Market Overview: Strong Growth Driven by Water Scarcity, Industrial Needs, and Technological Advancements

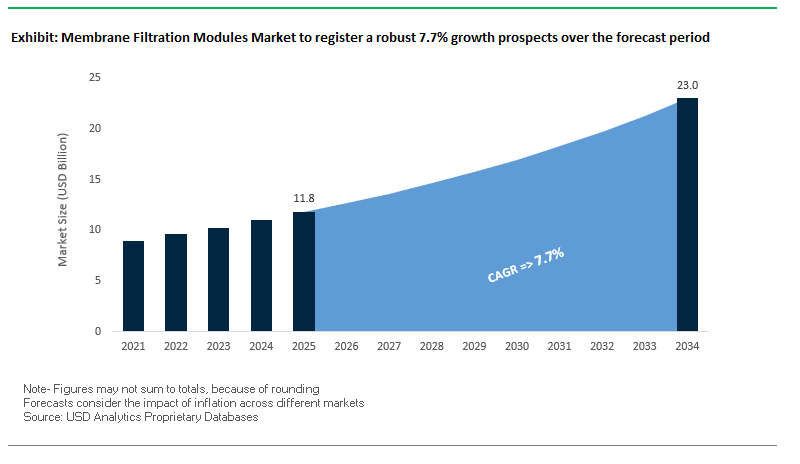

The global membrane filtration modules market is projected to grow from USD 11.8 billion in 2025 to USD 23 billion by 2034, reflecting a robust CAGR of 7.7%. This growth is driven by increasing demand for high-quality water, stricter regulatory frameworks, and expanding industrial applications in food, beverage, pharmaceuticals, and wastewater treatment. Membrane filtration modules function by separating particles and contaminants through size exclusion, ensuring consistent purity levels while reducing energy and chemical use compared to conventional treatment processes.

Key Insights Shaping the Market

- Spiral wound modules dominate due to their compact design, high efficiency, and proven performance in reverse osmosis (RO) and nanofiltration (NF) systems.

- Polymeric membranes hold the largest share, balancing cost, durability, and broad applicability across industrial and municipal treatment.

- Food and beverage applications are rapidly expanding, with membranes increasingly used for sterilizing milk, clarifying juices, and enabling low-alcohol beverages.

- Reverse osmosis (RO) and ultrafiltration (UF) are the most widely deployed technologies, crucial for desalination, high-purity industrial water, and municipal wastewater treatment.

- Asia-Pacific leads adoption, with China and India driving growth through industrial expansion, stricter wastewater regulations, and heavy investments in clean water infrastructure.

Market Analysis: Recent News and Developments Reshaping the Industry

The membrane filtration modules market is marked by continuous innovation, capacity expansion, and cross-industry applications that demonstrate the versatility of the technology. Recent developments indicate strong momentum in municipal, industrial, and even extraterrestrial applications, underscoring the wide adaptability of membranes across diverse environments. Industry leaders are investing in next-generation products to improve biofouling resistance, optimize energy efficiency, and extend the lifespan of modules, which are critical factors for operators aiming to reduce total cost of ownership.

Another defining trend is the growing role of partnerships and acquisitions in expanding global footprints. Leading players such as Veolia, SUEZ, DuPont, and Toray are securing contracts in high-growth regions, while also collaborating with scientific institutions and space research agencies to push the boundaries of what membrane technology can achieve. This pattern highlights how the industry is shifting from simply providing filtration solutions to becoming enablers of sustainable development, renewable energy generation, and even extraterrestrial exploration.

Recent Strategic Developments

- July 2025: Veolia Water Technologies awarded contract for a large municipal wastewater reuse project in Brazil, showcasing advanced membranes for water reclamation.

- May 2025: Veolia acquired full ownership of Water Technologies & Solutions from CDPQ, simplifying its structure and accelerating innovation.

- April 2025: SUEZ and CNRS signed a five-year research partnership to advance sustainable water technologies, signaling stronger R&D integration in Europe.

- January 2025: DuPont launched FilmTec™ Fortilife™ CR membranes designed for high biofouling industrial reuse, strengthening its anti-fouling product line.

- November 2024: Kurita partnered with ispace to test water purification in lunar conditions, demonstrating space-grade versatility of its filtration modules.

- October 2024: Toray supplied RO and UF membranes to a refinery project in Indonesia, reinforcing its strength in industrial process water treatment.

- October 2024: Veolia contracted to provide MemGas™ membrane technology in San Francisco for renewable natural gas production from wastewater biogas.

- June 2024: Asahi Kasei launched a membrane-based sterile water system for pharmaceuticals, offering energy-efficient alternatives to distillation.

Emerging Trends and Strategic Opportunities in the Membrane Filtration Modules Market

Innovation in Advanced Membrane Materials and Configurations

One of the most defining trends is the integration of nanomaterials into polymeric membranes to improve fouling resistance, energy efficiency, and service life. For instance, studies published in ACS Applied Materials & Interfaces highlight the use of graphene and carbon nanotubes to create membranes with higher hydrophilicity and anti-fouling performance. A flat-sheet advanced polymeric membrane demonstrated 98.4% protein removal, proving the improved separation performance and extended cleaning cycles. This underscores how material innovation is central to cost reduction and operational stability in filtration modules.

Expansion into Decentralized and Modular Water Treatment Systems

The global shift toward modular and decentralized water treatment solutions is accelerating adoption of membrane filtration modules. Their compact, scalable design makes them ideal for rural infrastructure, emergency relief, and fast-growing industrial hubs. NX Filtration’s deployment of hollow-fiber nanofiltration modules in Saudi Arabia illustrates this trend, with repeat orders to double plant capacity showcasing the scalability advantage. Such systems reduce civil construction costs and lead times, directly aligning with global water resilience strategies.

Strategic Investments, Mergers, and Acquisitions

Industry consolidation is shaping the competitive landscape of the membrane modules market. Leading water technology firms are expanding manufacturing capacities and acquiring niche players to diversify their product portfolios. A notable case includes a global water solutions company’s acquisition of a specialized ceramic membrane manufacturer, strengthening its position in the high-durability industrial filtration segment. These strategic mergers highlight strong confidence in the long-term profitability of specialized, high-performance filtration modules.

Market Share Analysis of Membrane Filtration Modules

Market Share by Technology

Reverse Osmosis (RO) dominates with 35% market share, driven by its indispensable role in seawater desalination and ultra-pure water production. Despite high energy costs, RO remains non-negotiable in regions facing acute water scarcity, making it the revenue leader of the sector. Ultrafiltration (UF) follows with 28% share, acting as the “workhorse” of water treatment and a critical pre-treatment for RO. Microfiltration (MF) holds 20% share, widely applied in food & beverage and biopharma, while Nanofiltration (NF) at 17% is the fastest-growing segment, gaining traction in water softening and food concentration processes.

Market Share by Material

Polymeric membranes dominate with 80% share, cementing their role as the cost-effective and versatile choice across municipal, industrial, and desalination plants. Ceramic membranes, while holding only 12%, are rapidly expanding in harsh industrial environments due to superior durability, thermal resistance, and ease of cleaning. Composite membranes account for 8%, but their ability to combine ceramic robustness with polymer affordability positions them as the innovation frontier for next-generation membrane modules.

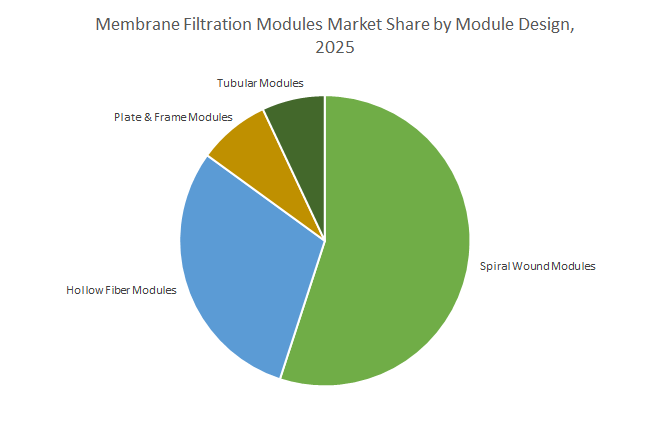

Market Share by Module Design

Spiral wound modules hold the largest share at 55%, serving as the standard for RO and NF systems due to their high packing density and cost-effectiveness. Hollow fiber modules follow with 30%, widely used in UF and MF applications, offering a high surface-area-to-volume ratio. Plate & frame modules at 8% serve niche applications with high fouling potential, such as dairy and food processing, where cleanability outweighs footprint efficiency. Tubular modules account for 7%, dominating in challenging feeds with high viscosity or solids content, including pigments and industrial wastewater.

China: Regulatory Push and Technological Leadership Driving Membrane Module Adoption

China’s membrane filtration modules market is strongly influenced by stringent regulatory policies and technological innovation. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge standards, driving companies to adopt advanced membrane filtration technologies. The government’s "Guiding Opinions on Promoting the Utilization of Wastewater Resources" emphasizes achieving a recycled water utilization rate of 25% or more in water-scarce cities by 2025, with modular membrane systems playing a central role. Technological advancements include a dual-functional reverse osmosis (RO) membrane developed in 2024 by the Chinese Academy of Sciences, featuring enhanced antibacterial and anti-adhesion properties ideal for modular applications. China has also achieved approximately 85% production localization of membrane modules, enabling local companies to compete aggressively with foreign players, particularly in industrial wastewater treatment replacement projects. Municipal wastewater treatment is increasingly leveraging membrane bioreactors (MBRs) housed in modular systems to meet strict discharge standards while minimizing footprint, highlighting China’s rapid adoption of advanced filtration solutions.

United States: Government Funding and Innovative Membrane Solutions for Critical Applications

The United States market for membrane filtration modules is propelled by government investment, academic R&D, and corporate innovations. Through the Bipartisan Infrastructure Law, over $50 billion is allocated to the EPA to enhance national water infrastructure, including technologies that address emerging contaminants such as PFAS, driving demand for advanced membrane filtration modules. Public-private partnerships like the National Alliance for Water Innovation (NAWI), funded by the Department of Energy, focus on reducing the cost and energy requirements of desalination while developing membranes for waste-brine treatment and renewable-powered plants. Corporations such as ZwitterCo are expanding their portfolios with zwitterionic membranes that offer superior fouling resistance for industrial applications. Key applications in the U.S. include dialysis centers and biologics manufacturing, where modular membrane filtration is critical for monoclonal antibodies, cell and gene therapies, and mRNA-based drug production, reinforcing the country’s leadership in high-performance membrane technologies.

India: Infrastructure Investments and Rural Water Technology Driving Market Growth

India is advancing its membrane filtration modules market through government initiatives and strategic infrastructure investments. The “Jal Jeevan Mission” promotes membrane technology adoption in rural areas, while the Department of Science & Technology’s Water Technology Initiative supports R&D in nano-material and filtration technologies to provide affordable, safe drinking water. The Ghaziabad Nagar Nigam raised ₹150 crore through India’s first Certified Green Municipal Bond to establish a Tertiary Sewage Treatment Plant (TSTP) utilizing advanced membrane filtration modules for industrial water reuse. Industrial applications are also expanding; in July 2025, Kakinada SEZ announced a ₹1,310 crore investment for a 3x50 MLD desalination plant in Andhra Pradesh, reducing reliance on freshwater and showcasing membrane filtration modules’ versatility in municipal and industrial settings.

Germany: Industrial Expertise and Advanced Ceramic Membranes Enhancing Filtration Efficiency

Germany’s membrane filtration modules market benefits from robust industrial applications and technological innovations. PWT Wassertechnik specializes in advanced membrane processes for industrial wastewater treatment and reuse, ensuring compliance with stringent European environmental regulations. The German firm CERAFILTEC announced in 2024 the deployment of ceramic flat membranes for MBR projects across four continents, ranging from 250 m³/d industrial units to 10,000 m³/d municipal systems. Companies like MANN+HUMMEL are focusing on innovative membrane and digital solutions that address global water challenges, integrating modular filtration systems into industrial process applications and green energy initiatives, reinforcing Germany’s leadership in high-efficiency, biofouling-resistant membrane technologies.

Japan: Academic Research and High-Performance Membrane Modules for Biopharmaceuticals

Japan remains a global leader in membrane filtration modules, supported by academic research, corporate innovation, and government funding. In 2025, Toray Industries developed a high-efficiency separation membrane module for biopharmaceutical manufacturing, offering more than double the filtration performance of conventional systems by minimizing clogging. The Ministry of the Environment allocated USD 1.2 billion in 2024 to promote sustainable infrastructure, including wastewater treatment systems integral to MBR technology. Japan has over 3,000 full-scale MBR applications, ranging from small-scale industrial and household systems to large municipal plants. Companies like Metawater employ ceramic membrane filtration systems to deliver high-quality tap water by removing impurities and turbidity, demonstrating the effectiveness of modular membrane systems in municipal and industrial water treatment.

Saudi Arabia: Strategic RO Investments and Regional Expansion Driving Market Leadership

Saudi Arabia is a key market for membrane filtration modules, driven by large-scale RO infrastructure investments and regional technology expansion. ACWA Power is constructing the Jubail 3A desalination plant, an independent water project (IWP) producing 600,000 cubic meters of freshwater daily using RO technology. The Saline Water Conversion Corporation (SWCC) is advancing energy-efficient RO membranes, as demonstrated at the Yanbu 4 plant, which produces 450,000 cubic meters per day, contributing to sustainable water management objectives. In June 2025, Toray Industries established a Water Treatment Technology Center in Saudi Arabia to serve the Middle East, Africa, and neighboring regions, underscoring the country’s growing importance in the global membrane filtration modules market and facilitating the deployment of advanced modular RO systems.

Competitive Landscape: Leaders Driving Innovation and Global Adoption

The competitive landscape of the membrane filtration modules market is shaped by a mix of global water giants and specialized technology innovators. Companies compete on performance, durability, energy efficiency, and integration capabilities. What differentiates leaders is their ability to deliver end-to-end solutions, invest in cutting-edge R&D, and align with sustainability megatrends. Below is a closer look at the top players reshaping the market.

SUEZ – Water Technologies & Solutions

SUEZ has built a global reputation as a provider of comprehensive water and wastewater treatment solutions, with a strong focus on membrane systems. Its recent commissioning of a large-scale seawater desalination plant for Wanhua Chemical Group in China demonstrates its industrial influence. The company’s product line spans RO, UF, and MBR systems, supported by predictive analytics and digital optimization tools. By integrating digital monitoring, SUEZ enhances system reliability and lowers operational costs, strengthening its market positioning.

DuPont Water Solutions

DuPont’s FilmTec™ membranes remain an industry benchmark in reverse osmosis and nanofiltration. Its portfolio includes RO, UF, and ion exchange resins, with strong penetration in desalination, industrial reuse, and food and beverage processing. Recent launches of anti-fouling membranes underscore its innovation-driven strategy. DuPont’s focus on energy efficiency and lifecycle cost reduction ensures its relevance in regions with rising operational cost pressures, particularly in industrial markets.

Toray Industries, Inc.

Toray leverages its expertise in synthetic polymer chemistry to deliver high-performance membranes used across desalination, industrial wastewater, and food processing. Its establishment of a Water Treatment Technology Center in Saudi Arabia signals deeper engagement in the Middle East, a critical hub for water-scarce economies. Toray’s involvement in a solar-powered desalination project further underscores its alignment with sustainability and renewable energy integration.

Veolia Water Technologies

Veolia positions itself as a leader in ecological transformation, delivering large-scale municipal and industrial water solutions. Its portfolio spans RO, UF, and specialized energy-efficient membrane systems. Recent projects in the semiconductor and energy sectors highlight its strategic pivot toward high-purity applications. Veolia also stands out for integrating circular economy principles, such as its biogas-to-renewable natural gas project in San Francisco using membrane modules.

Kurita Water Industries Ltd.

Kurita blends chemical expertise, digital services, and membrane solutions into holistic water management strategies. Its innovative projects, such as collaborating with JAXA and ispace for water purification in space, demonstrate both technological leadership and future-oriented thinking. By focusing on difficult water conditions and niche industrial challenges, Kurita strengthens its value proposition as a premium solution provider in specialized markets.

Membrane Filtration Modules Market Report Scope

Membrane Filtration Modules Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.8 Billion

|

|

Market Size (2034)

|

$23 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Technology (Reverse Osmosis (RO), Ultrafiltration (UF), Microfiltration (MF), Nanofiltration (NF) ), By Material (Polymeric Membranes, Ceramic Membranes, Composite Membranes), By Module Design (Hollow Fiber Modules, Spiral Wound Modules, Tubular Modules, Plate & Frame Modules), By Application (Water & Wastewater Treatment, Food & Beverage Processing, Pharmaceutical & Biotechnology, Chemical & Petrochemical, Power Generation, Oil & Gas, Others (textiles, mining, pulp & paper) ), By End-User (Municipal, Industrial, Residential & Commercial), By Flow Rate / Capacity (Low-Capacity Modules, Medium-Capacity Modules, High-Capacity Modules)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Toray Industries, Inc., SUEZ, Veolia, Pentair plc, Xylem Inc., The Dow Chemical Company, Koch Industries, LG Chem, Evoqua Water Technologies, MANN+HUMMEL, Asahi Kasei Corporation, Kubota Corporation, Kuraray Co., Ltd., Mitsubishi Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Membrane Filtration Modules Market Segmentation

By Technology

- Reverse Osmosis (RO)

- Ultrafiltration (UF)

- Microfiltration (MF)

- Nanofiltration (NF)

By Material

- Polymeric Membranes

- Polyethersulfone (PES)

- Polyvinylidene Fluoride (PVDF)

- Polysulfone (PS)

- Polyacrylonitrile (PAN)

- Others

- Ceramic Membranes

- Composite Membranes

By Module Design

- Hollow Fiber Modules

- Spiral Wound Modules

- Tubular Modules

- Plate & Frame Modules

By Application

- Water & Wastewater Treatment

- Food & Beverage Processing

- Pharmaceutical & Biotechnology

- Chemical & Petrochemical

- Power Generation

- Oil & Gas

- Others (textiles, mining, pulp & paper)

By End-User

- Municipal

- Industrial

- Residential & Commercial

By Flow Rate / Capacity

- Low-Capacity Modules

- Medium-Capacity Modules

- High-Capacity Modules

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Membrane Filtration Modules Industry include-

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- SUEZ

- Veolia

- Pentair plc

- Xylem Inc.

- The Dow Chemical Company

- Koch Industries

- LG Chem

- Evoqua Water Technologies

- MANN+HUMMEL

- Asahi Kasei Corporation

- Kubota Corporation

- Kuraray Co., Ltd.

- Mitsubishi Chemical Corporation

*- List not Exhaustive

Research Coverage

This report investigates the global Membrane Filtration Modules Market in depth, offering comprehensive analysis reviews, breakthroughs in material science, and strategic highlights shaping the industry. Produced by USDAnalytics, this report is an essential resource for industry professionals, policymakers, and technology providers aiming to understand the growth outlook, competitive strategies, and regulatory shifts that define this high-impact sector. It highlights advancements in reverse osmosis (RO), ultrafiltration (UF), microfiltration (MF), and nanofiltration (NF) technologies, the rising role of polymeric and ceramic membranes, and the growing adoption across municipal, industrial, and residential sectors. With a focus on water scarcity challenges, industrial wastewater reuse, and technological innovation, this study underscores how membrane modules are transforming into a strategic enabler of sustainable development and industrial efficiency. Scope Includes-

- Segmentation: By Technology (RO, UF, MF, NF), By Material (Polymeric, Ceramic, Composite), By Module Design (Hollow Fiber, Spiral Wound, Tubular, Plate & Frame), By Application (Water & Wastewater, Food & Beverage, Pharma & Biotech, Chemical & Petrochemical, Power, Oil & Gas, Others), By End-User (Municipal, Industrial, Residential & Commercial), By Flow Rate (Low, Medium, High-Capacity).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies Covered: Analysis and profiles of 15+ companies including DuPont de Nemours, Toray Industries, SUEZ, Veolia, Pentair, Xylem, Dow Chemical, Koch Industries, LG Chem, Evoqua Water Technologies, MANN+HUMMEL, Asahi Kasei, Kubota, Kuraray, and Mitsubishi Chemical Corporation.

Methodology

The research methodology integrates a blend of primary and secondary approaches to ensure data accuracy and industry relevance. Primary research includes structured interviews with executives, engineers, and decision-makers across utilities, manufacturing, and industrial end-users of membrane modules. Secondary research draws from company reports, government policies, R&D publications, and global trade databases to validate market trends and competitive movements. Quantitative analysis leverages bottom-up and top-down approaches to estimate market size across technologies, applications, and regions, while qualitative assessments highlight emerging opportunities, regulatory frameworks, and innovation trends. Triangulation was applied at every stage to ensure consistency across demand-side data, supply-side performance, and macroeconomic indicators, resulting in a robust forecast from 2025 to 2034.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Membrane Filtration Modules Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

2. Membrane Filtration Modules Market Outlook (2025–2034)

2.1. Market Overview: Growth Driven by Water Scarcity and Industrial Needs

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): USD 11.8 Billion

2.2.2. Forecasted Market Size (2034): USD 23 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 7.7%

2.3. Emerging Trends and Strategic Opportunities

2.3.1. Innovation in Advanced Membrane Materials and Configurations

2.3.2. Expansion into Decentralized and Modular Water Treatment Systems

2.3.3. Strategic Investments, Mergers, and Acquisitions

3. Recent Developments Reshaping the Industry

3.1. Market Analysis: Recent News and Strategic Developments

3.1.1. Veolia Awarded Large Municipal Wastewater Reuse Contract in Brazil (July 2025)

3.1.2. Veolia Acquires Full Ownership of Water Technologies & Solutions (May 2025)

3.1.3. SUEZ and CNRS Sign Five-Year Research Partnership (April 2025)

3.1.4. DuPont Launches FilmTec™ Fortilife™ CR Membranes (January 2025)

3.1.5. Kurita Partners with ispace for Lunar Water Purification Test (November 2024)

3.1.6. Toray Supplies Membranes for Indonesian Refinery Project (October 2024)

3.1.7. Veolia Contracts MemGas™ Technology for Biogas Production (October 2024)

3.1.8. Asahi Kasei Launches Membrane-Based Sterile Water System (June 2024)

4. Membrane Filtration Modules Market Competitive Landscape: Leading Players

4.1. Market Overview: Focus on Performance, Durability, and Innovation

4.2. Profiles of Leading Players

4.2.1. SUEZ Water Technologies & Solutions

4.2.2. DuPont Water Solutions

4.2.3. Toray Industries, Inc.

4.2.4. Veolia Water Technologies

4.2.5. Kurita Water Industries Ltd.

5. Membrane Filtration Modules Market Market Share Analysis by Segment

5.1. Market Share by Technology

5.1.1. Reverse Osmosis (RO)

5.1.2. Ultrafiltration (UF)

5.1.3. Microfiltration (MF)

5.1.4. Nanofiltration (NF)

5.2. Market Share by Material

5.2.1. Polymeric Membranes

5.2.2. Ceramic Membranes

5.2.3. Composite Membranes

5.3. Market Share by Module Design

5.3.1. Spiral Wound Modules

5.3.2. Hollow Fiber Modules

5.3.3. Plate & Frame Modules

5.3.4. Tubular Modules

6. Country Analysis and Outlook

6.1. China: Regulatory Push and Technological Leadership

6.2. United States: Government Funding and Innovative Solutions

6.3. India: Infrastructure Investments and Rural Water Technology

6.4. Germany: Industrial Expertise and Advanced Ceramic Membranes

6.5. Japan: Academic Research and High-Performance Modules

6.6. Saudi Arabia: Strategic RO Investments and Regional Expansion

6.7. Other Key Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

- By Technology

- By Material

- By Module Design

- By Application

- By End-User

- By Flow Rate / Capacity

7.2. Europe Market Size Outlook to 2034

- By Technology

- By Material

- By Module Design

- By Application

- By End-User

- By Flow Rate / Capacity

7.3. Asia Pacific Market Size Outlook to 2034

- By Technology

- By Material

- By Module Design

- By Application

- By End-User

- By Flow Rate / Capacity

7.4. South America Market Size Outlook to 2034

- By Technology

- By Material

- By Module Design

- By Application

- By End-User

- By Flow Rate / Capacity

7.5. Middle East and Africa Market Size Outlook to 2034

- By Technology

- By Material

- By Module Design

- By Application

- By End-User

- By Flow Rate / Capacity

8. Company Profiles: Top Players

8.1. DuPont de Nemours, Inc.

8.2. Toray Industries, Inc.

8.3. SUEZ

8.4. Veolia

8.5. Pentair plc

8.6. Xylem Inc.

8.7. The Dow Chemical Company

8.8. Koch Industries

8.9. LG Chem

8.10. Evoqua Water Technologies

8.11. MANN+HUMMEL

8.12. Asahi Kasei Corporation

8.13. Kubota Corporation

8.14. Kuraray Co., Ltd.

8.15. Mitsubishi Chemical Corporation

9. Methodology and Appendix

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables