Emergency Water Treatment Equipment Market Outlook

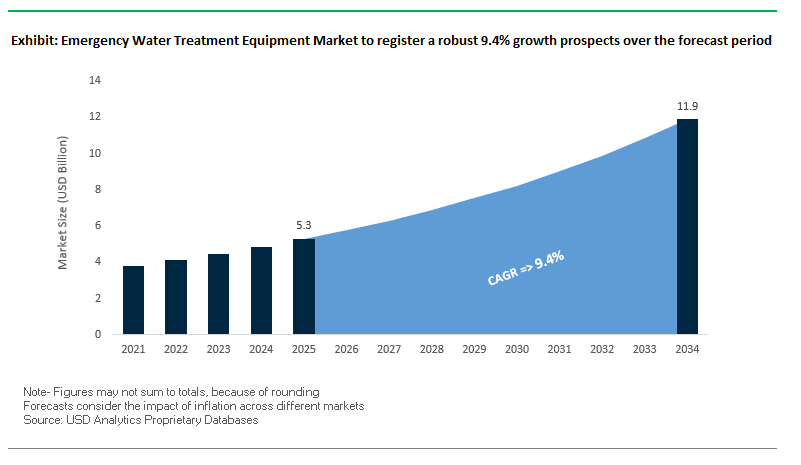

The global emergency water treatment equipment market is projected to grow from USD 5.3 billion in 2025 to USD 11.9 billion by 2034, achieving a compound annual growth rate (CAGR) of 9.4%. The strong upward trend reflects the increasing necessity for rapid-deployment potable water systems that can safeguard public health during disasters by preventing the spread of waterborne diseases.

Industry professionals and purchasing decision-makers are increasingly appreciating the strategic importance of gear that can treat variable feedwater sources such as floodwaters, polluted rivers, and seawaters via multi-stage sequences involving pre-filtration, membrane separation, and disinfection. It is especially motivated by a predominance of transportable and containerized "plug-and-play" configurations that obviate or circumvent any need for civil works and facilitate quick deployment to distant or infrastructurally-spoilt locations.

Technological innovation is also informing the next generation of emergency water treatment technology. Rising use of solar power units, long-range monitoring sensors, and control systems is improving resilience in off-grid locations while cutting operating expenses by reducing the deployment of on-site experts. Such developments not only present the sector as a humanitarian and environmental protection but can also be a strategic asset for business operating in disaster locations.

Strategic Imperatives for Shareholders:

- Prioritize multi-source water treatment capability to meet varied emergency scenarios.

- Invest in solar-powered and automated control systems to reduce dependency on external power and manual operation.

- Expand containerized and trailer-mounted product portfolios for fast and flexible deployment.

- Strengthen partnerships with government agencies, NGOs, and industrial sectors for long-term emergency contracts.

- Leverage digital monitoring platforms to offer predictive maintenance and enhance uptime during crises.

Market Analysis: Strong Demand Fueled by Disaster Response, Industrial Preparedness, and Infrastructure Resilience

The market’s momentum is reinforced by a series of strategic developments and deployments that illustrate its expanding role in public health protection, industrial continuity, and disaster recovery.

iSpring Water Systems donated 100 reverse osmosis and under-sink filters to flood communities in August 2025 in response to disastrous flooding in the state of Texas. Operating in collaboration with the Austin Disaster Relief Network, this rapid disaster response shows how convenient portable products can restore a source of safe drinking water in disaster aftermath scenarios.

Later in August 2025, Xylem furthered its message about enabling industrial disaster preparedness, while Strategy and Marketing Manager Chetan Mistry cited portable dewatering and rental fleet contracts as two important preparation strategies against unforeseeable weather for mines. That matches up within the company's overall plan of enabling both municipal and industrial customers to prepare against and manage operational risks.

Veolia's November 2023 collaboration between EDF and REEL is a highly technical deployment of emergency water treatment constructing mobile units within nuclear accident situations. With interchangeable filtration and adsorption cartridges, these units allow contaminated water to be treated on site, reflecting a capacity within the market to treat extreme and technically challenging emergencies.

WaterStep's work with the U.S. EPA on the "Water-on-Wheels" portable cart module reinforces this trend toward small-footprint, user-friendly systems that can be fielded and run by rapidly trained responders. Likewise, SUEZ's worldwide inventory of mobile water systems is built to be available around the clock, providing rapid response in municipal outages and breakdowns in industrial equipment.

Portability innovation can be seen in Crystal Quest's "ROVER" system, a portable, rugged water purifier that can treat water from almost any source designed especially for disaster relief applications. Veolia extended its rapid-response capacity further into Southeast Asia in March of 2024 by acquiring three modular trailer-mounted RO systems for use in Malaysia. These moveable solutions are part of a broader plan to bring flexible, on-demand treatment capabilities to high-growth and disaster-afflicted areas.

Thirdly, Xylem's proactive involvement across local governments in disaster plan preparations demonstrates a shift within the market toward a more service-based aspect where providers not only provide equipment but help customers design broad-based emergency plans. A shift toward comprehensive planning services bolsters customer relationships and strengthens long-term revenues.

Trends and Opportunities in Emergency Water Treatment Equipment Market

Trend 1: AI-Powered Rapid Deployment Systems for Disaster Zones

The emergency water treatment systems market is increasingly employing artificial intelligence (AI) and real-time monitoring to improve rapid deployment in disaster-hit locations. AI-based systems facilitate predictive maintenance by examining sensor inputs and past operational histories, recognizing patterns that indicate likely failures, and decreasing unplanned downtime. Real-time contamination alerts employing software such as the United States EPA's CANARY system provide operators with early notification of water quality irregularities, such that protected water is always safe to use. Such intelligent systems can automatically change chemical dosing levels, filtration rates, and operating parameters while optimizing energy efficiency and producing a consistent quality of water. By integrating AI, this consequently changes emergency response to supply rapid, consistent, and low-manpower water treatment in disastrous situations.

Trend 2: Solar-Hybrid Emergency Desalination for Coastal Disasters

Solar-hybrid emergency desalination units are becoming a vital answer to flood- and drought-prone coastal communities. Integrating reverse osmosis (RO) or ultrafiltration technology with solar or other renewable energy sources, these units provide a continued supply of clean water even if local power grids go down. With energy-efficient operating designs that use only 3.0 kWh/m³ or less and solar photovoltaics and energy storage to eliminate or decrease use of diesel generators, operational sustainability is improved while needing less. With solar-hybrid deployments tested to date, impressive environmental advantages and financial savings have been realized through CO2 emissions reduction and community water collection costs reduced by 40% or more. Through adaptability, these units can treat brackish floodwaters and seawaters during a drought or provide a multi-disaster scenario-compatible solution in a single package.

Opportunity 1: Military-Civilian Dual-Use Technology Transfer

Technologies designed for military applications in water treatment continue to be adopted in civilian disaster relief operations, opening new possibilities in the emergency water treatment equipment market. Military-specification systems, built to be hardened and portable, are now incorporated into civilian rapid-deployment units to achieve high contaminant removal and stand-alone water supply. Advanced membrane technology such as RO, ultrafiltration, and nanofiltration provide energy-efficient and high-quality purity water production. Portable tactical configurations enable rapid deployment in distant or disaster-struck locations while on-demand production ensures consistent supply for emergency responders. Technology transfer optimizes efficiency, minimizes logistics difficulties, and enhances resilience to civilian emergency water management operations.

Opportunity 2: Pharmaceutical Contaminant Crisis Response

Post-disaster water pollution due to pharmaceutical residue and non-traditional chemical contaminants is a new issue. Emergency water treatment has an increasing opportunity to utilize systems with advanced contaminant destruction capabilities, beyond conventional microbial disinfections. Advanced oxidation processes (AOPs), granular activated carbon (GAC), and specialty membrane filtration, such as reverse osmosis, are employed to remove complex organic molecules, such as pharmaceutical substances. With research calling attention to high levels of pharmaceutical concentrations in disaster-struck water supplies, these systems become paramount in public health defense. By treating chemical contaminants in addition to biological pathogens, companies can stand out in their offerings and fulfill a growing regulatory and humanitarian demand for integrated water treatment technology.

Emergency Water Treatment Equipment Market Share Insights

Market Share by Equipment Type: Portable Units and Rapid Deployment Systems at the Forefront

Portable purification units are forecasted to capture about 36.1% of the global emergency water treatment equipment market by 2025, reflecting their role as the first responder’s tool in crisis scenarios. Compact and hand-carried, these units are indispensable in the critical first 72 hours after disasters, providing safe drinking water for clinics, schools, and small communities. Meanwhile, rapid deployment systems represent the backbone of large-scale emergency response, where trailer-mounted and containerized treatment plants supply camps, hospitals, and distribution centers. The balance between immediate mobility and medium-capacity reliability ensures these two categories dominate adoption across global relief and defense operations.

.png)

Market Share by Capacity: 1,000–10,000 Liters/day Systems as the Response Sweet Spot

The 1,000–10,000 liters/day capacity range leads with around 41.7% of market share, positioning it as the most practical scale for both disaster relief agencies and municipal contingency planning. These systems can sustain hospitals, schools, or small community clusters with rapid deployment and manageable logistics. Larger systems between 10,000–100,000 liters/day are increasingly adopted in refugee and internally displaced persons (IDP) camps, where continuous water supply for thousands of people is critical. Ultra-portable units under 1,000 liters/day remain vital for scattered populations and frontline responders, while municipal-scale emergency plants above 100,000 liters/day are rare but strategic, often procured for urban disaster resilience programs.

Market Share by Power Source: Diesel Generators Still Leading, Solar Power Rising Rapidly

Generator and diesel-powered systems account for about 46.3% of the global emergency water treatment equipment market, underscoring their role as the workhorse of medium and large-scale deployments. They remain indispensable in disasters where grid power is down and fuel logistics can be established quickly. However, battery and solar-powered units are the fastest-growing segment, driven by their silent operation, long-term sustainability, and independence from volatile fuel supply chains. The makes them particularly attractive for military field operations and extended humanitarian missions in remote, sunny regions. Manual power systems retain importance for zero-resource emergency contexts, while grid-connected units remain niche, deployed primarily in contamination crises where infrastructure is intact.

Market Share by End-User: Disaster Relief Agencies as the Global Leaders in Deployment

Disaster relief agencies, including NGOs and international organizations, represent about 39.8% of market share, making them the largest end-user segment in the emergency water treatment equipment market. Their procurement priorities focus on ease of deployment, reliability against diverse contaminants, and adaptability to low-resource environments. Military and defense users form the second-largest segment, demanding ruggedized, mobile, and often stealth-capable units to support forward operating bases and humanitarian missions. Municipal water authorities are increasingly investing in containerized and plug-and-play systems for emergency preparedness and resilience, while industrial facilities remain niche buyers, prioritizing business continuity and sanitation during utility disruptions.

Country Analysis of the Emergency Water Treatment Equipment Market

United States: Advanced Mobile and Emergency Water Solutions

The U.S. emergency water treatment equipment market is being significantly driven by the Bipartisan Infrastructure Law, which allocates substantial funding for upgrading drinking water and wastewater infrastructure. The investment fuels demand for mobile and emergency water treatment solutions to maintain service during facility upgrades or contamination events. The EPA’s focus on emerging contaminants like PFAS has created a need for systems with advanced filtration and rapid-deployment capabilities. Leading companies, such as Culligan Commercial WaterWorks, offer Emergency Mobile Treatment Units capable of treating up to 800 gpm with comprehensive contaminant removal. Additionally, Pentair provides emergency solutions including battery backup sump pumps and reusable flood kits. Government initiatives like USDA Emergency Community Water Assistance Grants and the EPA’s Water Technical Assistance programs further enhance adoption, helping communities maintain water safety, resilience, and regulatory compliance during emergencies.

China: Robust Emergency Response and Mobile Water Treatment Infrastructure

China’s emergency water treatment systems market is strengthened by a national framework for rapid accident detection and contaminant removal. Legislation such as the Law of Emergency Response mandates structured emergency water management, supported by the Ministry of Ecology and Environment and the Ministry of Water Resources. Specialized emergency protocols, classified into four levels, rely on mobile and decentralized treatment systems and professional teams. Significant investment in rural drinking water safety projects has improved access for millions, while urban areas focus on centralized water supply supplemented by portable emergency water purification units. These efforts ensure safe drinking water in both urban and remote regions while fostering the adoption of advanced emergency water treatment solutions.

India: Mobile and Packaged Solutions for Rural and Emergency Water Supply

India’s Emergency Water Treatment Equipment Market benefits from initiatives like the Jal Jeevan Mission, which prioritizes safe drinking water in rural areas using mobile, packaged, and containerized purification systems. Financial support for states under the program encourages infrastructure development and the implementation of innovative water technologies. The Water Technology Initiative (WTI) further promotes research, development, and demonstration (RD&D) of sustainable water solutions suitable for emergency scenarios. Companies are deploying water ATMs and mobile treatment units that can rapidly respond to contamination events or supply shortages. State-level stationary and mobile laboratories enhance water quality monitoring, enabling timely detection and response during emergencies.

Japan: Disaster-Resilient Portable and Decentralized Systems

Japan’s emergency water treatment market is driven by a strong emphasis on disaster preparedness, innovation, and advanced technology. WOTA Corp. developed a portable water recycling system capable of reclaiming over 98% of wastewater, which was deployed after the 2024 Noto Peninsula Earthquake. Johkasou technology, pioneered by Daiki Axis, offers compact, self-contained decentralized sewage treatment systems ideal for emergency deployment. Japanese companies focus on compact, energy-efficient, and easy-to-operate systems, ensuring rapid installation and operation during disasters. The integration of IoT, sensors, and automated water quality monitoring enhances the reliability of emergency water supply in both urban and remote areas.

Germany: Modular, Plug-and-Play Systems for Rapid Deployment

Germany’s emergency water treatment equipment market is characterized by flexible, containerized plug-and-play water treatment plants, enabling rapid deployment in areas without sewer connectivity or during emergency situations. The German Association for Gas and Water (DVGW) supports the development of innovative technologies that promote the circular economy and energy-efficient wastewater treatment. Advanced membrane filtration and modular mobile systems are increasingly adopted to meet emergency and decentralized water needs. Companies like Wasser 3.0 focus on detecting and removing microplastics, offering rapid analysis crucial for identifying new contaminants during emergency events.

Saudi Arabia: Strategic Emergency Water Management and Mobile Solutions

Saudi Arabia’s emergency water treatment market is closely aligned with Vision 2030 and the National Water Strategy 2030, emphasizing water security and supply flexibility. The Saudi Water Authority (SWA) regulates water management and oversees emergency preparedness through tools like the Saudi Water Quality Index, enabling rapid assessment and decision-making. Investments in treated wastewater for industrial purposes and mobile infrastructure solutions provide dual-use capabilities for emergency situations. The ongoing development of major urban and industrial projects increases demand for temporary and mobile water treatment units, which are crucial for emergency preparedness, regulatory compliance, and operational resilience.

Competitive Landscape: Key Players Driving Innovation and Rapid Deployment in Emergency Water Treatment

The emergency water treatment equipment market is characterized by a competitive mix of global leaders offering containerized, trailer-mounted, and portable treatment solutions supported by strong service networks. These companies differentiate themselves through rapid deployment capabilities, diverse application coverage, and integration of advanced monitoring technologies.

Veolia Environnement S.A. – Global Leader in On-Demand Mobile Water Treatment

Veolia’s emergency water treatment strategy centers on fast-response, on-demand solutions backed by a global fleet of mobile demineralization units, RO/UF membrane trailers, and carbon filtration systems. These units can process everything from river water to complex industrial effluents. Notably, its partnership with EDF on a nuclear emergency water treatment system showcases its expertise in specialized, high-risk scenarios. Expansion in Brazil and Malaysia reinforces Veolia’s global reach, while its InSight digital platform delivers real-time monitoring and predictive maintenance to ensure maximum reliability during emergencies.

SUEZ S.A. – Flexible, Containerized Systems for Municipal and Industrial Emergencies

SUEZ focuses on delivering containerized RO and UF systems engineered for rapid deployment in both municipal and industrial contexts. Its 24/7 logistics and extensive global network enable it to respond swiftly to outages and disasters. Known for its customizable configurations, SUEZ ensures water quality compliance even under extreme conditions. Digital platforms and field experts support seamless integration with existing networks, making SUEZ a trusted partner for cities and industries requiring both reliability and speed.

Xylem Inc. – Integrated Equipment and Service Solutions for Disaster Preparedness

Xylem differentiates itself with a broad rental fleet of pumps, filtration systems, and treatment equipment under brands like Godwin and Flygt. The company’s strategy integrates equipment provision with disaster preparedness planning for clients, ensuring that contingency measures are in place before emergencies occur. Xylem’s off-grid-capable units are vital in power-outage situations, and its vast network of branches enables rapid mobilization anywhere in the world. By combining engineering expertise with a comprehensive product portfolio, Xylem offers a turnkey solution for both immediate response and long-term resilience.

Emergency Water Treatment Equipment Market Report Scope

Emergency Water Treatment Equipment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.3 Billion

|

|

Market Size (2034)

|

$11.9 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Equipment Type (Portable Purification Units, Rapid Deployment Systems, Bulk Water Treatment Solutions, Disinfection Equipment), By Capacity (<1,000 Liters/day, 1,000–10,000 Liters/day, 10,000–100,000 Liters/day, >100,000 Liters/day), By Power Source (Manual, Battery/Solar-Powered, Generator/Diesel-Powered, Grid-Connected), By End-User (Disaster Relief Agencies, Military & Defense, Municipal Water Authorities, Industrial Facilities)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, Xylem Inc., Fluence Corporation, Sustainable Biosolutions Private Limited (SUSBIO), Aquatech International LLC, Culligan Water, Pentair, Trojan Technologies, IDE Technologies, Kurita Water Industries, Katadyn, MSR (Mountain Safety Research), LifeStraw

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Emergency Water Treatment Equipment Market Segmentation

By Equipment Type

- Portable Purification Units

- Handheld UV purifiers

- Gravity-fed filters

- Straw-style personal filters

- Rapid Deployment Systems

- Mobile treatment trailers

- Inflatable water tanks with filtration

- Compact RO/UF units

- Bulk Water Treatment Solutions

- High-capacity filtration systems

- Chemical dosing stations

- Modular desalination units

- Disinfection Equipment

- Chlorine generators

- Ozonation units

- UV sterilization systems

By Capacity

- <1,000 Liters/day

- 1,000–10,000 Liters/day

- 10,000–100,000 Liters/day

- >100,000 Liters/day

By Power Source

- Manual

- Battery/Solar-Powered

- Generator/Diesel-Powered

- Grid-Connected

By End-User

- Disaster Relief Agencies

- Military & Defense

- Municipal Water Authorities

- Industrial Facilities

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Emergency Water Treatment Equipment Market

- Veolia

- Xylem Inc.

- Fluence Corporation

- Sustainable Biosolutions Private Limited (SUSBIO)

- Aquatech International LLC

- Culligan Water

- Pentair

- Trojan Technologies

- IDE Technologies

- Kurita Water Industries

- Katadyn

- MSR (Mountain Safety Research)

- LifeStraw

* List Not Exhaustive

Research Coverage

This report investigates the Global Emergency Water Treatment Equipment Market, delivering analysis reviews on rapid-deployment potable water technologies, industry-specific adoption, and technological breakthroughs reshaping disaster response and resilience strategies. Published by USDAnalytics, the study highlights how demand is surging due to climate-related disasters, industrial contingency planning, and the growing need for mobile, plug-and-play treatment systems capable of handling diverse water sources from floodwater to seawater. It examines how leading companies like Veolia, SUEZ, and Xylem are innovating with solar-hybrid desalination, AI-driven monitoring, and modular trailer-mounted RO systems, offering immediate access to safe water in critical scenarios. With detailed market forecasts, regional adoption patterns, and strategic imperatives for stakeholders, this report is an essential resource for industry professionals, regulators, NGOs, and investors navigating the fast-growing emergency water treatment sector.

Scope Includes:

- Segmentation: By Equipment Type (Portable Units, Rapid Deployment Systems, Containerized Plants, Trailer-Mounted Units), By Capacity (Under 1,000 L/day, 1,000–10,000 L/day, 10,000–100,000 L/day, Above 100,000 L/day), By Power Source (Diesel, Solar, Battery, Manual, Grid-Connected), and By End-User (Disaster Relief Agencies, Military, Municipal Authorities, Industrial Facilities).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic & Forecast: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Profiles and competitive strategies of 15+ global leaders including Veolia, SUEZ, Xylem, Pentair, Culligan, and Crystal Quest.

Methodology

The research methodology adopted by USDAnalytics integrates primary interviews and secondary data analysis to deliver reliable and actionable insights. Primary research included structured discussions with relief agencies, municipal utilities, military procurement specialists, and water technology providers to validate adoption patterns and operational challenges. Secondary research leveraged regulatory frameworks, company reports, humanitarian case studies, and academic publications to capture market dynamics. Market sizing applied both top-down and bottom-up approaches, reconciled through triangulation across regions, equipment categories, and end-user segments. Advanced scenario modeling factored in disaster frequency, government funding cycles, and technological adoption rates, ensuring that the projections reflect realistic, data-driven expectations for the global emergency water treatment equipment market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Emergency Water Treatment Equipment Market

1. Executive Summary

1.1. Market Highlights

1.2. Strategic Imperatives for Shareholders

1.3. Global Market Snapshot

2. Emergency Water Treatment Equipment Market Overview (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $5.3 Billion

2.2.2. Forecasted Market Size (2034): $11.9 Billion at 9.4% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Increasing Frequency of Natural Disasters

2.3.2. Demand for Rapid-Deployment and "Plug-and-Play" Solutions

2.3.3. Technological Advancements in Membrane Separation and Disinfection

2.3.4. Growing Focus on Public Health and Disease Prevention

3. Market Analysis: Strategic Deployments and Infrastructure Resilience

3.1. Overview of Market Momentum

3.2. Strategic Developments of Key Players

3.2.1. iSpring Water Systems's Rapid Disaster Response

3.2.2. Xylem's Focus on Industrial Preparedness and Rental Fleets

3.2.3. Veolia's Specialization in High-Risk Emergency Scenarios

3.2.4. SUEZ's Global Inventory of Mobile Water Systems

3.3. Government and Humanitarian Initiatives

3.3.1. Partnerships with Agencies like the U.S. EPA and NGOs

3.3.2. Shift toward Comprehensive Emergency Planning Services

4. Trends and Opportunities in Emergency Water Treatment Equipment

4.1. Trend 1: AI-Powered Rapid Deployment Systems

4.1.1. Predictive Maintenance and Automated Process Control

4.1.2. Real-Time Contamination Alerts

4.2. Trend 2: Solar-Hybrid Emergency Desalination

4.2.1. Off-Grid Water Supply for Coastal Disasters

4.2.2. Energy Efficiency and Reduced Environmental Footprint

4.3. Opportunity 1: Military-Civilian Dual-Use Technology Transfer

4.3.1. Adoption of Rugged, Portable Military-Spec Systems

4.3.2. Enhanced Contaminant Removal Capabilities

4.4. Opportunity 2: Pharmaceutical Contaminant Crisis Response

4.4.1. Addressing Non-Traditional Chemical Contaminants

4.4.2. Advanced Oxidation Processes (AOPs) and Specialty Filtration

5. Emergency Water Treatment Equipment Market Share Insights

5.1. By Equipment Type

5.1.1. Portable Purification Units

5.1.2. Rapid Deployment Systems

5.1.3. Bulk Water Treatment Solutions

5.1.4. Disinfection Equipment

5.2. By Capacity

5.2.1. <1,000 Liters/day

5.2.2. 1,000–10,000 Liters/day

5.2.3. 10,000–100,000 Liters/day

5.2.4. >100,000 Liters/day

5.3. By Power Source

5.3.1. Generator/Diesel-Powered

5.3.2. Battery/Solar-Powered

5.3.3. Manual and Grid-Connected

5.4. By End-User

5.4.1. Disaster Relief Agencies

5.4.2. Military & Defense

5.4.3. Municipal Water Authorities

5.4.4. Industrial Facilities

6. Country Analysis of the Emergency Water Treatment Equipment Market

6.1. United States: Infrastructure Resilience and Advanced Mobile Solutions

6.2. China: National Emergency Response Framework and Mobile Infrastructure

6.3. India: Rural Access and Packaged Solutions

6.4. Japan: Disaster-Resilient Portable Systems

6.5. Germany: Modular, Plug-and-Play Systems for Rapid Deployment

6.6. Saudi Arabia: Strategic Emergency Water Management

6.7. Other Country Analysis

7. Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Equipment Type, Capacity, Power Source, and End-User

7.2. Europe Market Size Outlook to 2034

7.2.1. By Equipment Type, Capacity, Power Source, and End-User

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Equipment Type, Capacity, Power Source, and End-User

7.4. South America Market Size Outlook to 2034

7.4.1. By Equipment Type, Capacity, Power Source, and End-User

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Equipment Type, Capacity, Power Source, and End-User

8. Competitive Landscape: Leading Players in Emergency Water Treatment Equipment

8.1. Veolia

8.2. Xylem Inc.

8.3. Fluence Corporation

8.4. Sustainable Biosolutions Private Limited (SUSBIO)

8.5. Aquatech International LLC

8.6. Culligan Water

8.7. Pentair

8.8. Trojan Technologies

8.9. IDE Technologies

8.10. Kurita Water Industries

8.11. Katadyn

8.12. MSR (Mountain Safety Research)

8.13. LifeStraw

8.14. SUEZ

8.15. VA Tech Wabag Ltd.

8.16. Thermax Limited

8.17. Ion Exchange India Ltd.

8.18. Corix Water System

8.19. RWL Water

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations