Advanced Water Filtration Systems Market Overview – Regulatory Shifts, Smart Technologies, and Sustainable Membrane Innovations Driving Growth

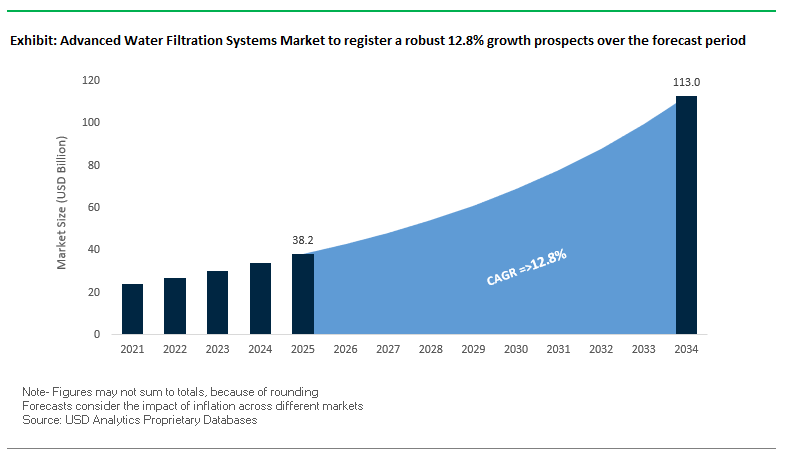

The global advanced water filtration systems market is projected to grow from USD 38.2 billion in 2025 to USD 112.9 billion by 2034, expanding at a CAGR of 12.8%. The growth trajectory is being shaped by a combination of regulatory tightening, technological integration, and sustainability imperatives across industries.

Stricter environmental standards, such as the U.S. EPA’s regulations on per- and polyfluoroalkyl substances (PFAS) and Europe’s updated Drinking Water Directive, are compelling utilities and industries to adopt advanced filtration technologies capable of removing a wider spectrum of emerging contaminants, including micropollutants like pharmaceutical residues, pesticides, and herbicides.

Simultaneously, the integration of IoT-enabled sensors, AI-driven analytics, and real-time operational dashboards is creating a new era of smart water filtration systems. These solutions predict maintenance needs, optimize chemical dosing, and send automated alerts, reducing operational costs and improving system reliability. On the technology front, next-generation reverse osmosis (RO) and nanofiltration (NF) membranes are improving energy efficiency, resisting fouling, and enabling higher water recovery rates remain critical for industrial wastewater reuse and minimal liquid discharge (MLD) schemes that recycle up to 95% of process water.

For industry stakeholders, these market forces represent not just compliance necessities but strategic opportunities for differentiation and ROI enhancement.

Strategic imperatives for shareholders:

- Prioritize investments in PFAS removal and micropollutant-targeting technologies to capture high-growth regulatory-driven demand.

- Expand portfolios with AI-powered filtration systems to command a premium in both municipal and industrial tenders.

- Target water-stressed regions with MLD-capable systems to address the dual challenge of water scarcity and discharge minimization.

- Forge partnerships with membrane innovators to integrate high-performance materials into proprietary solutions.

Market Analysis – Contract Wins, Breakthrough Technologies, and Cross-Sector Expansion

The past 18 months have seen an acceleration in R&D commercialization and strategic partnerships within the advanced water filtration systems market, underscoring its role in both industrial efficiency and environmental compliance.

In August 2025, DuPont Water Solutions received the BIG Sustainability Award for its FilmTec™ Fortilife™ membranes, which enable more efficient industrial wastewater reuse, particularly in MLD applications. That same month, Kurita Water Industries partnered with lunar exploration company ispace to develop a demonstration water purification system for deployment on the Moon.

September 2025 marked a milestone for Veolia, which secured a multi-million-dollar seawater desalination contract with Petrobras to support two FPSOs in Brazil’s offshore energy sector. Meanwhile, June 2025 saw Veolia announce its patented Drop® technology, capable of up to 99.9999% destruction of targeted PFAS compounds, offering integration potential for both municipal and industrial treatment lines.

Earlier developments in 2024 set the stage for the momentum. SUEZ won a October 2024 contract in Denmark to upgrade a wastewater plant with inline ozonation and Granular Activated Carbon (GAC) filtration to remove pharmaceutical residues, addressing Europe’s regulatory focus on micropollutants. Also in October 2024, Pentair acquired Porous Media, expanding its industrial filtration capabilities. In August 2024, Xylem launched the Rivo™ I modular analyzer and control platform for municipal water, enhancing operational precision in chemical dosing and filtration efficiency.

Trends and Opportunities in Advanced Water Filtration Systems Market

Trend 1: Nanofiltration & Graphene Membranes Replace Traditional RO for Selective Contaminant Removal

The advanced water filtration systems market is witnessing a pivotal shift from conventional reverse osmosis (RO) towards nanofiltration (NF) and graphene-based membranes due to the demand for targeted contaminant removal and reduced energy consumption. Nanofiltration membranes operate at significantly lower pressures (0.5–2.5 MPa) than RO systems (~4 MPa), decreasing electricity costs while maintaining effective removal of heavy metals like copper, cobalt, and lead. Graphene and graphene oxide membranes provide exceptional adsorption of emerging pollutants such as PFAS, with studies demonstrating over 95% rejection rates for antibiotics like tetracycline under optimized conditions. Research in next-generation graphene membranes emphasizes structural stability over extended operation, creating high-efficiency solutions that address both environmental and regulatory concerns in industrial, municipal, and residential water treatment applications.

Trend 2: Point-of-Use (POU) Filtration Systems Surge Due to Rising Concerns Over Microplastics

Rising awareness of microplastic contamination in drinking water has driven strong demand for point-of-use (POU) filtration systems. Studies indicate microplastics are present in over 70% of tap water samples globally, prompting consumers to seek reliable filtration solutions. Advanced POU systems with fine membranes (0.2 microns) are capable of removing nearly 100% of microplastics, along with other impurities such as bacteria and chlorine. The surge in adoption is fueled by growing concerns over human health impacts, including inflammation and hormonal disruption, and reflects an industry-wide effort to provide comprehensive, consumer-friendly water purification solutions in residential, commercial, and institutional settings.

Opportunity 1: Self-Cleaning Filters with AI-Powered Clog Detection for Industrial Applications

Industrial water filtration is increasingly adopting AI-integrated self-cleaning systems to minimize downtime and reduce operational costs. These systems monitor pressure and flow rates in real time and automatically initiate cleaning cycles when a clog is detected, ensuring continuous production. AI algorithms enable predictive maintenance by detecting early signs of fouling, reducing the need for manual intervention. The automation enhances efficiency, prolongs filter lifespan, and lowers labor and replacement costs, making AI-powered self-cleaning filtration systems a highly attractive investment for food & beverage, pharmaceutical, semiconductor, and metals & mining industries.

Opportunity 2: Ceramic Membrane Filters for Low-Cost, Long-Lasting Water Purification in Developing Countries

Ceramic membrane filters are emerging as a cost-effective, durable, and locally producible solution for decentralized water purification, particularly in developing nations and off-grid communities. Resistant to abrasion, corrosion, and extreme pH or temperature, ceramic membranes provide consistent high-quality effluent, effectively removing bacteria and turbidity while preserving taste and odor. Simple production using locally available materials like clay and sawdust ensures accessibility and sustainability. With a service life of up to five years, ceramic membranes reduce operational costs and maintenance frequency, offering a scalable and reliable method for safe drinking water provision in resource-limited environments.

Advanced Water Filtration Systems Market Share Insights

Membrane Filtration Dominates with 45% Market Share

Membrane filtration systems remain the dominant technology in the advanced water filtration market, accounting for approximately 45.7% of global demand in 2025. The segment includes Reverse Osmosis (RO) for dissolved solids, Ultrafiltration (UF) for pathogens, and Nanofiltration (NF) for selective contaminant removal, offering the highest performance for both residential drinking water and high-purity industrial applications. Media filtration serves as the versatile workhorse for removing chlorine, sediment, taste/odor compounds, and VOCs, forming the backbone of many whole-house and point-of-entry systems. Hybrid systems are gaining traction as premium solutions that combine multiple technologies into a single unit, addressing broad-spectrum contaminant removal for residential, commercial, and critical industrial applications.

.png)

Residential Applications Drive 40% of Market Demand

Residential use is the largest application segment at 40.4% market share, propelled by growing consumer health awareness and concerns over tap water quality. Under-sink RO systems, whole-house filtration units, and advanced shower filters dominate the category. Industrial users rely on high-capacity, skid-mounted filtration systems to provide process water, boiler feed, and ingredient water, with stringent requirements for reliability and regulatory compliance. Commercial demand comes from hotels, offices, restaurants, and schools, where safe, palatable water is critical for guests and employees. Municipal installations incorporate ultrafiltration and nanofiltration to comply with increasingly strict regulations on pathogens and emerging contaminants like PFAS, reflecting infrastructure modernization trends.

System Configuration Trends Highlight Under-Sink & Whole-House Solutions

Under-sink units (35.8%) remain the residential performance champion, combining space efficiency with high-quality drinking water output. Whole-house systems are increasingly adopted for point-of-entry treatment, protecting plumbing, skin, and household appliances from contaminants like chlorine and sediment. Industrial skid-mounted systems dominate factory, laboratory, and commercial applications, offering modular scalability and robust performance. Municipal-scale plants serve entire communities, emphasizing membrane-based filtration for large-scale public health protection, while countertop units (~5%) target renters and portable-use scenarios.

Smart Features Enhance Performance, Monitoring, and Efficiency

Filter life indicators (30.6%) represent the most widely adopted smart feature, enabling accurate replacement alerts based on real usage rather than simple timers. IoT connectivity allows users to remotely monitor system performance, water quality, and usage statistics, supporting predictive maintenance and remote diagnostics. Real-time monitoring ensures continuous water quality assurance, while automatic flushing preserves RO membrane integrity. Cutting-edge AI-powered optimization is emerging to analyze usage patterns, optimize flush cycles, and provide water quality insights, reflecting the industry's push towards intelligent, connected filtration solutions.

Flow Rate Capacity & Price Segment Insights

Low-flow systems (<5 GPM) dominate at 45%, encompassing most under-sink and countertop units for residential drinking water. Medium-flow systems (34.9%) serve whole-house residential and small commercial needs, while high-flow systems target industrial and large commercial applications requiring custom-engineered solutions. Price segmentation shows mid-range products as the largest revenue contributor, balancing performance and affordability. Premium units offer advanced features and integrated systems for residential luxury and commercial-grade applications, while economy units address entry-level, low-cost consumer demand, and luxury/commercial-grade systems cater to high-flow industrial and high-end commercial operations.

Country Analysis of the Advanced Water Filtration Systems Market

United States: Accelerating Advanced Filtration Through Regulations and AI Integration

The United States market for advanced water filtration systems is strongly influenced by the Bipartisan Infrastructure Law, which provides significant funding for drinking water and wastewater infrastructure upgrades. The EPA’s tightening of regulations on emerging contaminants, such as PFAS (per- and polyfluoroalkyl substances), is accelerating the adoption of granular activated carbon, nanofiltration technology, and sensor-based real-time monitoring systems. A growing trend is the integration of artificial intelligence (AI) and machine learning to optimize water treatment operations, predict demand, and support predictive maintenance. Leading companies like Xylem are collaborating with utilities to deploy PFAS treatment solutions, while the Department of the Interior’s $300 million funding for water recycling and desalination projects further underscores the governmental focus on advanced water technologies. These initiatives collectively enhance the efficiency, sustainability, and compliance of advanced filtration systems across the country.

China: Policy-Driven Growth in Advanced Filtration Technologies

China’s Water Ten Plan and Beautiful China initiative are central to the nation’s drive for clean water and advanced filtration infrastructure. The government aims for 95% wastewater treatment coverage in county-level cities and a 25% water reuse rate in water-scarce areas, fueling demand for high-efficiency filtration systems. With real-time emission disclosure requirements for key enterprises, China is pushing the development of continuously monitored, IoT-enabled advanced water filtration systems. Investments exceeding RMB 673 billion between 2017 and 2022 have been allocated to water pollution control, supporting industrial parks and containerized solutions for on-site treatment and reuse. The regulatory and investment environment positions China as a major growth hub for smart, sustainable filtration technologies.

Israel: Innovation Hub for Smart and Sustainable Water Filtration

Israel’s water sector is recognized globally for its innovation, with over 130 companies developing advanced filtration, smart water management, and emergency water solutions. Research at the Technion Institute focuses on aerated soil injection for agricultural wastewater treatment, complementing advanced filtration technologies. Companies like BioCastle Water Technologies are deploying eco-friendly MBR systems, while NanoClear Water Solutions uses ProBio Media, a nano-ceramic biofiltration technology, to enhance treatment capacity by up to 40% and reduce sludge generation. Israeli desalination plants, supplying 75% of national drinking water, employ Pressure-Filtration Reverse Osmosis (PFRO), which significantly improves fouling resistance and overall efficiency, establishing Israel as a global benchmark for sustainable, high-performance water filtration systems.

India: Expanding IoT-Enabled and Modular Filtration Solutions

India’s Jal Jeevan Mission is creating a smart rural water supply ecosystem by deploying sensor-based IoT devices in over six lakh villages. Rising water scarcity is driving adoption of advanced filtration technologies across municipal and industrial sectors. The Central and State Pollution Control Boards enforce stringent effluent discharge standards under The Water (Prevention and Control of Pollution) Act, 1974, which is accelerating the deployment of membrane bioreactors (MBR) and sequencing batch reactors (SBR). Innovative solutions, including water ATMs are enhancing accessibility in rural areas. These developments highlight India’s growing investment in modular, decentralized, and high-efficiency water filtration systems.

Germany (Europe): Driving Innovation Through Regulatory Compliance and Circular Economy

Germany’s adoption of advanced water filtration systems is fueled by the EU’s Urban Wastewater Treatment Directive, which mandates treatment for communities above 1,000 population-equivalents. The directive also enforces Extended Producer Responsibility for pharmaceuticals and cosmetics, supporting advanced micropollutant removal solutions. Collaborative initiatives like the Fraunhofer-Allianz SysWasser and the German Association for Gas and Water (DVGW) are advancing system-oriented water extraction, filtration, and sustainable wastewater treatment. Germany emphasizes energy-efficient and resource-recovering filtration technologies, integrating circular economy principles while ensuring compliance and operational reliability in urban and rural areas.

United Arab Emirates: Investing in Large-Scale Solar-Powered Filtration Systems

The UAE’s Water Security Strategy 2036 and Dubai’s Integrated Water Resource Management Strategy 2030 are major drivers for advanced filtration systems, particularly in large-scale desalination projects. The Hassyan Complex employs seawater reverse osmosis (SWRO) technology with a production capacity of 180 million gallons per day, powered solely by solar energy, making it the world’s largest solar-driven desalination initiative. Researchers at Khalifa University are advancing graphene-based nanostructured membranes and solar vapor generation techniques to produce freshwater efficiently and sustainably. IoT-enabled monitoring systems are increasingly adopted in industrial, commercial, and residential applications to track water quality, pressure, and consumption in real time, reflecting a shift toward smart and energy-efficient water filtration solutions.

Competitive Landscape – Key Players Driving Technological and Market Leadership

The advanced water filtration systems market is highly competitive, with global leaders combining material science innovation, digitalization, and market diversification to maintain strategic advantage.

DuPont Water Solutions – Leading in Membrane-Based Industrial Reuse

DuPont’s competitive edge lies in high-performance membranes and ion exchange resins engineered for resilience against fouling and high removal rates for emerging contaminants. Its FilmTec™ Fortilife™ membranes are central to industrial MLD applications, while the newly launched Multibore™ PRO UF membranes offer space and cost efficiencies for desalination pretreatment. DuPont’s material science heritage enables the development of membranes with longer lifecycles and superior contaminant removal rates.

Veolia Environnement S.A. – Full Lifecycle Water Solutions with PFAS Elimination

Veolia leverages a comprehensive approach to water treatment, from process water to wastewater reuse, underpinned by membrane bioreactors (MBR), RO, and CEDI systems. Its offshore sector strength was reaffirmed with the Petrobras desalination contract, while the Drop® PFAS destruction technology positions it as a pioneer in final-stage contaminant removal. Veolia’s deep municipal and industrial expertise makes it a partner of choice for large-scale, integrated projects.

SUEZ S.A. – Circular Water Solutions and Micropollutant Mitigation

SUEZ focuses on energy-efficient filtration systems and strategic collaborations to address emerging water challenges. Its October 2024 Danish wastewater plant upgrade showcased its hybrid treatment model combining ozonation with GAC filtration. With a global footprint and a strong municipal client base, SUEZ is positioned to capitalize on the surge in micropollutant regulation across Europe and beyond.

Xylem Inc. – Smart, Modular Filtration Systems for Municipal and Industrial Clients

Xylem’s strength is in digital integration, offering modular and vendor-agnostic solutions like the Rivo™ I platform for real-time monitoring and operational optimization. By combining hardware (pumps, mixers, filters) with advanced data analytics, Xylem enables clients to achieve greater efficiency and reduced environmental impact without full system overhauls.

Pentair – Bridging Residential and Industrial Filtration Markets

Pentair balances residential brand strength with industrial growth potential. Its Porous Media acquisition expanded its portfolio in advanced membrane filtration, complementing established brands like Everpure and X-Flow. Pentair’s dual-market approach and emphasis on PFAS removal allow cross-sector technology transfers and a diverse revenue base.

Advanced Water Filtration Systems Market Report Scope

Advanced Water Filtration Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$38.2 Billion

|

|

Market Size (2034)

|

$112.9 Billion

|

|

Market Growth Rate

|

12.8%

|

|

Segments

|

By Technology Type (Membrane Filtration, Media Filtration, Electrochemical Filtration, Hybrid Systems), By Application (Residential, Commercial, Industrial, Municipal), By System Configuration (Under-Sink Units, Countertop Systems, Whole-House Installations, Industrial Skid-Mounted Systems, Municipal-Scale Plants), By Smart Features (Real-Time Monitoring, Filter Life Indicators, Automatic Flushing, IoT Connectivity, AI-Powered Optimization), By Flow Rate Capacity (Low Flow (<5 GPM), Medium Flow (5-20 GPM), High Flow (>20 GPM)), By Price Segment (Economy, Mid-Range, Premium, Luxury/Commercial Grade)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

A.O. Smith Corporation, Pentair, LG Electronics, Eureka Forbes, Kent RO Systems Ltd., Culligan Water, 3M, Panasonic Holdings Corporation, Whirlpool Corporation, Unilever, Kinetico Incorporated, Aquasana, Watts Water Technologies, BRITA, Evoqua Water Technologies (now part of Xylem)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Advanced Water Filtration Systems Market Segmentation

By Technology Type

- Membrane Filtration

- Reverse Osmosis (RO)

- Nanofiltration (NF)

- Ultrafiltration (UF)

- Microfiltration (MF)

- Forward Osmosis (FO)

- Media Filtration

- Activated Carbon

- Ceramic Filters

- Biochar Filters

- Zeolite Filters

- Graphene-Based Filters

- Electrochemical Filtration

- Hybrid Systems

By Application

- Residential

- Commercial

- Office buildings

- Hotels/restaurants

- Hospitals

- Industrial

- Food & beverage

- Pharmaceuticals

- Semiconductor manufacturing

- Metals and Mining

- Other Industries

- Municipal

By System Configuration

- Under-Sink Units

- Countertop Systems

- Whole-House Installations

- Industrial Skid-Mounted Systems

- Municipal-Scale Plants

By Smart Features

- Real-Time Monitoring

- Filter Life Indicators

- Automatic Flushing

- IoT Connectivity

- AI-Powered Optimization

By Flow Rate Capacity

- Low Flow (<5 GPM)

- Medium Flow (5-20 GPM)

- High Flow (>20 GPM)

By Price Segment

- Economy

- Mid-Range

- Premium

- Luxury/Commercial Grade

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

* List Not Exhaustive

Research Coverage

This report investigates the Global Advanced Water Filtration Systems Market, delivering in-depth analysis reviews of regulatory shifts, sustainable membrane innovations, and smart technologies driving growth. Published by USDAnalytics, the study highlights breakthrough advancements such as PFAS destruction technologies, nanofiltration and graphene-based membranes, and IoT-enabled AI-driven filtration systems that redefine water quality and compliance worldwide. It also underscores milestone contracts, acquisitions, and cross-sector partnerships, showcasing how utilities, industries, and municipalities are integrating advanced solutions to meet emerging regulatory challenges while enhancing operational efficiency. By combining technology roadmaps, contract analysis, and regional market intelligence, this report is an essential resource for industry leaders, policymakers, utilities, and technology providers navigating one of the fastest-evolving segments of the water sector.

Scope Includes:

- Segmentation: By Technology (RO, NF, UF, Hybrid Systems, Media Filtration), By Application (Residential, Commercial, Industrial, Municipal), By System Configuration (Under-Sink, Whole-House, Industrial Skid-Mounted, Municipal-Scale, Countertop), By Flow Rate Capacity (Low, Medium, High), By Smart Features (IoT, AI, Real-Time Monitoring, Auto-Flushing, Filter Life Indicators), and By Price Segment (Economy, Mid-Range, Premium, Luxury/Commercial).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic Data: 2021 to 2024, and Forecast Data: 2025 to 2034.

- Companies: Profiles and analysis of 15+ key players including DuPont, Veolia, SUEZ, Xylem, Pentair, and Kurita.

Methodology

The research methodology adopted by USDAnalytics combines primary and secondary research to deliver robust and actionable insights. Primary research involved direct interviews with utilities, industrial water managers, technology providers, and regulators to validate adoption trends, regulatory impacts, and performance metrics. Secondary research drew from company filings, government directives, international water quality standards, and peer-reviewed studies to build a comprehensive evidence base. Market sizing was established using top-down and bottom-up triangulation, aligning installation data with regulatory-driven demand and technology penetration rates. Forecasts were modeled under varying scenarios, including PFAS compliance acceleration, AI-enabled system deployment, and the rise of modular MLD systems, ensuring that projections reflect both regulatory imperatives and technological adoption curves.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Advanced Water Filtration Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Stakeholders

1.3. Global Market Snapshot

2. Advanced Water Filtration Systems Market Overview & Outlook (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $38.2 Billion

2.2.2. Forecasted Market Size (2034): $112.9 Billion at 12.8% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Stricter Environmental and Health Regulations (e.g., PFAS)

2.3.2. Integration of Smart Technologies and AI

2.3.3. Demand for Sustainable and High-Efficiency Membranes

3. Market Analysis: Contract Wins, Breakthrough Technologies, and Cross-Sector Expansion

3.1. Overview of R&D Commercialization and Strategic Partnerships

3.2. Recent Strategic Developments of Key Players

3.2.1. DuPont's FilmTec™ Fortilife™ Membranes Award (August 2025)

3.2.2. Veolia's Petrobras Desalination Contract (September 2025) and Drop® PFAS Technology

3.2.3. SUEZ's Wastewater Upgrade in Denmark (October 2024)

3.2.4. Pentair's Acquisition of Porous Media (October 2024)

3.3. Key Technology and Policy Milestones

4. Trends and Opportunities in Advanced Water Filtration Systems

4.1. Trend 1: Nanofiltration & Graphene Membranes for Selective Contaminant Removal

4.1.1. Lower Energy Consumption and High Rejection Rates

4.1.2. Targeted Removal of Emerging Pollutants like PFAS and Micropollutants

4.2. Trend 2: Surge in Point-of-Use (POU) Filtration Systems

4.2.1. Addressing Concerns over Microplastic Contamination

4.2.2. Demand for Consumer-Friendly, Comprehensive Solutions

4.3. Opportunity 1: AI-Powered Self-Cleaning Filters for Industrial Applications

4.3.1. Minimizing Downtime and Reducing Operational Costs

4.3.2. Predictive Maintenance and Enhanced Efficiency

4.4. Opportunity 2: Ceramic Membrane Filters for Developing Countries

4.4.1. Low-Cost, Durable, and Locally Producible Solutions

4.4.2. Reliable Water Purification in Resource-Limited Environments

5. Advanced Water Filtration Systems Market Share and Segmentation Insights

5.1. By Technology Type

5.1.1. Membrane Filtration Dominates with 45% Market Share

5.1.2. Media Filtration and Hybrid Systems

5.2. By Application

5.2.1. Residential Applications Drive 40% of Demand

5.2.2. Industrial, Commercial, and Municipal Segments

5.3. By System Configuration

5.3.1. Under-Sink and Whole-House Solutions Lead

5.3.2. Industrial Skid-Mounted and Municipal-Scale Plants

5.4. By Smart Features

5.4.1. Filter Life Indicators and IoT Connectivity

5.4.2. Real-Time Monitoring and AI-Powered Optimization

5.5. By Flow Rate Capacity and Price Segment

5.5.1. Low-Flow and High-Flow Systems

5.5.2. Mid-Range and Premium Price Segments

6. Country Analysis of the Advanced Water Filtration Systems Market

6.1. United States: Accelerating Advanced Filtration Through Regulations and AI

6.2. China: Policy-Driven Growth in Advanced Filtration Technologies

6.3. Israel: Innovation Hub for Smart and Sustainable Water Filtration

6.4. India: Expanding IoT-Enabled and Modular Filtration Solutions

6.5. Germany (Europe): Regulatory Compliance and Circular Economy

6.6. United Arab Emirates: Large-Scale Solar-Powered Filtration Systems

7. Competitive Landscape: Key Players Driving Innovation

7.1. DuPont Water Solutions: Leading in Membrane-Based Industrial Reuse

7.2. Veolia Environnement S.A.: Full Lifecycle Water Solutions with PFAS Elimination

7.3. SUEZ S.A.: Circular Water Solutions and Micropollutant Mitigation

7.4. Xylem Inc.: Smart, Modular Filtration Systems

7.5. Pentair: Bridging Residential and Industrial Markets

7.6. Other Key Players

8. Market Size Outlook by Region (2025–2034)

8.1. North America Market Size Outlook to 2034

8.1.1. By Technology

8.1.2. By Application

8.1.3. By System Configuration

8.2. Europe Market Size Outlook to 2034

8.2.1. By Technology

8.2.2. By Application

8.2.3. By System Configuration

8.3. Asia Pacific Market Size Outlook to 2034

8.3.1. By Technology

8.3.2. By Application

8.3.3. By System Configuration

8.4. South America Market Size Outlook to 2034

8.4.1. By Technology

8.4.2. By Application

8.4.3. By System Configuration

8.5. Middle East and Africa Market Size Outlook to 2034

8.5.1. By Technology

8.5.2. By Application

8.5.3. By System Configuration

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations