Decentralized Wastewater Treatment Systems Market Growth Outlook to 2034

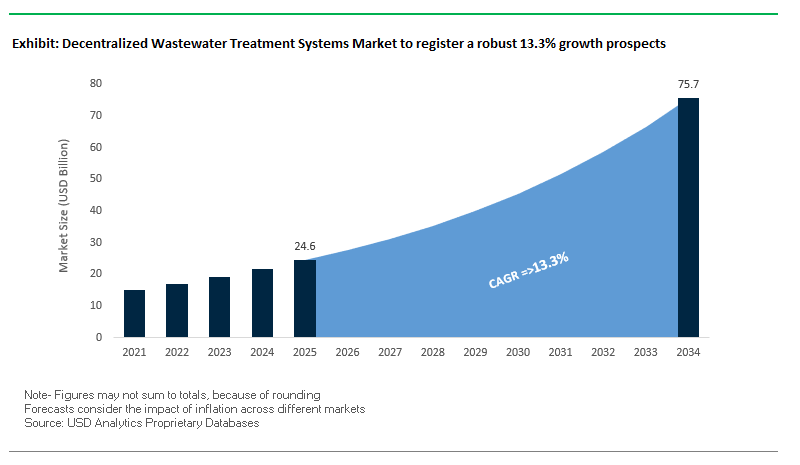

The decentralized wastewater treatment systems market is projected to grow from $24.6 billion in 2025 to $75.7 billion in 2034, expanding at an impressive CAGR of 13.3%. This rapid growth reflects increasing demand for flexible, cost-efficient wastewater management solutions where centralized sewer infrastructure is not feasible. By serving residential areas, small municipalities, and industrial facilities, decentralized systems are emerging as a cornerstone of sustainable water management.

Key Insights:

- Municipal and residential applications lead the market, extending service to underserved suburban and rural communities.

- Asia-Pacific is the fastest-growing region, supported by urban expansion, industrialization, and water recycling mandates.

- Regulatory frameworks worldwide are boosting adoption, with mandatory reuse targets creating opportunities for decentralized systems.

- Capital and operating costs are significantly lower than centralized infrastructure, making these systems attractive for governments and private developers.

Market Analysis: Innovation, Investments, and Regional Expansion

The decentralized wastewater treatment systems market is evolving rapidly, shaped by innovation, sustainability goals, and rising global investment in water infrastructure. In July 2025, SUEZ and SIAAP inaugurated France’s largest biogas unit at the Seine Aval plant, underlining the integration of energy recovery into wastewater systems. In the same month, Veolia Water Technologies was selected to equip France’s largest wastewater reuse project in Argelès-sur-Mer, which will treat over 1.3 million cubic meters of water annually for agriculture a model of decentralized solutions in water-scarce regions.

Strategic consolidation is also reshaping the sector. In May 2025, Veolia acquired full ownership of its Water Technologies and Solutions subsidiary, strengthening its decentralized offerings. That same month, SUEZ launched the Haliotis 2 wastewater treatment plant in Nice, designed as a next-generation municipal facility aligned with ecological transition policies. Earlier, in April 2025, SUEZ and Carcassonne Agglo inaugurated an anaerobic digestion unit in Saint-Jean, while European governments announced fresh R&D funding for advanced membrane coatings to improve efficiency and reduce chemical reliance in decentralized applications.

Technological frontiers are also advancing. In December 2024, Kurita Water Industries demonstrated microbial fuel cell technology, generating electricity from wastewater a breakthrough in energy-positive decentralized treatment systems. In November 2024, Nitto Denko Corporation showcased a carbon-negative membrane-based solution at COP29, designed to capture and reuse CO₂ emissions, marking a leap in cross-sectoral integration of wastewater treatment and carbon management.

Key Market Trends Driving Decentralized Wastewater Treatment Systems

Government Policies and Initiatives Fueling Adoption

Government mandates and strategic policies are central to market expansion. In India, NITI Aayog highlighted decentralized systems as essential to mitigating the looming “Day Zero” crisis, while CPHEEO guidelines emphasize their low-maintenance and energy-efficient nature. Globally, initiatives such as China’s US$27.5 million investment in 180 decentralized facilities in Changshu demonstrate that governments are prioritizing local water treatment to reduce dependence on freshwater and relieve centralized infrastructure. These supportive policies lower adoption barriers and provide funding frameworks, making decentralized wastewater treatment an attractive option for both urban and rural deployments.

Modular, Containerized, and Smart Systems Revolutionize Implementation

The rise of modular, containerized, and smart treatment solutions is transforming how decentralized systems are deployed and managed. Companies like Fluence are championing containerized MABR-based plants under their Aspiral™ line, offering up to 90% energy savings for aeration compared with traditional systems. Global implementations, such as a highway service area project in China, highlight how modularity accelerates deployment, ensures regulatory compliance, and significantly reduces civil works costs. These developments make decentralized treatment increasingly viable for off-grid locations, commercial clusters, and temporary installations.

Integration of Resource Recovery and Circular Economy Models

Decentralized wastewater systems are increasingly being leveraged for resource recovery, aligning with circular economy principles. Technologies such as vermicomposting, composting, and microbial fuel cells (MFCs) enable not only efficient wastewater treatment but also the generation of fertilizers and electricity. According to the U.S. EPA, decentralized systems enable localized water reuse for agriculture and landscaping, cutting costs and energy associated with transporting treated water from centralized facilities. This approach opens new revenue streams and enhances environmental sustainability, positioning decentralized systems as a multifunctional solution rather than a purely treatment-focused technology.

Decentralized Wastewater Treatment Systems Market Share Insights

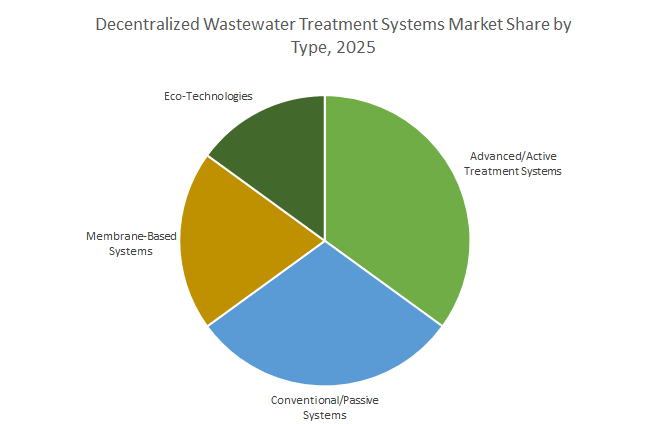

Market Share by System Type: Advanced Systems Lead Performance-Focused Adoption

Advanced/Active Treatment Systems (35%) are the fastest-growing segment due to superior effluent quality and compliance with stringent regulations, particularly in commercial, institutional, and cluster developments. Conventional/Passive Systems (30%), including septic tanks and constructed wetlands, remain significant due to low costs and deep rural penetration but face slower growth due to nutrient and groundwater pollution concerns. Membrane-Based Systems, especially MBR and UF, are gaining prominence for reuse applications, offering pathogen and solids removal suitable for irrigation or non-potable water. Eco-Technologies occupy a niche, valued for low energy consumption and environmental integration, often used in parks, resorts, and small communities.

Market Share by System Capacity: Cluster Systems Drive Growth Beyond Residential Units

Residential/on-site systems (45%) remain dominant due to the high number of unsewered homes; however, growth is plateauing as replacement cycles mature. Cluster systems (30%) represent the sweet spot, offering local treatment, economies of scale, and professional management ideal for suburban housing complexes, hotels, and office parks. Community systems (25%) serve as small-scale centralized alternatives for villages, small towns, or large campuses, reducing the need for costly sewer extensions while providing modern, compliant solutions. The shift toward cluster and community systems reflects a broader trend of balancing decentralization with operational efficiency.

Market Share by Treatment Level: Advanced Secondary and Tertiary Services Expand with Reuse Demand

Secondary treatment (50%) remains the baseline standard for removing biodegradable organics and suspended solids, particularly in residential and cluster systems. Advanced Secondary Treatment (30%), which incorporates nutrient removal (N, P), is rapidly growing due to environmental regulations preventing eutrophication and protecting sensitive water bodies. Tertiary treatment (20%) is entirely driven by water reuse requirements, including disinfection (UV, chlorination) and filtration, enabling safe irrigation, industrial reuse, and non-potable applications. This progression underscores the increasing demand for high-quality effluent and the strategic role decentralized systems play in water sustainability initiatives.

United States: Federal Initiatives and Technological Integration Propel Market Growth

The U.S. decentralized wastewater treatment systems market is benefiting from strong government initiatives and infrastructure funding. The EPA’s "Closing America's Wastewater Access Gap Initiative" is designed to support 150 communities with decentralized wastewater needs, offering access to federal funding. Under the Bipartisan Infrastructure Law (BIL), over $50 billion is allocated to enhance water infrastructure, including decentralized systems as cost-effective solutions for small communities and individual properties. The Clean Water State Revolving Fund provides low-interest loans, particularly for projects addressing emerging contaminants like PFAS. Advanced U.S. decentralized systems increasingly integrate IoT sensors, data analytics, and predictive maintenance technologies to improve treatment efficiency and reduce operational costs. These systems are widely deployed in rural and semi-urban areas, single-family homes, multi-family developments, and commercial facilities where centralized treatment is impractical.

China: Policy Enforcement and Containerized Innovations Drive Adoption

China’s decentralized wastewater treatment market is expanding due to stringent regulatory enforcement and government-backed initiatives. The Ministry of Ecology and Environment (MEE) mandates strict industrial wastewater discharge standards, aligning with the 14th Five-Year Plan, which targets 95% wastewater treatment coverage in county-level cities and promotes water reuse. Technological advancements have introduced containerized decentralized systems with ultrafiltration and solar-powered units, as well as household nanofiltration solutions using graphene oxide membranes. Corporate innovators like OriginWater and Jiangsu Jiuwu Hi-Tech have deployed 20-foot containerized systems capable of producing 50,000 liters of clean water daily at lower costs than conventional plants, with applications both domestically and internationally. Government efforts to enhance urban and rural living standards further accelerate adoption of decentralized solutions where centralized systems are not feasible.

India: Mission-Driven Adoption and Advanced Treatment Technologies

India’s decentralized wastewater treatment market is strongly influenced by national water initiatives, infrastructure investment, and technological adoption. The "Jal Jeevan Mission" prioritizes localized wastewater management, aiming to treat and reuse greywater at the community and household level. Advanced decentralized solutions, including constructed wetlands for rural areas, sequencing batch reactors (SBR) for semi-urban developments, and phycoremediation using microalgae, are gaining traction. Infrastructure investment through the Atal Mission for Rejuvenation and Urban Transformation (AMRUT) supports expansion of water supply and wastewater treatment services. Corporate players and innovation clusters, such as DRIIV (Delhi Research Implementation and Innovation), are fostering academia-industry collaborations, enabling real-world implementation of decentralized systems. These solutions are increasingly deployed in residential colonies, small townships, and industrial facilities in remote locations lacking centralized sewer connections.

Germany: Regulatory Stringency and Advanced MBR Development Promote Market

Germany’s decentralized wastewater treatment systems market is shaped by EU-wide regulatory updates and technological innovation. The 2025 EU Urban Wastewater Directive mandates the “4th purification stage” to remove micropollutants, driving demand for decentralized systems capable of meeting stringent discharge standards. German research is exploring membrane-like aerobic reactors and other decentralized approaches for domestic wastewater treatment, offering performance comparable to traditional membrane bioreactors (MBRs). These systems are especially suited for peri-urban and urban areas with space constraints, providing a compact, efficient alternative to conventional wastewater treatment plants while ensuring regulatory compliance.

Japan: Johkasou Systems and Aging Infrastructure Support Decentralization

Japan’s decentralized wastewater market is distinguished by advanced on-site systems known as "Johkasou," which biologically treat blackwater and greywater. These systems are cost-effective solutions for rural and peri-urban areas. Aging sewer infrastructure, much of which is over 50 years old, has prompted local governments to integrate decentralized systems with satellite and drone-based leak detection to improve efficiency and reduce reliance on large-scale centralized upgrades. Decentralized systems play a pivotal role in maintaining sustainable water infrastructure amidst a declining population and constrained municipal budgets.

Australia: Water Scarcity and Sustainable Urban Water Management Drive Growth

Australia’s decentralized wastewater treatment systems market is heavily influenced by water scarcity and integrated urban water management (IUWM) principles. Recycled water is a critical component for sustainable water services, and small-scale, environmentally-friendly sewerage systems are being increasingly adopted. Advanced biological and filtration methods, such as Biolytix vermiculture treatment, produce nutrient-rich effluent suitable for irrigation. Metropolitan utilities, particularly in Melbourne, are exploring decentralized systems as a long-term solution to address population growth, urbanization, and prolonged drought conditions, ensuring reliable wastewater management in water-stressed regions.

Competitive Landscape: Leading Players Driving Decentralized Wastewater Treatment

The competitive landscape of the decentralized wastewater treatment systems market is characterized by a mix of global leaders and specialized innovators. Companies are focusing on modular designs, energy recovery technologies, and digital monitoring platforms to improve system performance while reducing life-cycle costs. Below are key company profiles shaping the industry:

Xylem Inc. Expands Modular and Digital Wastewater Solutions

Xylem leverages its extensive global portfolio of pumps, biological treatment systems, and digital monitoring technologies to deliver modular decentralized solutions. Its expertise spans advanced oxidation processes, membrane bioreactors (MBR), and on-site monitoring systems designed for municipalities, agriculture, and food processing industries. The company’s acquisition of Evoqua in 2023 created a more integrated platform, enhancing its ability to serve both industrial and residential markets. Xylem continues to invest in IoT-enabled real-time monitoring and predictive maintenance, positioning itself as a leader in cost-efficient, digitally enabled decentralized treatment systems.

Veolia Strengthens Position with Large-scale Reuse Projects

Veolia Water Technologies is a global leader in ecological transformation, offering comprehensive decentralized wastewater treatment solutions. In July 2025, it was chosen to equip France’s largest water reuse project, demonstrating its capacity to execute high-impact projects for agriculture and municipal clients. Veolia’s offerings include packaged plants, MBR technologies, and the Ecodisk™ biodisc system, tailored for small to mid-sized communities. Its May 2025 acquisition of Water Technologies and Solutions further consolidated its market strength, enabling integrated delivery of decentralized solutions for municipal, industrial, and agricultural applications.

SUEZ Leverages Digital Integration for Decentralized Systems

SUEZ maintains strong global leadership in water and wastewater management, with a focus on customized decentralized systems for challenging environments. Recent contracts in Asia, including a large-scale plant in China, highlight its expanding global footprint. SUEZ provides modular plants, membrane technologies, and advanced biological treatment processes. Its integration of predictive analytics and digital monitoring platforms enables proactive plant management, optimizing energy consumption and reducing chemical use an advantage in decentralized installations where on-site staff is limited.

Orenco Systems Focuses on Affordable, Low-energy Decentralized Technologies

Orenco Systems is a pioneer in sustainable decentralized wastewater solutions, known for its AdvanTex® recirculating textile filters that serve everything from single homes to entire subdivisions. Its STEP (Septic Tank Effluent Pumping) and STEG (Septic Tank Effluent Gravity) systems cost only a fraction of traditional sewers, making them ideal for rural and peri-urban markets. Orenco emphasizes long-lasting, low-energy technologies that promote water reuse while maintaining minimal life-cycle costs. Its solutions are particularly attractive for fringe development projects and small municipalities seeking reliable, low-cost infrastructure.

DuPont Water Solutions Advances Membrane-based Decentralized Treatment

DuPont Water Solutions applies its materials science expertise to produce high-performance membranes, critical to decentralized wastewater treatment. Its FilmTec™ RO and NF membranes and IntegraTec™ ultrafiltration technologies form the backbone of efficient, compact systems deployed across industrial and municipal applications. In recognition of its sustainability leadership, DuPont received the BIG Sustainability Award for its FilmTec™ Fortilife™ membranes, which enable enhanced reuse and durability in challenging wastewater environments. The company continues to push for water circularity and carbon footprint reduction, making it a key player in shaping the decentralized treatment landscape.

Decentralized Wastewater Treatment Systems Market Report Scope

Decentralized Wastewater Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$24.6 Billion

|

|

Market Size (2034)

|

$75.7 Billion

|

|

Market Growth Rate

|

13.3%

|

|

Segments

|

By Type (Conventional/Passive Systems, Advanced/Active Treatment Systems, Membrane-Based Systems, Eco-Technologies), By System Capacity (Residential/On-Site Systems, Cluster Systems, Community Systems), By Treatment Level (Secondary Treatment, Advanced Secondary Treatment, Tertiary Treatment), By End-User (Residential, Commercial & Institutional, Industrial & Agricultural)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Kubota Corporation, Toray Industries, Inc., V.A. TECH WABAG Ltd., Aquatech International, Kurita Water Industries Ltd., Organica Water, Inc., H2O GmbH, Biolytix, OriginWater, MANN+HUMMEL

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Decentralized Wastewater Treatment Systems Market Segmentation

By Type

- Conventional/Passive Systems

- Advanced/Active Treatment Systems

- Membrane-Based Systems

- Eco-Technologies

By System Capacity

- Residential/On-Site Systems

- Cluster Systems

- Community Systems

By Treatment Level

- Secondary Treatment

- Advanced Secondary Treatment

- Tertiary Treatment

By End-User

- Residential

- Commercial & Institutional

- Industrial & Agricultural

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Decentralized Wastewater Treatment Systems Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Kubota Corporation

- Toray Industries, Inc.

- V.A. TECH WABAG Ltd.

- Aquatech International

- Kurita Water Industries Ltd.

- Organica Water, Inc.

- H2O GmbH

- Biolytix

- OriginWater

- MANN+HUMMEL

*- List not Exhaustive

Research Coverage

This report investigates the Decentralized Wastewater Treatment Systems Market through analysis reviews of demand drivers, deployment models, and policy catalysts, while mapping technology breakthroughs in modular MBR/UF, IoT-enabled operations, and energy-positive treatment. Produced by USDAnalytics, it highlights cost-to-serve advantages versus sewers, payback levers in reuse-ready effluent, and the shift toward cluster/community systems in fast-growing regions. With evidence-led benchmarking, risk/opportunity scoring, and procurement guidance for owners and EPCs, this report is an essential resource for utilities, developers, industrial estates, and investors planning compliant, scalable, and digitally monitored decentralized assets through 2034. Scope Includes-

- Segmentation

- By Type: Conventional/Passive Systems; Advanced/Active Treatment Systems; Membrane-Based Systems; Eco-Technologies

- By System Capacity: Residential/On-Site Systems; Cluster Systems; Community Systems

- By Treatment Level: Secondary Treatment; Advanced Secondary Treatment; Tertiary Treatment

- By End-User: Residential; Commercial & Institutional; Industrial & Agricultural

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic/Forecast Horizon: Historic data 2021–2024 and forecasts 2025–2034.

- Companies (Analysis/profiles of 15+ companies): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Kubota Corporation; Toray Industries, Inc.; V.A. TECH WABAG Ltd.; Aquatech International; Kurita Water Industries Ltd.; Organica Water, Inc.; H2O GmbH; Biolytix; OriginWater; MANN+HUMMEL.

Methodology

USDAnalytics applies an integrated top-down/bottom-up framework: country baselines are built from sanitation coverage, sewer extension costs, and reuse mandates, then reconciled with project/tender pipelines and vendor shipments by type, capacity band, and treatment level. Primary research (utility engineers, onsite system operators, OEMs/EPCs, regulators) validates CAPEX/OPEX, kWh/m³, chemical dose, sludge logistics, and SLA uptime for packaged plants, cluster systems, and community WWTPs. Secondary inputs span permits, tariff orders, subsidy rules, and technical datasheets to benchmark SDI control, TN/TP removal, and disinfection performance. Scenario analysis stress-tests energy prices, nutrient limits, groundwater protection rules, and labor constraints; a diffusion model quantifies modular/containerized adoption versus conventional build-outs to deliver defensible 2025–2034 forecasts.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Decentralized Wastewater Treatment Systems Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights: Market Drivers, Regional Growth, and Cost Efficiency

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): USD 24.6 Billion

1.3.2. Projected Market Valuation (2034): USD 75.7 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 13.3%

2. Market Outlook (2025–2034)

2.1. Introduction: Growth, Drivers, and the Shift to Decentralized Solutions

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Market Trends Driving Decentralized Wastewater Treatment

2.3.1. Government Policies and Initiatives Fueling Adoption

2.3.2. Modular, Containerized, and Smart Systems Revolutionize Implementation

2.3.3. Integration of Resource Recovery and Circular Economy Models

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Recent Innovations, Investments, and Regional Expansion

3.1.1. Veolia and SUEZ Secure Major Wastewater Reuse Contracts in Europe (July 2025)

3.1.2. Strategic Consolidations and Portfolio Expansions Drive Sector Growth

3.1.3. Technological Breakthroughs in Energy-Positive and Carbon-Negative Treatment

3.1.4. Federal Funding in the U.S. and India Deploys Decentralized Solutions

4. Competitive Landscape: Leading Players

4.1. Competitive Overview: Global Leaders and Specialized Innovators

4.2. Strategic Profiles of Key Companies

4.2.1. Xylem Inc.: Expanding Modular and Digital Wastewater Solutions

4.2.2. Veolia: Strengthening Position with Large-scale Reuse Projects

4.2.3. SUEZ: Leveraging Digital Integration for Decentralized Systems

4.2.4. Orenco Systems: Focus on Affordable, Low-energy Decentralized Technologies

4.2.5. DuPont Water Solutions: Advancing Membrane-based Decentralized Treatment

5. Decentralized Wastewater Treatment Systems Market – Segmentation Insights

5.1. By System Type

5.1.1. Advanced/Active Treatment Systems (35% Market Share)

5.1.2. Conventional/Passive Systems (30% Market Share)

5.1.3. Membrane-Based Systems

5.1.4. Eco-Technologies

5.2. By System Capacity

5.2.1. Residential/On-Site Systems (45% Market Share)

5.2.2. Cluster Systems (30% Market Share)

5.2.3. Community Systems (25% Market Share)

5.3. By Treatment Level

5.3.1. Secondary Treatment (50% Market Share)

5.3.2. Advanced Secondary Treatment (30% Market Share)

5.3.3. Tertiary Treatment (20% Market Share)

5.4. By End-User

5.4.1. Residential

5.4.2. Commercial & Institutional

5.4.3. Industrial & Agricultural

6. Country Analysis: Decentralized Wastewater Treatment Systems Market

6.1. United States: Federal Initiatives and Technological Integration Propel Market Growth

6.2. China: Policy Enforcement and Containerized Innovations Drive Adoption

6.3. India: Mission-Driven Adoption and Advanced Treatment Technologies

6.4. Germany: Regulatory Stringency and Advanced MBR Development Promote Market

6.5. Japan: Johkasou Systems and Aging Infrastructure Support Decentralization

6.6. Australia: Water Scarcity and Sustainable Urban Water Management Drive Growth

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Market Outlook

7.1.1. By System Type

7.1.2. By System Capacity

7.1.3. By End-User

7.2. Europe Market Outlook

7.2.1. By System Type

7.2.2. By System Capacity

7.2.3. By End-User

7.3. Asia Pacific Market Outlook

7.3.1. By System Type

7.3.2. By System Capacity

7.3.3. By End-User

7.4. South America Market Outlook

7.4.1. By System Type

7.4.2. By System Capacity

7.4.3. By End-User

7.5. Middle East & Africa Market Outlook

7.5.1. By System Type

7.5.2. By System Capacity

7.5.3. By End-User

8. Company Profiles: Leading Players

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. DuPont de Nemours, Inc.

8.6. Kubota Corporation

8.7. Toray Industries, Inc.

8.8. V.A. TECH WABAG Ltd.

8.9. Aquatech International

8.10. Kurita Water Industries Ltd.

8.11. Organica Water, Inc.

8.12. H2O GmbH

8.13. Biolytix

8.14. OriginWater

8.15. MANN+HUMMEL

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures