Protective Coatings Market Size, Industrial Demand, and Infrastructure-Driven Growth

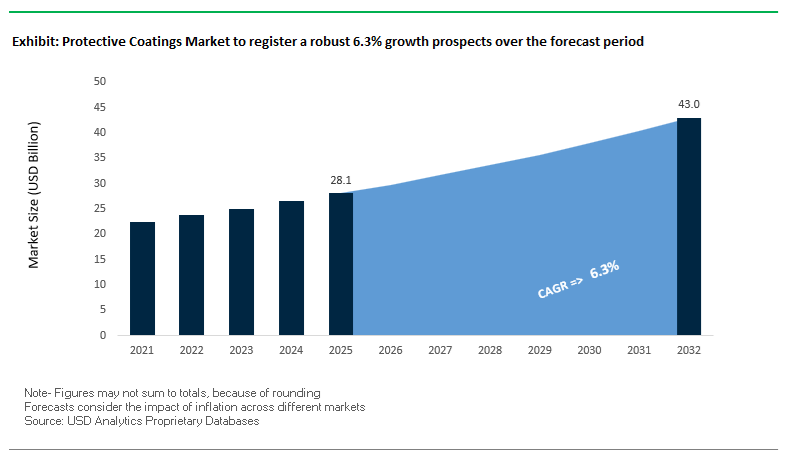

The global Protective Coatings Market was valued at $28.1 billion in 2025 and is projected to grow at a CAGR of 6.3% through 2032, reaching $43.1 billion by 2032. This growth trajectory reflects strong demand across oil & gas, marine, power generation, infrastructure, and renewable energy sectors, where protective coatings are critical for asset longevity, corrosion prevention, and lifecycle cost optimization.

Protective coatings serve as the primary defense layer for steel and concrete infrastructure exposed to aggressive environments, including offshore platforms, pipelines, bridges, refineries, and industrial plants. These coatings are engineered to withstand chemical exposure, high humidity, salt spray, UV radiation, and extreme temperature fluctuations, making them indispensable in both new-build and maintenance applications.

A key structural driver is the global expansion of energy infrastructure and transportation networks, particularly in emerging economies and offshore environments. The rapid growth of offshore wind farms, LNG terminals, and petrochemical facilities is creating sustained demand for high-performance coating systems capable of delivering multi-decade protection cycles.

In parallel, the increasing focus on asset integrity management and predictive maintenance is driving the adoption of advanced coatings that not only protect surfaces but also enable performance monitoring and lifecycle optimization. Sustainability considerations are also influencing procurement decisions, with growing preference for low-VOC, high-solids, and environmentally compliant coating systems.

Market Analysis: Advanced Anti-Corrosion Systems, Smart Coatings, and Low-VOC Technologies Driving Market Evolution

Recent developments in the Protective Coatings Market highlight a strong shift toward advanced material performance, digital integration, and regulatory compliance. In March 2026, Jotun introduced its next-generation anti-corrosion systems, featuring enhanced zinc-rich primers and barrier technologies specifically designed for offshore wind and oil & gas applications, where extended service life under extreme conditions is critical.

Environmental regulations are accelerating innovation in coating chemistry. Jotun’s ultra-low VOC epoxy coatings (January 2026) demonstrate how manufacturers are balancing high-build protection with reduced emissions, particularly in regions with strict environmental standards such as the Middle East and Asia.

Digitalization is emerging as a transformative trend. Kansai Helios’ smart coating technologies (September 2025) integrate sensor-based or reactive layers that allow real-time monitoring of corrosion and coating degradation. This capability supports predictive maintenance strategies, reducing downtime and maintenance costs for critical infrastructure assets.

Strategic investments and restructuring are strengthening market positioning. Sherwin-Williams reported record 2025 sales driven by its protective and marine segments, supported by the integration of Suvinil, which expanded its industrial footprint in Latin America. Meanwhile, PPG’s leadership restructuring aims to better align its protective coatings portfolio across infrastructure and transportation sectors, reflecting a more integrated global strategy.

Growth in renewable energy is becoming a major catalyst. Hempel’s “Accelerate to Win” strategy, backed by CVC investment, prioritizes expansion in offshore wind coatings, where long-term durability and resistance to harsh marine conditions are essential.

Portfolio optimization is also reshaping competitive dynamics. AkzoNobel’s divestment of its Indian subsidiary (February 2026) provides significant capital to refocus R&D on high-performance protective systems in developed markets, while maintaining leadership in aerospace and marine coatings.

Product innovation continues to address industrial requirements. Axalta’s Imron® Fleet Line Elite (October 2025) offers enhanced chemical resistance and flexible curing options, enabling faster throughput in industrial refinish applications without compromising durability.

Market Trend: Ultra-Low VOC Regulatory Enforcement Reshaping Protective Coatings Formulation Across EU and China

The global protective coatings market is entering a regulatory enforcement phase where ultra-low VOC compliance is no longer optional but a prerequisite for market access. As of mid-2026, regulatory convergence between China and Europe is fundamentally altering formulation strategies, raw material selection, and product certification pathways across industrial protective coatings.

The implementation of GB 30981.2-2025 by the Ministry of Ecology and Environment, effective June 1, 2026, marks a major standardization milestone. This unified regulation consolidates multiple sector-specific standards into a single compliance framework, covering industrial coatings across marine, automotive, and wood applications. Under this mandate, solvent-free industrial coatings classified as F-type must maintain VOC levels at or below 100 g/L, effectively pushing formulators toward high-purity resin systems and advanced reactive diluents.

Simultaneously, European regulatory alignment through REACH and the Packaging and Packaging Waste Regulation is accelerating the elimination of hazardous substances in protective coatings. The regulation imposes strict limits on heavy metals, with total concentrations of lead, cadmium, hexavalent chromium, and mercury restricted to less than 100 mg/kg. This is driving a rapid transition away from traditional anti-corrosive pigments toward non-toxic alternatives such as zinc-free inhibitors and advanced barrier coatings.

These combined regulatory pressures are transforming the competitive landscape. Coating manufacturers are increasingly investing in low-emission resin chemistries, reformulating product portfolios, and optimizing supply chains to meet evolving compliance thresholds. Ultra-low VOC coatings are emerging as the new baseline standard in industrial protective coatings, particularly in sectors such as infrastructure, marine, and energy.

Market Trend: Low-Temperature Cure Protective Coatings Extending Maintenance Windows in Energy and Pipeline Infrastructure

A significant operational trend in the protective coatings industry is the adoption of low-temperature cure chemistries, particularly in pipeline coatings and tank lining applications. Owner-operators in oil and gas, chemical processing, and storage infrastructure are increasingly specifying coatings capable of curing at temperatures as low as −7°C to extend maintenance capabilities in cold climates and reduce reliance on external heating systems.

Modern low-temperature cure epoxy novolac systems developed for 2026 applications demonstrate substantial improvements in curing efficiency. These coatings achieve return-to-service timelines within 24 hours at ambient temperatures as low as 2°C, compared to legacy high-build epoxy systems that require up to seven days under similar conditions. This accelerated curing capability significantly reduces downtime, improves asset availability, and enhances maintenance scheduling flexibility.

Beyond curing efficiency, these coatings are engineered to deliver high thermal and chemical resistance during service. Advanced formulations are capable of withstanding continuous immersion temperatures up to 177°C, making them suitable for aggressive chemical environments and high-temperature storage applications. This dual capability of cold-weather application and high-temperature operational stability is particularly valuable in sectors such as petrochemicals, refining, and bulk liquid storage.

The economic implications are substantial. By eliminating or reducing the need for temporary heating infrastructure during maintenance operations, operators can achieve significant cost savings while maintaining coating performance standards. This trend is expected to drive increased adoption of low-temperature cure protective coatings across northern geographies and offshore environments.

Market Opportunity: Intumescent Coatings for Lithium-Ion Battery Fire Protection Creating New Growth Segment in EV and Energy Storage

The rapid expansion of electric vehicles and energy storage systems is generating a high-growth opportunity for intumescent protective coatings designed for lithium-ion battery containment. These coatings are evolving from traditional passive fire protection solutions for structural steel into active thermal management systems for battery enclosures.

Advanced intumescent coatings developed for 2026 applications are engineered to withstand temperatures exceeding 1,000°C for durations of up to 30 minutes. This provides critical time for occupant evacuation in electric vehicles and helps maintain the structural integrity of battery enclosures during thermal runaway events. The ability to delay or contain fire propagation is becoming a key design requirement for automotive OEMs and energy storage system integrators.

Weight efficiency is a critical advantage driving adoption. Compared to conventional fire protection materials such as ceramic fiber blankets, spray-applied intumescent coatings add less than 2 kilograms to the overall vehicle mass while delivering equivalent or superior fire resistance. This lightweight profile is essential for electric vehicles, where weight directly impacts battery efficiency and driving range.

The convergence of safety regulations, EV adoption, and battery performance requirements is positioning intumescent coatings as a core technology in next-generation fire protection systems. This creates a significant opportunity for coating manufacturers to expand into automotive and energy storage markets with specialized high-performance formulations.

Market Opportunity: Self-Healing Polyurea Coatings Enabling Autonomous Corrosion Protection in Marine Splash Zones

Self-healing polyurea coatings are emerging as a transformative solution for corrosion protection in marine splash zones, where continuous exposure to oxygen, saltwater, and mechanical abrasion creates extreme degradation conditions. These environments are typically difficult to access for maintenance, making autonomous protection technologies highly valuable.

Recent advancements in supramolecular chemistry have enabled the development of polyurea coatings with intrinsic self-healing capabilities. Field data from 2026 indicates that these coatings can achieve healing efficiencies between 80% and 86% within 24 hours in underwater or high-humidity conditions without the need for external triggers. This allows micro-cracks caused by mechanical impact or environmental stress to be repaired before corrosive agents penetrate the coating layer.

The impact on maintenance strategies is significant. Offshore operators utilizing self-healing coatings have reported a 40% reduction in localized pitting corrosion over a five-year period, driven by the continuous repair of micro-damage. This reduces the frequency of inspection and maintenance interventions, lowering operational costs and improving asset longevity.

Importantly, these coatings maintain high mechanical performance despite their dynamic healing properties. With tensile strength values in the range of 40 to 50 MPa, self-healing polyurea coatings provide the necessary impact resistance for high-energy marine environments. This combination of durability and autonomous repair capability positions self-healing coatings as a next-generation solution for offshore structures, bridges, and coastal infrastructure.

Protective Coatings Market Share and Segmentation Insights: Anti-Corrosion Dominance and Contractor-Led Supply Chain Dynamics

By Function: Anti-Corrosion Coatings Lead with Critical Role in Infrastructure Protection

The anti-corrosion coatings segment dominated the protective coatings market with a 46.8% share in 2025, driven by its essential role in mitigating the massive economic impact of corrosion, which accounts for approximately 3–4% of global GDP annually. Industries such as oil & gas, marine, power generation, and infrastructure heavily rely on anti-corrosion coating systems including epoxy coatings, polyurethane coatings, and zinc-rich primers to extend asset life and reduce maintenance costs. These coatings are critical for protecting bridges, pipelines, offshore platforms, ships, and storage tanks, where exposure to moisture, chemicals, and harsh environments accelerates material degradation. The increasing focus on infrastructure durability, lifecycle cost reduction, and asset integrity management continues to drive demand for high-performance anti-corrosion solutions. As governments and private sectors invest in large-scale infrastructure projects, corrosion-resistant coatings remain the largest and most vital segment within the global protective coatings market.

By Sales Channel: Professional Contractor Supply Channels Dominate with Specification-Driven Procurement

The professional contractor supply channels segment accounted for a leading 45.3% share of the protective coatings market in 2025, reflecting the importance of certified application expertise and compliance with strict industry standards. Protective coatings require precise application processes, including surface preparation following SSPC/NACE standards, environmental condition control, and accurate film thickness measurement, which are typically handled by trained contractors. These professionals source coatings through specialized supply channels that provide approved products, technical guidance, and compliance documentation. Additionally, large-scale infrastructure and industrial projects are specification-driven, with engineering consultants mandating specific coating systems and approved suppliers to ensure warranty validity, performance reliability, and traceability. Contractor supply channels streamline procurement while aligning with project requirements and regulatory frameworks. As demand grows for high-performance protective coatings in infrastructure and industrial sectors, contractor-led distribution networks will continue to play a pivotal role in market expansion.

Competitive Landscape of the Protective Coatings Market

PPG Leads Global Protective Coatings Market with Digital Innovation and EV Integration

PPG Industries, Inc. remains a dominant force in the protective coatings market, supported by strong financial performance and technological leadership. In Q1 2026, the company reported a 7% year-over-year revenue increase to $3.9 billion, with its Protective and Marine Coatings segment achieving its 12th consecutive quarter of growth. PPG has introduced advanced solutions such as Sigma Glide® 650 coatings and dielectric primers for EV battery enclosures, providing both thermal management and electrical insulation. Its PPG LINQ™ digital platform enhances efficiency by reducing material waste and technical lead times through AI-driven optimization. Strategic restructuring, including plant closures in Europe, is aimed at improving profitability and focusing on high-margin technologies.

AkzoNobel Strengthens Market Position with Strategic Merger and AI-Driven Asset Management

AkzoNobel N.V. is a key player in the protective coatings market, undergoing a major transformation through its planned merger with Axalta. The company achieved a 14.5% EBITDA margin in Q1 2026 despite revenue adjustments following divestments. Its AI-driven drone inspection technology enables precise detection of corrosion and coating degradation, reducing maintenance downtime in critical infrastructure. AkzoNobel is also advancing sustainability by integrating bio-attributed resins into its marine coatings portfolio, reducing carbon footprint. Its focus on operational efficiency and high-performance coatings reinforces its leadership in global markets.

Sherwin-Williams Expands Infrastructure Leadership with High-Performance Coating Systems

The Sherwin-Williams Company continues to dominate the protective coatings market, particularly in North America. In Q1 2026, the company reported $5.67 billion in net sales, with strong growth in its Performance Coatings Group. Its EnviroLastic® polyaspartic coatings are widely used for same-day return-to-service applications, offering superior abrasion resistance for high-traffic infrastructure. The integration of Suvinil has strengthened its presence in South America, while strong cash flow supports ongoing investment in innovation and expansion.

Hempel Drives Efficiency and Sustainability with Advanced Marine and Energy Coatings

Hempel A/S is a leading innovator in the protective coatings market, focusing on efficiency and sustainability. The company entered 2026 with an EBITDA margin of 18.2% and record free cash flow. Its Hempaguard NB coatings reduce emissions and improve vessel efficiency, while Hempafire Extreme provides advanced fire protection for infrastructure. Hempel’s sustainability initiatives have enabled significant CO₂ reductions, positioning it as a leader in environmentally responsible coatings. Its “Accelerate to Win” strategy aims to further strengthen its position in marine and energy sectors.

Jotun Leads Offshore and Marine Coatings with Smart and High-Durability Technologies

Jotun Group is a dominant player in the protective coatings market, particularly in offshore and marine applications. The company reported record revenues exceeding NOK 34 billion, driven by strong growth in energy and infrastructure sectors. Its smart coatings incorporate advanced materials that signal corrosion or surface failure, enhancing maintenance efficiency. Jotun’s Next Generation Barrier Technologies provide superior adhesion and durability in harsh environments. Its integration of robotic cleaning systems with coating solutions offers a comprehensive approach to asset protection.

Nippon Paint Expands Global Presence with High-Value Protective Coatings and Green Technologies

Nippon Paint Holdings Co., Ltd. is a major player in the protective coatings market, leveraging its strong presence in Asia-Pacific and expanding globally. The company reported robust revenue growth and increased profitability driven by automotive recovery and industrial demand. Its focus on anti-viral, anti-fouling, and hydrophilic-hydrophobic coating technologies supports sustainable and high-performance applications. Nippon Paint is also targeting green transformation initiatives, ensuring a stable supply chain for polyurethane-based coatings. Its strategic expansion into North America and China strengthens its competitive position in the global market.

China Protective Coatings Market: High-End Specialization and “Blue Sky” Compliance

China is transitioning toward high-value protective coatings, driven by stringent environmental regulations under the “Blue Sky Defense War” (2025–2026). These policies are forcing the shutdown of high-emission solvent-based lines and accelerating adoption of waterborne and powder coatings across industrial clusters.

Technological advancements include ultra-durable PVDF fluorocarbon coatings offering over 30 years of performance in high-corrosion coastal environments. Infrastructure investments under the “New Infrastructure” initiative are driving demand for dielectric coatings in 5G base stations, while the EV sector is rapidly adopting intumescent fire-protective coatings for battery enclosures. China is also advancing digital manufacturing, with AI-enabled coating lines improving precision and reducing material waste, reinforcing its leadership in high-performance coating technologies.

India Protective Coatings Market: Infrastructure-Led Expansion and Smart Coating Adoption

India is one of the fastest-growing markets in the protective coatings industry, fueled by aggressive infrastructure development and urban modernization programs. Initiatives such as the National Industrial Corridor Development Programme (NICDP) and Gati Shakti Master Plan are significantly increasing demand for epoxy-zinc phosphate coatings in railway stations, airports, and industrial cities.

A major technological shift is the adoption of Cool Roof coatings with high Solar Reflective Index (SRI), now mandatory in many smart city projects to combat urban heat. The market is also seeing innovation in antimicrobial coatings for healthcare and food storage infrastructure. Capacity expansions by major domestic players and growing use of Al-Mg-Zn coated substrates in solar PV mounting structures are further strengthening India’s position as a key growth engine in the global market.

United States Protective Coatings Market: Regulatory Transformation and Reshoring Growth

The U.S. protective coatings market is being reshaped by strict environmental regulations and industrial reshoring trends. The implementation of PFAS-free mandates (2025–2026) is forcing a shift away from traditional fluoropolymer chemistries, driving innovation in alternative coating systems.

Infrastructure investments under the Bipartisan Infrastructure Law are fueling demand for fusion-bonded epoxy (FBE) coatings for bridges and transportation systems. The market is also advancing in UV-curable coatings, enabling rapid processing with minimal energy use. Reshoring of EV and appliance manufacturing is increasing installation of robotic powder coating systems, while sustainability goals are driving adoption of bio-based coatings. Additionally, demand for recyclable materials is boosting the use of matte-finish aluminum roofing with protective coatings in residential construction.

Germany Protective Coatings Market: Green Steel and Hydrogen Infrastructure Leadership

Germany leads Europe in sustainable protective coatings, integrating advanced materials with low-carbon manufacturing. The adoption of hydrogen-based green steel substrates is creating demand for specialized low-temperature curing coatings that maintain material integrity.

The government’s renewable energy initiatives are driving demand for C5-M rated coatings for offshore wind infrastructure, while compliance with EU building regulations is increasing the use of insulated metal panels with protective skins. Innovations such as self-healing coatings using microcapsule technology are enhancing durability in automotive and aerospace applications. Germany is also advancing blockchain-based material passports, ensuring traceability and supporting circular economy goals.

Saudi Arabia Protective Coatings Market: Vision 2030 and Mega-Project Demand

Saudi Arabia is witnessing rapid growth in the protective coatings market, driven by large-scale infrastructure projects under Vision 2030. Developments such as NEOM and The Line are generating significant demand for fusion-bonded epoxy coatings used in underground utilities and piping networks.

The government’s housing targets are increasing the use of waterborne architectural coatings, while the oil and gas sector is driving demand for phenolic epoxy coatings for tank linings. Technological advancements include nanotechnology-based zero-VOC coatings and solar-reflective coatings designed to reduce heat load in extreme desert climates. Expansion of local manufacturing facilities by global players is further strengthening the market.

Brazil Protective Coatings Market: Oil & Gas Investments and Agribusiness Demand

Brazil’s protective coatings market is strongly driven by its oil & gas sector and agricultural machinery industry. Government forecasts of $83.5 billion in oil and gas investments by 2032 are creating significant demand for subsea protective coatings.

The agricultural sector is a major application area, with widespread use of UV-stable coatings for tractors and harvesters. Regulatory measures, including anti-dumping duties on coated steel imports, are boosting domestic production. Technological advancements such as ZAM-compatible coatings are improving corrosion resistance, while government initiatives are supporting the transition to energy-efficient powder coating technologies. Housing programs are also driving demand for cost-effective protective roofing solutions.

South Korea Protective Coatings Market: Maritime Leadership and Electronics Innovation

South Korea remains a global leader in marine and electronics coatings, driven by its dominance in shipbuilding and advanced manufacturing. The country has standardized the use of zinc silicate shop primers and antifouling coatings for LNG carrier construction, ensuring long-term durability.

Technological advancements include EMI/RFI shielding coatings used in 5G devices and telecommunications equipment. Investments in new specialty coating plants are expanding production capacity for high-performance anticorrosive coatings. Regulatory updates under K-REACH 2025 are improving chemical safety standards, while innovations such as anti-fingerprint coatings and fouling-release silicone-hydrogel systems are enhancing product performance and environmental sustainability.

Protective Coatings Market Report Scope

Protective Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$28.1 Billion

|

|

Market Size (2032)

|

$43.1 Billion

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Acrylic, Alkyd, Polyester, Zinc-Rich, Polysiloxane, Chlorinated Rubber, Fluoropolymer), By Technology (Solvent-borne Coatings, Water-borne Coatings, Powder Coatings, Radiation-Cured, 100% Solids), By Substrate (Metal, Concrete and Masonry, Plastics and Composites, Wood, Glass), By End-Use Industry (Infrastructure, Oil and Gas, Power Generation, Marine, Industrial Plants and Facilities, Mining and Metal Processing, Automotive and Transportation, Aerospace and Defense, Water and Wastewater Treatment), By Function (Anti-Corrosion, Fire Protection, Abrasion and Wear Resistance, Chemical and Acid Resistance, Heat, Anti-Fouling, UV and Weathering Resistance), By Sales Channel (Direct Sales, Specialty Industrial Coating Distributors, Professional Contractor Supply Channels)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., Akzo Nobel N.V., Jotun A/S, Hempel A/S, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Axalta Coating Systems Ltd., BASF SE, RPM International Inc., Sika AG, Asian Paints Limited, Chugoku Marine Paints, Ltd., KCC Corporation, Teknos Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Protective Coatings Market Segmentation

By Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Alkyd

- Polyester

- Zinc-Rich

- Polysiloxane

- Chlorinated Rubber

- Fluoropolymer

By Technology

- Solvent-borne Coatings

- Water-borne Coatings

- Powder Coatings

- Radiation-Cured

- 100% Solids

By Substrate

- Metal

- Concrete and Masonry

- Plastics and Composites

- Wood

- Glass

By End-Use Industry

- Infrastructure

- Oil and Gas

- Power Generation

- Marine

- Industrial Plants and Facilities

- Mining and Metal Processing

- Automotive and Transportation

- Aerospace and Defense

- Water and Wastewater Treatment

By Function

- Anti-Corrosion

- Fire Protection

- Abrasion and Wear Resistance

- Chemical and Acid Resistance

- Heat

- Anti-Fouling

- UV and Weathering Resistance

By Sales Channel

- Direct Sales

- Specialty Industrial Coating Distributors

- Professional Contractor Supply Channels

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Protective Coatings Industry

- Sherwin-Williams Company

- PPG Industries, Inc.

- Akzo Nobel N.V.

- Jotun A/S

- Hempel A/S

- Nippon Paint Holdings Co., Ltd.

- Kansai Paint Co., Ltd.

- Axalta Coating Systems Ltd.

- BASF SE

- RPM International Inc.

- Sika AG

- Asian Paints Limited

- Chugoku Marine Paints, Ltd.

- KCC Corporation

- Teknos Group

*- List not Exhaustive