Biofouling-Resistant Membranes Market Overview: Growth Outlook and Strategic Importance

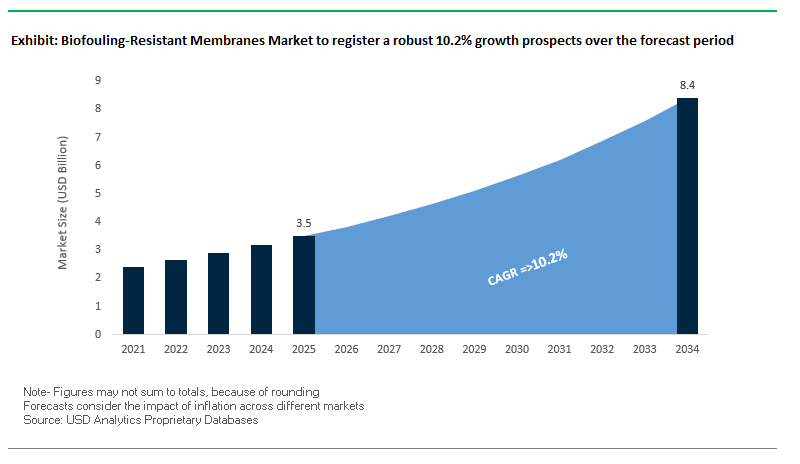

The global biofouling-resistant membranes market is poised for robust expansion, projected to grow from USD 3.5 billion in 2025 to USD 8.4 billion by 2034, registering a CAGR of 10.2%. This growth underscores the urgent demand for sustainable and efficient water treatment solutions, particularly in regions where water scarcity, industrial wastewater management, and municipal treatment are critical priorities.

Biofouling continues to be one of the most persistent challenges in membrane-based filtration systems, reducing efficiency, raising operational costs, and increasing downtime. With industries and municipalities seeking cost-effective and reliable filtration, biofouling-resistant membranes have emerged as a transformative solution.

Key Insights Driving Market Growth

- Biofouling accounts for a major share of performance decline in membrane filtration systems, resulting in frequent chemical cleaning and significant operational downtime.

- Zwitterionic polymers and nanocoatings represent the latest innovations, offering surface modifications that prevent microbial adhesion and biofilm formation.

- Operating expenses in RO and NF plants are significantly impacted by fouling, strengthening the case for investment in antifouling membranes that reduce lifetime costs.

- Low-energy, fouling-resistant membranes are a major focus of innovation, enabling high water permeability at reduced operating pressures critical for sustainable water reuse projects.

Market Analysis: Recent Developments in Biofouling-Resistant Membranes

The biofouling-resistant membranes industry is experiencing rapid innovation, marked by cutting-edge product launches, strategic collaborations, and growing investment in sustainable water treatment solutions.

In July 2025, ZwitterCo introduced three new membrane families Evolution, Elevation, and Expedition tailored for food processing and challenging industrial wastewater applications. These innovations utilize zwitterionic chemistry to deliver unmatched fouling resistance. Around the same time, Toray Industries supplied its advanced RO membranes for the solar-powered Shuaibah 3 IWP desalination plant in Saudi Arabia, showcasing their application in sustainable, high-demand environments.

Earlier, in January 2025, DuPont Water Solutions expanded its FilmTec™ Fortilife™ CR membrane series, designed to withstand high biofouling conditions in industrial water reuse, thereby extending operational life and minimizing cleaning needs. Similarly, May 2025 saw Pentair’s X-Flow division launch ultrafiltration membrane elements optimized for high-turbidity pretreatment, effectively reducing downstream fouling in reverse osmosis systems.

The momentum extends beyond commercial rollouts. In April 2025, Europe launched a government-backed funding initiative to support the development of advanced antifouling coatings, aimed at reducing dependence on chemical cleaning agents. Academic research is also shaping the sector, with August 2024 marking the publication of a study on "living antifouling membranes" using beneficial biofilms that release nitric oxide to suppress harmful microbial growth. Additionally, September 2024 highlighted the growing adoption of quorum quenching (QQ) strategies in membrane bioreactors, significantly enhancing operational lifespan.

Industrial adoption is accelerating globally. SUEZ’s October 2024 project in China integrated antifouling membranes into a large-scale SWRO plant, while Pentair and Toray continue strengthening portfolios with products tailored for industrial wastewater, municipal reuse, and sustainable desalination systems.

Trends and Opportunities Driving the Biofouling-Resistant Membranes Market

The Biofouling-Resistant Membranes Market is entering a phase of accelerated innovation, fueled by the urgent need to reduce fouling-related costs in water treatment, desalination, and industrial wastewater reuse. With biofouling accounting for up to 50% of operational issues in reverse osmosis plants, industry stakeholders are investing heavily in next-generation materials, coatings, and hybrid solutions.

Innovation in Anti-Adhesion and Antimicrobial Membranes

A major trend is the development of anti-adhesion and antimicrobial membrane surfaces that prevent microbial colonization at the earliest stage. Research published in ACS Applied Materials & Interfaces by the Chinese Academy of Sciences demonstrated a dual-functional RO membrane grafted with ionic liquid and sulfonic acid monomers. The result was a 99.8% bactericidal rate against E. coli and a significantly lower flux decline compared to commercial membranes, proving the viability of long-term, self-sustaining biofouling resistance. Such innovations directly address the $15 billion annual global cost of membrane fouling, underscoring their commercial potential.

Strategic Investments and Collaborations in R&D

The market is witnessing record venture funding and institutional research collaborations focused on scaling up biofouling-resistant technologies. A leading water technology company recently closed a Series B funding round valued in the hundreds of millions, aimed at commercializing membranes for industrial wastewater reuse. Government-backed initiatives, as reported in PNAS, are also pushing new designs such as polymer brush architectures and biomimetic coatings. These collaborations highlight a growing recognition that tackling biofouling is not just an operational challenge but a strategic imperative for sustainable water security.

Hybrid Membrane Solutions for Comprehensive Biofouling Control

A third trend is the shift toward integrating biofouling-resistant membranes with complementary water treatment technologies. In a comparative study of reverse osmosis (RO) vs. membrane distillation (MD) systems, researchers found that biofilms in MD were more heterogeneous, requiring a multi-barrier strategy. This has accelerated the adoption of UF/RO hybrid trains and advanced pre-treatment protocols, creating layered defense mechanisms against fouling. Hybridization not only improves system resilience but also reduces chemical cleaning cycles, directly lowering OPEX for large-scale desalination plants.

Expanding Applications in Challenging Water Sources

The durability of biofouling-resistant membranes is opening doors to new, high-microbial-load water sources. A technical case study from a Saudi Arabian desalination plant showed that biofouling is among the top cost drivers in seawater reverse osmosis (SWRO), prompting utilities to trial anti-biofouling membranes. By cutting cleaning frequency and energy use, such solutions directly lower the levelized cost of water (LCOW), making desalination more economically sustainable. Beyond seawater, opportunities are growing in industrial wastewater reuse, food processing, and biotechnology, where reliability and throughput are mission-critical.

Market Share Analysis of the Biofouling-Resistant Membranes Market

Market Share by Membrane Type

By 2025, reverse osmosis (RO) membranes are projected to capture 35% of the market, cementing their position as the leading segment. RO membranes are indispensable for seawater desalination and ultrapure water production, where fouling directly impacts energy efficiency. Ultrafiltration (UF, 22%) and microfiltration (MF, 15%) membranes serve as critical pre-treatment technologies for RO systems, protecting them from particulate load and biofilm formation. Meanwhile, membrane bioreactor (MBR) membranes are the fastest-growing segment at 18%, driven by their integration of biological treatment with filtration. Nanofiltration (NF, 10%) maintains a niche role in selective softening and organic removal. The balance across segments reflects a growing ecosystem where anti-biofouling features are vital across both primary and supporting filtration processes.

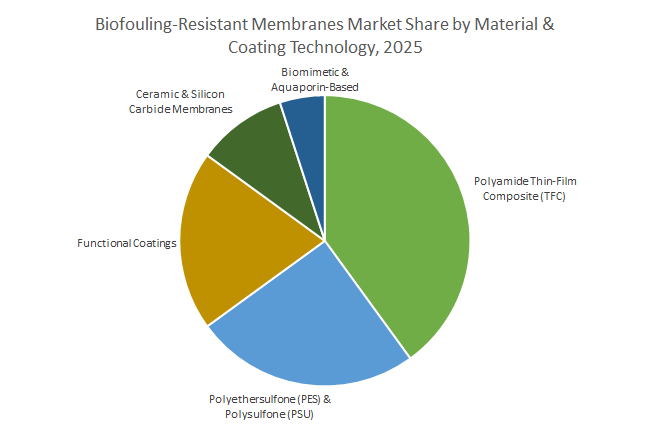

Market Share by Material & Coating Technology

Polyamide thin-film composite (TFC) membranes dominate with 40% share, thanks to their ubiquity in RO and NF applications. Next in line are polyethersulfone (PES) and polysulfone (PSU) membranes (25%), which lead the UF/MF segment due to their mechanical strength and chemical resistance. Functional coatings (20%) are emerging as the fastest-scaling innovation, adding hydrophilic, zwitterionic, and antimicrobial properties to existing platforms without requiring full redesigns. Ceramic and silicon carbide membranes (10%) occupy a durable niche in harsh industrial environments, such as pharma and petrochemicals, where aggressive cleaning is required. Meanwhile, biomimetic and aquaporin-based membranes (5%) remain in early adoption but are considered the future of high-efficiency filtration, with disruptive potential as costs fall.

Market Share by Application

In terms of applications, municipal water and wastewater treatment leads with 30% market share, driven by large-scale adoption of biofouling-resistant membranes to meet tightening effluent discharge regulations and water reuse mandates. Industrial wastewater treatment (25%) is the second-largest segment, fueled by complex effluents from chemicals, textiles, and power generation, where fouling-resistant membranes ensure operational continuity. Seawater desalination (20%) remains a strategic growth market, especially in MENA, where biofouling-resistant RO membranes directly reduce energy consumption and LCOW. The food & beverage sector (15%) depends on membranes for product quality and waste valorization, while brackish water treatment and pharmaceuticals/biotech (5% each) serve specialized but critical niches. Collectively, these segments highlight how the biofouling-resistant membranes market underpins both water security and industrial productivity worldwide.

United States: Government-Funded Research and Commercial Innovations Driving Biofouling-Resistant Membranes

The United States is a global leader in biofouling-resistant membrane innovation, supported by strong government funding, academic research, and corporate initiatives. The U.S. National Science Foundation (NSF) provides grants for developing new materials and processes to combat biofouling, including NSF Small Business Innovation Research (SBIR) funding awarded to NALA Systems for chlorine-resistant membranes designed to prevent fouling. Academic institutions such as the University of California, San Diego, are advancing hybrid biofouling-resistant systems, including “living membranes” engineered with beneficial biofilms to inhibit harmful bacterial growth. On the corporate front, ZwitterCo expanded its membrane portfolio in July 2025 with three new families leveraging zwitterionic chemistry for enhanced fouling resistance, particularly in industrial wastewater treatment and food processing. Additionally, the National Alliance for Water Innovation (NAWI), funded by the Department of Energy, focuses on lowering the cost and energy requirements of desalination technologies while mitigating biofouling, a critical operational challenge for large-scale membrane systems.

China: Advanced Materials and Regulatory Pressure Fuel Biofouling-Resistant Membrane Development

China’s biofouling-resistant membrane market is rapidly evolving through technological innovations, R&D focus, and regulatory enforcement. Researchers at the Institute of Process Engineering (IPE) of the Chinese Academy of Sciences developed a dual-functional reverse osmosis (RO) membrane in 2024 with antibacterial and anti-adhesion properties, addressing biofouling that accounts for over 45% of fouling in RO systems. Concurrently, Chinese institutions are exploring advanced materials for membrane surface modification, such as ceramic membranes enhanced with vanadium carbide (V2C) MXene, demonstrating resistance to oil fouling and stable performance across a wide pH range. The Ministry of Ecology and Environment (MEE) enforces strict industrial wastewater discharge standards, encouraging companies to adopt membrane bioreactors (MBRs) and hybrid systems that require robust biofouling resistance for efficient operation, further driving innovation and market adoption.

Germany: Industrial Expertise and Ceramic Membranes Leading Biofouling-Resistant Applications

Germany leverages industrial expertise and advanced ceramic membrane technologies to address biofouling challenges. PWT Wassertechnik specializes in applying membrane processes with anti-fouling properties for industrial wastewater treatment and reuse, ensuring compliance with stringent European environmental regulations. CERAFILTEC, a German ceramic membrane manufacturer, announced in 2024 the deployment of flat membranes for MBR projects across four continents. The inherent chemical resistance and durability of ceramic membranes make them particularly effective in biofouling-prone environments, positioning Germany as a global hub for high-performance, industrial-grade biofouling-resistant membrane solutions.

Japan: Research-Driven MBR Solutions and Strategic Corporate Collaborations

Japan continues to lead in biofouling-resistant membrane technology through academic and corporate innovation. Toray Industries unveiled a next-generation hollow fiber membrane in 2025, featuring 20% higher permeability and significantly reduced fouling, lowering operational costs for MBR systems. Japan has over 3,000 full-scale MBR applications, ranging from small industrial and household wastewater systems to large municipal plants where fouling resistance is critical for performance. Strategic collaborations with companies like Sumitomo Electric Industries further enhance the availability of high-performance MBR membranes that combine chemical resistance, durability, and superior fouling mitigation, reflecting Japan’s strong focus on sustainable and efficient water treatment.

Australia: Water Recycling Leadership and Green Chemical Innovations

Australia’s biofouling-resistant membrane market is driven by water scarcity, recycling initiatives, and government-supported research. The Australian Water Recycling Centre of Excellence funded projects demonstrating the effectiveness of ceramic membranes in treating high-organic secondary effluent, a scenario prone to biofouling. The Institute for Sustainable Industries and Liveable Cities (ISILC) at Victoria University focuses on advancing water treatment technologies, particularly reducing membrane fouling and scaling while improving water recovery from desalination processes. Additionally, the Centre funds research on “green chemicals” for biofouling removal and membrane preservation, providing an environmentally sustainable alternative to harsh chemical cleaning agents, further solidifying Australia’s leadership in advanced, eco-friendly membrane technologies.

The Netherlands: Innovative Membrane Solutions and Industrial Expertise

The Netherlands has established itself as a hub for biofouling-resistant membrane innovation and operational optimization. A 2024 study revealed that fouling accounts for approximately 11% and 24% of operating expenses in nanofiltration and reverse osmosis plants, respectively, emphasizing the importance of biofouling mitigation. Dutch companies like Lenntech offer comprehensive services including biofilm removal, chemical cleaning agents, and pretreatment solutions to maintain membrane performance while reducing scaling and fouling. The combination of advanced technological research and active corporate involvement positions the Netherlands as a key player in the global biofouling-resistant membranes market.

Competitive Landscape: Leading Players in the Biofouling-Resistant Membranes Market

The biofouling-resistant membranes market is defined by competition among global leaders with strong R&D capabilities, robust material science expertise, and extensive project portfolios. Companies are focusing on anti-biofouling innovation, cost optimization, and long-term durability to secure a competitive edge.

DuPont Water Solutions: FilmTec™ Driving Industrial Water Reuse

DuPont is a global leader in advanced membrane technologies, leveraging its FilmTec™ brand as a benchmark for RO and NF membranes. Its Fortilife™ CR series targets biofouling-prone applications, reducing cleaning cycles by up to 50% and lowering total cost of ownership. DuPont’s strategy centers on extending membrane lifespan and improving energy efficiency, positioning it as a preferred choice in industrial reuse and municipal applications.

Toray Industries: Innovation Through Polymer Chemistry

Toray Industries brings unmatched expertise in advanced polymer chemistry, enabling the development of anti-biofouling and anti-scaling membranes. Its solutions have been deployed in landmark desalination projects, including the solar-powered Shuaibah 3 IWP facility in Saudi Arabia. Under its “Toray Vision 2030” strategy, the company is focused on global water sustainability, reinforcing technical support in high-demand regions while delivering durable membranes tailored for wastewater reuse and seawater treatment.

SUEZ Water Technologies & Solutions: Integrated Anti-Fouling Solutions

SUEZ combines advanced membrane systems with digital analytics and predictive monitoring for optimized fouling control. Since acquiring GE Water & Process Technologies, SUEZ has expanded its portfolio and global reach. Its membranes are widely applied in industrial wastewater treatment, particularly in chemical and pharmaceutical industries where biofouling is prevalent. The company’s integrated solutions position it strongly in both municipal and industrial sectors.

Pentair: X-Flow Ultrafiltration for Pretreatment Efficiency

Through its X-Flow division, Pentair specializes in robust ultrafiltration (UF) and microfiltration (MF) membranes. Products such as the XF64 series are designed to mitigate fouling in pretreatment stages, ensuring downstream RO systems maintain high efficiency. Pentair’s innovations focus on durability, reduced operating costs, and easier maintenance, making its solutions attractive for municipal water reuse and industrial wastewater management.

Kuraray Co., Ltd.: Hollow-Fiber Membranes for Demanding Applications

Kuraray, a Japanese leader in specialty polymers, has carved out a niche in chemically resistant hollow-fiber membranes. Its solutions are widely applied in ultrapure water production, medical processes, and high-turbidity treatment environments. Recent advances in production technology have improved permeability, enabling higher throughput with reduced energy costs. Kuraray’s strategic focus remains on providing long-lasting, chemical-resistant membranes for challenging industrial and municipal applications.

Biofouling-Resistant Membranes Market Report Scope

Biofouling-Resistant Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.5 Billion

|

|

Market Size (2034)

|

$8.4 Billion

|

|

Market Growth Rate

|

10.2%

|

|

Segments

|

By Membrane Type (Reverse Osmosis (RO) Membranes, Ultrafiltration (UF) Membranes, Nanofiltration (NF) Membranes, Microfiltration (MF) Membranes, Membrane Bioreactor (MBR) Membranes), By Material & Coating Technology (Polyamide Thin-Film Composite (TFC) Membranes, Polyethersulfone (PES) & Polysulfone (PSU) Membranes, Ceramic & Silicon Carbide Membranes, Biomimetic & Aquaporin-Based Membranes, Functional Coatings), By Application (Seawater Desalination, Brackish Water Treatment, Municipal Water & Wastewater Treatment, Industrial Wastewater Treatment, Pharmaceuticals & Biotechnology, Food & Beverage Processing), By End-User Industry (Municipal Utilities, Power Generation, Oil & Gas / Petrochemicals, Food & Beverage, Pharmaceuticals & Life Sciences, Textiles & Chemicals)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Toray Industries, Inc., SUEZ, Veolia, Pentair plc, Xylem Inc., The Dow Chemical Company, ZwitterCo, Kubota Corporation, MANN+HUMMEL, Evoqua Water Technologies, Koch Separation Solutions, LG Chem, Kuraray Co., Ltd., Mitsubishi Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biofouling-Resistant Membranes Market Segmentation

By Membrane Type

- Reverse Osmosis (RO) Membranes

- Ultrafiltration (UF) Membranes

- Nanofiltration (NF) Membranes

- Microfiltration (MF) Membranes

- Membrane Bioreactor (MBR) Membranes

By Material & Coating Technology

- Polyamide Thin-Film Composite (TFC) Membranes

- Polyethersulfone (PES) & Polysulfone (PSU) Membranes

- Ceramic & Silicon Carbide Membranes

- Biomimetic & Aquaporin-Based Membranes

- Functional Coatings

By Application

- Seawater Desalination

- Brackish Water Treatment

- Municipal Water & Wastewater Treatment

- Industrial Wastewater Treatment

- Pharmaceuticals & Biotechnology

- Food & Beverage Processing

By End-User Industry

- Municipal Utilities

- Power Generation

- Oil & Gas / Petrochemicals

- Food & Beverage

- Pharmaceuticals & Life Sciences

- Textiles & Chemicals

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biofouling-Resistant Membranes Industry include-

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- SUEZ

- Veolia

- Pentair plc

- Xylem Inc.

- The Dow Chemical Company

- ZwitterCo

- Kubota Corporation

- MANN+HUMMEL

- Evoqua Water Technologies

- Koch Separation Solutions

- LG Chem

- Kuraray Co., Ltd.

- Mitsubishi Chemical Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Biofouling-Resistant Membranes landscape with an emphasis on market sizing to 2034, operating-cost impacts, and adoption patterns across municipal and industrial reuse. Our analysis reviews vendor pipelines, regulatory catalysts, and cost-down levers (anti-adhesion chemistries, zwitterionic surfaces, living/QQ strategies), and highlights breakthroughs that cut cleaning cycles, stabilize flux, and lower LCOW in RO/NF/MBR trains. Leveraging capex/opex benchmarks, case libraries, and scenario modeling, this report is an essential resource for utilities, EPCs, OEMs, and investors seeking validated performance thresholds, risk factors, and bankable specifications for antifouling upgrades and greenfield builds. Scope Includes-

- Segmentation: By Membrane Type (RO, UF, NF, MF, MBR); By Material & Coating Technology (Polyamide TFC, PES & PSU, Ceramic & SiC, Biomimetic & Aquaporin-Based, Functional Coatings); By Application (Seawater Desalination, Brackish Water Treatment, Municipal Water & Wastewater, Industrial Wastewater, Pharmaceuticals & Biotechnology, Food & Beverage Processing); By End-User Industry (Municipal Utilities, Power Generation, Oil & Gas/Petrochemicals, Food & Beverage, Pharmaceuticals & Life Sciences, Textiles & Chemicals).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): DuPont de Nemours, Inc.; Toray Industries, Inc.; SUEZ; Veolia; Pentair plc; Xylem Inc.; The Dow Chemical Company; ZwitterCo; Kubota Corporation; MANN+HUMMEL; Evoqua Water Technologies; Koch Separation Solutions; LG Chem; Kuraray Co., Ltd.; Mitsubishi Chemical Corporation.

Methodology

USDAnalytics employed a triangulated approach: bottom-up sizing from plant-level datasets (cleaning frequency, TMP trends, flux recovery, chemistry dose, energy/kWh-m³) and disclosed orders; top-down reconciliation with national reuse mandates and budget pipelines; and primary interviews with operators, OEMs, and EPCs. We normalized opex using duty-cycle models for RO/NF/MBR pretreatment trains, applied sensitivity testing (feed microbiology, SDI, temperature, cleaning regime, coating choice), and benchmarked suppliers on durability, anti-adhesion efficacy, antimicrobial performance, and lifecycle economics. Forecasts use scenario bands (base/accelerated) with adoption curves for zwitterionic coatings, functionalized TFCs, ceramics, and biomimetic membranes.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Biofouling-Resistant Membranes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights Driving Market Growth

1.3. Global Market Snapshot

2. Biofouling-Resistant Membranes Market Outlook (2025–2034)

2.1. Market Overview: Growth Driven by Efficiency and Sustainability

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): USD 3.5 Billion

2.2.2. Forecasted Market Size (2034): USD 8.4 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 10.2%

2.3. Trends and Opportunities Driving Market Growth

2.3.1. Innovation in Anti-Adhesion and Antimicrobial Membranes

2.3.2. Strategic Investments and Collaborations in R&D

2.3.3. Hybrid Membrane Solutions for Comprehensive Biofouling Control

2.3.4. Expanding Applications in Challenging Water Sources

3. Recent Developments in Biofouling-Resistant Membranes

3.1. Market Analysis: Recent Innovations and Strategic Activities

3.1.1. ZwitterCo Introduces New Membrane Families (July 2025)

3.1.2. Toray Industries Supplies Membranes for Shuaibah 3 Desalination Plant (July 2025)

3.1.3. DuPont Water Solutions Expands FilmTec™ Fortilife™ CR Series (January 2025)

3.1.4. Pentair’s X-Flow Division Launches New Ultrafiltration Elements (May 2025)

3.1.5. Europe Launches Government-Backed Funding for Antifouling Coatings (April 2025)

3.1.6. Publication of "Living Antifouling Membranes" Study (August 2024)

3.1.7. SUEZ Integrates Antifouling Membranes into China SWRO Project (October 2024)

4. Biofouling-Resistant Membranes Market Competitive Landscape: Leading Players

4.1. Market Overview: Focus on Innovation and Durability

4.2. Profiles of Leading Players

4.2.1. DuPont Water Solutions

4.2.2. Toray Industries

4.2.3. SUEZ Water Technologies & Solutions

4.2.4. Pentair

4.2.5. Kuraray Co., Ltd.

5. Biofouling-Resistant Membranes Market Share Analysis by Segment

5.1. Biofouling-Resistant Membranes Market Share by Membrane Type

5.1.1. Reverse Osmosis (RO) Membranes

5.1.2. Ultrafiltration (UF) Membranes

5.1.3. Nanofiltration (NF) Membranes

5.1.4. Microfiltration (MF) Membranes

5.1.5. Membrane Bioreactor (MBR) Membranes

5.2. Biofouling-Resistant Membranes Market Share by Material & Coating Technology

5.2.1. Polyamide Thin-Film Composite (TFC) Membranes

5.2.2. Polyethersulfone (PES) & Polysulfone (PSU) Membranes

5.2.3. Functional Coatings

5.2.4. Ceramic & Silicon Carbide Membranes

5.2.5. Biomimetic & Aquaporin-Based Membranes

5.3. Biofouling-Resistant Membranes Market Share by Application

5.3.1. Municipal Water & Wastewater Treatment

5.3.2. Industrial Wastewater Treatment

5.3.3. Seawater Desalination

5.3.4. Food & Beverage Processing

5.3.5. Brackish Water Treatment

5.3.6. Pharmaceuticals & Biotechnology

6. Biofouling-Resistant Membranes Country Analysis and Outlook

6.1. United States: Government-Funded Research and Commercial Innovations

6.2. China: Advanced Materials and Regulatory Pressure

6.3. Germany: Industrial Expertise and Ceramic Membranes

6.4. Japan: Research-Driven MBR Solutions and Strategic Collaborations

6.5. Australia: Water Recycling Leadership and Green Chemical Innovations

6.6. The Netherlands: Innovative Membrane Solutions and Industrial Expertise

6.7. Other Key Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (India, South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Biofouling-Resistant Membranes Market Segmentation

7.1. By Membrane Type

7.2. By Material & Coating Technology

7.3. By Application

7.4. By End-User Industry

8. Market Size Outlook by Region (2025-2034)

8.1. North America Market Size Outlook to 2034

8.2. Europe Market Size Outlook to 2034

8.3. Asia Pacific Market Size Outlook to 2034

8.4. South America Market Size Outlook to 2034

8.5. Middle East and Africa Market Size Outlook to 2034

9. Company Profiles: Top Players

9.1. DuPont de Nemours, Inc.

9.2. Toray Industries, Inc.

9.3. SUEZ

9.4. Veolia

9.5. Pentair plc

9.6. Xylem Inc.

9.7. The Dow Chemical Company

9.8. ZwitterCo

9.9. Kubota Corporation

9.10. MANN+HUMMEL

9.11. Evoqua Water Technologies

9.12. Koch Separation Solutions

9.13. LG Chem

9.14. Kuraray Co., Ltd.

9.15. Mitsubishi Chemical Corporation

10. Methodology and Appendix

10.1. Research Scope

10.2. Market Research Approach

10.3. Market Sizing and Forecasting Model

10.4. Research Coverage

10.5. Data Horizon

10.6. Deliverables