Municipal Water Treatment Equipment Market Size, Growth Trends, and Strategic Imperatives (2025–2034)

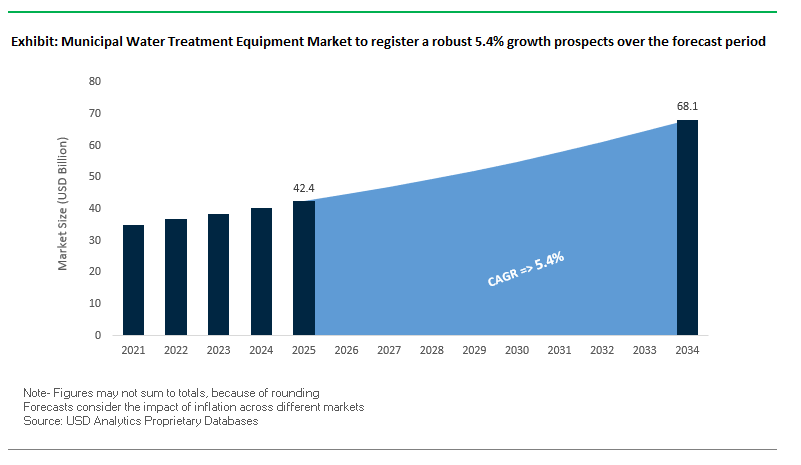

The municipal water treatment equipment market is projected to grow from $42.4 billion in 2025 to $68.1 billion by 2034, reflecting a CAGR of 5.4%. The steady growth is fueled by tightening water quality regulations, increasing urbanization, and technological innovations in advanced treatment systems.

A critical driver is the enforcement of stricter environmental standards such as the revised EU Urban Wastewater Treatment Directive, mandating the removal of micropollutants like PFAS and pharmaceutical residues. The has accelerated the adoption of tertiary and quaternary treatment technologies across Europe and beyond. In parallel, water-scarce regions such as Chennai, India, are setting global benchmarks for water reuse recycling to over 20% of treated water and spurring demand for membrane filtration and reverse osmosis systems.

Smart water infrastructure is also transforming the market. Municipalities are investing in IoT-enabled grids, real-time sensors, and AI-driven analytics to detect leaks, optimize treatment processes, and extend asset life. Additionally, rapid population growth in emerging economies is driving capacity expansions in cities like Ahmedabad, India, and Chongqing, China, creating lucrative opportunities for equipment manufacturers.

Strategic Imperatives for Stakeholders:

- Invest in micropollutant removal technologies to stay ahead of regulatory requirements.

- Focus on water reuse and recycling solutions for regions facing water scarcity.

- Integrate digital monitoring and predictive analytics into product offerings.

- Target urban infrastructure expansion projects in high-growth markets.

Market Analysis: Key Developments and Growth Catalysts

The municipal water treatment equipment sector has witnessed a series of strategic expansions, partnerships, and regulatory-driven upgrades in the past three years, directly influencing market competitiveness.

In August 2025, Veolia partnered with Brazilian authorities to design and implement the country’s most advanced municipal wastewater reuse system in Vitória. Using membrane bioreactors (MBR) and reverse osmosis (RO), the facility will process 450 liters per second of wastewater for industrial reuse, freeing freshwater resources for nearly 200,000 residents. The same month, the Ahmedabad Municipal Corporation in India announced capacity expansions for its Jaspur and Raska plants, adding a 200 MLD unit and planning an additional 400 MLD plant, demonstrating the urgent need for infrastructure upgrades in urban centers.

Earlier, in October 2024, SUEZ secured a €4.5 million contract to retrofit Denmark’s Hillerød wastewater facility with inline ozonation and granular activated carbon (GAC) filtration to meet new EU micropollutant standards. The move aligns with its broader strategy of tackling emerging contaminants. In July 2024, Xylem committed $50 million to climate-focused startups, prioritizing water scarcity and quality innovations.

Notably, in September 2023, SUEZ partnered with Chongqing Water Group to build and operate a 400,000 m³/day water treatment plant, strengthening supply for 3.3 million residents. Similarly, the City of DuPont, Washington, recently completed two PFAS treatment facilities using GAC filtration, funded by $7.3 million in grants, showcasing the rising importance of contaminant-specific solutions in municipal water treatment.

Trends and Opportunities in Municipal Water Treatment Equipment Market

Trend 1: Smart Water Infrastructure with AI-Driven Optimization

Municipal water treatment is rapidly transitioning toward smart, AI-driven water infrastructure. IoT-enabled sensors and AI platforms allow municipalities to monitor water networks in real-time, predict equipment failures, and optimize resource allocation. The digital transformation results in substantial operational savings and enhanced service reliability. For example, a wastewater treatment plant in Italy achieved a 19% reduction in energy consumption within 1-2 years by implementing AI-based optimization, primarily through precise control of energy-intensive aeration processes. Predictive maintenance enabled by AI reduces unplanned downtimes, extends equipment life, and ensures uninterrupted water supply. Furthermore, real-time adjustments to chemical dosing and treatment processes improve water quality, ensuring compliance with regulatory standards and promoting public health. The integration of AI thus transforms municipal water operations into more efficient, resilient, and cost-effective systems.

Trend 2: Advanced Nutrient Removal for Stricter Regulations

Increasingly stringent regulations are driving municipalities to adopt advanced nutrient removal technologies to mitigate nitrogen and phosphorus pollution. Conventional wastewater treatment may struggle to meet low limits, such as total phosphorus below 0.3 mg/L and total nitrogen below 5 mg/L, without significantly increasing operational costs. Biological nutrient removal (BNR) processes, including simultaneous nitrification and denitrification (SND), provide cost-effective alternatives with lower oxygen and energy requirements. Anammox technology, which requires less energy and produces less sludge, is emerging as another innovative approach. Membrane bioreactors (MBRs) combine biological treatment with membrane filtration, offering compact systems that achieve high nutrient removal efficiency and significantly reduce the footprint compared to traditional setups. These technologies enable municipalities to comply with regulations while optimizing energy and operational efficiency.

Opportunity 1: PFAS Removal Mandates Driving Upgrades

The U.S. Environmental Protection Agency (EPA) has finalized enforceable standards for six PFAS compounds, creating an immediate demand for municipal water treatment upgrades. Utilities must implement advanced treatment technologies, including granular activated carbon (GAC), anion exchange resins, and reverse osmosis, to comply with maximum contaminant levels (MCLs) for PFOA and PFOS. Approximately 100 million people in the U.S. will benefit from reduced PFAS exposure, and municipalities have a three-year window for monitoring and five years for system upgrades. The Bipartisan Infrastructure Law allocates $21 billion for water quality improvements, including $1 billion specifically for PFAS compliance, ensuring financial feasibility for municipalities. The regulatory push presents a clear and substantial market opportunity for water treatment equipment manufacturers specializing in PFAS removal solutions.

Opportunity 2: Climate-Resilient Decentralized Systems

Decentralized water treatment systems are gaining traction as municipalities seek climate-resilient strategies to address droughts, floods, and urban water security challenges. Localized systems, including rainwater harvesting, retention, and reuse, reduce pressure on centralized networks while providing reliable water supplies. Cities like Almere in the Netherlands are leveraging decentralized systems to mitigate flood risk, while Mexico City’s Rainwater Harvesting Program aims to install 100,000 systems, providing peri-urban communities with sustainable water sources. Decentralized solutions also lower infrastructure costs and energy consumption associated with large-scale plants, enabling municipalities to achieve flexible, adaptive, and sustainable water management. These systems are emerging as a long-term strategic opportunity for water treatment providers.

Municipal Water Treatment Equipment Market Share Insights

By Treatment Stage: Secondary Treatment Dominates, Tertiary Processes Accelerate

Secondary treatment accounts for nearly 31.3% of the municipal water treatment equipment market by 2025, cementing its role as the biological core of wastewater management. Activated sludge systems and membrane bioreactors (MBR) remain the cornerstone, especially in urban centers managing nutrient-heavy sewage streams. Meanwhile, tertiary treatment is the fastest-growing stage, driven by stricter effluent quality standards and water reuse mandates. Sand filtration, UV disinfection, and advanced micropollutant removal are fueling the segment’s rapid expansion, making it a growth engine for municipal utilities globally.

By Equipment Type: Pumps, Membranes, and Smart Systems Driving Investments

Pumps and valves hold around 21.3% of the global municipal water treatment equipment market, reflecting their indispensable role as the “circulatory system” moving water and wastewater across plants. Alongside, filter media and membranes are a high-value category, with microfiltration, ultrafiltration, and RO membranes powering both drinking water purification and wastewater reuse. Equally critical is the rise of control and monitoring systems, where SCADA, sensors, and IoT platforms transform utilities into “smart plants,” enabling predictive maintenance, remote operation, and real-time regulatory compliance.

.png)

By Plant Capacity: Mid-Sized Plants as the Global Sweet Spot

Plants with a capacity of 10–100 MLD represent around 45% of the municipal water treatment market, making them the sweet spot for mid-sized cities and regional hubs. These plants balance scale with replicability, creating a high number of projects globally. On the higher end, megaproject plants exceeding 100 MLD capture about 30% of market share, reflecting the scale of investment needed to serve major metropolitan populations. These facilities are highly customized, capital-intensive, and often at the center of urban water resilience strategies.

By Technology Type: Conventional Dominates, Membrane and AOPs Gain Ground

Conventional treatment processes hold nearly 48.9% of the municipal water treatment equipment market, underscoring the entrenched use of coagulation, sedimentation, sand filtration, and activated sludge in legacy plants. However, membrane-based systems are rapidly scaling, particularly in water reuse projects and advanced drinking water plants, where they deliver superior effluent quality. Advanced oxidation processes (AOPs), though still at 10.6%, represent a fast-emerging niche, targeting pharmaceutical residues, pesticides, and persistent organics that traditional systems cannot address.

By Water Source: Surface Water as the Primary Focus, Wastewater Gaining Strategic Value

Surface water treatment accounts for about 51.2% of global municipal water treatment investments, as rivers, lakes, and reservoirs remain the main supply source for large urban populations. However, wastewater treatment has become a critical parallel segment, driven not only by compliance but also by municipal water reuse initiatives. Increasingly, cities are converting treated sewage into a strategic water resource for industrial, agricultural, and even indirect potable applications, positioning wastewater reuse as a central pillar of long-term urban resilience.

By Application: Drinking Water Leads, Reuse as the Strategic Future

Drinking water treatment represents roughly 45% of the municipal water treatment equipment market, reaffirming its role as the fundamental public health mandate for cities worldwide. Wastewater treatment follows closely at 40.6%, evolving beyond pollution control to include energy and nutrient recovery strategies. Meanwhile, water reuse is the fastest-growing application, as cities shift from linear supply models to circular water economies, leveraging treated effluent for irrigation, industrial cooling, and even potable augmentation in drought-prone regions.

By Automation Level: Fully Automated Systems Define the Standard

Fully automated systems dominate with nearly 70.6% of municipal water treatment plants globally, underscoring their role as the unquestionable standard for new builds. SCADA and AI-driven automation platforms enable utilities to optimize energy consumption, reduce chemical costs, and ensure real-time compliance with tightening water quality regulations. Semi-automated plants persist mainly in legacy facilities, while manual operations are increasingly obsolete, confined to small, resource-constrained municipalities.

Country Analysis of the Municipal Water Treatment Equipment Market

United States: Government Initiatives and Smart Water Management Driving Municipal Water Equipment Demand

The U.S. municipal water treatment equipment market is experiencing robust growth driven by the Bipartisan Infrastructure Law, which allocates over $50 billion to upgrade drinking water, wastewater, and stormwater infrastructure. Distributed through State Revolving Funds (SRFs), the historic investment is a key driver for the adoption of advanced municipal water treatment systems. The EPA’s new PFAS standards targeting GenX chemicals, PFOA, PFOS, PFNA, PFHxS, and HFPO-DA are prompting utilities to implement anion exchange and granular-activated carbon systems. In addition, the EPA’s updated lead rule and Water Technical Assistance (WaterTA) initiatives emphasize regulatory compliance and operational resilience. Industry consolidation, such as H2O America’s $540 million acquisition of Quadvest, reflects the trend toward engineering-driven growth. AI and smart monitoring technologies are being increasingly deployed to optimize chemical use, enhance real-time water quality management, and streamline municipal operations.

China: Policy-Led Expansion and Decentralized Municipal Water Solutions

China’s municipal water treatment market is being shaped by the Water Ten Plan, Dual Carbon goals, and RMB 26 billion allocated in 2024 for water pollution control. Urban water reuse targets, including a 35% reclaimed water use rate by 2025 and over 60% rural wastewater coverage, are driving demand for high-performance municipal treatment equipment and decentralized solutions. Investment priorities include sewage pipeline maintenance, remediation of black and odorous water bodies, and construction of new wastewater treatment plants in second- and third-tier cities. Advanced technologies, including membrane bioreactor (MBR) systems, nutrient removal processes, and smart pipeline monitoring, are increasingly integrated. Chinese enterprises are also expanding exports of turnkey municipal water treatment solutions to Belt and Road countries, reinforcing China’s global leadership in water technology.

India: Scaling Sewage Treatment and Advanced Urban Water Systems

India’s municipal water treatment market is advancing through initiatives like AMRUT 2.0 and the Swachh Bharat Mission – Urban (SBM-U) 2.0, aimed at universal water supply and sewage management. The Namami Gange Programme, extended until March 2026, focuses on river rejuvenation through wastewater treatment, solid waste management, and urban riverfront development. Advanced treatment technologies such as sequencing batch reactors (SBR) and membrane bioreactors (MBR) are becoming standard in municipal applications. Under AMRUT and AMRUT 2.0, over 1,000 STP projects have been approved or grounded, totaling over 6,900 MLD of new sewage treatment capacity. Regulatory oversight by Central and State Pollution Control Boards ensures effluent discharge compliance, further driving the adoption of state-of-the-art municipal water treatment systems across urban centers.

Germany: Innovation, Pre-Treatment, and Resource Recovery in Municipal Water

Germany’s municipal water treatment equipment market benefits from initiatives like the InDigWa project, which integrates isolated innovations to optimize drinking water supply efficiency. Researchers focus on ultra-tight ultrafiltration (u-t UF) membranes and advanced pre-treatment methods for reverse osmosis to reclaim water from complex municipal wastewater streams. The Fraunhofer-Allianz SysWasser consortium pools expertise to develop system-oriented solutions spanning extraction, infrastructure, and wastewater treatment. Energy efficiency and resource recovery remain central, with new technologies enhancing sustainability and maximizing water reuse. These innovations underscore Germany’s commitment to cutting-edge municipal water solutions suitable for both national and international applications.

Saudi Arabia: Vision 2030 and Strategic Water Reuse Expansion

Saudi Arabia’s municipal water treatment market is heavily influenced by Vision 2030 and the National Water Strategy, focusing on sustainability and nearly 100% wastewater reuse. In 2024, the National Water Company (NWC) completed 118 water and sanitation projects worth SR 5.5 billion, increasing operational STP capacity by 478,000 m³/day and benefiting 1.8 million people. With a portfolio exceeding SR 51 billion across 677 development projects, the government leverages public-private partnerships (PPP) to expand municipal treatment capacity. The King Abdullah University of Science and Technology (KAUST) International Water Research Center further supports innovation in advanced municipal water technologies. These initiatives are driving widespread adoption of reclaimed water solutions and sustainable urban water management.

Japan: Leading Membrane Technologies and Compact Municipal Solutions

Japan remains at the forefront of municipal water treatment technology, with advanced membrane systems like Johkasou units and Kubota Submerged Membrane Units enabling efficient onsite wastewater reclamation. The government promotes high-quality, safe tap water through advanced purification using ozone, activated carbon, and polymeric membranes, while academic research from institutions such as Gunma University develops innovative semi-dry FGD processes with minimal wastewater generation. Japan’s emphasis on compact, easy-to-maintain systems ensures wide applicability across densely populated and rural areas alike. Continuous innovation in membrane technology, smart water management, and decentralized municipal systems reinforces Japan’s leadership in sustainable urban water treatment.

Competitive Landscape: Market Leaders Driving Innovation

The municipal water treatment equipment market is dominated by global leaders with diverse strengths in treatment technologies, project execution, and digital integration. These players are shaping the industry through strategic contracts, technology launches, and targeted investments in emerging markets.

Veolia Environnement S.A.: Comprehensive Water Lifecycle Solutions

Veolia leads in “ecological transformation” for both drinking water and wastewater treatment. Its municipal portfolio spans desalination, MBR, and advanced reuse systems, exemplified by the Vitória project in Brazil deploying memDENSE™ MBR and PROflex™ RO. The company emphasizes energy efficiency, climate resilience, and long-term partnerships. Backed by strong R&D capabilities, Veolia addresses pressing challenges like micropollutant removal, positioning itself as a trusted partner for large-scale municipal contracts across Latin America and beyond.

SUEZ S.A.: Circular Water and Waste Management Leader

SUEZ focuses on high-performance, energy-efficient municipal water solutions, integrating advanced oxidation, membrane filtration, and biotech processes. Landmark projects include the €700 million Mumbai wastewater treatment plant and a major upgrade in Denmark targeting pharmaceutical residues. With a global footprint and platforms like AQUADVANCED® for smart network management, SUEZ excels in PPP and DBO contracts while advancing regulatory compliance capabilities.

Xylem Inc.: Smart and Sustainable Water Infrastructure

Xylem delivers smart, interconnected municipal water solutions, combining pumps, filtration, and AI-driven platforms for operational efficiency. Its venture capital investments into water scarcity and quality solutions, coupled with acquisitions like Idrica, strengthen its digital and IoT integration. Xylem’s real-time telemetry expertise makes it a leader in predictive maintenance and intelligent leak detection, addressing both operational costs and resource sustainability.

DuPont Water Solutions: Membrane Technology Specialist

DuPont specializes in high-performance separation and purification technologies, particularly RO, UF, and NF membranes under the FilmTec™ brand. Its ion exchange resins target critical contaminants such as PFAS, making it a go-to provider for compliance-driven projects. Recent deployments in PFAS-focused municipal facilities highlight its strength in emerging contaminant solutions. With deep material science expertise, DuPont delivers membranes that are more resilient, longer-lasting, and capable of achieving higher contaminant removal rates than industry averages.

Municipal Water Treatment Equipment Market Report Scope

Municipal Water Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$42.4 Billion

|

|

Market Size (2034)

|

$68.1 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Treatment Stage (Intake & Pretreatment, Primary Treatment, Secondary Treatment, Tertiary Treatment, Sludge Treatment), By Equipment Type (Pumps & Valves, Aeration Equipment, Chemical Dosing Systems, Filter Media & Membranes, Control & Monitoring Systems), By Plant Capacity (<10 MLD, 10-100 MLD, >100 MLD), By Technology Type (Conventional Treatment, Membrane-Based Systems, Biological Nutrient Removal (BNR), Advanced Oxidation Processes (AOPs)), By Water Source (Surface Water Treatment, Groundwater Treatment, Brackish Water Treatment, Seawater Desalination), By Application (Drinking Water Treatment, Wastewater Treatment, Water Reuse/Recycling, Stormwater Treatment), By Automation Level (Manual Operation, Semi-Automated, Fully Automated)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., SUEZ, Evoqua Water Technologies (now part of Xylem), Pentair, DuPont, Aquatech International LLC, VA Tech WABAG Ltd., Thermax Limited, IDE Technologies, ACCIONA, Kurita Water Industries, Calgon Carbon Corporation, Siemens AG, Trojan Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Municipal Water Treatment Equipment Market Segmentation

By Treatment Stage

- Intake & Pretreatment

- Primary Treatment

- Secondary Treatment

- Tertiary Treatment

- Sludge Treatment

By Equipment Type

- Pumps & Valves

- Aeration Equipment

- Chemical Dosing Systems

- Filter Media & Membranes

- Control & Monitoring Systems

By Plant Capacity

- <10 MLD

- 10-100 MLD

- >100 MLD

By Technology Type

- Conventional Treatment

- Membrane-Based Systems

- Biological Nutrient Removal (BNR)

- Advanced Oxidation Processes (AOPs)

By Water Source

- Surface Water Treatment

- Groundwater Treatment

- Brackish Water Treatment

- Seawater Desalination

By Application

- Drinking Water Treatment

- Wastewater Treatment

- Water Reuse/Recycling

- Stormwater Treatment

By Automation Level

- Manual Operation

- Semi-Automated

- Fully Automated

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Municipal Water Treatment Equipment Market

- Veolia

- Xylem Inc.

- SUEZ

- Evoqua Water Technologies (now part of Xylem)

- Pentair

- DuPont

- Aquatech International LLC

- VA Tech WABAG Ltd.

- Thermax Limited

- IDE Technologies

- ACCIONA

- Kurita Water Industries

- Calgon Carbon Corporation

- Siemens AG

- Trojan Technologies

* List Not Exhaustive

Research Coverage

This report investigates the Global Municipal Water Treatment Equipment Market, presenting detailed analysis reviews of market drivers, regulatory influences, and technological breakthroughs shaping future growth. Published by USDAnalytics, the study highlights how stricter effluent regulations, rapid urbanization, and smart water infrastructure adoption are reshaping the sector. It examines critical trends such as PFAS removal mandates in the U.S., EU micropollutant standards, and Asia’s large-scale capacity expansions. The report also reviews strategic imperatives including water reuse initiatives, AI-driven optimization, and nutrient removal technologies, supported by case studies from global cities. With comprehensive insights into competitive strategies, regional policy frameworks, and investment opportunities, this report is an essential resource for utilities, policymakers, and equipment manufacturers seeking to align with the evolving municipal water treatment landscape.

Scope Includes:

- Segmentation: By Treatment Stage (Primary, Secondary, Tertiary, Quaternary), By Equipment Type (Pumps & Valves, Membranes, Filter Media, Monitoring & Control Systems), By Plant Capacity (Up to 10 MLD, 10–100 MLD, Above 100 MLD), By Technology Type (Conventional, Membrane-Based, Advanced Oxidation), By Water Source (Surface Water, Groundwater, Wastewater), By Application (Drinking Water, Wastewater, Reuse), and By Automation Level (Manual, Semi-Automated, Fully Automated).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Competitive analysis and profiles of 15+ leading companies including Veolia, SUEZ, Xylem, DuPont, and Kurita.

Methodology

The research methodology employed by USDAnalytics combines primary interviews and secondary data analysis to build reliable, actionable insights. Primary research included consultations with municipal utility managers, regulators, EPC contractors, and equipment providers to validate demand patterns, compliance pressures, and technology adoption rates. Secondary data sources included policy documents, regulatory guidelines, company disclosures, and international project databases. Market sizing used both top-down and bottom-up approaches, cross-verified through data triangulation across regions, treatment processes, and equipment categories. Scenario modeling incorporated factors such as population growth, regulatory enforcement timelines, and infrastructure investment cycles, ensuring projections that reflect realistic market evolution.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Municipal Water Treatment Equipment Market

Table of Contents: Municipal Water Treatment Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Stakeholders

1.3. Global Market Snapshot

2. Market Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $42.4 Billion

2.2.2. Forecasted Market Size (2034): $68.1 Billion at 5.4% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Tightening Water Quality Regulations and Micropollutant Removal

2.3.2. Increasing Urbanization and Population Growth in Emerging Markets

2.3.3. Advancements in Smart Water Infrastructure and Digitalization

2.3.4. Water Scarcity and the Push for Water Reuse

3. Market Analysis: Key Developments and Growth Catalysts

3.1. Overview of Strategic Expansions and Partnerships

3.2. Key Player Developments

3.2.1. Veolia's Water Reuse Project in Brazil

3.2.2. SUEZ's Micropollutant Retrofit in Denmark and Mega-Plant in China

3.2.3. Xylem's Investment in Climate-Focused Startups

3.2.4. City of DuPont, Washington's PFAS Treatment Facilities

3.3. Major Infrastructure Expansion Projects in High-Growth Cities

4. Trends and Opportunities in Municipal Water Treatment

4.1. Trend 1: Smart Water Infrastructure with AI-Driven Optimization

4.1.1. Real-Time Monitoring and Predictive Maintenance

4.1.2. Operational Savings and Enhanced Reliability

4.2. Trend 2: Advanced Nutrient Removal for Stricter Regulations

4.2.1. Biological Nutrient Removal (BNR) and Anammox Technologies

4.2.2. Membrane Bioreactors (MBRs) for High-Efficiency Removal

4.3. Opportunity 1: PFAS Removal Mandates Driving Upgrades

4.3.1. EPA Standards and Funding from the Bipartisan Infrastructure Law

4.3.2. Demand for GAC, Ion Exchange Resins, and RO Systems

4.4. Opportunity 2: Climate-Resilient Decentralized Systems

4.4.1. Mitigating Droughts and Floods with Localized Solutions

4.4.2. Reduced Infrastructure Costs and Energy Consumption

5. Municipal Water Treatment Equipment Market Share Insights

5.1. By Treatment Stage

5.1.1. Secondary Treatment (Dominating) vs. Tertiary Treatment (Fastest-Growing)

5.2. By Equipment Type

5.2.1. Pumps & Valves, Filter Media & Membranes, and Control Systems

5.3. By Plant Capacity

5.3.1. Mid-Sized Plants (10-100 MLD) as the Global Sweet Spot

5.3.2. Megaproject Plants (>100 MLD) for Metropolitan Areas

5.4. By Technology Type

5.4.1. Conventional Treatment vs. Membrane-Based and AOPs

5.5. By Water Source

5.5.1. Surface Water vs. Wastewater Treatment

5.6. By Application

5.6.1. Drinking Water vs. Water Reuse/Recycling

5.7. By Automation Level

5.7.1. Fully Automated Systems as the Industry Standard

6. Country Analysis of the Municipal Water Treatment Equipment Market

6.1. United States: Government Initiatives and Smart Water Management

6.2. China: Policy-Led Expansion and Decentralized Solutions

6.3. India: Scaling Sewage Treatment and Urban Systems

6.4. Germany: Innovation, Pre-Treatment, and Resource Recovery

6.5. Saudi Arabia: Strategic Water Reuse Expansion

6.6. Japan: Leading Membrane Technologies and Compact Solutions

6.7. Other Country Analysis

7. Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Treatment Stage

7.1.2. By Equipment Type

7.1.3. By Plant Capacity

7.1.4. By Technology Type

7.1.5. By Water Source

7.1.6. By Application

7.1.7. By Automation Level

7.2. Europe Market Size Outlook to 2034

7.2.1. By Treatment Stage

7.2.2. By Equipment Type

7.2.3. By Plant Capacity

7.2.4. By Technology Type

7.2.5. By Water Source

7.2.6. By Application

7.2.7. By Automation Level

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Treatment Stage

7.3.2. By Equipment Type

7.3.3. By Plant Capacity

7.3.4. By Technology Type

7.3.5. By Water Source

7.3.6. By Application

7.3.7. By Automation Level

7.4. South America Market Size Outlook to 2034

7.4.1. By Treatment Stage

7.4.2. By Equipment Type

7.4.3. By Plant Capacity

7.4.4. By Technology Type

7.4.5. By Water Source

7.4.6. By Application

7.4.7. By Automation Level

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Treatment Stage

7.5.2. By Equipment Type

7.5.3. By Plant Capacity

7.5.4. By Technology Type

7.5.5. By Water Source

7.5.6. By Application

7.5.7. By Automation Level

8. Competitive Landscape: Leading Players in Municipal Water Treatment Equipment

8.1. Veolia Environnement S.A.

8.2. SUEZ S.A.

8.3. Xylem Inc.

8.4. DuPont Water Solutions

8.5. Evoqua Water Technologies (now part of Xylem)

8.6. Pentair

8.7. Aquatech International LLC

8.8. VA Tech WABAG Ltd.

8.9. Thermax Limited

8.10. IDE Technologies

8.11. ACCIONA

8.12. Kurita Water Industries

8.13. Calgon Carbon Corporation

8.14. Siemens AG

8.15. Trojan Technologies

8.16. Other Key Companies

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations