Market Overview: Rising Importance of Agricultural Wastewater Treatment

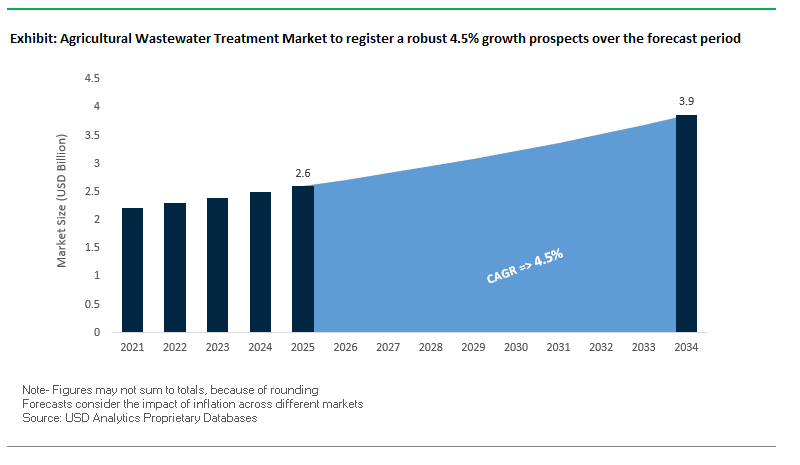

The global agricultural wastewater treatment market is projected to grow from USD 2.6 billion in 2025 to USD 3.9 billion by 2034, registering a steady CAGR of 4.5%. This growth is underpinned by increasing agricultural intensification, rising freshwater scarcity, and the urgent need for sustainable farming practices. Agricultural wastewater treatment not only reduces environmental pollution but also supports water reuse for irrigation, enabling food security in water-stressed regions.

Key insights shaping the agricultural wastewater treatment market:

- Over 80% of urban wastewater in India can potentially be reused for irrigation, alleviating pressure on scarce freshwater resources.

- Tertiary treatment technologies for removing nitrogen and phosphorus are expanding rapidly to combat nutrient pollution in agricultural runoff.

- Adoption of advanced biological systems such as anaerobic digesters and membrane bioreactors is enabling both wastewater purification and valuable byproduct recovery (biogas, fertilizers).

- Studies confirm that using treated wastewater for irrigation not only enhances soil fertility but also reduces farmers’ reliance on chemical fertilizers.

Market Analysis: Innovations, Investments, and Strategic Shifts

The agricultural wastewater treatment industry is advancing with significant investments in infrastructure, sustainability initiatives, and technological innovation. Governments, corporations, and technology providers are increasingly aligning their strategies to address wastewater reuse and circular economy goals.

In July 2025, Veolia Water Technologies advanced its "GreenUp" strategic plan by securing a contract for France’s largest treated wastewater reuse project in Argelès-sur-Mer. The facility is designed to treat 1.3 million cubic meters annually for agricultural irrigation, demonstrating the shift toward circular water use in European agriculture. Just months earlier, in May 2025, Veolia consolidated its leadership in the water solutions space by acquiring full ownership of its Water Technologies and Solutions subsidiary from CDPQ, strengthening its agricultural solutions portfolio.

Asian and North American markets are also seeing important moves. In April 2025, Kurita Water Industries introduced a new initiative to develop PFAS-free components for water treatment plants, targeting one of agriculture’s most pressing environmental concerns. This followed its December 2024 breakthrough, where Kurita successfully demonstrated electricity generation from wastewater via microbial fuel cells, opening new avenues for energy-positive treatment solutions.

The global scope of investments is equally notable. In June 2024, Kurita expanded in India by establishing Kurita AquaChemie India Private Limited (KAIL) to tap into one of the largest agricultural wastewater markets. Meanwhile, Aquacycl’s December 2023 partnership with a global food and beverage giant to deploy its BioElectrochemical Treatment Technology (BETT) showcased the potential of decentralized, modular solutions for managing high-strength agricultural wastewater.

Key Trends Driving the Agricultural Wastewater Treatment Market

Advanced Biological and Hybrid Systems for Nutrient and Pathogen Removal

The integration of biological and hybrid systems is revolutionizing agricultural wastewater treatment. A study in Frontiers in Water demonstrated that treated biosolids from wastewater can significantly enhance soil fertility, with nitrogen levels on a banana plantation in the Dominican Republic increasing from 3.7 g/kg to 9.6 g/kg and phosphorus from 1.7 g/kg to 4.1 g/kg. Hybrid systems, including microbial fuel cells (MFCs), not only remove organic contaminants and pathogens but also generate electricity as a byproduct, offering a path toward energy-neutral treatment facilities. These innovations are enabling farms to treat wastewater efficiently while recovering value-added resources.

Policy and Regulatory Frameworks Encouraging Treatment Adoption

Government mandates are increasingly shaping the agricultural wastewater treatment landscape. The European Union's Water Reuse Regulation (effective June 2023) sets minimum quality requirements for safe reuse of treated wastewater in irrigation, promoting investment in advanced treatment infrastructure. In the United States, multiple states are exploring the reuse of treated water from oil and gas operations for agriculture, requiring higher treatment standards to ensure safety and compliance. These policies are directly influencing market adoption rates and investment in innovative treatment technologies.

Decentralized and Modular Treatment Systems for Farms

Decentralized and modular wastewater treatment systems are gaining traction as flexible and cost-effective solutions for agricultural operations. California’s long-standing practice of using reclaimed municipal water for irrigating food and nursery crops exemplifies decentralized water management, conserving millions of cubic meters of freshwater annually. Companies like BioFiltro are developing compact, low-cost Biodynamic Aerobic (BIDA®) systems that remove up to 99% of wastewater contaminants within four hours. These modular solutions cater to small farms and communities, providing an alternative to centralized treatment plants and enabling localized, sustainable water management.

Agricultural Wastewater Treatment Market Share Insights

Market Share by Treatment Technology

Biological treatment dominates the market with a projected 35% share in 2025, driven by its cost-effectiveness in handling high organic loads from livestock, dairy, and food processing operations. Physical treatment (25%) remains essential as a preliminary step to remove solids such as manure fibers and food residues. Membrane-based and advanced treatment technologies (15% and 10%, respectively) are critical for producing high-quality water suitable for reuse or for meeting stringent discharge standards. Chemical treatments (15%) are used primarily for pathogen removal and nutrient polishing, particularly for phosphorus, helping prevent eutrophication and supporting compliance with environmental regulations.

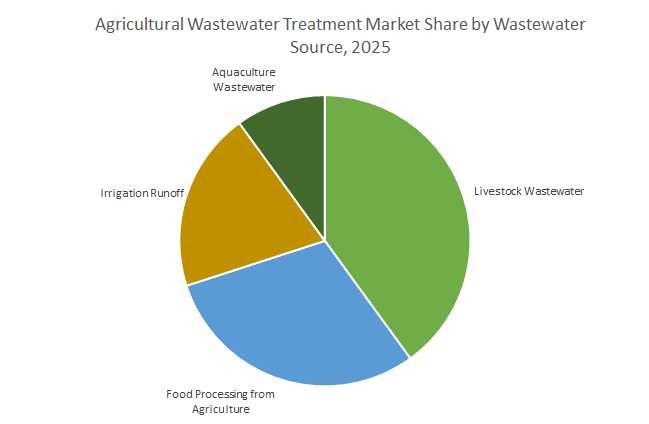

Market Share by Wastewater Source

Livestock wastewater represents the largest segment (40%), due to its high concentration of organics, nutrients, and pathogens, and is a major regulatory focus for concentrated animal feeding operations (CAFOs). Food processing wastewater (30%) is a consistent industrial stream with high organic content, treated both for compliance and for internal water reuse. Irrigation runoff presents diffuse pollution challenges, often managed through constructed wetlands or tailwater recovery systems. Aquaculture wastewater requires specialized treatment for solid removal and biofiltration to maintain water quality in recirculating systems and ensure safe discharge.

Market Share by Application

Discharge compliance leads the application segment with 45% projected market share in 2025, as regulatory mandates globally dictate safe wastewater disposal. Water reuse and recycling (30%) is increasingly adopted to reduce freshwater demand and ensure operational resilience in water-scarce regions. Nutrient recovery (15%) transforms wastewater into a valuable resource by extracting nitrogen and phosphorus for fertilizer applications, supporting the circular agriculture model. Energy generation through anaerobic digestion of high-strength organic waste further enhances the economic and environmental sustainability of agricultural wastewater treatment systems.

China: Government Investments and Membrane Production Strengthen Market

China’s agricultural wastewater treatment market is heavily influenced by stringent regulatory policies and strong government support. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge standards, aligning with the 14th Five-Year Plan’s goal of 95% wastewater treatment in all county-level cities. This has driven widespread adoption of biological treatment technologies, particularly membrane bioreactors (MBRs), in municipal and agricultural wastewater projects. The Chinese government is investing $50 billion in wastewater treatment by 2025, targeting heavy-polluting industries such as textiles, steel, and pharmaceuticals. Additionally, China has become a major producer of membrane modules, achieving approximately 85% self-sufficiency, intensifying competition with foreign suppliers and enabling lower-cost solutions for industrial and agricultural wastewater applications. MBR systems are increasingly employed in expansion and renovation projects, offering high efficiency and reduced physical footprint for sustainable water management.

United States: Federal Funding and Innovative Technologies Accelerate Adoption

The U.S. agricultural wastewater treatment market benefits from substantial federal support, technological innovation, and industry-driven solutions. Through the Bipartisan Infrastructure Law, over $50 billion has been allocated to the EPA for enhancing water infrastructure, including emerging contaminants like PFAS. Grants are awarded to universities to accelerate alternative and innovative wastewater treatment methods in lagoon and pond systems for small and rural agricultural communities. Companies such as Aquacycl have introduced modular BioElectrochemical Treatment Technology (BETT) for high BOD wastewater, while Gross-Wen Technologies utilizes Revolving Algal Biofilm Systems for nutrient recovery. The food, beverage, agriculture, and dairy sectors increasingly adopt biological treatment and resource recovery solutions, highlighting the strong application potential of advanced agricultural wastewater treatment in the U.S.

India: Government Programs and PPP Investments Drive Treatment Expansion

India’s agricultural wastewater treatment sector is driven by robust government initiatives and large-scale infrastructure investments. Programs like the Jal Jeevan Mission, Namami Gange Mission, Smart Cities Mission, and the National Mission for Clean Ganga (NMCG) accelerate the deployment and modernization of wastewater treatment facilities, with 39 new projects sanctioned in 2024 totaling ₹2,056 crore. The AMRUT mission contributes over USD 10 billion toward enhancing water supply and wastewater treatment infrastructure, leveraging public-private partnerships for large-scale projects. Advanced technologies such as sequencing batch reactors (SBR) and MBRs are increasingly adopted to achieve higher treatment efficiency. Municipalities like Pimpri Chinchwad employ SCADA-based central monitoring systems for improved operational control. Industrial sectors including power, chemicals, and textiles also drive adoption, focusing on water reuse to mitigate scarcity and comply with stringent regulations.

Germany: Regulatory Leadership and Advanced Biological Treatment Systems

Germany is a leader in agricultural wastewater treatment, guided by strict regulations and widespread adoption of biological treatment technologies. The German Federal Wastewater Charges Act enforces fees on entities discharging wastewater into water bodies, incentivizing advanced treatment adoption. Biological treatment techniques, including nitrification and denitrification, are recognized as best available technologies, applied to over 95% of treated wastewater. German companies such as PPU Umwelttechnik develop containerized membrane systems suitable for retrofitting existing tanks, providing cost-effective solutions for agricultural wastewater management and promoting sustainable water reuse practices.

Japan: Johkasou Systems and MBR Technology Enable Agricultural Reuse

Japan has a long-standing focus on advanced on-site agricultural wastewater treatment. Innovative systems like Johkasou, combining biological processes to treat blackwater and greywater, are widely deployed. The government-backed "Advance of Japan Ultimate Membrane bioreactor technology Project (A-JUMP)" promotes full-scale adoption of MBRs in medium- to large-scale treatment plants, ensuring improved conditions for reconstruction and expansion projects. In agriculture, treated wastewater is increasingly applied for irrigation and nutrient recovery, exemplifying Japan’s integration of technology-driven sustainability in the agricultural sector.

Brazil: Privatization and Investment Unlock Agricultural Wastewater Management

Brazil’s agricultural wastewater treatment market is benefiting from a new legal framework encouraging private sector participation in water infrastructure. The framework sets ambitious targets for 2033, including 99% water coverage and 90% sewage treatment, providing regulatory certainty and attracting investments. Approximately BRL 105 billion is expected across 43 privatization projects, marking one of the largest infrastructure financing efforts in Latin America. Given the country’s extensive agricultural production, particularly in central regions, these investments are critical for effective wastewater management, enabling sustainable irrigation practices and reducing conflicts over water resources.

Competitive Landscape: Leading Companies Driving Growth

The agricultural wastewater treatment market is competitive, with global leaders, regional specialists, and innovative startups reshaping how wastewater is managed and reused in farming systems. Key players are leveraging R&D, strategic partnerships, and acquisitions to expand their presence.

Veolia Water Technologies – Leading Circular Agricultural Wastewater Solutions

Veolia’s strength lies in delivering large-scale, integrated water treatment solutions. Its agricultural capabilities include advanced filtration, anaerobic digestion, and reuse technologies. In July 2025, Veolia was awarded France’s largest agricultural wastewater reuse project, underscoring its leadership in membrane ultrafiltration for irrigation water reuse. Its GreenUp plan emphasizes climate change mitigation through depollution and resource recovery, aligning closely with agriculture’s sustainability goals.

Kurita Water Industries Ltd. – Specialist in Innovative Chemical and Biological Solutions

Kurita stands out for its customized chemical and equipment-based solutions that target nutrient removal, odor control, and energy recovery. Its April 2025 launch of PFAS-free components is a major advancement for agricultural water safety. Kurita also innovated microbial fuel cells that convert wastewater into electricity, advancing energy-positive agriculture. The establishment of Kurita AquaChemie India Private Limited (2024) highlights its commitment to expanding in high-growth agricultural regions.

SUEZ – Expanding Water Reuse Capabilities in Asia and Beyond

SUEZ is a global wastewater management leader, with expertise spanning membrane bioreactors, biological nutrient removal, and seawater desalination. Its agricultural relevance lies in designing customized wastewater recycling systems for both farms and agro-industries. Recent contracts in China and the Philippines highlight its ability to handle large, complex projects, advancing 100% wastewater recycling goals that can be applied to agriculture.

DuPont Water Solutions – Material Science Powering Agricultural Membranes

DuPont brings decades of expertise in high-performance membranes, with its FilmTec™ Fortilife™ membranes earning recognition for advancing industrial and agricultural reuse efficiency. Its product portfolio spans RO, NF, and UF membranes, along with ion exchange resins, enabling integrated treatment. DuPont’s sustainability-driven strategy emphasizes water circularity, carbon footprint reduction, and operational cost savings, which directly benefit water-stressed agricultural regions.

Evoqua Water Technologies LLC – Strengthening Agricultural Applications through Xylem Integration

Evoqua, now part of Xylem (since 2023), is a major player in mission-critical water and wastewater solutions. It serves over 38,000 customers across 200,000 installations, with a strong North American footprint. Its recent launch of a Sustainability and Innovation Hub in Pittsburgh accelerates R&D into emerging contaminants like PFAS, digital monitoring, and decentralized reuse – all critical for future agricultural wastewater treatment efficiency.

Agricultural Wastewater Treatment Market Report Scope

Agricultural Wastewater Treatment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$3.9 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Treatment Technology (Physical Treatment, Biological Treatment, Membrane-Based Treatment, Chemical Treatment, Advanced Treatment), By Wastewater Source (Livestock Wastewater, Irrigation Runoff, Aquaculture Wastewater, Food Processing from Agriculture), By Application (Water Reuse & Recycling, Nutrient Recovery, Discharge Compliance, Energy Generation), By End-Use (Crop Farms, Livestock Farms & Dairy Units, Aquaculture Farms, Agro-Processing Units, Agricultural Cooperatives & Community Wastewater Facilities), By System Configuration (Centralized Treatment Systems, Decentralized / On-Site Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, Pentair plc, DuPont de Nemours, Inc., Toray Industries, Inc., Aquatech International, Kubota Corporation, The Dow Chemical Company, V.A. TECH WABAG Ltd., Mitsubishi Chemical Corporation, Kuraray Co., Ltd., Nalco Water (An Ecolab Company), Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Agricultural Wastewater Treatment Market Segmentation

By Treatment Technology

- Physical Treatment

- Sedimentation & Clarification

- Screening & Grit Removal

- Sand & Multimedia Filtration

- Biological Treatment

- Constructed Wetlands

- Activated Sludge Systems

- Anaerobic Digesters & Lagoons

- Sequencing Batch Reactors (SBR)

- Moving Bed Biofilm Reactors (MBBR)

- Membrane-Based Treatment

- Microfiltration (MF)

- Ultrafiltration (UF)

- Nanofiltration (NF)

- Reverse Osmosis (RO)

- Membrane Bioreactors (MBR)

- Chemical Treatment

- Coagulation & Flocculation

- Neutralization & pH Adjustment

- Disinfection (Chlorination, Ozonation, UV)

- Advanced Treatment

- Advanced Oxidation Processes (AOPs)

- Electrocoagulation & Electro-oxidation

- Nutrient Recovery & Recycling

By Wastewater Source

- Livestock Wastewater

- Irrigation Runoff

- Aquaculture Wastewater

- Food Processing from Agriculture

By Application

- Water Reuse & Recycling

- Nutrient Recovery

- Discharge Compliance

- Energy Generation

By End-Use

- Crop Farms

- Livestock Farms & Dairy Units

- Aquaculture Farms

- Agro-Processing Units

- Agricultural Cooperatives & Community Wastewater Facilities

By System Configuration

- Centralized Treatment Systems

- Decentralized / On-Site Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Agricultural Wastewater Treatment Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- Pentair plc

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Aquatech International

- Kubota Corporation

- The Dow Chemical Company

- V.A. TECH WABAG Ltd.

- Mitsubishi Chemical Corporation

- Kuraray Co., Ltd.

- Nalco Water (An Ecolab Company)

- Thermax Limited

*- List not Exhaustive

Research Coverage

This report investigates the Agricultural Wastewater Treatment Market, delivering analysis reviews on demand drivers, policy shifts, and technology breakthroughs that are reshaping nutrient removal, reuse quality, and farm-scale economics. Produced by USDAnalytics, it highlights how advanced biological systems, membrane-enabled polishing, and modular/decentralized plants convert agricultural effluents into reliable irrigation resources while lowering OPEX and emissions. With clear benchmarking of upgrade pathways, ROI levers, and compliance strategies, this report is an essential resource for agri-processors, farmer cooperatives, utilities, and EPCs planning retrofits or greenfield deployments through 2034. Scope Includes-

- Segmentation:

- By Treatment Technology: Physical (Sedimentation & Clarification; Screening & Grit Removal; Sand & Multimedia Filtration); Biological (Constructed Wetlands; Activated Sludge; Anaerobic Digesters & Lagoons; SBR; MBBR); Membrane-Based (MF, UF, NF, RO, MBR); Chemical (Coagulation & Flocculation; Neutralization & pH; Disinfection Chlorination/Ozone/UV); Advanced (AOPs; Electrocoagulation/Electro-oxidation; Nutrient Recovery & Recycling).

- By Wastewater Source: Livestock Wastewater; Irrigation Runoff; Aquaculture Wastewater; Food Processing from Agriculture.

- By Application: Water Reuse & Recycling; Nutrient Recovery; Discharge Compliance; Energy Generation.

- By End-Use: Crop Farms; Livestock Farms & Dairy Units; Aquaculture Farms; Agro-Processing Units; Agricultural Cooperatives & Community Facilities.

- By System Configuration: Centralized Treatment Systems; Decentralized / On-Site Systems.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Data Coverage: Historic data 2021–2024 and forecast data 2025–2034.

- Companies (Profiles of 15+ companies): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; Pentair plc; DuPont de Nemours, Inc.; Toray Industries, Inc.; Aquatech International; Kubota Corporation; The Dow Chemical Company; V.A. TECH WABAG Ltd.; Mitsubishi Chemical Corporation; Kuraray Co., Ltd.; Nalco Water (An Ecolab Company); Thermax Limited.

Methodology

USDAnalytics applies a mixed top-down/bottom-up approach, sizing demand by technology, source, application, end-use, and system configuration at the country level, then triangulating with agricultural water balances, fertilizer prices, energy tariffs, and PPP/tender pipelines. Primary research includes structured interviews with farm operators, cooperative boards, utilities, OEMs, and EPC integrators to validate CAPEX/OPEX ranges, performance deltas (TN/TP removal, pathogen log-reduction, SDI, kWh/m³), and payback periods for centralized and modular deployments. Secondary inputs span regulatory frameworks (reuse/nutrient limits), project databases, vendor specifications, and peer-reviewed literature to benchmark KPIs for wetlands, anaerobic digestion, SBR/MBBR/MBR, membranes, AOPs, and nutrient-recovery units. Scenario modeling stress-tests sensitivities to drought frequency, effluent standards, energy and chemical costs, and sludge valorization revenues to produce robust 2025–2034 forecasts.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Agricultural Wastewater Treatment Market

1. Executive Summary

1.1. Market Highlights and Key Projections

1.2. Key Insights: Market Drivers and Technology Trends

1.3. Global Market Snapshot

1.3.1. Current Market Valuation (2025): USD 2.6 Billion

1.3.2. Projected Market Valuation (2034): USD 3.9 Billion

1.3.3. Compound Annual Growth Rate (CAGR): 4.5%

2. Market Outlook (2025–2034)

2.1. Introduction: Rising Importance of Agricultural Wastewater Treatment

2.2. Market Valuation and Growth Projections (2025–2034)

2.3. Key Trends Driving the Agricultural Wastewater Treatment Market

2.3.1. Advanced Biological and Hybrid Systems for Nutrient and Pathogen Removal

2.3.2. Policy and Regulatory Frameworks Encouraging Treatment Adoption

2.3.3. Decentralized and Modular Treatment Systems for Farms

3. Innovations and Strategic Developments Redefining the Market

3.1. Market Analysis: Key Innovations, Investments, and Strategic Shifts

3.1.1. Veolia Secures France's Largest Agricultural Wastewater Reuse Project (July 2025)

3.1.2. Kurita Water Industries Pioneers PFAS-Free Components and Energy-Positive Solutions (April 2025)

3.1.3. Aquacycl Expands with BioElectrochemical Treatment Technology (BETT)

3.1.4. Other Strategic Investments and Global Partnerships (2024-2025)

4. Competitive Landscape: Leading Companies Driving Growth

4.1. Competitive Overview: Global Leaders and Regional Specialists

4.2. Strategic Profiles of Key Companies

4.2.1. Veolia Water Technologies: Leading Circular Agricultural Wastewater Solutions

4.2.2. Kurita Water Industries Ltd.: Specialist in Innovative Chemical and Biological Solutions

4.2.3. SUEZ: Expanding Water Reuse Capabilities in Asia and Beyond

4.2.4. DuPont Water Solutions: Material Science Powering Agricultural Membranes

4.2.5. Evoqua Water Technologies LLC: Strengthening Agricultural Applications through Xylem Integration

5. Agricultural Wastewater Treatment Market – Segmentation Insights (2025)

5.1. By Treatment Technology

5.1.1. Biological Treatment (35% Market Share)

5.1.2. Physical Treatment (25% Market Share)

5.1.3. Chemical Treatment (15% Market Share)

5.1.4. Membrane-Based and Advanced Treatment (25% Market Share)

5.2. By Wastewater Source

5.2.1. Livestock Wastewater (40% Market Share)

5.2.2. Food Processing from Agriculture (30% Market Share)

5.2.3. Irrigation Runoff

5.2.4. Aquaculture Wastewater

5.3. By Application

5.3.1. Discharge Compliance (45% Market Share)

5.3.2. Water Reuse & Recycling (30% Market Share)

5.3.3. Nutrient Recovery (15% Market Share)

5.3.4. Energy Generation

5.4. By End-Use

5.4.1. Crop Farms

5.4.2. Livestock Farms & Dairy Units

5.4.3. Aquaculture Farms

5.4.4. Agro-Processing Units

5.4.5. Agricultural Cooperatives & Community Wastewater Facilities

5.5. By System Configuration

5.5.1. Centralized Treatment Systems

5.5.2. Decentralized / On-Site Systems

6. Country Analysis: Agricultural Wastewater Treatment Market

6.1. China: Government Investments and Membrane Production Strengthen Market

6.2. United States: Federal Funding and Innovative Technologies Accelerate Adoption

6.3. India: Government Programs and PPP Investments Drive Treatment Expansion

6.4. Germany: Regulatory Leadership and Advanced Biological Treatment Systems

6.5. Japan: Johkasou Systems and MBR Technology Enable Agricultural Reuse

6.6. Brazil: Privatization and Investment Unlock Agricultural Wastewater Management

6.7. Other Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Market Outlook

7.1.1. By Treatment Technology

7.1.2. By Wastewater Source

7.1.3. By Application

7.2. Europe Market Outlook

7.2.1. By Treatment Technology

7.2.2. By Wastewater Source

7.2.3. By Application

7.3. Asia Pacific Market Outlook

7.3.1. By Treatment Technology

7.3.2. By Wastewater Source

7.3.3. By Application

7.4. South America Market Outlook

7.4.1. By Treatment Technology

7.4.2. By Wastewater Source

7.4.3. By Application

7.5. Middle East & Africa Market Outlook

7.5.1. By Treatment Technology

7.5.2. By Wastewater Source

7.5.3. By Application

8. Company Profiles: Leading Players

8.1. Veolia

8.2. SUEZ

8.3. Xylem Inc.

8.4. Evoqua Water Technologies

8.5. Pentair plc

8.6. DuPont de Nemours, Inc.

8.7. Toray Industries, Inc.

8.8. Aquatech International

8.9. Kubota Corporation

8.10. The Dow Chemical Company

8.11. V.A. TECH WABAG Ltd.

8.12. Mitsubishi Chemical Corporation

8.13. Kuraray Co., Ltd.

8.14. Nalco Water (An Ecolab Company)

8.15. Thermax Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures