Technologies

8.11. MANN+HUMMEL

8.12. Asahi Kasei Corporation

8.13. Kubota Corporation

8.14. Kuraray Co., Ltd.

8.15. Mitsubishi Chemical Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures