Water Purification Equipment Market Overview

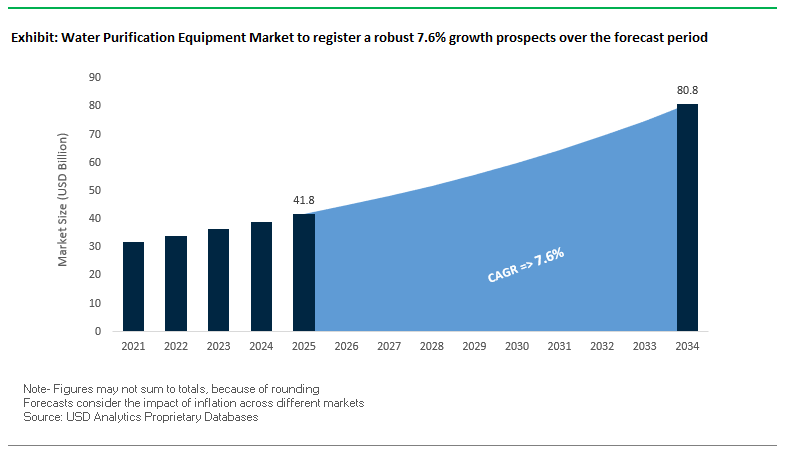

The water purification equipment market is expected to grow from $41.8 billion in 2025 to $80.8 billion by 2034, at a steady CAGR of 7.6%. The expansion is fueled by tightening global regulations on micropollutant removal, the growing use of hybrid water treatment technologies, and the rapid adoption of IoT-enabled smart purification systems.

Across Europe and North America, regulatory frameworks are now mandating advanced treatment processes to remove pharmaceutical residues, pesticides, and PFAS chemicals from municipal and industrial water streams. Hybrid purification systems combining reverse osmosis (RO), ultrafiltration (UF), and UV sterilization are becoming standard, delivering multi-barrier protection and higher efficiency in contaminant removal.

The industry is also seeing a surge in real-time monitoring systems integrated with IoT and AI, enabling automated filter replacement alerts, remote quality tracking, and predictive maintenance. Industrial facilities are prioritizing energy-efficient purification systems with high recovery rates, such as Veolia’s CaptuRO™, to reduce operational costs while promoting water reuse.

Strategic imperatives for stakeholders:

- Invest in hybrid multi-barrier purification systems combining RO, UF, and UV for maximum contaminant removal.

- Adopt IoT-enabled smart water purifiers for real-time quality monitoring and predictive maintenance.

- Expand capabilities in micropollutant removal technologies to meet tightening global regulations.

- Focus on industrial water reuse systems with high recovery rates to reduce costs and environmental impact.

Market Analysis: Strategic Expansions, Technological Breakthroughs, and Regulatory Alignment Driving Growth

The water purification equipment market is undergoing a wave of strategic activity, with companies expanding portfolios, entering new geographies, and integrating advanced purification technologies.

In November 2024, A.O. Smith completed its acquisition of Hindustan Unilever's Pureit business, significantly broadening its product range and distribution reach in India as one of the fastest-growing consumer markets for drinking water purification systems. Similarly, LG Electronics India in September 2024 introduced nine new models equipped with airtight stainless-steel tanks, advanced UV sterilization, and multi-stage filtration, addressing the rising demand for high-performance household purifiers.

Innovation is also reshaping industrial applications. Kurita Water Industries in December 2024 successfully demonstrated wastewater-powered electricity generation via microbial fuel cells, paving the way for energy-neutral water treatment plants. On the pharmaceutical side, Veolia Water Technologies launched PoIaris™ 2.0 in February 2024, a high-capacity distillation and steam generation system meeting the strict requirements for water for injection (WFI).

International expansion remains a key growth lever. Kent RO Systems announced in January 2024 its entry into the U.S. market under a licensing deal with Black & Decker, targeting a turnover of Rs 2,000 crore within three years. Meanwhile, DuPont Water Solutions received the 2025 BIG Innovation Award for sustainable purification technologies that minimize environmental impact.

On the infrastructure side, SUEZ secured a landmark €700 million contract in September 2022 for a 500 MLD wastewater treatment facility in Mumbai, featuring membrane bioreactor (MBR) and high-rate clarifier technology. In July 2025, H2O America acquired Quadvest for $540 million, committing an additional $500 million to infrastructure modernization with advanced modular purification systems.

Trends and Opportunities in Water Purification Equipment Market

Trend 1: Decentralized Point-of-Use (POU) Systems for Emerging Contaminants

The water purification equipment market is witnessing a surge in demand for decentralized point-of-use (POU) systems due to rising concerns over emerging contaminants such as PFAS, microplastics, and pharmaceuticals. These systems provide a final barrier of protection at the tap, directly addressing public health risks and supplementing aging municipal water infrastructure. Reverse osmosis (RO) units, which held a 32% revenue share in the POU segment in 2024, are highly preferred for their ability to remove dissolved solids, viruses, and bacteria, making them a cornerstone technology for households and commercial applications. According to the EPA, around 70 million Americans are exposed to PFAS in drinking water, further driving the adoption of advanced POU filtration. The POU market’s rapid expansion, from $31.90 billion in 2024 to a projected $53.56 billion by 2030 at a CAGR of 9.2%, highlights the increasing consumer and commercial emphasis on immediate, point-specific water safety solutions.

Trend 2: Military-Grade Mobile Purification for Disaster Response

Climate-induced disasters and critical infrastructure failures are creating a growing need for mobile, military-grade water purification systems capable of rapid deployment. These compact, containerized systems, including vehicle-mounted RO units, can produce over 100 liters of clean water per day from almost any source, from seawater to floodwaters. Rapid setup, often within 90 minutes, allows immediate disaster relief and supports emergency operations. Beyond microbial contaminants, these systems are engineered to remove chemical, biological, and radiological threats, ensuring comprehensive safety in unpredictable environments. Such rugged, multi-contaminant systems are increasingly adopted by governments, NGOs, and emergency response agencies, reflecting a trend toward resilient, on-demand water purification in both developed and disaster-prone regions.

Opportunity 1: Industrial Ultrapure Water for Semiconductor Manufacturing

The global semiconductor industry is driving a critical opportunity in ultrapure water (UPW) systems. Modern chip fabrication plants consume up to 10 million gallons of ultrapure water per day, requiring purity levels in parts per quadrillion to prevent microchip defects. With the global UPW market projected to reach $30 billion by 2040, semiconductor fabs represent a high-growth segment for advanced filtration, ion exchange, and membrane distillation technologies. The increasing number of new semiconductor fabs worldwide, coupled with rising global chip demand, underscores the strategic importance of investing in industrial-scale water purification systems that can consistently deliver extreme water quality.

Opportunity 2: Atmospheric Water Generation (AWG) for Arid Regions

Atmospheric Water Generation (AWG) technology is emerging as a sustainable solution to address chronic water scarcity, particularly in arid and semi-arid regions. AWG systems extract water vapor from the air, creating decentralized, on-demand water sources. The atmosphere contains an estimated 13,000 cubic kilometers of water, representing a largely untapped renewable resource. Solar-powered AWG units, integrating renewable energy, can produce 0.89 to 18 liters per day depending on humidity and seasonal conditions, at an economical cost of approximately $0.11 per liter. Adoption of AWG technologies in water-stressed areas not only provides reliable drinking water but also reduces pressure on municipal water networks, offering long-term environmental and economic benefits.

Water Purification Equipment Market Share Insights

By Technology Type: Filtration Systems Lead While Reverse Osmosis Sets Premium Standard

Filtration systems command nearly 35% of the global water purification equipment market by 2025, making them the core technology across residential, municipal, and commercial installations. Their versatility spans from basic sediment and carbon filters to advanced ultrafiltration (UF) and nanofiltration (NF) membranes, ensuring broad applicability for chlorine, particulate, and microorganism removal. Meanwhile, reverse osmosis (RO) systems, with a 20% market share, dominate high-purity applications, particularly in premium residential units and industrial settings like pharmaceuticals and semiconductors, where ultra-low TDS is non-negotiable.

.png)

By End-Use Application: Residential Demand Drives Volume, Industrial Use Secures Value

Residential applications account for about 40% of the water purification equipment market, fueled by consumer health concerns, deteriorating tap water quality, and demand for convenient point-of-use (POU) solutions such as under-sink RO systems and whole-house filters. On the other hand, the industrial segment represents the highest value density, with manufacturing sectors such as semiconductors, power generation, and food & beverage requiring ultrapure process water. The industrial reliance on large-scale RO, ion exchange, and EDI systems underscores its strategic role in market growth.

By Contaminant Removal: Microbiological Safety and Chemical Contaminants Take Priority

Microbiological removal technologies contribute nearly 30% of the global market, reflecting the ongoing global priority on pathogen-free drinking water. Disinfection systems (UV, ozone, chlorination) and fine membranes (UF, MF) continue to dominate in both municipal and residential applications. Simultaneously, the chemical contaminant removal segment is gaining traction, driven by rising awareness of pesticides, VOCs, PFAS, and other emerging contaminants. Activated carbon, advanced oxidation processes (AOPs), and RO membranes are central to addressing the broadening category of chemical risks.

By Distribution Channel: Retail Stores Lead, Online Platforms Surge Ahead

Retail stores retain the largest share (34.65%) of water purification equipment sales, remaining the key channel for residential products such as pitcher filters, faucet-mounted attachments, and replacement cartridges. However, online platforms are the fastest-growing channel with 30% market share, driven by direct-to-consumer sales, broader product availability, and consumer reliance on digital research and price comparison. The shift is transforming how manufacturers engage with end-users, placing greater emphasis on e-commerce strategies and subscription filter replacement models.

By System Configuration: Standalone Units Dominate, Modular Systems Gain Relevance

Standalone units represent around 51.7% of the market, led by consumer-friendly POU solutions such as countertop purifiers, under-sink RO, and pitchers. Ease of use, affordability, and mass availability make the configuration the global standard for households. However, modular systems are carving a niche in industrial and decentralized treatment markets, where scalability, skid-mounted flexibility, and rapid deployment are essential. The segment is increasingly favored in regions with expanding industrial clusters and remote operations.

By Energy Requirement: Low-Energy Systems Take the Lead, RO and Distillation Drive High-Energy Demand

Low-energy systems contribute nearly 46.2% of global market share, powered by the efficiency of UV systems, activated carbon, and ion exchange technologies. Their moderate energy demand positions them as the balanced choice across residential, commercial, and municipal installations. By contrast, high-energy systems led by reverse osmosis and distillation dominate the premium end of the market, where superior contaminant removal justifies energy-intensive operation. The energy-performance trade-off is reshaping procurement decisions in both industrial and high-end residential applications.

By Price Segment: Mid-Range Solutions Define the Sweet Spot

Mid-range systems hold about 40% of the water purification equipment market, balancing affordability with advanced features, particularly in multi-stage filters and quality under-sink RO systems. They cater to the largest consumer base, especially in urban middle-class households worldwide. Meanwhile, premium and luxury systems (~30% combined) are rising steadily, led by smart RO systems with Wi-Fi integration, whole-house solutions, and designer units offering alkalization and mineralization. The premiumization trend highlights a growing shift from basic utility to lifestyle-driven water purification.

Country Analysis of the Water Purification Equipment Market

United States: Advanced Water Purification and Smart Monitoring Integration

The U.S. water purification equipment market is experiencing strong growth, driven by the Bipartisan Infrastructure Law, which dedicates over $50 billion for upgrading drinking water and wastewater infrastructure. The investment is spurring demand for advanced water treatment technologies, including granular activated carbon systems, anion exchange resins, and mobile purification units. Regulatory pressures from the EPA, including new PFAS standards and lead rules, are accelerating the adoption of multi-pollutant removal systems capable of handling emerging contaminants like pharmaceuticals and microplastics. USDA Emergency Community Water Assistance Grants further promote the deployment of mobile and emergency water purification equipment. Companies like Xylem, through its Sensus brand, are integrating IoT-enabled monitoring and data analytics, allowing utilities to remotely manage water quality and optimize operations for efficiency and sustainability.

China: Policy-Driven Modernization and Membrane Technology Adoption

China’s water purification equipment market is powered by government initiatives such as the Water Ten Plan and the 14th Five-Year Plan, with over RMB 26 billion allocated to water pollution control in 2024. The country is emphasizing the treatment of “black and odorous” water bodies and the protection of drinking water sources, which has increased public participation and investment in remediation efforts. Advanced technologies, including membrane bioreactors (MBR) and reverse osmosis (RO) systems, are being deployed to meet stringent water quality standards. Real-time emission monitoring mandated by the Ministry of Ecology and Environment has created a need for continuously monitored purification systems. Additionally, containerized plants are being deployed in industrial parks for process water treatment and reuse, while smart pipeline management and nutrient removal projects in cities like Shanghai and the Greater Bay Area reflect a shift toward technologically advanced water purification solutions.

India: IoT-Enabled Rural Water Purification and Zero Liquid Discharge Adoption

India’s growing water demand, projected to be double the available supply by 2030, is a critical driver for the water purification equipment market. The Jal Jeevan Mission aims to provide safe tap water to every rural household, creating a large market for residential and community-level purification systems, supported by a $51 billion budget. The government is deploying IoT-based monitoring devices across over six lakh villages, forming a smart rural water supply ecosystem. Wastewater recycling and zero liquid discharge (ZLD) technologies, including sequencing batch reactors (SBR) and MBR systems, are gaining adoption across industrial and municipal applications. Startups are also developing IoT-enabled smart meters and management solutions for real-time consumption tracking and leak detection. The use of water ATMs, which are containerized purification and dispensing units, is increasingly common in water-scarce regions, highlighting a growing trend toward mobile and decentralized water treatment.

Germany: Regulatory Compliance and Energy-Efficient Purification Solutions

Germany’s stringent regulations under the Water Framework Directive are a major driver for the water purification equipment market, requiring all water bodies to achieve good ecological and chemical status. German companies like Bosch Manufacturing Solutions are developing innovative, chemical-free, energy-efficient systems, particularly for green hydrogen production in remote areas. BWT is introducing revolutionary backwash filters with rotary-pulse technology to enhance drinking water hygiene. The adoption of membrane bioreactors and intelligent monitoring systems is increasing operational efficiency and reducing energy usage. Initiatives like Fraunhofer-Allianz SysWasser, which pool expertise from multiple Fraunhofer Institutes, focus on system-oriented solutions for water extraction, infrastructure, and wastewater treatment at both national and international levels, reinforcing Germany’s leadership in advanced and sustainable water purification technologies.

Israel: Desalination Leadership and Circular Water Economy Innovations

Israel is a global leader in desalination technology, producing approximately 75% of its drinking water from the Mediterranean Sea. The country also reclaims nearly 90% of wastewater for agricultural irrigation and industrial use, making it a pioneer in the circular water economy. Technological advancements focus on developing cost-efficient, high-performance membranes for desalination and decontamination that resist contaminant buildup. Researchers at the Technion-Israel Institute of Technology are exploring innovative methods to clean wastewater for agricultural purposes by injecting air into the soil. Israel’s commitment to resource recovery extends to nutrients from wastewater, which are utilized for bioenergy and fertilizers, highlighting the country’s leadership in sustainable water purification and water reuse technologies.

Competitive Landscape: Global Leaders Redefining Water Purification Technologies

The water purification equipment market is led by multinational corporations and specialized technology innovators delivering advanced membrane filtration, reverse osmosis, biological treatment, and smart water solutions. These companies are differentiating themselves through digital integration, sustainable engineering, and end-to-end service capabilities.

Veolia Environnement S.A.: Full-Lifecycle, Energy-Efficient Water Solutions

Veolia focuses on delivering ecological transformation through a complete water lifecycle approach, from process water treatment to wastewater recycling. Its portfolio spans membrane bioreactors, reverse osmosis systems, and continuous electro-deionisation. The recently launched PoIaris™ 2.0 caters to pharmaceutical clients requiring ultra-high purity WFI. Veolia’s strength lies in combining engineering expertise with operational management, making it a trusted partner for both municipal utilities and industrial operators worldwide.

SUEZ S.A.: Circular Water Solutions with Global Project Execution

SUEZ drives circular economy principles in water purification, offering membrane filtration, advanced oxidation, and biological treatment. It has delivered high-profile projects such as the Mumbai wastewater facility and the Wanhua Chemical seawater desalination plant. Known for its expertise in public-private partnerships, SUEZ also collaborates with research bodies like CNRS to combat micropollutants, aligning with evolving regulatory demands.

DuPont Water Solutions: Advanced Membrane and Ion Exchange Technology Leader

DuPont is a pioneer in RO, UF, and NF membranes under its FilmTec™ brand, complemented by specialized ion exchange resins. Its R&D investments focus on developing anti-fouling, high-recovery membranes for industrial water reuse and ultrapure applications. The Sustainability Navigator digital tool underscores DuPont’s commitment to ESG-aligned purification solutions that meet performance and environmental targets.

Xylem Inc.: Smart, Interconnected Water Purification Platforms

Xylem delivers integrated purification solutions combining pumps, aeration, filtration, and data analytics. Its vendor-agnostic platforms incorporate AI-driven leak detection and network optimization via acquisitions like Idrica. Designed for industries from food and beverage to pharmaceuticals, Xylem’s modular and scalable systems enable clients to improve efficiency, reduce environmental impact, and integrate legacy assets seamlessly.

Water Purification Equipment Market Report Scope

Water Purification Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$41.8 Billion

|

|

Market Size (2034)

|

$80.8 Billion

|

|

Market Growth Rate

|

7.6%

|

|

Segments

|

By Technology Type (Filtration Systems, Disinfection Systems, Distillation Systems, Ion Exchange Systems, Emerging Technologies), By End-Use Application (Residential, Commercial, Industrial, Municipal), By Contaminant Removal (Microbiological, Chemical, Physical, TDS Reduction), By Distribution Channel (Direct Sales, Retail Stores, Online Platforms, Distributor Networks), By System Configuration (Standalone Units, Modular Systems, Fully Integrated Plants), By Energy Requirement (Non-Electric, Low-Energy, High-Energy), By Price Segment (Economy, Mid-Range, Premium, Luxury)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Pentair, A.O. Smith, Eureka Forbes, LG Electronics, Panasonic Holdings Corporation, Kent RO Systems Ltd., Culligan Water, Coway Co., Ltd., 3M, Unilever, BWT Holding GmbH, Kinetico Incorporated, Aquatech International LLC, Watts Water Technologies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Purification Equipment Market Segmentation

By Technology Type

- Filtration Systems

- Reverse Osmosis (RO) Systems

- Ultrafiltration (UF) Systems

- Nanofiltration (NF) Systems

- Activated Carbon Filters

- Ceramic Filters

- Sand/Multimedia Filters

- Disinfection Systems

- UV Purifiers

- Ozone Generators

- Chlorination Systems

- Electrochlorination Units

- Distillation Systems

- Thermal Distillation

- Membrane Distillation

- Ion Exchange Systems

- Water Softeners

- Deionizers

- Emerging Technologies

- Forward Osmosis

- Photocatalytic Oxidation

- Graphene-based Filters

By End-Use Application

- Residential

- Under-sink purifiers

- Countertop units

- Whole-house systems

- Commercial

- Offices

- Hotels/Restaurants

- Schools/Hospitals

- Industrial

- Pharmaceutical

- Food & Beverage

- Power Plants

- Electronics Manufacturing

- Municipal

- Drinking Water Treatment

- Wastewater Reclamation

By Contaminant Removal

- Microbiological

- Chemical

- Physical

- TDS Reduction

By Distribution Channel

- Direct Sales

- Retail Stores

- Online Platforms

- Distributor Networks

By System Configuration

- Standalone Units

- Modular Systems

- Fully Integrated Plants

By Energy Requirement

- Non-Electric

- Low-Energy

- High-Energy

By Price Segment

- Economy

- Mid-Range

- Premium

- Luxury

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water Purification Equipment Market

- Pentair

- A.O. Smith

- Eureka Forbes

- LG Electronics

- Panasonic Holdings Corporation

- Kent RO Systems Ltd.

- Culligan Water

- Coway Co., Ltd.

- 3M

- Unilever

- BWT Holding GmbH

- Kinetico Incorporated

- Aquatech International LLC

- Watts Water Technologies

* List Not Exhaustive

Research Coverage

This report investigates the Global Water Purification Equipment Market, delivering comprehensive analysis reviews on regulatory drivers, technological breakthroughs, and competitive dynamics shaping industry growth through 2034. Published by USDAnalytics, the study highlights the accelerating demand for hybrid multi-barrier purification systems, IoT-enabled smart monitoring, and advanced micropollutant removal technologies as governments enforce stricter PFAS and pharmaceutical residue limits. It also underscores strategic imperatives such as industrial water reuse, decentralized purification, and atmospheric water generation for arid regions. With detailed assessments of technology adoption, regional policies, and competitive strategies, this report is an essential resource for equipment manufacturers, utilities, investors, and policymakers seeking to capture opportunities in the rapidly evolving water purification equipment landscape.

Scope Includes:

- Segmentation: By Technology Type (Filtration Systems, Reverse Osmosis, UV, Hybrid Multi-Barrier Systems, Advanced Oxidation, AWG), By End-Use Application (Residential, Industrial, Municipal, Commercial, Military & Emergency Response), By Contaminant Removal (Microbiological, Chemical, Emerging Contaminants), By Distribution Channel (Retail, Online, Direct), By System Configuration (Standalone, Modular, Containerized), By Energy Requirement (Low-Energy, High-Energy), and By Price Segment (Entry, Mid-Range, Premium).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic & Forecast Data: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Profiles and strategic assessments of 15+ leading companies including Veolia, SUEZ, DuPont, Xylem, A.O. Smith, LG, Kent, and Kurita.

Methodology

The research methodology adopted by USDAnalytics combines primary interviews and secondary research to ensure accuracy and relevance. Primary data was gathered from manufacturers, utilities, EPC contractors, and regulators to validate adoption patterns, technology preferences, and investment priorities. Secondary research included government policy frameworks, company financials, patent filings, and industry databases to capture macro and micro-level developments. Market estimates were derived using both top-down and bottom-up approaches, with data triangulation applied across regions, technologies, and end-use applications. Scenario modeling incorporated variables such as regulatory timelines, infrastructure spending, consumer adoption of POU systems, and industrial demand for ultrapure water, producing robust and actionable forecasts.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Purification Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Stakeholders

1.3. Global Market Snapshot

2. Market Overview (2025–2034)

2.1. Market Valuation and Growth Projections (2025–2034)

2.1.1. Current Market Size (2025): $41.8 Billion

2.1.2. Forecasted Market Size (2034): $80.8 Billion at 7.6% CAGR

2.2. Key Drivers and Market Dynamics

2.2.1. Tightening Global Regulations on Micropollutant Removal

2.2.2. Growing Use of Hybrid Water Treatment Technologies

2.2.3. Rapid Adoption of IoT-enabled Smart Purification Systems

3. Market Analysis: Strategic Expansions, Technological Breakthroughs, and Regulatory Alignment

3.1. Overview of Strategic Activity and Market Reshaping

3.2. Key Player Developments and Acquisitions

3.2.1. A.O. Smith's Acquisition of Pureit Business

3.2.2. LG Electronics India's New Product Launch

3.2.3. Kurita Water Industries' Wastewater-Powered Electricity Demonstration

3.2.4. Veolia Water Technologies' PoIaris™ 2.0 Launch

3.2.5. Kent RO Systems' Entry into the U.S. Market

3.3. Major Infrastructure Projects and High-Value Contracts

4. Trends and Opportunities in Water Purification Equipment

4.1. Trend 1: Decentralized Point-of-Use (POU) Systems

4.1.1. Addressing Emerging Contaminants like PFAS and Microplastics

4.1.2. Rapid Expansion of the POU Market

4.2. Trend 2: Military-Grade Mobile Purification for Disaster Response

4.2.1. Rapid Deployment for Emergency Operations

4.2.2. Comprehensive Contaminant Removal (Chemical, Biological, Radiological)

4.3. Opportunity 1: Industrial Ultrapure Water for Semiconductor Manufacturing

4.3.1. High-Purity Water Demand in Chip Fabrication

4.3.2. Projected Market Growth for UPW Systems

4.4. Opportunity 2: Atmospheric Water Generation (AWG) for Arid Regions

4.4.1. A Sustainable, On-Demand Water Source

4.4.2. Cost-Effective and Decentralized Solutions

5. Water Purification Equipment Market Share Insights

5.1. By Technology Type

5.1.1. Filtration Systems and Reverse Osmosis (RO)

5.2. By End-Use Application

5.2.1. Residential vs. Industrial Segments

5.3. By Contaminant Removal

5.3.1. Microbiological vs. Chemical Contaminants

5.4. By Distribution Channel

5.4.1. Retail Stores vs. Online Platforms

5.5. By System Configuration

5.5.1. Standalone Units vs. Modular Systems

5.6. By Energy Requirement

5.6.1. Low-Energy vs. High-Energy Systems

5.7. By Price Segment

5.7.1. Mid-Range vs. Premium Systems

6. Country Analysis of the Water Purification Equipment Market

6.1. United States: Advanced Purification and Smart Monitoring

6.2. China: Policy-Driven Modernization and Membrane Technology

6.3. India: IoT-Enabled Rural Water Purification and ZLD Adoption

6.4. Germany: Regulatory Compliance and Energy-Efficient Solutions

6.5. Israel: Desalination Leadership and Circular Water Economy

6.6. Other Country Analysis

7. Competitive Landscape: Global Leaders Redefining Water Purification Technologies

7.1. Veolia Environnement S.A.

7.2. SUEZ S.A.

7.3. DuPont Water Solutions

7.4. Xylem Inc.

7.5. Pentair

7.6. A.O. Smith

7.7. LG Electronics

7.8. Eureka Forbes

7.9. Kent RO Systems Ltd.

7.10. Culligan Water

7.11. Coway Co., Ltd.

7.12. 3M

7.13. Unilever

7.14. BWT Holding GmbH

7.15. Kinetico Incorporated

7.16. Aquatech International LLC

7.17. Watts Water Technologies

7.18. Other Key Companies

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. Market Overview and Growth Drivers

8.1.2. By Technology Type

8.1.3. By End-Use Application

8.1.4. By Distribution Channel

8.1.5. By System Configuration

8.2. Europe Market Size Outlook to 2034

8.2.1. Market Overview and Growth Drivers

8.2.2. By Technology Type

8.2.3. By End-Use Application

8.2.4. By Distribution Channel

8.2.5. By System Configuration

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. Market Overview and Growth Drivers

8.3.2. By Technology Type

8.3.3. By End-Use Application

8.3.4. By Distribution Channel

8.3.5. By System Configuration

8.4. South America Market Size Outlook to 2034

8.4.1. Market Overview and Growth Drivers

8.4.2. By Technology Type

8.4.3. By End-Use Application

8.4.4. By Distribution Channel

8.4.5. By System Configuration

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. Market Overview and Growth Drivers

8.5.2. By Technology Type

8.5.3. By End-Use Application

8.5.4. By Distribution Channel

8.5.5. By System Configuration

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations