Industrial Water Treatment Equipment Market Outlook 2025–2034: Growth Dynamics, Market Size, and Strategic Imperatives

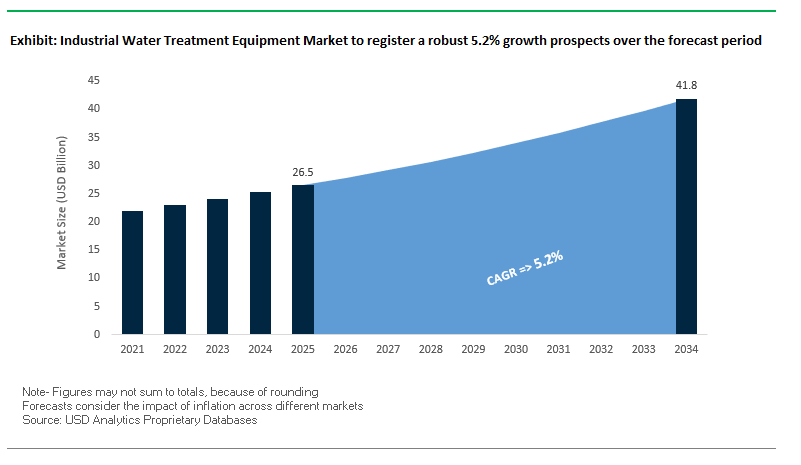

The global industrial water treatment equipment market is poised for sustained expansion, projected to grow from USD 26.5 billion in 2025 to USD 41.8 billion by 2034, registering a CAGR of 5.2%. The growth is underpinned by an interplay of tightening environmental regulations, escalating freshwater scarcity, and the need for ultra-pure process water in advanced manufacturing sectors.

A major catalyst for market expansion is the enforcement of stringent discharge regulations such as the revised EU Urban Wastewater Treatment Directive and updated U.S. EPA effluent guidelines. These policies mandate advanced contaminant removal including PFAS driving industrial facilities toward investment in high-performance treatment systems to avoid compliance penalties. Meanwhile, industrial water reuse is emerging as a critical operational strategy, with nations like India setting aggressive targets for water recycling of 20% by FY2027–28 and 50% by 2031.

In addition, the microelectronics, pharmaceuticals, and power generation industries are spurring demand for ultra-pure water through adoption of advanced membrane filtration and continuous electro-deionization (CEDI) systems. The push for digitalization and automation, leveraging IoT-enabled monitoring and AI-powered predictive maintenance, is reshaping operational efficiency while reducing energy costs and downtime.

Strategic Imperatives for Stakeholders:

- Invest in PFAS and micropollutant removal technologies to align with upcoming global compliance standards.

- Capitalize on industrial water reuse and circular economy trends to unlock new revenue streams.

- Expand digital water solutions for predictive analytics, process automation, and efficiency optimization.

- Target high-purity water markets such as pharmaceuticals and semiconductors with tailored product lines.

- Build regional manufacturing hubs to reduce lead times and mitigate supply chain risks.

Recent Developments Reshaping the Industrial Water Treatment Equipment Landscape

Recent developments between 2024 and 2025 reflect both technological advancements and strategic market positioning by key players. In August 2025, Veolia Water Technologies expanded its pharmaceutical sector footprint by delivering a containerized ORION™ 2000S RO and CEDI unit to a major manufacturer, enabling a 40% reduction in water footprint while increasing production capacity. Just a month later, in September 2025, Veolia secured a multi-million-dollar contract with Petrobras for advanced seawater desalination systems to be deployed on two major FPSOs in Brazil, underscoring the demand for space-efficient, offshore-compatible treatment systems.

SUEZ has also made notable strides. In April 2025, the company entered a five-year research collaboration with CNRS to develop innovative solutions for micropollutant treatment, including PFAS reduction. The move signals a long-term commitment to addressing emerging industrial water challenges. Furthermore, SUEZ inaugurated a 300,000 m³/day seawater desalination plant in China for Wanhua Chemical Group, demonstrating its engineering capability for large-scale, high-demand industrial applications.

On the innovation front, DuPont Water Solutions earned the 2025 BIG Innovation Award for advancements in sustainable purification technologies and introduced the Sustainability Navigator as a digital platform helping water producers assess environmental performance across technology options. Xylem Inc. continues to advance digital water systems, with its Rivo™ I system (launched in August 2024) offering modular, real-time chemical dosing and monitoring solutions adaptable to industrial operations.

Emerging developments also reflect cross-sector innovation. In March 2025, Kurita Water Industries partnered with ispace to deliver a water purification demonstration system to the moon, showcasing the company’s ultra-pure water expertise. Additionally, Pentair’s acquisition of Porous Media in October 2024 expands its industrial filtration capabilities and strengthens its global manufacturing presence.

Trends and Opportunities in Industrial Water Treatment Equipment Market

Trend 1: Zero Liquid Discharge (ZLD) Adoption in Heavy Industry

Industrial water treatment is witnessing a significant shift toward Zero Liquid Discharge (ZLD) systems, particularly in heavy industries such as textiles, chemicals, and power generation. Driven by stringent environmental regulations and ESG (Environmental, Social, and Governance) mandates, ZLD systems enable facilities to recycle 100% of their wastewater, converting a traditional liability into a valuable resource. ZLD adoption delivers operational cost savings and resource recovery, as demonstrated by an Indian textile unit that reused recovered salts from dye effluent in production, creating a circular economy and reducing operational expenses. Beyond cost efficiency, ZLD improves ESG reporting and mitigates water-related business risks with over $300 billion in global water risks were reported by companies in a single year, according to CDP Global Water Report. Regulatory imperatives, particularly in markets like India under initiatives such as Namami Gange, are accelerating adoption, making ZLD a strategic priority for industries seeking compliance and sustainability leadership.

Trend 2: Smart Industrial Water Networks with Digital Twins

The adoption of AI-driven digital twin technology is revolutionizing industrial water treatment operations. By creating virtual replicas of treatment plants, operators can optimize chemical dosing, predict equipment failures, and remotely monitor processes. Studies show AI frameworks can reduce system inefficiency by up to 26%, enabling predictive maintenance, extending asset life, and minimizing costly downtime. Digital twins also enhance regulatory compliance by providing continuous monitoring and generating accurate operational reports. Optimized chemical dosing reduces overuse, ensuring consistent water quality and lower operational costs. As industrial facilities adopt smart networks, digital twin-enabled plants are emerging as a benchmark for operational efficiency, resilience, and sustainability, setting a new standard in industrial water management.

Opportunity 1: PFAS Destruction Technology for Manufacturing

Rising regulatory scrutiny on per- and polyfluoroalkyl substances (PFAS), or ""forever chemicals,"" is creating a significant market opportunity for advanced destruction technologies in industrial water treatment. Unlike conventional methods that only remove PFAS, emerging solutions like electrochemical oxidation (ECO) and supercritical water oxidation (SCWO) permanently destroy these persistent chemicals. Laboratory studies demonstrate up to 99.999% reduction of high-concentration PFAS. Targeted applications include metal finishing, textiles, electronics manufacturing, and landfill leachate streams, which are often high in PFAS content. Modular, automated systems tailored to specific wastewater chemistry allow industries to implement effective on-site solutions, transforming hazardous waste streams into safe outputs while meeting stringent environmental regulations.

Opportunity 2: Modular Treatment for Distributed Manufacturing

Decentralized manufacturing and circular economy initiatives are fueling demand for modular and containerized industrial water treatment systems. These compact units allow on-site water recycling, reducing dependence on municipal water and minimizing environmental impact. Equipped with membrane bioreactors (MBR), reverse osmosis (RO), or other advanced treatment technologies, modular systems enable businesses to recycle water for reuse in processes such as cooling, washing, and landscaping. Their plug-and-play design ensures rapid scalability, relocation, and flexible deployment, which is ideal for facilities with variable production demands or temporary sites. On-site water reuse can reduce freshwater consumption by up to 50%, delivering both cost savings and sustainability benefits, making modular systems a strategic solution for modern industrial water management.

Industrial Water Treatment Equipment Market Share Insights

Market Share by Equipment Type: Filtration Systems as the Universal Workhorse, Specialized Treatment Gaining Ground

Filtration systems are expected to account for around 24.8% of the global industrial water treatment equipment market by 2025, reinforcing their position as the universal backbone of treatment trains. From media and cartridge filters to advanced membrane processes (UF, NF, RO), these systems are indispensable for removing suspended solids, protecting downstream assets, and delivering high-purity water. Alongside the, specialized treatment solutions are gaining momentum, with technologies like electrodeionization (EDI), zero-liquid discharge (ZLD) evaporators, and advanced oxidation processes (AOPs) addressing niche but high-value industrial needs such as ultrapure water and trace organic removal.

.png)

Market Share by Treatment Process: Tertiary and Advanced Treatment Driving Growth Momentum

Tertiary and advanced treatment processes represent roughly 30.6% of the industrial water treatment equipment market, making them the fastest-growing segment. The dominance stems from tightened discharge regulations and escalating corporate water reuse commitments, where advanced oxidation, RO, and polishing filters are essential to close the loop. Secondary biological treatment remains the “heart” of industrial wastewater management, particularly in sectors like food & beverage and chemicals, where membrane bioreactors (MBRs) and moving bed biofilm reactors (MBBRs) ensure compliance and cost efficiency.

Market Share by Industry: Power Generation and Heavy Industries at the Forefront

Power generation holds the largest share at about 22% of the industrial water treatment market, reflecting its demand for massive volumes of ultra-pure boiler feedwater and cooling tower supply. Failure to maintain water quality directly impacts operational uptime and turbine longevity, making treatment systems mission-critical. Metals & mining and pulp & paper industries (~22% combined) also represent major demand centers, driven by acid mine drainage, heavy metal remediation, and high-organic wastewater challenges. Meanwhile, food & beverage and pharmaceuticals drive demand for stringent water quality compliance and ultrapure water (UPW) standards, ensuring product safety and regulatory alignment.

Market Share by System Configuration: Skid-Mounted Systems as the Industry Standard

Skid-mounted systems dominate the market with nearly 45.7% share, reflecting their reputation as the industrial standard for new projects and retrofits. These pre-assembled, pre-piped, and pre-wired modules minimize installation risk, reduce commissioning time, and deliver predictable performance for CAPEX-heavy industries. Fully integrated treatment trains represent the high-value, engineering-intensive projects, especially in zero-liquid discharge and full-scale reuse plants. Modular and containerized systems are expanding in remote sites and temporary operations, where speed and mobility outweigh customization.

Market Share by Automation Level: Fully Automated Systems Cementing Market Leadership

Fully automated systems are set to capture nearly 64.7% of the global industrial water treatment equipment market, underscoring the sector’s reliance on PLC/SCADA-based, IoT-enabled monitoring. These solutions optimize chemical dosing, minimize energy consumption, and ensure continuous compliance with minimal operator intervention. Semi-automated systems remain common in mid-scale plants where cost control and human oversight balance automation, while manual systems persist only in small-scale or low-cost regions, gradually phasing out due to inefficiency.

Market Share by Water Source: Process Wastewater as the Core Application

Process wastewater treatment dominates with about 34.9% market share, as industries prioritize compliance with stringent discharge norms and internal water reuse targets. The segment is the core driver of biological and advanced treatment adoption, with solutions tailored to high-organic, high-salinity, or chemically complex effluents. Municipal water and surface/groundwater remain critical input sources requiring further conditioning through RO, softening, and disinfection to meet industrial standards. Meanwhile, seawater plays an increasing role for coastal industries and power plants, where desalination provides a strategic safeguard against freshwater scarcity.

Country Analysis of the Industrial Water Treatment Equipment Market

United States: Advanced Industrial Water Treatment and Circular Water Practices

The U.S. industrial water treatment equipment market is being propelled by the Bipartisan Infrastructure Law, which allocates significant funding to modernize drinking water and wastewater infrastructure. The initiative, coupled with EPA regulations targeting emerging contaminants like PFAS, is creating strong demand for advanced industrial water treatment systems. Companies are increasingly adopting circular water practices, reclaiming process effluent for reuse to minimize freshwater withdrawals and reduce wastewater discharge, particularly in food and beverage and petrochemical sectors. Market leaders such as Xylem and Evoqua are expanding their portfolios through strategic mergers and acquisitions, offering comprehensive industrial water management solutions. Additionally, the integration of remote monitoring, artificial intelligence, and predictive maintenance platforms enhances operational efficiency and compliance for industrial operators.

China: Policy-Driven Growth in Industrial Water Treatment Technology

China’s industrial water treatment market is strongly influenced by national strategies such as the Water Ten Plan and the Dual Carbon goals, emphasizing sustainable water governance. The government allocated over RMB 26 billion in 2024 for water pollution control, coupled with stricter discharge standards that are phasing out outdated capacity. Industrial wastewater, which accounted for 28.7% of China’s 55.7 billion cubic meters discharged in 2021, is a key target for treatment improvements. Advanced technologies like membrane bioreactors (MBR), reverse osmosis (RO), and nutrient removal systems are being implemented in industrial hubs including Shanghai and the Greater Bay Area. Additionally, Chinese enterprises are increasingly exporting water treatment technologies, extending their footprint across Belt and Road countries, highlighting the global influence of China’s industrial water solutions.

India: Growing Adoption of ZLD and Industrial Wastewater Recycling

India faces a projected water demand twice the available supply by 2030, creating significant growth opportunities for the industrial water treatment equipment market. Industries in power, food and beverage, chemicals, pharmaceuticals, and textiles are adopting advanced treatment technologies including reverse osmosis membranes, sequencing batch reactors (SBR), and membrane bioreactors (MBR). The principles of zero liquid discharge (ZLD) and wastewater recycling are gaining traction, particularly in industrial clusters. Coastal states such as Tamil Nadu and Gujarat are investing in desalination plants to meet process water needs, while government programs like Jal Jeevan Mission and AMRUT 2.0 encourage technological innovation that can extend to industrial applications. Containerized and modular systems are also being deployed to meet decentralized industrial water treatment requirements.

Germany: High-Tech, Decentralized Industrial Water Solutions

Germany’s industrial water treatment equipment market is driven by stringent regulations under the Water Framework Directive, requiring all water bodies to achieve good ecological and chemical status. Advanced technologies such as membrane bioreactors, vacuum distillation, and intelligent monitoring systems are increasingly adopted to enhance operational efficiency and reduce energy consumption. Decentralized wastewater treatment systems are gaining popularity, particularly in rural and industrial zones where central facilities are not practical. Companies like H2O GmbH focus on wastewater-to-resource technologies, producing up to 98% recyclable distillate and enabling wastewater-free industrial production. The country’s robust manufacturing and chemical sectors continue to be major consumers of industrial water treatment solutions, ensuring compliance and sustainable water management.

Saudi Arabia: Strategic Investments in Industrial Water Reuse

Saudi Arabia’s industrial water treatment market aligns with Vision 2030 and the National Water Strategy 2030, emphasizing sustainability, water conservation, and efficient industrial water management. The government is heavily investing in wastewater infrastructure with a focus on treatment and reuse for industrial purposes, targeting nearly 100% water reuse by 2025. The Saudi Water Partnership Company (SWPC) facilitates private sector participation to expand treatment and storage capacities. With approximately 200 wastewater treatment plants already operational, treated non-potable water (“grey water”) is being leveraged for industrial processes. Public-private partnership models are driving six new wastewater treatment projects aimed at industrial water reuse and sustainable process water management, boosting market growth and adoption of modern treatment technologies.

Japan: Innovation in Compact and Energy-Efficient Industrial Water Treatment

Japan’s industrial water treatment market is defined by advanced membrane bioreactor (MBR) systems and continuous innovation in compact, energy-efficient solutions. Companies such as Kubota Corporation have developed submerged membrane units that reclaim industrial effluent efficiently, while startups like DG TAKANO introduce water-saving technologies such as the Bubble90 nozzle, delivering industrial cleaning efficiency with minimal water use. Japanese firms are also integrating IoT, machine learning, and sensor-based monitoring to enhance predictive maintenance and optimize industrial water use. The focus on smart industrial water management solutions ensures compliance, reduces water consumption, and supports sustainability goals across various industrial sectors.

Competitive Landscape: Global Leaders in Industrial Water Treatment Equipment

The competitive environment is characterized by high innovation intensity, integrated solutions, and strategic positioning across diverse industrial sectors. Leading players are differentiating through R&D investment, digital integration, and large-scale project execution capabilities.

Veolia Environnement S.A. – Comprehensive Ecological Transformation Solutions

Veolia has established itself as a global leader in industrial water treatment by delivering end-to-end ecological transformation services. Its portfolio covers membrane bioreactors (MBR), reverse osmosis (RO), and CEDI systems, with the ORION™ series being a preferred choice for pharmaceutical-grade applications. Recent high-value contracts, including the Petrobras offshore desalination project, highlight Veolia’s stronghold in the oil and gas sector. The company’s Hubgrade digital platform enhances plant efficiency through real-time performance monitoring and predictive analytics.

SUEZ S.A. – Pioneering Circular and Sustainable Water Solutions

SUEZ’s competitive advantage lies in its circular economy-driven approach and deployment of energy-efficient, high-performance industrial water systems. Its solutions span membrane filtration, advanced oxidation, and biological treatment, often offered in containerized and modular formats for rapid deployment. The CNRS partnership and large-scale Wanhua Chemical desalination project exemplify its long-term innovation roadmap and ability to execute mega-capacity projects globally.

Xylem Inc. – Smart, Interconnected Industrial Water Technologies

Xylem’s strength is in merging mechanical expertise with digital intelligence. Its portfolio includes pumps, mixers, aerators, filtration units, and analytical devices. The company’s Xylem Vue digital platform and Rivo™ I modular system empower industries with real-time data for process optimization. The combination of physical and digital solutions positions Xylem as a key enabler of Industry 4.0 in water management.

DuPont Water Solutions – Advanced Membrane and Purification Technologies

DuPont specializes in high-performance RO, UF, and NF membranes alongside ion exchange resins, catering to high-purity and industrial reuse applications. The Sustainability Navigator digital tool reflects DuPont’s alignment with ESG-driven decision-making. Its membrane technologies are widely adopted in chemical, semiconductor, and desalination projects, supporting mission-critical water quality standards.

Industrial Water Treatment Equipment Market Report Scope

Industrial Water Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$26.5 Billion

|

|

Market Size (2034)

|

$41.8 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Equipment Type (Filtration Systems, Separation & Clarification Equipment, Disinfection Systems, Softening & Conditioning, Specialized Treatment), By Treatment Process (Preliminary Treatment, Primary Treatment, Secondary Treatment, Tertiary Treatment, Sludge Treatment), By Industry (Power Generation, Oil & Gas, Chemicals & Petrochemicals, Food & Beverage, Pharmaceuticals, Pulp & Paper, Metals & Mining), By System Configuration (Standalone Units, Skid-Mounted Systems, Modular/Containerized Plants, Fully Integrated Treatment Trains), By Automation Level (Manual Operation, Semi-Automated, Fully Automated), By Water Source (Municipal Water, Surface Water, Groundwater, Process Wastewater, Seawater)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., Ecolab, SUEZ, DuPont, Evoqua Water Technologies (now part of Xylem), Kurita Water Industries, Aquatech International LLC, Pentair, Thermax Limited, VA Tech WABAG Ltd., Calgon Carbon Corporation, Kemira Oyj, Dow Water & Process Solutions, GE Water & Process Technologies (now part of SUEZ and others)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Water Treatment Equipment Market Segmentation

By Equipment Type

- Filtration Systems

- Media Filters

- Membrane Systems

- Cartridge & Bag Filters

- Separation & Clarification Equipment

- Disinfection Systems

- UV Sterilizers

- Ozone Generators

- Chlorination Systems

- Softening & Conditioning

- Specialized Treatment

By Treatment Process

- Preliminary Treatment

- Primary Treatment

- Secondary Treatment

- Tertiary Treatment

- Sludge Treatment

By Industry

- Power Generation

- Oil & Gas

- Chemicals & Petrochemicals

- Food & Beverage

- Pharmaceuticals

- Pulp & Paper

- Metals & Mining

By System Configuration

- Standalone Units

- Skid-Mounted Systems

- Modular/Containerized Plants

- Fully Integrated Treatment Trains

By Automation Level

- Manual Operation

- Semi-Automated

- Fully Automated

By Water Source

- Municipal Water

- Surface Water

- Groundwater

- Process Wastewater

- Seawater

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Industrial Water Treatment Equipment Market

- Veolia

- Xylem Inc.

- Ecolab

- SUEZ

- DuPont

- Evoqua Water Technologies (now part of Xylem)

- Kurita Water Industries

- Aquatech International LLC

- Pentair

- Thermax Limited

- VA Tech WABAG Ltd.

- Calgon Carbon Corporation

- Kemira Oyj

- Dow Water & Process Solutions

- GE Water & Process Technologies (now part of SUEZ and others)

* List Not Exhaustive

Research Coverage

This report investigates the Global Industrial Water Treatment Equipment Market, delivering in-depth analysis reviews of regulatory impacts, market dynamics, and technology-driven breakthroughs shaping the industry outlook through 2034. Published by USDAnalytics, the study highlights how rising freshwater scarcity, stricter effluent guidelines, and ultra-pure water demand in industries such as semiconductors, power generation, and pharmaceuticals are accelerating adoption of advanced treatment technologies. It also examines the shift toward digital twin-enabled smart networks, zero liquid discharge (ZLD) adoption, and modular containerized solutions designed for distributed manufacturing. With detailed insights into competitive strategies, recent contracts, and regional policy frameworks, this report is an essential resource for industry professionals, investors, and decision-makers aiming to understand the evolving industrial water treatment equipment landscape.

Scope Includes:

- Segmentation: By Equipment Type (Filtration Systems, Specialized Treatment, Biological Treatment, Desalination, ZLD), By Process (Primary, Secondary, Tertiary & Advanced), By Industry (Power, Metals & Mining, Pulp & Paper, Food & Beverage, Pharmaceuticals, Chemicals, Others), By System Configuration (Skid-Mounted, Fully Integrated, Modular/Containerized), By Automation Level (Manual, Semi-Automated, Fully Automated), and By Water Source (Process Wastewater, Municipal Water, Surface/Groundwater, Seawater).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic & Forecast: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Profiles and strategic assessments of 15+ leading global companies including Veolia, SUEZ, Xylem, DuPont, Pentair, and Kurita.

Methodology

The research methodology applied by USDAnalytics integrates a combination of primary interviews and secondary data analysis to ensure accuracy and reliability. Primary research involved structured interactions with industrial operators, EPC contractors, regulators, and technology providers to validate market adoption patterns, regulatory impacts, and equipment performance trends. Secondary data sources included regulatory frameworks, trade publications, company annual reports, technical white papers, and academic studies to capture global market developments. Market size estimations and forecasts were derived through both top-down and bottom-up approaches, reinforced with data triangulation across geographies, end-use industries, and system types. Scenario analysis factored in global regulatory enforcement, industrial expansion cycles, and technology adoption rates, ensuring robust and forward-looking projections for the industrial water treatment equipment market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Industrial Water Treatment Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Stakeholders

1.3. Global Market Snapshot

2. Industrial Water Treatment Equipment Market Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $26.5 Billion

2.2.2. Forecasted Market Size (2034): $41.8 Billion at 5.2% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Tightening Environmental Regulations (e.g., EU, U.S. EPA)

2.3.2. Escalating Freshwater Scarcity and Water Reuse Targets

2.3.3. Demand for Ultra-Pure Water in Advanced Manufacturing

2.3.4. Digitalization and Automation (IoT, AI)

3. Recent Developments Reshaping the Market Landscape

3.1. Veolia's Expansion in Pharmaceutical and Offshore Sectors

3.2. SUEZ's R&D Collaboration on Micropollutants and Mega-Projects

3.3. DuPont's Innovation in Sustainable Technologies

3.4. Xylem's Advancements in Digital Water Systems

3.5. Other Strategic Developments (Kurita, Pentair)

4. Trends and Opportunities in Industrial Water Treatment

4.1. Trend 1: Zero Liquid Discharge (ZLD) Adoption in Heavy Industry

4.1.1. Regulatory Drivers and ESG Mandates

4.1.2. Operational Cost Savings and Resource Recovery

4.2. Trend 2: Smart Industrial Water Networks with Digital Twins

4.2.1. Optimization of Operations and Predictive Maintenance

4.2.2. Enhanced Regulatory Compliance

4.3. Opportunity 1: PFAS Destruction Technology for Manufacturing

4.3.1. Addressing "Forever Chemicals" with Advanced Methods

4.3.2. Targeted Applications in High-PFAS Industries

4.4. Opportunity 2: Modular Treatment for Distributed Manufacturing

4.4.1. On-Site Water Recycling and Reduced Freshwater Consumption

4.4.2. Plug-and-Play Design for Scalability and Flexibility

5. Industrial Water Treatment Equipment Market Share Insights

5.1. By Equipment Type

5.1.1. Filtration Systems

5.1.2. Specialized Treatment Solutions

5.2. By Treatment Process

5.2.1. Tertiary and Advanced Treatment

5.2.2. Secondary Biological Treatment

5.3. By Industry

5.3.1. Power Generation and Heavy Industries

5.3.2. Food & Beverage and Pharmaceuticals

5.4. By System Configuration

5.4.1. Skid-Mounted Systems

5.4.2. Fully Integrated and Modular Plants

5.5. By Automation Level

5.5.1. Fully Automated Systems

5.5.2. Semi-Automated and Manual Systems

5.6. By Water Source

5.6.1. Process Wastewater Treatment

5.6.2. Municipal Water, Surface/Groundwater, and Seawater

6. Country Analysis of the Industrial Water Treatment Equipment Market

6.1. United States: Advanced Water Treatment and Circular Practices

6.2. China: Policy-Driven Growth and Technology Exports

6.3. India: ZLD and Wastewater Recycling Adoption

6.4. Germany: High-Tech, Decentralized Solutions

6.5. Saudi Arabia: Strategic Investments in Industrial Water Reuse

6.6. Japan: Innovation in Compact and Energy-Efficient Systems

6.7. Other Country Analysis

7. Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Equipment Type, Process, Industry, Configuration, Automation, and Water Source

7.2. Europe Market Size Outlook to 2034

7.2.1. By Equipment Type, Process, Industry, Configuration, Automation, and Water Source

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Equipment Type, Process, Industry, Configuration, Automation, and Water Source

7.4. South America Market Size Outlook to 2034

7.4.1. By Equipment Type, Process, Industry, Configuration, Automation, and Water Source

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Equipment Type, Process, Industry, Configuration, Automation, and Water Source

8. Competitive Landscape: Leading Players in Industrial Water Treatment Equipment

8.1. Veolia

8.2. Xylem Inc.

8.3. Ecolab

8.4. SUEZ

8.5. DuPont

8.6. Evoqua Water Technologies (now part of Xylem)

8.7. Kurita Water Industries

8.8. Aquatech International LLC

8.9. Pentair

8.10. Thermax Limited

8.11. VA Tech WABAG Ltd.

8.12. Calgon Carbon Corporation

8.13. Kemira Oyj

8.14. Dow Water & Process Solutions

8.15. GE Water & Process Technologies (now part of SUEZ and others)

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations