Market Overview: Rising Demand for Wastewater Treatment Services Amid Global Water Scarcity

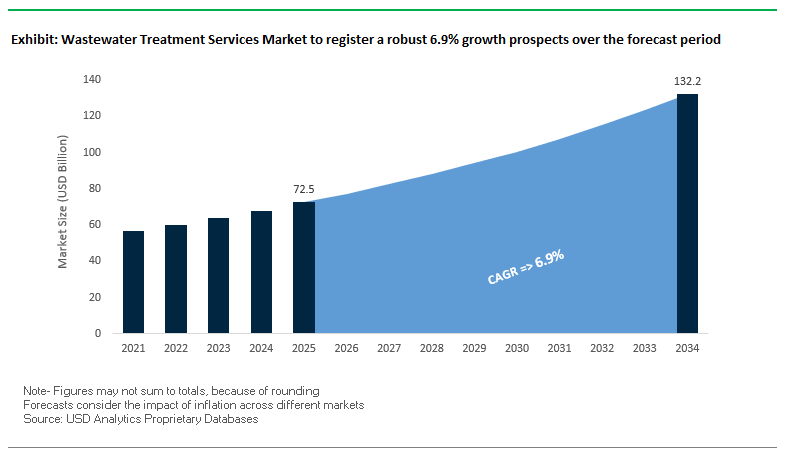

The wastewater treatment services market is projected to reach $72.5 billion in 2025 and expand to $132.2 billion by 2034, registering a steady CAGR of 6.9%. Growth is fueled by escalating urbanization, stricter discharge regulations, and the rising importance of water reuse, sludge management, and digital water optimization technologies.

Key Insights:

- Operation and Maintenance (O&M) services dominate the market, holding over 44% share in 2024, underscoring the critical role of recurring, long-term contracts in wastewater plant management.

- Industrial wastewater services account for more than 52% of the total share in 2024, driven by compliance pressures on chemicals, pharmaceuticals, textiles, and food processing industries.

- Asia-Pacific leads the market, supported by industrial expansion, urbanization, and rising environmental regulations in China and India.

- Smart sewer and digital water services are gaining traction, with one U.S. utility reducing sewer overflow by 80% and saving $400 million through advanced analytics.

Market Analysis: Key Developments Shaping Wastewater Treatment Services

The wastewater treatment services industry is evolving rapidly, with strategic acquisitions, digital innovations, and energy-positive wastewater treatment systems emerging as focal points.

In August 2025, DuPont Water Solutions was recognized in the BIG Sustainability Awards for breakthroughs in industrial wastewater reuse and minimal liquid discharge (MLD), reinforcing the role of advanced membranes in circular water management. Just a month earlier, in July 2025, SUEZ and SIAAP inaugurated France’s largest biogas unit at the Seine Aval plant, showcasing how wastewater services are being integrated with the circular economy and renewable energy generation. That same month, Veolia Water Technologies was contracted for France’s largest treated wastewater reuse project in Argelès-sur-Mer, further cementing Europe’s leadership in reuse-driven wastewater strategies.

Strategic consolidation also defined the year, with Veolia’s acquisition in May 2025 of its Water Technologies and Solutions subsidiary, positioning it to expand capacity in advanced treatment and operation services. Meanwhile, Kurita Water Industries (April 2025) demonstrated wastewater’s potential as a renewable energy source by powering devices with microbial fuel cells, reflecting a shift toward energy-positive wastewater plants.

Earlier innovations included Europe’s March 2025 funding initiative for anti-fouling membrane coatings, designed to extend membrane lifespans and cut chemical costs, and Xylem’s January 2025 partnership with UAJA in Pennsylvania to implement a biological hydrolysis system for biosolid-to-energy conversion. Additionally, in September 2024, Veolia delivered water facilities to Brazil’s largest eucalyptus pulp project, highlighting growth opportunities in emerging economies.

Key Trends Shaping the Wastewater Treatment Services Market

Public-Private Partnerships (PPPs) as a Growth Engine

The adoption of PPPs is redefining infrastructure development in wastewater management. The Shanghai Zhuyuan Youlian No. 1 wastewater treatment plant (ZY1WWTP) demonstrates how leveraging private investment can reduce costs by approximately 40% while improving operational efficiency. Globally, municipalities are under increasing fiscal pressure to meet stringent environmental mandates, making partnerships with private service providers an attractive strategy. This trend highlights the market's shift toward risk-sharing and performance-based models, where the public sector focuses on regulation while the private sector brings operational expertise, advanced technologies, and financial efficiency.

Outsourcing and “Wastewater Treatment as a Service” (WTaaS)

Outsourcing and Water Treatment As A Service operations to specialized service providers is rapidly gaining traction, particularly in manufacturing, food & beverage, and industrial sectors. Companies like Veolia are enabling clients to transition from capital-intensive infrastructure ownership to operational expenditure models, offering complete O&M management. This approach allows businesses to focus on core operations while accessing cutting-edge, energy-efficient treatment technologies. With wastewater treatment processes consuming 3–4% of global energy, outsourcing is not only cost-effective but also reduces carbon footprints, making WTaaS a strategic lever for sustainability and operational resilience.

Integration of Digital and Smart Technologies

The market is witnessing accelerated adoption of digital solutions such as AI, IoT, and predictive analytics for real-time monitoring and process optimization. These technologies reduce manual intervention, enhance predictive maintenance, and ensure regulatory compliance with stringent discharge standards. For example, India’s CPCB 2025 mandatory discharge norms are catalyzing demand for advanced digital solutions that guarantee continuous compliance. The integration of smart technologies is positioning wastewater service providers as essential partners in operational optimization, regulatory adherence, and resource efficiency.

Resource Recovery Transforming Waste into Revenue

Wastewater is increasingly recognized as a valuable resource rather than a disposal problem. Policies like India’s National Water Policy and Liquid Waste Management Rules (2025) incentivize the reuse of treated wastewater, encouraging industries to monetize water and biosolid byproducts. Case studies on biosolid reuse in agriculture demonstrate tangible improvements in soil fertility and nutrient management. This shift toward circular economy models is creating new market opportunities for service providers specializing in resource recovery, offering both environmental and economic value.

Wastewater Treatment Services Market Share Insights

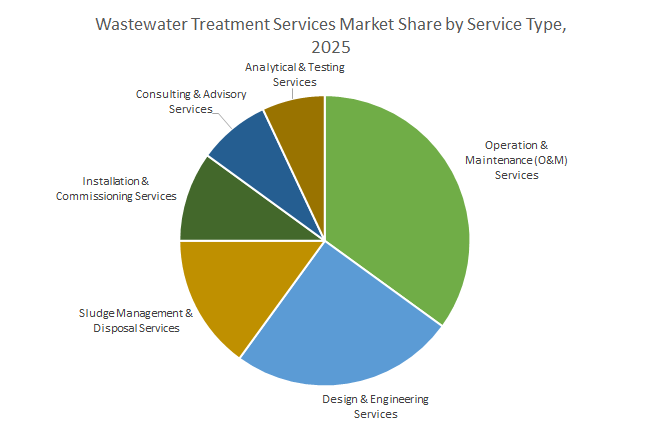

Market Share by Service Type: Dominance of Operation & Maintenance (O&M)

O&M services are projected to hold 35% of the market by 2025, driven by the ongoing need to keep complex wastewater treatment systems operational and compliant. This dominance reflects a broader trend toward outsourcing day-to-day operations to specialized service providers, reducing risk and controlling long-term OPEX. Design & Engineering services (25%) are closely tied to CAPEX cycles for plant construction and upgrades, while Sludge Management (15%) is a growing niche due to the complexity and high cost of disposal. Consulting, Advisory, and Analytical services, though smaller, are high-margin offerings crucial for navigating regulatory landscapes and optimizing operational efficiency.

Market Share by Treatment Type: Growth in Advanced and Tertiary Services

Secondary treatment services (45%) form the backbone of compliance, addressing biological nutrient removal and organic matter reduction. However, the fastest-growing segments are tertiary/advanced treatment (30%) and specialized advanced services (10%), which cater to water reuse, nutrient removal, and emerging contaminants such as PFAS. This trend indicates that wastewater treatment service providers must invest in expertise and technologies capable of meeting stringent environmental standards and facilitating resource recovery, positioning themselves as strategic partners rather than just compliance providers.

Market Share by Service Delivery Model: Rise of Long-Term Contractual Agreements

Contractual O&M services (40%) and PPP models (25%) dominate the service delivery landscape, reflecting the market’s shift toward risk-sharing and long-term operational commitments. On-demand services (20%) remain essential for emergency response and specialized interventions, while BOT (15%) supports greenfield projects with eventual public ownership. The prevalence of long-term models underscores the increasing importance of reliability, performance guarantees, and operational expertise, providing service providers with stable revenue streams and clients with predictable outcomes.

China: Regulatory Enforcement and Technological Innovation Drive Service Demand

China’s wastewater treatment services market is expanding rapidly due to stringent regulatory oversight and government-driven initiatives. The Ministry of Ecology and Environment (MEE) enforces rigorous industrial wastewater discharge standards, motivating companies to adopt advanced treatment technologies. The 14th Five-Year Plan emphasizes water reuse, aiming for 95% wastewater treatment in all county-level cities, creating robust demand for biological treatment services. Government investment is substantial, targeting heavily polluting industries such as textiles, steel, and pharmaceuticals, with plans to allocate $50 billion by 2025. Technological advancements are also shaping the market; in 2025, SUEZ introduced the “embedded WWTP” concept for Hengli Group, leveraging 12 patented technologies to reduce energy and material consumption while minimizing emissions and preventing secondary pollution. Membrane bioreactors (MBRs) are increasingly deployed in municipal and industrial wastewater treatment projects, offering compact designs and compliance with stringent discharge standards.

United States: Infrastructure Upgrades and Regulatory Push Enhance Market Growth

The U.S. wastewater treatment services market is fueled by significant government funding and infrastructure investments. The Bipartisan Infrastructure Law allocates over $50 billion to the EPA, with specific focus on emerging contaminants like PFAS, necessitating advanced biological and membrane filtration technologies. Retrofits of existing water treatment facilities are underway to comply with the EPA’s new PFAS Maximum Contaminant Levels. Major infrastructure projects, such as the Northeast Boundary Tunnel in Washington, D.C., part of the $3 billion Clean Rivers Project, exemplify innovative approaches to combined sewage overflow (CSO) management. Leading companies like Xylem Inc. are expanding services, with strong revenue growth reflecting robust demand for biological treatment, resource recovery, and bioenergy generation in sectors including food and beverage.

India: National Missions and PPP Models Accelerate Wastewater Treatment Services

India’s wastewater treatment services market is growing under the influence of regulatory policies, government programs, and infrastructure investment. The Central Pollution Control Board (CPCB) has implemented new discharge standards for sewage treatment plants (STPs) effective in 2025, complemented by the Liquid Waste Management Rules covering urban and rural local bodies. National initiatives, such as the extended “Namami Gange Mission” through 2026, focus on sewerage infrastructure development with 193 projects worth ₹30,387.24 crore. AMRUT has allocated over ₹44,943 crore for 501 new sewerage and septage management projects, creating 3,591 MLD of new STP capacity. Corporate participation, including SUEZ’s performance-based contract with the Kerala Water Authority (KWA), underscores the increasing role of private expertise in operations and maintenance of municipal wastewater systems.

Germany: Advanced Standards and Technology Adoption Lead Europe’s Market

Germany remains a leader in wastewater treatment services due to regulatory enforcement and advanced technological deployment. The revised EU Urban Wastewater Treatment Directive, effective January 2025, imposes deeper treatment requirements covering more settlements, positioning Germany at the forefront of compliance. The German Federal Environment Agency (UBA) reports that over 90% of major cities are implementing strategies for climate-resilient wastewater management, driving demand for advanced monitoring systems, digital twins, and AI-enabled optimization. Germany is Europe’s largest exporter of water technologies, with export volumes of nearly EUR 1.28 billion in 2024, while its domestic sustainable water management market reached EUR 18.8 billion in 2023, reflecting a strong ecosystem for wastewater services.

Saudi Arabia: Vision 2030 and Large-Scale ISTPs Boost Service Market

Saudi Arabia’s wastewater treatment services market is strengthened by strategic investments and infrastructure development. The Saudi Water Partnership Company (SWPC) commissioned three independent sewage treatment plants (ISTPs) in 2024 with a combined capacity of 440,000 m³/d, serving Madinah, Tabuk, and Buraydah. Upcoming projects, including the Arana ISTP in Makkah, aim for an initial 250,000 m³/day capacity, expandable to 500,000 m³/day, under the PPP model. Aligned with Vision 2030, these projects focus on treated wastewater reuse for agriculture and non-potable municipal applications, integrating transmission pipelines to link effluent with downstream users, enhancing the market for sustainable wastewater treatment services.

Japan: Membrane Technology Leadership and MBR Adoption Propel Market Growth

Japan’s wastewater treatment services market is characterized by technological leadership and regulatory support. The MLIT-led A-JUMP project promotes full-scale adoption of membrane bioreactor (MBR) technology, enhancing conditions for medium- to large-scale plant reconstruction. Japanese firms and academic institutions excel in biological wastewater treatment innovation, building on a tradition of advanced on-site systems, including “Johkasou” for blackwater and greywater treatment. In 2025, Toray Industries developed a high-efficiency separation membrane module for biopharmaceutical applications, showcasing Japan’s prowess in membrane technologies critical for delivering advanced wastewater treatment services. The market is also driven by high population density and the necessity for optimized water reuse.

Competitive Landscape: Leading Wastewater Treatment Service Providers

The competitive landscape of wastewater treatment services is shaped by global leaders in ecological transformation, specialized water technology innovators, and sustainability-focused startups. The industry is defined by large-scale service contracts, strategic acquisitions, and technological leadership in digital water platforms, membrane innovations, and energy recovery solutions.

Veolia Water Technologies – Global Leader in Wastewater Services

Veolia is a frontrunner in ecological transformation and offers end-to-end wastewater services, from plant construction to long-term O&M contracts. Its May 2025 acquisition of full ownership of Water Technologies and Solutions enhanced its integrated portfolio. Veolia’s key offerings include biological treatment systems, mobile water solutions, and smart reuse infrastructure, aligned with its GreenUp strategy, which emphasizes resource recovery and climate resilience.

SUEZ – End-to-End Wastewater Management with Digital Integration

SUEZ delivers comprehensive wastewater treatment services, combining equipment, process optimization, and predictive analytics. With a strong presence in Asia since 1978, it recently secured major projects in China to enhance municipal water resilience. Its portfolio spans sludge management, wastewater reuse, and O&M contracts, strengthened by digital platforms that optimize plant performance and reduce fouling.

Xylem Inc. – Full Water Cycle Solutions with Strong Innovation Focus

Xylem is a global water technology powerhouse, offering MBRs, advanced oxidation, biological treatment, and digital asset management. Its 2023 acquisition of Evoqua created a more integrated portfolio for utilities and industries. With over 8,300 patents, Xylem continues to innovate, including a partnership with Gross-Wen Technologies to scale algal biofilm systems for nutrient recovery and carbon reduction.

Evoqua Water Technologies – Mission-Critical Industrial Water Services

Now integrated into Xylem, Evoqua remains a leader in industrial and municipal wastewater treatment. With 160 locations across 10 countries, it serves more than 38,000 customers worldwide. Evoqua recently launched a Sustainability and Innovation Hub in Pittsburgh, focusing on treating emerging contaminants such as PFAS, alongside filtration and reuse services for process and drinking water.

DuPont Water Solutions – Advanced Membrane Leader Driving Industrial Reuse

DuPont plays a crucial role in membrane-based wastewater services, with its FilmTec™ Fortilife™ membranes recognized for enabling high-efficiency water reuse. Winner of the BIG Sustainability Award in 2025, DuPont’s portfolio spans RO, NF, ultrafiltration, and ion exchange technologies, currently purifying over 50 million gallons per minute across 112 countries. Its strategy focuses on sustainable water circularity, carbon footprint reduction, and operational cost efficiency.

Wastewater Treatment Services Market Report Scope

Wastewater Treatment Services Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$72.5 Billion

|

|

Market Size (2034)

|

$132.2 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Service Type (Design & Engineering Services, Operation & Maintenance (O&M) Services, Installation & Commissioning Services, Consulting & Advisory Services, Analytical & Testing Services, Sludge Management & Disposal Services), By Treatment Type (Primary Treatment Services, Secondary Treatment Services, Tertiary Treatment Services, Advanced Treatment Services), By Service Delivery Model (Contractual Services, On-Demand Services, Build-Operate-Transfer (BOT) Services, Public-Private Partnership (PPP) Services), By End User Industry (Municipal Wastewater Utilities, Industrial Wastewater Treatment), By Ownership Model (Government-Owned Wastewater Treatment Services, Privately-Owned Wastewater Treatment Services, Third-Party Contracted Services)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia Environnement, SUEZ Worldwide, Xylem Inc, Evoqua Water Technologies LLC, Ecolab, Pentair PLC, Kurita Water Industries Ltd, VA Tech WABAG Ltd, DuPont, Aquatech International LLC, Thermax Limited, Kemira, Calgon Carbon, Toshiba Water Solutions, American Water Works Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Wastewater Treatment Services Market Segmentation

By Service Type

- Design & Engineering Services

- Operation & Maintenance (O&M) Services

- Installation & Commissioning Services

- Consulting & Advisory Services

- Analytical & Testing Services

- Sludge Management & Disposal Services

By Treatment Type

- Primary Treatment Services

- Secondary Treatment Services

- Tertiary Treatment Services

- Advanced Treatment Services

By Service Delivery Model

- Contractual Services

- On-Demand Services

- Build-Operate-Transfer (BOT) Services

- Public-Private Partnership (PPP) Services

By End User Industry

- Municipal Wastewater Utilities

- Industrial Wastewater Treatment

- Oil & Gas

- Chemicals & Petrochemicals

- Power Generation

- Food & Beverage

- Pharmaceuticals & Biotechnology

- Pulp & Paper

- Textile & Dyeing

- Mining & Metals

- Semiconductor & Electronics

By Ownership Model

- Government-Owned Wastewater Treatment Services

- Privately-Owned Wastewater Treatment Services

- Third-Party Contracted Services

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Wastewater Treatment Services Industry include-

- Veolia Environment

- SUEZ Worldwide

- Xylem Inc

- Evoqua Water Technologies LLC

- Ecolab

- Pentair PLC

- Kurita Water Industries Ltd

- VA Tech WABAG Ltd

- DuPont

- Aquatech International LLC

- Thermax Limited

- Kemira

- Calgon Carbon

- Toshiba Water Solutions

- American Water Works Company

*- List not Exhaustive

Research Coverage

This report investigates the global Wastewater Treatment Services Market, delivering analysis reviews of demand drivers, breakthrough digitalization, and service-model shifts that are reshaping compliance, reuse, and lifecycle economics. Produced by USDAnalytics, it highlights how O&M outsourcing, PPP/BOT delivery, energy-positive biosolids, and PFAS-ready advanced treatment are redefining utility and industrial strategies; it also maps value creation from smart sewer networks, resource recovery, and WTaaS offerings. With decision-grade sizing, case-led benchmarks, and risk/opportunity mapping across regions and end-user verticals, this report is an essential resource for utilities, industrial operators, EPCs, and investors planning capacity upgrades, retrofits, and long-term service contracts through 2034. Scope Includes-

- Segmentation

- By Service Type: Design & Engineering; Operation & Maintenance (O&M); Installation & Commissioning; Consulting & Advisory; Analytical & Testing; Sludge Management & Disposal.

- By Treatment Type: Primary; Secondary; Tertiary; Advanced Treatment Services.

- By Service Delivery Model: Contractual Services; On-Demand Services; Build-Operate-Transfer (BOT); Public-Private Partnership (PPP).

- By End User Industry: Municipal Wastewater Utilities; Industrial Wastewater (Oil & Gas; Chemicals & Petrochemicals; Power Generation; Food & Beverage; Pharmaceuticals & Biotechnology; Pulp & Paper; Textile & Dyeing; Mining & Metals; Semiconductor & Electronics).

- By Ownership Model: Government-Owned; Privately-Owned; Third-Party Contracted Services.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic/Forecast Horizon: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Analysis/profiles of 15+ companies): Veolia Environment; SUEZ Worldwide; Xylem Inc.; Evoqua Water Technologies LLC; Ecolab; Pentair PLC; Kurita Water Industries Ltd; VA Tech WABAG Ltd; DuPont; Aquatech International LLC; Thermax Limited; Kemira; Calgon Carbon; Toshiba Water Solutions; American Water Works Company.

Methodology

USDAnalytics applies a mixed top-down/bottom-up approach: we size demand by service type, treatment type, delivery model, end-user, ownership, and country, then triangulate with municipal budgets, industrial capex/opex, tariff structures, PPP/BOT pipelines, and regulatory timelines. Primary research includes structured interviews with utility managers, plant superintendents, O&M providers, OEMs, and EPCs to validate cost curves (CAPEX/OPEX), SLAs, uptime, energy intensity (kWh/m³), biosolids pathways, and reuse KPIs. Secondary inputs span permits, tender databases, corporate filings, and peer-reviewed literature, benchmarking advanced services for PFAS, nutrient removal, and digital twins. Scenario analyses stress-test sensitivities to energy prices, sludge disposal fees, discharge norms, drought frequency, and labor availability to produce robust 2025–2034 forecasts and margin/outlook bands.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Wastewater Treatment Services Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights: O&M Dominance, Industrial Share, and Asia-Pacific Leadership

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): USD 72.5 Billion

1.3.2. Projected Market Valuation (2034): USD 132.2 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 6.9%

2. Market Outlook (2025–2034)

2.1. Introduction: Market Value, CAGR, and Growth Drivers

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends Shaping the Wastewater Treatment Services Market

2.3.1. Public-Private Partnerships (PPPs) as a Growth Engine

2.3.2. Outsourcing and “Wastewater Treatment as a Service” (WTaaS)

2.3.3. Integration of Digital and Smart Technologies

2.3.4. Resource Recovery Transforming Waste into Revenue

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Key Developments (2024–2025)

3.1.1. DuPont Water Solutions Wins BIG Sustainability Award for Membrane Advancements (August 2025)

3.1.2. SUEZ and SIAAP Unveil France's Largest Biogas Unit at Seine Aval Plant (July 2025)

3.1.3. Strategic Acquisitions and Partnerships Define Competitive Landscape

3.1.4. Veolia and Kurita Drive Energy-Positive Wastewater Treatment

3.1.5. Advanced Membrane and Biosolids-to-Energy Innovations

4. Competitive Landscape: Leading Service Providers

4.1. Competitive Overview: Global Leaders and Specialized Innovators

4.2. Strategic Profiles of Key Companies

4.2.1. Veolia Water Technologies: Global Leader in Wastewater Services

4.2.2. SUEZ: End-to-End Wastewater Management with Digital Integration

4.2.3. Xylem Inc.: Full Water Cycle Solutions with a Focus on Innovation

4.2.4. Evoqua Water Technologies: Mission-Critical Industrial Water Services

4.2.5. DuPont Water Solutions: Advanced Membrane Leader Driving Industrial Reuse

5. Wastewater Treatment Services Market – Segmentation Insights

5.1. By Service Type

5.1.1. Operation & Maintenance (O&M) Services (35% Market Share)

5.1.2. Design & Engineering Services (25% Market Share)

5.1.3. Sludge Management (15% Market Share)

5.1.4. Other Services

5.2. By Treatment Type

5.2.1. Secondary Treatment Services (45% Market Share)

5.2.2. Tertiary/Advanced Treatment Services (30% Market Share)

5.2.3. Specialized Advanced Services (10% Market Share)

5.2.4. Primary Treatment Services

5.3. By Service Delivery Model

5.3.1. Contractual Services (40% Market Share)

5.3.2. Public-Private Partnership (PPP) Models (25% Market Share)

5.3.3. On-Demand Services (20% Market Share)

5.3.4. Build-Operate-Transfer (BOT) Services (15% Market Share)

5.4. By End User Industry

5.4.1. Municipal Wastewater Utilities

5.4.2. Industrial Wastewater Treatment

5.5. By Ownership Model

5.5.1. Government-Owned Services

5.5.2. Privately-Owned Services

5.5.3. Third-Party Contracted Services

6. Country Analysis: Wastewater Treatment Services Market

6.1. China: Regulatory Enforcement and Technological Innovation

6.2. United States: Infrastructure Upgrades and Regulatory Push

6.3. India: National Missions and PPP Models Accelerate Services

6.4. Germany: Advanced Standards and Technology Adoption Lead Europe’s Market

6.5. Saudi Arabia: Vision 2030 and Large-Scale ISTPs Boost Service Market

6.6. Japan: Membrane Technology Leadership and MBR Adoption Propel Market

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Market Outlook

7.1.1. By Service Type

7.1.2. By Treatment Type

7.1.3. By End-User Industry

7.2. Europe Market Outlook

7.2.1. By Service Type

7.2.2. By Treatment Type

7.2.3. By End-User Industry

7.3. Asia Pacific Market Outlook

7.3.1. By Service Type

7.3.2. By Treatment Type

7.3.3. By End-User Industry

7.4. South America Market Outlook

7.4.1. By Service Type

7.4.2. By Treatment Type

7.4.3. By End-User Industry

7.5. Middle East & Africa Market Outlook

7.5.1. By Service Type

7.5.2. By Treatment Type

7.5.3. By End-User Industry

8. Company Profiles: Leading Players

8.1. Veolia Environment

8.2. SUEZ Worldwide

8.3. Xylem Inc.

8.4. Evoqua Water Technologies LLC

8.5. Ecolab

8.6. Pentair PLC

8.7. Kurita Water Industries Ltd.

8.8. VA Tech WABAG Ltd.

8.9. DuPont

8.10. Aquatech International LLC

8.11. Thermax Limited

8.12. Kemira

8.13. Calgon Carbon

8.14. Toshiba Water Solutions

8.15. American Water Works Company

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures