Global Sludge Management and Dewatering Market Overview

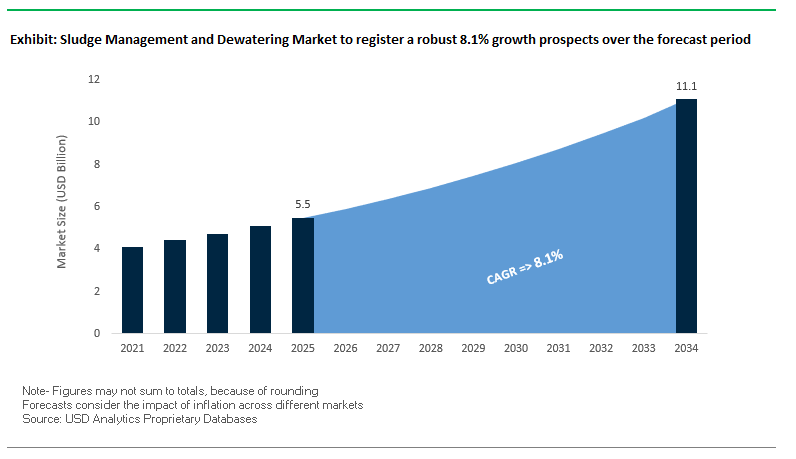

The global sludge management and dewatering market is poised for significant growth, with the market value projected to rise from $5.5 billion in 2025 to $11.1 billion by 2034, registering a robust CAGR of 8.1%. This growth is being driven by the increasing volumes of municipal and industrial wastewater, coupled with the pressing need for sustainable and efficient sludge management solutions. As urbanization and industrialization accelerate globally, wastewater generation continues to surge, creating a critical demand for advanced dewatering and sludge treatment technologies.

Regulatory compliance is another key driver shaping the market landscape. Governments worldwide, including India, have implemented stringent discharge limits, compelling municipalities and industries to adopt innovative sludge management practices. Technological advancements not only improve operational efficiency but also enable significant cost reduction, with dewatering processes capable of reducing sludge volume by 70–90%, leading to lower transportation and disposal expenses.

Moreover, the market is increasingly aligned with sustainability and resource recovery initiatives. Techniques such as anaerobic digestion and advanced sludge drying are enabling the conversion of waste into valuable biogas or energy-recoverable material.

Key Insights for Industry Stakeholders:

- Municipal and industrial wastewater volumes are driving demand for scalable dewatering solutions.

- Stricter environmental regulations are enforcing the adoption of advanced sludge management systems.

- Effective sludge dewatering reduces disposal costs by 60–80%, enhancing operational efficiency.

- Technologies like anaerobic digestion support biogas production and resource recovery.

- Growing focus on circular economy principles is shaping investment in sludge treatment innovations.

Market Analysis: Recent Developments in Sludge Management and Dewatering

The sludge management and dewatering market has seen several strategic moves and technological innovations in recent years. In May 2025, Pelagia, a leading aquaculture solutions provider, acquired Fjord Solutions, a supplier of aquaculture equipment. This acquisition under Pelagia's Blue Ocean Technology brand enhances its sludge and water treatment offerings, particularly in sustainable aquaculture applications.

In April 2025, the Los Angeles Department of Water and Power announced a major investment in a new wastewater treatment facility. This initiative aims to modernize aging infrastructure with state-of-the-art sludge management technologies to improve operational efficiency and ensure compliance with future regulations. Earlier, in August 2024, Japanese pump manufacturer Tsurumi launched an improved KRD series of heavy-duty dewatering pumps. Designed for abrasive sludge and slurry handling, these pumps deliver higher power and durability for municipal and industrial applications.

Key acquisitions and regulatory opportunities have also shaped the market. In November 2023, U.S.-based Synagro acquired New England Fertilizer Co. to expand biosolids processing capabilities and strengthen sustainable waste management. In October 2023, the U.S. International Trade Administration highlighted opportunities for U.S. companies in India's growing environmental sludge management sector, reflecting increased investment in wastewater infrastructure.

Smaller-scale innovations have also emerged, with Sulzer launching a new line of dewatering pumps in September 2022, catering to compact and efficient operations. Additionally, reports by NFSSMA and NITI Aayog in August 2022 highlighted successful business models for faecal sludge and septage management (FSSM) in Indian cities, emphasizing private sector participation and technological innovation. The regulatory backbone was further reinforced in June 2021, when the Supreme Court of India upheld the NGT’s stricter discharge limits from 2019, accelerating the adoption of advanced sludge dewatering solutions.

Key Market Trends Shaping Sludge Management and Dewatering

Regulatory Pressure Accelerates Adoption of Advanced Dewatering

The sludge management and dewatering market is being strongly influenced by stricter environmental regulations and discharge limits, with bodies like India’s Central Pollution Control Board (CPCB) and National Green Tribunal (NGT) enforcing tighter standards. Municipal and industrial facilities are compelled to adopt advanced dewatering technologies to reduce sludge volume and comply with evolving limits. Global case studies, such as a municipal solid waste incinerator in the Czech Republic, highlight the economic and operational incentives of optimizing sludge handling, where excessive sludge volumes previously incurred high off-site disposal costs, pushing adoption of efficient mechanical and thermal systems.

Emergence of Advanced Mechanical and Thermal Technologies

Technological innovations are redefining sludge treatment, with electrokinetic dewatering, thermal hydrolysis, and high-efficiency drying systems becoming increasingly mainstream. Academic research in 2024 underscores electrokinetic methods as delivering drier final sludge, while thermal hydrolysis enhances digestibility for biogas generation. These technologies enable operators to balance energy use with operational efficiency, reduce transportation costs, and produce higher-quality byproducts, demonstrating a shift from simple volume reduction to integrated resource recovery.

Resource Recovery and Energy Generation as Growth Drivers

Sludge is increasingly recognized as a resource rather than a waste, with biogas and fertilizer production becoming critical value streams. Companies such as Gills Onions report annual savings of approximately US$700,000 by generating energy from wastewater sludge. Municipal initiatives, like the Greater Lawrence Sanitary District in Massachusetts, invest in additional digesters to co-process food waste and sludge, generating up to 3.2 MW of electricity while producing biosolids for sale. This trend highlights a clear opportunity for municipalities and industries to transform sludge management into profitable, self-sustaining operations aligned with circular economy principles.

Market Opportunities in Sludge Management

The sludge management market offers significant opportunities for service providers and technology developers to expand in advanced dewatering, thermal processing, energy recovery, and automation. Growing regulatory pressure, rising sludge volumes, and increased focus on sustainable resource recovery create demand for integrated systems that combine mechanical, chemical, and thermal processes. Providers that can offer predictable operational performance, reduced disposal costs, and renewable energy generation are well-positioned to capture market share in both municipal and industrial sectors, making sludge management a strategic growth area in water and wastewater treatment.

Market Share Analysis of Sludge Management and Dewatering

Dewatering and Pre-Treatment Lead Market Share by Technology

By treatment technology, dewatering dominates with 32.8% share, as it is the critical mechanical step that significantly reduces sludge volume, lowering transportation and disposal costs. Thickening & Conditioning (22.5%) is essential as a pre-treatment step to optimize downstream dewatering efficiency through polymer conditioning. Drying & Digestion (20.9%) provides added value by stabilizing sludge and enabling biogas production, while Advanced & Thermal Treatments (16.9%) such as incineration, gasification, and pyrolysis cater to regions with strict disposal regulations, delivering maximum volume reduction, pathogen destruction, and energy recovery, reflecting the market’s strong push toward resource recovery and circular economy integration.

Municipal Sludge Drives Market While Industrial Sludge Offers High-Value Opportunities

By sludge type, municipal sludge commands 64.3% of the market, driven by the consistent, high-volume production from urban wastewater plants worldwide. Industrial sludge (35.7%), while smaller, presents high-value and complex treatment challenges due to hazardous compounds and variable composition. This segment requires specialized handling, pre-treatment, and disposal solutions, making it a lucrative niche for advanced dewatering, digestion, and thermal treatment technologies that can safely and efficiently process diverse industrial waste streams.

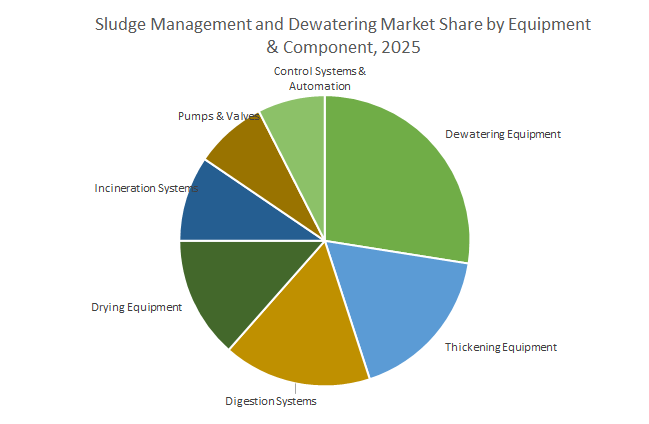

Dewatering Equipment and Automation Lead Capital Investment by Component

In terms of equipment and components, dewatering equipment (26.9%) represents the largest market segment, encompassing centrifuges, belt presses, and screw presses that are essential for almost all sludge streams. Thickening equipment (16.9%) and digestion systems enable volume reduction and resource recovery, while drying equipment (13.2%) and incineration systems serve high-capex, regulatory-driven applications. Pumps & valves and control systems & automation are critical for handling abrasive sludge and optimizing operational efficiency, with automation emerging as a fast-growing segment due to its ability to reduce energy and polymer consumption, enhancing overall cost-effectiveness.

Full-Service Outsourcing Dominates Market Share by Service

By service type, treatment & disposal services lead with 35.7%, reflecting the trend of outsourcing entire sludge management responsibilities to specialized providers, transferring regulatory and operational risk. Operation & Maintenance services (26.9%) ensure high uptime and optimal equipment performance without requiring in-house expertise, while transportation & handling (22.5%) addresses the high costs of moving sludge from generation to treatment sites. Consulting & Engineering services (11.8%) play a strategic role in planning, designing, and upgrading facilities with advanced technologies such as thermal hydrolysis and anaerobic digestion, ensuring compliance and long-term operational efficiency.

China: Driving High-Volume Sludge Treatment and Resource Recovery

China’s sludge management and dewatering market is primarily driven by stringent regulatory policies, substantial infrastructure investments, and technological innovation. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge standards, with a 2022 plan aiming for over 90% harmless disposal of urban sludge by 2025. To achieve this, the government is heavily investing in wastewater treatment infrastructure, including new harmless sludge disposal facilities with daily capacities of 20,000 metric tons or more. Technological advancements such as anaerobic digestion, thermal hydrolysis, and hydrothermal carbonization are being promoted to enable resource recovery and reduce sludge volumes efficiently. The market is strongly propelled by applications in high-organic-load wastewater treatment from industries including food and beverage, pulp and paper, and pharmaceuticals, where sludge conversion to renewable biogas represents a dual environmental and economic benefit.

United States: Modernization and PFAS-Driven Investment in Sludge Dewatering

In the United States, the sludge management and dewatering market is growing due to government funding, regulatory mandates, and corporate initiatives. The Bipartisan Infrastructure Law (BIL) provides over $50 billion through the EPA to modernize water infrastructure, which includes upgrading sludge dewatering facilities. Regulatory focus on limiting PFAS discharges has increased demand for advanced sludge management solutions as a critical first step in treating complex wastewater streams. Corporate innovations are exemplified by the Los Angeles Department of Water and Power’s 2024 investment in sludge management projects, alongside capabilities expanded through the 2023 Xylem-Evoqua merger. Key applications include treating wastewater from food and beverage industries and converting organic waste into renewable biogas, supporting energy self-sufficiency and sustainable operations.

India: Government Programs and Hybrid Annuity Models Fuel Market Expansion

India’s sludge management and dewatering market is expanding through government initiatives, infrastructure investments, corporate projects, and technological advancements. Programs such as Jal Jeevan Mission, Namami Gange, and Swachh Bharat Mission-Urban 2.0 drive adoption of municipal and industrial wastewater solutions. The National Mission for Clean Ganga (NMCG) introduced the Hybrid Annuity Model (HAM) to fund new sewage treatment projects, with significant investment directed toward STP capacity, including dewatering units. Leading Indian companies like VA Tech Wabag specialize in large-scale anaerobic sludge processes. Technological collaborations, such as Ion Exchange (India) Ltd.’s 2024 agreement with TERI to commercialize patented photocatalytic oxidation processes, demonstrate the integration of advanced treatment technologies with sludge management solutions.

Germany: Advanced Regulations and Digitalization Enhance Sludge Treatment Efficiency

Germany’s market for sludge management and dewatering is shaped by stricter EU regulations, technological advancements, and corporate innovation. The revised EU Urban Wastewater Treatment Directive (January 2025) mandates expansion to a “4th purification stage” to remove micropollutants, prompting adoption of advanced sludge treatment methods that reduce load on these systems. German cities are leveraging AI, digital twins, and advanced monitoring to optimize water management and enhance anaerobic digestion efficiency. Companies such as H2O GmbH and GEA Group AG are at the forefront of developing sustainable, service-based sludge solutions, integrating Zero Liquid Discharge (ZLD) and other innovative approaches for industrial wastewater management.

United Kingdom: Regulatory Compliance and Strategic Investments Drive Growth

The United Kingdom’s sludge management and dewatering market benefits from government frameworks, stringent regulations, and substantial investment. The Water Industry National Environment Programme (WINEP) outlines environmental obligations for water companies, allocating £22.1 billion to asset improvements, including sludge management projects. Regulatory requirements focus on minimizing the use of sewage sludge in agriculture and controlling toxic chemicals and heavy metals in applied sludge. WINEP investments include phosphorous reduction and storm overflow mitigation, reinforcing the demand for advanced sludge dewatering technologies. Key applications involve sustainable wastewater management, regulatory compliance, and minimizing environmental impact from sludge disposal.

Japan: Innovation in Resource Recovery and Advanced Membrane Technologies

Japan’s sludge management and dewatering market is driven by government-led initiatives, technological advancement, and corporate R&D. The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) leads the B-DASH project, targeting next-generation sewage sludge solid fuel production and efficient conversion of sludge into fertilizers and fuels. Technological innovations include phosphorus recovery rates of 40% and volume reduction of dewatered sludge by 3.3% in Kobe City facilities. Corporations like Toray Industries Inc. provide advanced membrane technologies, widely applied in anaerobic membrane bioreactors (AnMBRs), facilitating enhanced sludge dewatering and energy recovery. The market is fueled by applications in municipal wastewater treatment, industrial sludge processing, and sustainable resource recovery strategies.

Competitive Landscape of Sludge Management and Dewatering Market

The global sludge management and dewatering market is highly competitive, with leading players focusing on technology innovation, operational efficiency, and sustainable solutions. Companies are investing in advanced equipment and integrated services to meet the rising demand for efficient sludge processing.

Veolia Environnement S.A.: Global Leader in Integrated Sludge Solutions

Veolia Environnement is a global leader in optimized resource management, offering an extensive range of sludge treatment and valorization technologies. Its advanced anaerobic digestion processes enable biogas production while reducing sludge volume. Key offerings include the BioCon™ sludge dryer, delivering high dewatering rates and supporting cost-efficient operations. Strategically, Veolia leverages digital solutions through its Hubgrade platform, optimizing sludge management processes with real-time data and expert analysis. The company has demonstrated capabilities in large-scale municipal projects, including Lille Métropole's integrated fixed-film activated sludge plant, reinforcing its market dominance in municipal wastewater management.

Andritz AG: Expert in Mechanical Dewatering Technologies

Andritz AG specializes in mechanical dewatering solutions with a strong portfolio of decanter centrifuges, belt presses, and screw presses. These systems handle diverse sludge compositions across municipal and industrial sectors. Continuous investment in R&D allows Andritz to enhance energy efficiency and automation, providing clients with low-maintenance, high-performance solutions. Its dewatering equipment integrates seamlessly into broader wastewater treatment systems, positioning Andritz as a critical partner for municipalities and industrial plants seeking efficient and reliable sludge processing technologies.

Alfa Laval AB: High-Efficiency Dewatering and Separation Solutions

Alfa Laval is globally recognized for separation and fluid handling technologies. Its decanter centrifuges deliver superior separation efficiency, producing high-solid-content sludge cakes. The company emphasizes energy-efficient and automated solutions, reducing operational costs for end-users. Alfa Laval’s innovations cater to specialized industrial sectors, including food, beverage, and chemicals, where sludge presents unique processing challenges.

Hitachi Zosen Corporation: Transforming Sludge into Energy

Hitachi Zosen provides comprehensive sludge management solutions with a focus on thermal treatment and energy recovery. Its technologies enable dewatering and incineration, converting waste into energy in line with circular economy principles. The company’s projects span wastewater treatment and waste-to-energy plants, showcasing its ability to deliver end-to-end solutions that maximize resource recovery while ensuring environmental compliance.

Evoqua Water Technologies: Integrated Dewatering Innovations

Evoqua Water Technologies is a leading provider of innovative water and wastewater solutions. Its Envirex Belt Press is renowned for high throughput and enhanced sludge conditioning. Evoqua continuously introduces automated and water-efficient models, addressing evolving municipal and industrial requirements. Recent innovations focus on achieving drier sludge cakes and lower disposal costs, solidifying Evoqua’s position as a key player in the global sludge dewatering market.

Sludge Management and Dewatering Market Report Scope

Sludge Management and Dewatering Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.5 Billion

|

|

Market Size (2034)

|

$11.1 Billion

|

|

Market Growth Rate

|

8.1%

|

|

Segments

|

By Treatment Technology (Thickening & Conditioning, Dewatering, Drying & Digestion, Advanced & Thermal Treatment), By Sludge Type (Municipal Sludge, Industrial Sludge), By Equipment & Component (Dewatering Equipment, Thickening Equipment, Drying Equipment, Digestion Systems, Incineration Systems, Control Systems & Automation, Pumps & Valves), By Service (Treatment & Disposal Services, Operation & Maintenance Services, Transportation & Handling Services, Consulting & Engineering Services), By End-Use & Disposal Method (Recovery & Reuse, Disposal), By End-User (Municipalities, Industrial Facilities, Commercial Establishments)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, Alfa Laval, Andritz AG, DuPont de Nemours, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. Tech Wabag Ltd., Mitsubishi Chemical Corporation, Kurita Water Industries Ltd., H2O GmbH, Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Sludge Management and Dewatering Market Segmentation

By Treatment Technology

- Thickening & Conditioning

- Dewatering

- Drying & Digestion

- Advanced & Thermal Treatment

By Sludge Type

- Municipal Sludge

- Industrial Sludge

- Oil & Gas

- Chemical & Petrochemical

- Food & Beverage

- Pulp & Paper

- Textile

- Metal Processing

By Equipment & Component

- Dewatering Equipment

- Thickening Equipment

- Drying Equipment

- Digestion Systems

- Incineration Systems

- Control Systems & Automation

- Pumps & Valves

By Service

- Treatment & Disposal Services

- Operation & Maintenance Services

- Transportation & Handling Services

- Consulting & Engineering Services

By End-Use & Disposal Method

- Recovery & Reuse

- Disposal

By End-User

- Municipalities

- Industrial Facilities

- Commercial Establishments

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Sludge Management and Dewatering Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- Alfa Laval

- Andritz AG

- DuPont de Nemours, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. Tech Wabag Ltd.

- Mitsubishi Chemical Corporation

- Kurita Water Industries Ltd.

- H2O GmbH

- Thermax Limited

*- List not Exhaustive

Research Coverage – USDAnalytics

This report investigates the Global Sludge Management and Dewatering Market, highlighting how rising wastewater volumes, stricter discharge norms, and resource-recovery imperatives are reshaping strategies from mere volume reduction to value extraction. It analyzes breakthroughs in electrokinetic dewatering, thermal hydrolysis, high-efficiency drying, and automation, and reviews recent investments, acquisitions, and policy shifts that are accelerating adoption across municipalities and industry. The study highlights cost advantages from achieving 70–90% volume cuts and energy gains from digestion-driven biogas, while mapping where advanced mechanical and thermal systems deliver the sharpest OPEX savings. With segment-specific demand signals and region-wise compliance trajectories, this report is an essential resource for utilities, EPCs, plant operators, and investors seeking defensible, regulation-ready sludge strategies, backed by USDAnalytics’ market sizing, technology benchmarking, and competitive analysis reviews. Scope Includes-

- By Treatment Technology: Thickening & Conditioning; Dewatering; Drying & Digestion; Advanced & Thermal Treatment (incineration, gasification, pyrolysis)

- By Sludge Type: Municipal; Industrial (Oil & Gas; Chemical & Petrochemical; Food & Beverage; Pulp & Paper; Textile; Metal Processing)

- By Equipment & Component: Dewatering Equipment; Thickening Equipment; Drying Equipment; Digestion Systems; Incineration Systems; Control Systems & Automation; Pumps & Valves

- By Service: Treatment & Disposal Services; Operation & Maintenance Services; Transportation & Handling Services; Consulting & Engineering Services

- By End-Use & Disposal Method: Recovery & Reuse; Disposal

- By End-User: Municipalities; Industrial Facilities; Commercial Establishments

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Time Frame: Historic data from 2021–2024 and forecast data from 2025–2034.

- Companies (Analysis/ profiles of 15+ companies, include the list of given companies): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; Alfa Laval; Andritz AG; DuPont de Nemours, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. Tech Wabag Ltd.; Mitsubishi Chemical Corporation; Kurita Water Industries Ltd.; H2O GmbH; Thermax Limited.

Methodology

USDAnalytics employs a bottom-up market model triangulated with vendor shipments, installed base, and procurement pipelines, layered with top-down validation using municipal budgets, industrial CAPEX/OPEX, and disposal tariff benchmarks. Primary research spans interviews with utility managers, biosolids coordinators, OEMs, polymer suppliers, and O&M contractors, complemented by secondary reviews of regulatory rulings, tender awards, and technology white papers. Forecasts (2025–2034) incorporate scenario weights for regulation tightening, landfill gate-fee inflation, energy prices, and polymer/chemical cost curves. Technology learning rates (centrifuges, belt/screw presses, thermal hydrolysis, dryers) are embedded to capture efficiency gains, while sensitivity tests quantify impacts of sludge cake %TS, haul distances, and co-digestion rates on payback and TCO.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Sludge Management and Dewatering Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Sludge Management and Dewatering Market Outlook (2025–2034)

2.1. Introduction: From Waste Disposal to Resource Recovery

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $5.5 Billion

2.2.2. Forecasted Market Size (2034): $11.1 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 8.1%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Increasing Wastewater Volumes, Regulatory Compliance, and Sustainability Goals

2.3.2. Challenges: High Capital Costs and Complex Sludge Characteristics

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments (2024–2025)

3.1. Market Trend: The Shift from Volume Reduction to Resource Recovery

3.2. Market Trend: Emergence of Advanced Technologies

3.3. Recent Developments & Strategic Moves

4. Sludge Management and Dewatering Market – Segmentation Insights (2025–2034)

4.1. By Treatment Technology

4.1.1. Dewatering

4.1.2. Thickening & Conditioning

4.1.3. Drying & Digestion

4.1.4. Advanced & Thermal Treatment

4.2. By Sludge Type

4.2.1. Municipal Sludge

4.2.2. Industrial Sludge

4.3. By Equipment & Component

4.3.1. Dewatering Equipment

4.3.2. Thickening Equipment

4.3.3. Drying Equipment

4.3.4. Digestion Systems

4.3.5. Incineration Systems

4.3.6. Control Systems & Automation

4.3.7. Pumps & Valves

4.4. By Service

4.4.1. Treatment & Disposal Services

4.4.2. Operation & Maintenance Services

4.4.3. Transportation & Handling Services

4.4.4. Consulting & Engineering Services

4.5. By End-Use & Disposal Method

4.5.1. Recovery & Reuse

4.5.2. Disposal

4.6. By End-User

4.6.1. Municipalities

4.6.2. Industrial Facilities

4.6.3. Commercial Establishments

5. Country Analysis and Outlook: Sludge Management and Dewatering Market

5.1. United States: Modernization and PFAS-Driven Investment

5.2. China: High-Volume Treatment and Regulatory Enforcement

5.3. India: Government Programs and Hybrid Annuity Models

5.4. Germany: Advanced Regulations and Digitalization

5.5. United Kingdom: Regulatory Compliance and Strategic Investments

5.6. Japan: Innovation in Resource Recovery and Membranes

5.7. Other Countries Analyzed

5.7.1. North America (Canada, Mexico)

5.7.2. Europe (Spain, Italy, Russia, Rest of Europe)

5.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

5.7.4. South America (Brazil, Argentina, Rest of South America)

5.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

6. Market Size Outlook by Region (2025-2034)

6.1. North America Sludge Management and Dewatering Market Size Outlook to 2034

6.1.1. By Treatment Technology

6.1.2. By Sludge Type

6.1.3. By Equipment & Component

6.1.4. By Service

6.1.5. By End-Use & Disposal Method

6.1.6. By End-User

6.1.7. By Country (U.S., Canada, Mexico)

6.2. Europe Sludge Management and Dewatering Market Size Outlook to 2034

6.2.1. By Treatment Technology

6.2.2. By Sludge Type

6.2.3. By Equipment & Component

6.2.4. By Service

6.2.5. By End-Use & Disposal Method

6.2.6. By End-User

6.2.7. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Sludge Management and Dewatering Market Size Outlook to 2034

6.3.1. By Treatment Technology

6.3.2. By Sludge Type

6.3.3. By Equipment & Component

6.3.4. By Service

6.3.5. By End-Use & Disposal Method

6.3.6. By End-User

6.3.7. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Sludge Management and Dewatering Market Size Outlook to 2034

6.4.1. By Treatment Technology

6.4.2. By Sludge Type

6.4.3. By Equipment & Component

6.4.4. By Service

6.4.5. By End-Use & Disposal Method

6.4.6. By End-User

6.4.7. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Sludge Management and Dewatering Market Size Outlook to 2034

6.5.1. By Treatment Technology

6.5.2. By Sludge Type

6.5.3. By Equipment & Component

6.5.4. By Service

6.5.5. By End-Use & Disposal Method

6.5.6. By End-User

6.5.7. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Company Profiles: Leading Players

7.1. Veolia Environnement S.A.

7.2. Andritz AG

7.3. Alfa Laval AB

7.4. Hitachi Zosen Corporation

7.5. Evoqua Water Technologies LLC (a Xylem company)

7.6. SUEZ

7.7. Other Key Players

7.7.1. DuPont de Nemours, Inc.

7.7.2. Aquatech International

7.7.3. Kubota Corporation

7.7.4. The Dow Chemical Company

7.7.5. V.A. Tech Wabag Ltd.

7.7.6. Mitsubishi Chemical Corporation

7.7.7. Kurita Water Industries Ltd.

7.7.8. H2O GmbH

7.7.9. Thermax Limited

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures