Mobile Water Treatment Systems Market Outlook

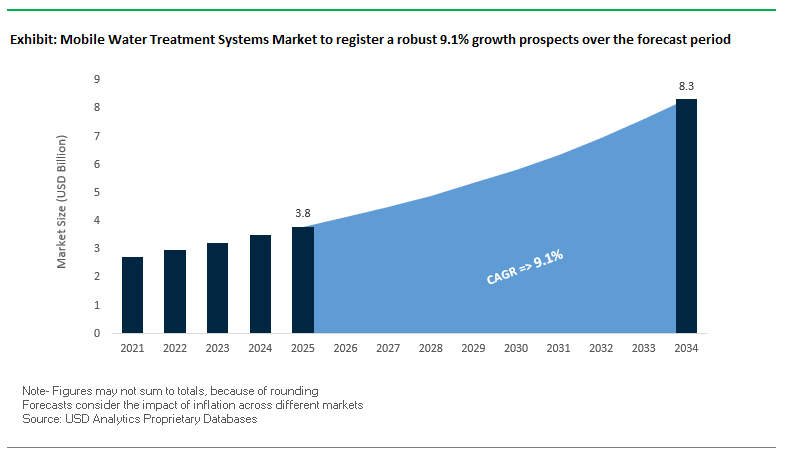

The global mobile water treatment systems market is set to grow from USD 3.8 billion in 2025 to USD 8.3 billion by 2034, reflecting a CAGR of 9.1% over the forecast period. The robust expansion is being fueled by the increasing need for rapid-deployment water purification solutions across emergency relief operations, industrial continuity plans, and high-purity water production applications.

Industry professionals recognize mobile water treatment solutions as invaluable in disaster response initiatives, while governmental agencies like the United States Environmental Protection Agency (EPA) and non-profits like WaterStep spearhead deployments to recover potable water supplies after hurricanes, flooding, and other catastrophic events. Concomitant with relief efforts, the application in the industrial market consisting of oil & gas, power generation, and manufacturing involving planned maintenance, plant expansion work, and unplanned power outages is gaining traction to achieve compliance and operational uptime.

It is also transformed by innovation in technology driven mainly by membrane-based purification like ultrafiltration (UF) and reverse osmosis (RO). These become indispensable in satisfying highly stringent quality requirements of process water and treated effluent/wastewater reuse. On top of these developments, the market is tilting toward a trend toward containerized and module-based plug-and-play designs that have a correspondingly reduced on-site installation time and requirements for civil works.

Key Industry Insights for Decision-Makers:

- Emergency Readiness: Disaster relief agencies and industrial operators alike are investing in mobile RO and UF systems for rapid deployment during crises.

- Industrial Integration: Mobile water units are increasingly integrated into existing plant infrastructure to maintain production during maintenance or emergencies.

- Technology Backbone: Membrane-based filtration remains the dominant choice for achieving high-purity water and wastewater reuse standards.

- Design Evolution: Containerized and modular units lead the market, offering faster setup and lower operational disruptions.

Global Mobile Water Treatment Systems Market Analysis: Expansion Strategies, Technological Advancements, and Regional Developments

Mobile water treatment systems market is undergoing rapid changes driven both by major players' strategic investments and environmental and regulatory imperatives. Veolia announced in July 2025 that Nicole Springer was appointed CEO of its Mobile Water and Integrated Services business unit in a move to accelerate efforts to expand the firm's largest-in-industry mobile fleet and enhance ability to respond to emergencies.

Capacity expansion remains a key theme. Three trailer-mounted reverse osmosis (RO) units were dispatched to Malaysia in March 2024 by Veolia to solidify its presence in Southeast Asia's industrial water services market. Another move to solidify global coverage was made by Veolia in April 2025 with a new Mobile Water Service Center launched in Cajamar, Brazil. It is meant to improve service rapidity for industrial and municipal clients across Latin America.

Governments are also making mobile water in emergencies a priority. In July 2025, the United States EPA and WaterStep initiated the Water-on-Wheels (WOW) Cart program involving modular systems built to provide a system for safe drinking water in hurricane- or flood-struck areas.

Other market players are also making progress in capabilities. SUEZ has won recent contracts in the Philippines, China, and Singapore, demonstrating flexibility in meeting containerized desalination and wastewater recycling units to a range of water quality challenges. Xylem has expanded its technological advantage by acquiring Idrica in December 2024, bringing AI-based monitoring to its portable water services. Xylem introduced new online water quality monitoring services in May 2025, indispensable to optimizing mobile treatment performance in real-time.

sector-based applications broaden too. With downstream applications for oil and gas extending from boiler feed water preparation to temporary demineralization to even wastewater reclaims, operators can apply mobile water treatment to reduce capital investments in permanent facilities while still maintaining compliance.

Trends and Opportunities in Mobile Water Treatment Systems Market

Trend 1: Rapid Deployment for Disaster Response & Emergency Water Supply

Mobile water treatment systems market is experiencing rapid growth driven by increasing occurrence and severity of natural disasters and demand for sustainable emergency water infrastructure. Mobile water treatment systems provide quick, plug-and-play installation to deliver safe drinking water in disaster-struck areas to respond to key public health emergencies. Examples like the United States EPA's "Water-on-Wheels (WOW) Mobile Water Treatment System" highlight innovation in transportable water treatment that can produce up to 10 gallons per minute with optional power sources. Practical applications prove efficiency: in disaster-struck Turkey post-earthquake, mobile purification units effectively minimized turbidity and inactivated pathogens to WHO quality levels. State-of-the-art emergency units come equipped with multi-stage treatability features such as filtration, UV disinfection, and chemical treatability to manage suspended solids, organics, and microbial threats to provide potable water supplies in emergencies.

Trend 2: Modular Systems for Temporary Industrial & Municipal Use

Industrial and municipal applications still utilize modular mobile water treatment systems to achieve temporary or intermittent water supply demands such as maintenance work, modernization of a plant, or capacity augmentation. Such systems ensure maintained operations while regulatory compliance remains intact. A manufacturer of specialty chemicals, for instance, maintained uninterrupted 24-hour production while operating mobile ion exchange and reverse osmosis units during renovation. Plug-and-play architecture allows rapid commissioning within a few days; some units become operational within 72 hours after despatch, a schedule far shorter than conventional plant installation. Flexibility in rental or leasing model supports a reasonably priced solution, enabling temporary use without permanent installation's upfront capex. The trend substantiates growing demand for scalable, temporary, and affordable mobile water treatment applications in municipal and industrial applications

Opportunity 1: Offshore & Remote Site Applications

Mobile water treatment systems become even more indispensable in offshore and distant places such as oil rigs, mines, and military camps where centralized water supply does not exist. Such systems allow on-site production of water by treating seawater or dirty sources to yield potable and process water while meeting stringent environmental regulations. Offshore reverse osmosis units, say, eliminate between 99.9% and all dissolved salts, pathogens, and contaminants to allow for trouble-free operations. Portable and robust designs such as shipping containers facilitate ease of transportation and deployment in cramped and unforgiving habitats. The market prospect in The segment continues to increase due to rising numbers of remote defense and industrial locations worldwide which require self-contained, portable solutions for treating water.

Opportunity 2: Event-Based Water Treatment for Mega-Events

Large events such as Olympics, World Cup, and large music festivals create episodic but aggregate water demand. Trucked or trailer-mounted water treatment units provide sustainable on-site solutions that mitigate bottled-water usage and municipal-grid demand. Portable units can produce tens of thousands of gallons daily of potable water to accommodate attendees' and personnel's use. The solution supports environmental sustainability targets while keeping use of single-use plastic packaging to a minimum and enabling local-source water treatment while effectively bypassing infrastructural limitations. Greater focus on environmentally friendly, efficient, and rapid-response solutions within high-visibility events makes mobile water treatment units a prime market segment.

Mobile Water Treatment Systems Market Share Insights

Market Share by System Type: Filtration Systems Retain Core Dominance

Filtration systems are projected to capture nearly 40% of the global mobile water treatment systems market share by 2025, underlining their position as the backbone of mobile treatment technologies. Leveraging ultrafiltration (UF) and reverse osmosis (RO) membranes, these systems are crucial for desalination, high-purity water production, and industrial wastewater recovery. Chemical treatment systems remain critical in pathogen control and process-specific applications, particularly in emergency deployments where chlorination and ozonation ensure water safety. Meanwhile, specialized treatment systems are carving out share in contaminant-specific removal, such as PFAS, nitrates, and heavy metals making them a high-value niche for industries facing stricter discharge regulations.

Market Share by Mobility Configuration: Containerized Systems as the Global Standard

Containerized mobile water treatment systems account for about 50% of market share, making them the gold standard for both rental and permanent deployments. Their ability to protect sensitive RO membranes, enable global transport via ship, rail, or truck, and ensure quick commissioning has solidified their adoption in large-scale industrial and municipal projects. Trailer-mounted systems are expanding in rapid-deployment use cases such as disaster relief and construction projects, where road-readiness is critical. Vehicle-integrated systems serve specialized, ultra-mobile applications such as military operations, remote oil & gas sites, and first-responder units where portability outweighs scale.

.png)

Market Share by Treatment Capacity: Medium-Scale Systems Driving Industrial & Community Demand

The medium-scale (50–500 m³/day) segment is projected to hold 45% of the market share, driven by demand from industrial operations, plant upgrades, and small community water supply. These systems strike a balance between scalability and mobility, making them the most versatile category. Small-scale systems remain crucial in emergency water supply and disaster relief, serving field hospitals, refugee camps, and remote outposts where point-of-use treatment is essential. Large-scale (>500 m³/day) units are strategically important in municipal backup supply, major industrial shutdowns, and refugee support high-value projects that command significant rental and engineering resources.

Market Share by Application: Industrial Uses Leading with 60% Share

Industrial applications dominate the mobile water treatment systems market with an estimated 60% share by 2025, as industries increasingly rely on mobile solutions for continuity during plant turnarounds, construction dewatering, and off-grid mining or oil & gas projects. Emergency and disaster relief is a high-growth application, supported by government and NGO investments to address hurricanes, earthquakes, and refugee crises. Other uses such as municipal backup supply during droughts or major public events highlight how mobile water treatment is extending beyond core industrial and humanitarian sectors into urban resilience and event-based water solutions.

Market Share by Water Source: Surface Water & Groundwater Leading, Seawater Desalination Gaining Strategic Role

Surface water treatment contributes around 30% of the market share, reflecting its widespread use in emergencies and construction projects drawing from rivers, lakes, and ponds. Groundwater treatment follows closely, especially for pump-and-treat remediation of contaminated aquifers and removal of naturally occurring elements such as iron and arsenic. Wastewater treatment is gaining traction in industries seeking to reduce intake and discharge costs through reuse strategies. Meanwhile, seawater desalination represents a strategically critical niche for coastal and island communities, offshore facilities, and defense applications, where containerized SWRO units are essential for freshwater security.

Market Share by Rental vs Purchase Model: Short-Term Rentals Dominate with 40% Share

Short-term rental systems lead with about 40% share, underlining the preference for flexibility, quick deployment, and low upfront cost in emergencies and construction projects. The model also acts as a "try before you buy" pathway, appealing to industries with fluctuating water needs. Long-term lease systems are expanding in multi-year remediation and industrial operations, providing CAPEX-free access to mobile treatment technologies. Outright purchase remains the strategy of choice for militaries, utilities, and large industrial operators that require permanent mobile treatment infrastructure for recurring emergencies or strategic redundancy.

Market Share by Level of Automation: Fully Automated Systems as the Reliability Benchmark

Fully automated mobile water treatment systems command approximately 50% of the market share, as industries and municipalities increasingly demand systems capable of remote monitoring via SCADA/IoT, PLC-controlled adjustments, and minimal operator intervention. Semi-automated units remain relevant in construction sites and mid-scale industrial projects where skilled staff are already present on-site. Manual systems represent a niche low-cost alternative for basic treatment tasks or low-resource settings, where reduced capital outlay justifies higher operator involvement. The dominance of automation reflects the industry’s shift toward operational resilience, water quality consistency, and reduced human error in mission-critical deployments.

Country Analysis of the Mobile Water Treatment Systems Market

United States: Flexible Solutions for Contamination and Infrastructure Upgrades

The United States mobile water treatment systems market is driven by large investments pursuant to the Bipartisan Infrastructure Law, committing funds to modernize drinking water and wastewater facilities. Municipal authorities continue to adopt portable and modular drinking water purification systems to provide continued water service while facilities are undergoing upgrade and respond to new contaminants like PFAS. DuPont's PES ultrafiltration membranes are now part of mobile systems to achieve higher efficiency in municipal, industrial, and RO applications. Furthermore, the combination of Culligan and Waterlogic Inc. amplifies the ability of the market to provide sustainable and fast-deployment water solutions. Mobile systems are similarly essential in a disaster response situation to provide immediate accessibility to a source of safe drinking water in flood and wildland fires and other disasters.

China: IoT and AI-Driven Smart Mobile Water Treatment Units

China's push to modernize existing water structures by "Water Ten Plan" and the 14th Five-Year Plan is fostering an environment conducive to smart, mobile applications for water treatment. Veolia Water Technologies expanded its fleet of mobile units with trailer-mounted reverse osmosis (RO) units that can be easily transported across chemicals, petrochemicals, and power facilities. IoT-based sensors and analytical technology powered by AI work in harmony to create real-time monitoring of water quality and predictive maintenance to enable even rural and disaster-struck locations to monitor and manage water safety independently. With a likely reach above $12 billion by 2025 in the market for smart water monitoring, mobile units for water purification remain considered a scalable, technically advanced solution both in industries and municipal applications.

India: Rural Access and Government-Driven Innovation

India's Jal Jeevan Mission focuses on ensuring safe potable water for all rural families and identifying a role for innovative mobile water treatment technology in inaccessible terrain. Startups and innovators are motivated by the AMRUT 2.0 plan to innovate new urban water applications involving containerized and mobile purification units. Initiatives like India's Water Technology Initiative (WTI) facilitate R&D on sustainable water applications and accelerate the use of mobile treatment technology. Ponds sand filters and "water ATMs" or portable and containerized purification and dispensing units are being used by companies to achieve effective water access in arid watersheds.

Germany: Modular and Containerized Mobile Water Treatment Plants

Germany's mobile water treatment system market is fueled by technology innovation in modular and containerized plants. Klaro GmbH is creating plug-and-play systems to treat wastewater in standard shipping containers that can be deployed fast. High-end membrane filtration technology and energy-efficient solutions continue to be made available in mobile applications to allow easy installation and decentralization. German Association for Gas and Water (DVGW) advocates water protection and circular economy concepts, while stringent standards by the Federal Environment Agency keep mobile treatment units at high-quality hygienic and toxicological levels and boost a mature market in portable water treatment technology.

Japan: Portable, IoT-Enabled Water Solutions for Disaster Management

Japan is at the forefront of portable and mobile water treatment technologies, integrating advanced sensors, IoT, and machine learning for water quality monitoring and prediction. Startups like WOTA Corp. have developed systems capable of reclaiming over 98% of wastewater, deployed during emergencies such as the 2024 Noto Peninsula Earthquake. The fully automated systems utilize digital algorithms for optimized treatment control, making them user-friendly and efficient. Additionally, Johkasou technology, pioneered by companies like Daiki Axis, offers compact, decentralized sewage treatment solutions ideal for mobile applications, disaster relief, and remote areas, demonstrating Japan’s leadership in emergency-ready and decentralized water purification solutions.

Middle East (UAE & Saudi Arabia): Mobile Water Solutions for Industrial and Construction Needs

The Middle East mobile water treatment market is expanding due to high demand in oil & gas, construction, and remote industrial locations. Veolia implemented a 16,000 m³/day mobile system for Ezz Steel in Egypt, featuring trailer-mounted RO units and ultrafiltration containerized plants to reduce reliance on Nile River water. Almar Water Solutions operates fleets of mobile plants offering urgent, short-term solutions for industrial clients. Ongoing mega-infrastructure projects, such as the Hassyan seawater desalination plant in the UAE and the Zuluf water treatment project in Saudi Arabia, create additional demand for temporary and mobile water treatment systems during construction and commissioning phases, emphasizing flexibility, rapid deployment, and operational efficiency.

Competitive Landscape: Global Leaders in Mobile Water Treatment Systems

The mobile water treatment systems market is shaped by global giants with extensive fleets, proprietary technologies, and integrated service offerings. These companies differentiate through rapid deployment capabilities, advanced membrane technologies, and regional service networks that cater to both industrial and emergency use cases.

Veolia Environnement S.A. – Expanding the World’s Largest Mobile Water Fleet

Veolia’s strategy is centered on comprehensive, on-demand mobile water solutions, supported by the largest fleet in the industry. The company offers a wide range of trailer-mounted and containerized systems utilizing UF, RO, and demineralization technologies. Recent expansions include the Cajamar facility in Brazil and new modular RO units in Malaysia, enhancing regional response capabilities. Veolia is also known for integrating mobile units seamlessly into existing plant operations, providing both temporary and emergency water capacity with minimal downtime.

SUEZ S.A. – Innovating with Containerized and Digital Water Solutions

SUEZ specializes in rapid-deploying, high-performing water treatment systems available for desalination applications, wastewater reuse applications, and high-salinity applications. Its mobile offerings consist of small-footprint RO systems and tailor-made containerized units supported by sophisticated digital solutions enabling real-time performance monitoring and energy management. SUEZ's global reach and capacity to tailor a solution to suit both municipal and industrially-oriented customers continue to be chief strengths against competitors.

Xylem Inc. – Digital Intelligence Meets Mobile Water Solutions

Xylem Rental Solutions has a full portfolio of temporary pumping, filtration, and treatment solutions in known brands such as Godwin and Flygt. With its December 2024 acquisition of Idrica, Xylem has expanded its portfolio with AI-based monitoring and leak detection in real time. It covers customers via a broad network of service centers that provide full project management from basic dewatering to highly advanced and sophisticated temporary treatment applications.

DuPont Water Solutions – Membrane Technology Backbone for Mobile Systems

DuPont is a world leader in high-performing membrane elements, especially FilmTec™ RO and UF membranes that are at the heart of numerous mobile water systems. Desalination units in containerized applications benefit from installation efficiency and performance through the company's innovative products like dry SWRO membrane elements. DuPont products find common application in emergency drinking water supply, process water in industry applications, and use in aeration or effluent reuse application to be a principal supplier to global mobile water service operators.

Mobile Water Treatment Systems Market Report Scope

Mobile Water Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.8 Billion

|

|

Market Size (2034)

|

$8.3 Billion

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By System Type (Filtration Systems, Chemical Treatment Systems, Specialized Treatment Systems), By Mobility Configuration (Trailer-Mounted Systems, Containerized Systems, Vehicle-Integrated Systems), By Treatment Capacity (Small-scale (<50 m³/day), Medium-scale (50-500 m³/day), Large-scale (>500 m³/day)), By Application (Emergency & Disaster Relief, Industrial Applications), By Water Source (Surface Water Treatment, Groundwater Treatment, Wastewater Treatment, Seawater Desalination), By Rental vs Purchase Model (Short-term Rental Systems, Long-term Lease Systems, Outright Purchase Systems), By Level of Automation (Manual Operation Systems, Semi-automated Systems, Fully Automated Systems)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia Water Technologies, Xylem Inc., SUEZ, Evoqua Water Technologies (now part of Xylem), Pentair, Aquatech International LLC, DuPont, Lenntech B.V., Pall Water Processing, MPW, Ecolutia, Applied Membranes Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Mobile Water Treatment Systems Market Segmentation

By System Type

- Filtration Systems

- Membrane filtration

- Media filtration

- Cartridge filters

- Chemical Treatment Systems

- Disinfection units

- Coagulation/flocculation systems

- pH adjustment systems

- Specialized Treatment Systems

- Deionization units

- Desalination systems

- Heavy metal removal systems

By Mobility Configuration

- Trailer-Mounted Systems

- Containerized Systems

- Vehicle-Integrated Systems

By Treatment Capacity

- Small-scale (<50 m³/day)

- Medium-scale (50-500 m³/day)

- Large-scale (>500 m³/day)

By Application

- Emergency & Disaster Relief

- Industrial Applications

- Oil & gas operations

- Mining camps

- Power plants

- Construction sites

- Municipal & Utility

- Military & Defense

By Water Source

- Surface Water Treatment

- Groundwater Treatment

- Wastewater Treatment

- Seawater Desalination

By Rental vs Purchase Model

- Short-term Rental Systems

- Long-term Lease Systems

- Outright Purchase Systems

By Level of Automation

- Manual Operation Systems

- Semi-automated Systems

- Fully Automated Systems

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Mobile Water Treatment Systems Market

- Veolia Water Technologies

- Xylem Inc.

- SUEZ

- Evoqua Water Technologies (now part of Xylem)

- Pentair

- Aquatech International LLC

- DuPont

- Lenntech B.V.

- Pall Water Processing

- MPW

- Ecolutia

- Applied Membranes Inc.

* List Not Exhaustive

Research Coverage

This report investigates the Global Mobile Water Treatment Systems Market, delivering in-depth analysis reviews of emergency response applications, industrial continuity solutions, and technological breakthroughs shaping the sector. Published by USDAnalytics, it highlights how increasing climate-related disasters, stringent industrial water standards, and innovations in membrane-based purification are fueling strong adoption worldwide. The study examines how leading companies like Veolia, SUEZ, Xylem, and DuPont are expanding fleets, integrating AI-driven monitoring, and pioneering modular, containerized designs that reduce setup time and enhance reliability. By assessing regional policies, sector-specific adoption, and system-level advancements, this report is an essential resource for industry professionals, regulators, and investors navigating the fast-evolving landscape of mobile water treatment systems.

Scope Includes:

- Segmentation: By System Type (Filtration, Chemical, Specialized Treatment), By Mobility Configuration (Containerized, Trailer-Mounted, Vehicle-Integrated), By Capacity (Small, Medium, Large-Scale), By Application (Industrial, Emergency Relief, Municipal & Events), By Water Source (Surface Water, Groundwater, Wastewater, Seawater), By Rental vs Purchase Model (Rental, Lease, Purchase), and By Automation Level (Manual, Semi-Automated, Fully Automated).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Historic & Forecast: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Profiles and competitive analysis of 15+ leading companies including Veolia, SUEZ, Xylem, DuPont, and others.

Methodology

The research methodology adopted by USDAnalytics combines primary interviews and secondary data analysis to ensure comprehensive and validated market insights. Primary research included structured discussions with water treatment specialists, emergency response agencies, utility operators, and industrial end-users to capture practical deployment challenges and adoption strategies. Secondary research leveraged regulatory documents, company reports, technical journals, and global water infrastructure databases. Market size estimates were derived through both top-down and bottom-up approaches, reconciled using data triangulation and scenario analysis across disaster relief, industrial integration, and municipal applications. This multi-layered methodology ensures that the findings deliver a reliable, data-backed, and forward-looking assessment of the global mobile water treatment systems market.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.