Water Treatment System Leasing Market Overview

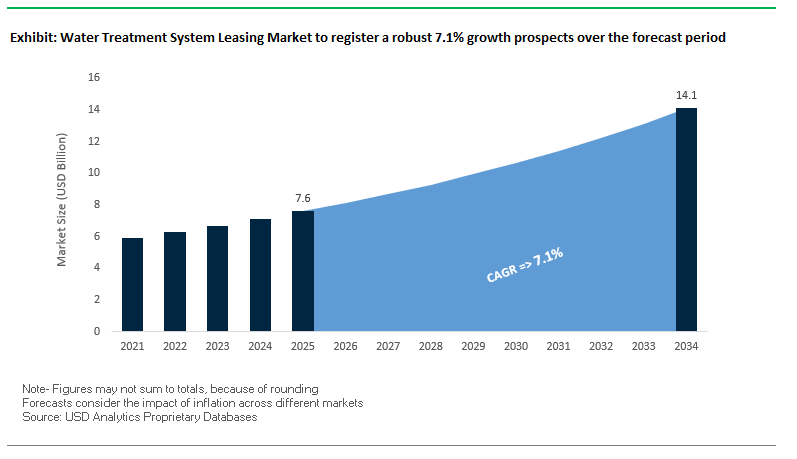

The global water treatment system leasing market is projected to grow from $7.6 billion in 2025 to $14.1 billion by 2034, registering a CAGR of 7.1%. This growth is primarily driven by industrial and commercial clients seeking CapEx-free access to advanced water treatment technologies, coupled with the need for flexible, scalable solutions that address fluctuating water demands. Leasing models allow companies to convert large upfront investments into predictable operational expenses, making this approach attractive for startups, temporary projects, and organizations facing budget constraints.

The market also benefits from increasing regulatory pressure on water quality, sustainability mandates, and the emergence of contaminants such as PFAS, which require rapid deployment of treatment solutions. Leasing ensures optimized operations, reduced energy consumption, and adherence to environmental standards while providing immediate access to state-of-the-art technologies.

Key Insights for Industry Stakeholders:

- CapEx-Avoidance: Leasing enables industrial and commercial users to access advanced water treatment systems without significant upfront costs.

- Flexibility and Scalability: Solutions can be scaled based on seasonal demand, project expansion, or emergency needs.

- Sustainability Focus: Leased systems are often maintained and optimized to minimize water waste and energy consumption.

- Emerging Contaminant Management: Leasing allows quick deployment of specialized systems to remove PFAS and other hazardous substances.

- Operational Efficiency: Digital monitoring, predictive maintenance, and optimized workflows ensure reliable and efficient operations.

Market Analysis: Recent Developments in Water Treatment System Leasing

The water treatment system leasing market has experienced rapid developments through strategic expansions, technology deployment, and mobile treatment solutions. In August 2025, RSE, a Scottish clean water technology company, expanded into North America by opening a new office in Milwaukee, Wisconsin, targeting modular biological and nature-based treatment systems, including leasing of Moving Bed Biofilm Reactors. In July 2025, Veolia launched one of the largest PFAS treatment plants in Delaware, U.S., highlighting the increasing need for leased, on-demand systems to address emerging contaminants.

Earlier, in March 2024, Veolia expanded its mobile water services in Malaysia, deploying three new assets for temporary and emergency industrial applications. GE Vernova in February 2024 reaffirmed its commitment to service packages for water treatment systems, emphasizing equipment protection and reliability. In June 2023, Veolia added trailer-mounted reverse osmosis (RO) systems in China to meet growing industrial demand, while in May 2023, Evoqua Water Technologies acquired a Texas-based industrial water service business to strengthen its regional leasing and mobile service capabilities.

Additionally, in January 2023, Veolia commissioned the Al Dur 1 Independent Water and Power Project in Bahrain, producing 218,000 cubic meters per day. This project exemplifies long-term O&M contracts that incorporate flexible leasing components, highlighting the market’s focus on reliability, rapid deployment, and scalable water treatment solutions.

Key Trends Driving Water Treatment System Leasing

Shift from Capital Expenditure (CapEx) to Operational Expenditure (OpEx)

The water treatment system leasing market is increasingly driven by the financial advantages of converting large upfront investments into predictable, manageable operational expenses. Veolia Water Technologies’ Water-as-a-Service (WaaS) programs exemplify this shift, offering pay-for-volume solutions that relieve companies and municipalities from the burden of ownership, operation, and maintenance. A Public-Private Partnership in Alice, Texas, enabled the city to bypass a $12 million capital expenditure, demonstrating the financial flexibility and attractiveness of the OpEx model. This trend reflects a growing preference for leasing as a strategic alternative to traditional purchase models.

Rapid Deployment and Operational Flexibility

Leased water treatment systems are prized for their modularity and rapid deployment, enabling businesses and municipalities to address short-term or evolving water treatment needs without lengthy procurement processes. For example, a U.S. residential development used a leased wastewater treatment plant to maintain uninterrupted service during phased construction, circumventing municipal utility limitations. Industries with seasonal production cycles or fluctuating demand, such as food and beverage, benefit from the ability to scale capacity up or down, avoiding underutilization or oversized infrastructure costs.

Access to Advanced Technology and Risk Mitigation

Leasing provides immediate access to state-of-the-art water treatment technologies, including energy-efficient membranes, advanced filtration, and smart monitoring systems. Companies like NuWater offer mobile water treatment fleets with warranties and technical support similar to purchased systems, allowing clients to trial technology before committing to ownership. Academic research highlights the integration of AI and IoT in water quality monitoring, enabling predictive maintenance, real-time data insights, and optimized performance capabilities often unattainable with older, owned equipment.

Strategic Opportunities in Water Treatment System Leasing

The market offers significant opportunities in providing customized, technology-driven, and flexible leasing solutions. Leasing addresses financial constraints, ensures regulatory compliance, and reduces operational risk while delivering cutting-edge treatment capabilities. Industrial, commercial, and residential clients increasingly recognize leasing as a strategic tool to preserve capital, improve operational efficiency, and access advanced water technologies without long-term commitment, opening avenues for long-term contracts and service expansion.

Market Share Insights of Water Treatment System Leasing Market

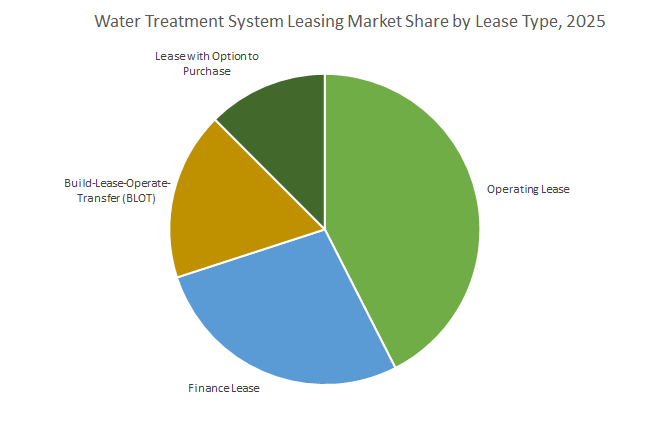

Market Share by Lease Type: Operating Leases Lead Due to Flexibility

Operating Leases (44.1%) dominate, offering short-term, flexible agreements treated as off-balance-sheet OpEx. Finance Leases (26.9%) are suited for long-term ownership intentions, functioning like loans. Build-Lease-Operate-Transfer (BLOT, 16.9%) is ideal for large-scale projects where the lessor assumes design, construction, and operation risk before transferring ownership. Lease with Option to Purchase (11.8%) allows clients to trial systems before committing, minimizing risk. This segmentation underscores the market’s emphasis on financial flexibility, risk management, and scalable solutions.

Market Share by System Type: Membrane Systems and Package Plants Dominate

Membrane Systems (26.9%), including RO, UF, and NF, are high-capex drivers ideal for leasing to avoid large upfront costs. Package/Containerized Plants (22.5%) provide modular solutions for temporary or decentralized applications, while Filtration Systems (16.9%) cater to point-of-entry or industrial pre-treatment needs. Wastewater & Recycling Systems (12.6%) address onsite treatment and reuse, reflecting increasing regulatory and sustainability demands. Smaller segments like POE/Whole-House, Softening Systems, Disinfection Systems, and POU Systems highlight emerging residential and commercial leasing adoption. The distribution emphasizes the preference for high-capex, flexible, and rapidly deployable systems.

Market Share by End-User: Industrial Segment Dominates

The Industrial segment (54.2%) leads due to the need for process water and wastewater treatment systems without heavy capital investment. Commercial end-users (32.8%), including offices, hotels, hospitals, and restaurants, prefer leasing for operational ease and maintenance coverage. Residential clients (16.9%) are increasingly adopting leased solutions for whole-house softening, filtration, and POU systems, particularly in rental or multi-tenant properties. This segmentation reflects the strategic importance of leasing for capital preservation, operational efficiency, and access to advanced water treatment technologies across industries.

United States: Leasing Models Gain Momentum Amid PFAS Regulations and Infrastructure Funding

The United States water treatment system leasing market is witnessing rapid growth, driven by regulatory compliance, capital efficiency, and advanced technologies. The U.S. Environmental Protection Agency (EPA) is actively encouraging municipalities and industries to adopt alternative delivery models that minimize upfront capital expenditure. The Bipartisan Infrastructure Law (BIL) allocates over $50 billion to water infrastructure, much of which supports leasing and service-based contracts. Additionally, the USDA’s Rural Energy for America Program (REAP) is incentivizing farm-based anaerobic digester projects, often structured as leasing agreements.

Regulatory pressure is intensifying with the EPA finalizing new Maximum Contaminant Levels (MCLs) for PFAS, forcing municipalities and industries to adopt costly treatment technologies. Leasing becomes an attractive option as communities increasingly turn to plug-and-play PFAS removal cartridge systems, available on rental contracts. With rising demand from urban utilities, industrial facilities, and residential applications, the U.S. remains a central hub for water treatment system leasing growth.

China: Government-Led Water Governance Driving Leasing Adoption

China is one of the fastest-growing markets for water treatment system leasing, fueled by strong government initiatives and strict regulations. The “Water Ten Plan” and Dual Carbon goals embed water governance into national sustainability strategy, ensuring long-term demand for leased systems. Significant government investments in pollution control and industrial wastewater treatment are creating strong incentives for leasing high-cost technologies.

The country is enforcing strict regulations on pollutant discharge, particularly for industrial facilities, pushing adoption of advanced membrane bioreactors (MBRs), reverse osmosis (RO), and smart water management (SWM) solutions. These high-cost systems are often acquired under leasing or service-based contracts to reduce capital strain. With increasing demand for industrial wastewater recycling, reclaimed water in urban centers, and decentralized solutions for rural communities, China is becoming a global leader in AI- and IoT-powered water treatment leasing models.

India: Government Missions and PPP Models Driving Leasing Growth

The Indian water treatment system leasing market is expanding rapidly under government-backed initiatives and infrastructure investments. The “Jal Jeevan Mission” is driving large-scale adoption of treatment systems to provide tap water to all rural households, leveraging IoT-enabled monitoring solutions that support leasing-based delivery. The “Swachh Bharat Mission-Urban (SBM-U) 2.0” is creating strong demand for leased wastewater systems to ensure zero untreated discharge in urban areas.

Corporate players like Enviro Infra Engineers Limited are capitalizing on the trend, with large EPC projects that include operation and maintenance (O&M) contracts, creating annuity-style revenues typical of leasing markets. With strong demand for river rejuvenation, wastewater reuse, and rural drinking water solutions, India is positioning itself as a hotspot for service-based and leasing water treatment contracts.

Germany: Digital Transformation and Leasing Models for Advanced Treatment Systems

Germany is a mature but evolving market for water treatment system leasing, particularly due to the revised EU Urban Wastewater Treatment Directive (2025). The directive mandates a 4th purification stage to remove micropollutants, requiring municipalities and industries to deploy advanced treatment technologies. Leasing becomes an attractive solution given the high costs of compliance.

Technological innovation is a key driver. The German Federal Environment Agency (UBA) emphasizes the integration of digital twins, AI-based monitoring, and climate adaptation strategies, often offered as part of leasing agreements. Corporate initiatives, led by the German Water Partnership’s “WATER 4.0” program, are accelerating the adoption of IoT-enabled and flexible water treatment leasing models. With stricter EU standards and climate resilience goals, Germany is a benchmark market for advanced water treatment leasing systems.

Singapore: Innovation-Driven Leasing for a Water-Scarce Nation

Singapore is a pioneer in innovative water treatment leasing solutions, focusing on recycling, reuse, and decentralized treatment systems. In January 2024, Hydroleap launched its Advanced Electrochemical Treatment (AET) technology, which delivers chemical-free wastewater treatment and reduces operational hours by up to 95%. Such systems are highly suitable for leasing due to their low-maintenance, efficiency-driven models.

Corporate initiatives strengthen Singapore’s position as a regional hub. CleanEdge Water Pte Ltd., in collaboration with IDE Technologies, is developing large-scale industrial wastewater projects across Asia, showcasing Singapore’s role in service-based water treatment exports. With its strong emphasis on water security, reuse, and efficient O&M contracts, Singapore’s leasing market is expected to expand further across both municipal and industrial sectors.

Australia: Long-Term Investments and Digital Leasing Solutions

Australia is increasingly turning to water treatment leasing models to address infrastructure modernization and climate resilience. In July 2025, Sydney Water announced a $34 billion investment plan over the next decade to renew assets and deploy smart monitoring solutions, many under service and leasing contracts.

Corporate innovators like Aqua Analytics are leading the way with Digital Twin technologies for water utilities, helping reduce non-revenue water and optimize decision-making under contract-based service models. With the dual challenges of aging infrastructure and climate variability, Australia is emerging as a key growth market for digital, contract-based, and leasing-driven water treatment solutions.

Competitive Landscape of Water Treatment System Leasing Market

The water treatment system leasing market is highly competitive, with leading players offering flexible, CAPEX-free solutions for industrial and commercial clients. Companies differentiate themselves through mobile fleets, digital integration, expertise in emerging contaminants, and sustainable operational models.

Veolia Water Technologies offers a global fleet of mobile water treatment systems

Veolia operates one of the largest fleets of mobile and leased water treatment systems, covering RO, ultrafiltration, demineralization, and disinfection technologies. Its InSight asset performance management platform ensures high operational efficiency and reliability. Strategic expansions include the March 2024 deployment in Malaysia and the June 2023 fleet expansion in China, reflecting its focus on responsive, on-demand solutions in key industrial markets.

Xylem Inc. provides integrated and digitally-enabled rental solutions

Xylem offers a diverse range of water and wastewater systems for rent, including dewatering pumps and biological treatment units. Its Xylem Vue digital platform allows remote monitoring and data-driven operational optimization, providing value-added services for rental customers. Xylem’s global footprint spans over 150 countries, supported by its extensive IP portfolio of 8,300+ patents and trademarks, ensuring technology leadership in the leasing segment.

Evoqua Water Technologies delivers mobile water systems and PFAS solutions

Evoqua, now part of Xylem, specializes in mobile water treatment and emerging contaminants management, including PFAS removal. Its flexible leasing model allows industrial clients to rapidly access mobile treatment solutions. The company’s high value-add, service-based business model supports steady revenue growth while addressing urgent environmental challenges through innovation and agile deployment of mobile assets.

SUEZ S.A. focuses on custom-made leased water treatment units

SUEZ provides a broad range of mobile water treatment leasing services, including reverse osmosis and ion exchange units for temporary or emergency needs. Its expertise in pre-treatment, energy recovery, and process optimization ensures leased units operate efficiently. SUEZ’s solutions help industrial clients diversify water resources, maintain production continuity, and respond to operational disruptions effectively.

Pall Corporation offers fast, CAPEX-free rental solutions for industrial fluids

Pall, a Danaher subsidiary, specializes in filtration, separation, and purification rentals. Its fleet includes high-flow particulate filtration skids and coalescer filter skids, deployed for mission-critical, emergency, or short-term needs. Pall’s leasing model allows customers to test technology, resolve contamination issues, and enhance product quality without heavy upfront investments.

Water Treatment System Leasing Market Report Scope

Water Treatment System Leasing Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.6 Billion

|

|

Market Size (2034)

|

$14.1 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Lease Type (Operating Lease, Finance Lease, Build-Lease-Operate-Transfer (BLOT), Lease with Option to Purchase), By System Type (Point-of-Use (POU) Systems, Point-of-Entry (POE) / Whole-House Systems, Membrane Systems, Filtration Systems, Disinfection Systems, Softening & Conditioning Systems, Package Plants / Containerized Systems, Wastewater & Recycling Systems), By End-User (Residential, Commercial, Industrial), By Application (Drinking Water Purification, Process Water Treatment, Wastewater Treatment, Water Reuse & Recycling), By Lease Term (Short-Term Lease, Medium-Term Lease, Long-Term Lease)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Veolia, SUEZ, Xylem Inc., Evoqua Water Technologies, DuPont de Nemours, Inc., Aquatech International, Kubota Corporation, Siemens, Pentair plc, Kurita Water Industries Ltd., H2O GmbH, Thermax Limited, Ecolab, Lenntech, Abengoa

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Treatment System Leasing Market Segmentation

By Lease Type

- Operating Lease

- Finance Lease

- Build-Lease-Operate-Transfer (BLOT)

- Lease with Option to Purchase

By System Type

- Point-of-Use (POU) Systems

- Point-of-Entry (POE) / Whole-House Systems

- Membrane Systems (RO, UF, NF)

- Filtration Systems (Media, Carbon, Sediment)

- Disinfection Systems (UV, Ozone, Chlorination)

- Softening & Conditioning Systems

- Package Plants / Containerized Systems

- Wastewater & Recycling Systems

By End-User

- Residential

- Commercial

- Office Buildings

- Hotels & Restaurants

- Hospitals & Healthcare

- Educational Institutions

- Industrial

- Manufacturing

- Food & Beverage

- Pharmaceuticals

- Power & Energy

- Mining

By Application

- Drinking Water Purification

- Process Water Treatment

- Wastewater Treatment

- Water Reuse & Recycling

By Lease Term

- Short-Term Lease (< 2 years)

- Medium-Term Lease (2-5 years)

- Long-Term Lease (> 5 years)

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Water Treatment System Leasing Industry include-

- Veolia

- SUEZ

- Xylem Inc.

- Evoqua Water Technologies

- DuPont de Nemours, Inc.

- Aquatech International

- Kubota Corporation

- Siemens

- Pentair plc

- Kurita Water Industries Ltd.

- H2O GmbH

- Thermax Limited

- Ecolab

- Lenntech

- Abengoa

*- List not Exhaustive

Research Coverage

The Water Treatment System Leasing Market Report by USDAnalytics investigates how CapEx-free access, rapid deployment, and PFAS-ready solutions are redefining procurement, operations, and compliance for industrial, commercial, and residential users. This study highlights breakthroughs in modular/mobile fleets, AI-enabled monitoring, and Water-as-a-Service models; delivers analysis reviews on risk allocation, uptime-linked SLAs, and digital performance management; and highlights the role of leasing in accelerating sustainability outcomes and regulatory responsiveness. By connecting financial engineering with technology adoption curves, this report is an essential resource for CFOs, operations leaders, facility managers, and policymakers seeking flexible capacity, predictable OpEx, and faster time-to-compliance without long procurement cycles. Scope Includes-

- Segmentation:

- By Lease Type: Operating Lease; Finance Lease; Build-Lease-Operate-Transfer (BLOT); Lease with Option to Purchase

- By System Type: Point-of-Use (POU); Point-of-Entry/Whole-House; Membrane Systems (RO, UF, NF); Filtration (Media, Carbon, Sediment); Disinfection (UV, Ozone, Chlorination); Softening & Conditioning; Package/Containerized Plants; Wastewater & Recycling Systems

- By End-User: Residential; Commercial (Office Buildings, Hotels & Restaurants, Hospitals & Healthcare, Educational Institutions); Industrial (Manufacturing, Food & Beverage, Pharmaceuticals, Power & Energy, Mining)

- By Application: Drinking Water Purification; Process Water; Wastewater Treatment; Water Reuse & Recycling

- By Lease Term: Short-Term (<2 years); Medium-Term (2–5 years); Long-Term (>5 years)

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Veolia; SUEZ; Xylem Inc.; Evoqua Water Technologies; DuPont de Nemours, Inc.; Aquatech International; Kubota Corporation; Siemens; Pentair plc; Kurita Water Industries Ltd.; H2O GmbH; Thermax Limited; Ecolab; Lenntech; Abengoa

Methodology

USDAnalytics uses a mixed-methods approach that blends executive interviews and buyer surveys with secondary validation from regulatory dockets, municipal tenders, financial filings, and technical literature. We construct bottom-up lease fleet and installed-base models by system type and term, reconcile them with top-down spend indicators, and triangulate using disclosed rental utilization, backlog, and service attach rates. Forecasts (2025–2034) incorporate PFAS/MCL timelines, OpEx adoption curves, mobile-fleet growth, energy cost scenarios, and replacement cycles. Competitive mapping applies feature benchmarking (membranes, disinfection, digital/IoT), SLA structures, and total cost of water (TCoW) analytics to deliver decision-grade insights.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Treatment System Leasing Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Water Treatment System Leasing Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $7.6 Billion

2.2.2. Forecasted Market Size (2034): $14.1 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 7.1%

2.3. Market Drivers and Challenges

2.3.1. Drivers: CapEx-Avoidance, Flexibility, and Regulatory Pressure

2.3.2. Challenges: Competition from Traditional Purchase Models and Lack of Awareness

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Shift from Capital Expenditure (CapEx) to Operational Expenditure (OpEx)

3.2. Rapid Deployment and Operational Flexibility

3.3. Access to Advanced Technology and Risk Mitigation

3.4. Recent Developments & Strategic Moves (2023–2025)

3.4.1. Strategic Expansions and Acquisitions

3.4.2. Technology Deployment and New Service Launches

4. Water Treatment System Leasing Market – Segmentation Insights

4.1. By Lease Type

4.1.1. Operating Lease (44.1% Market Share)

4.1.2. Finance Lease (26.9% Market Share)

4.1.3. Build-Lease-Operate-Transfer (BLOT) (16.9% Market Share)

4.1.4. Lease with Option to Purchase (11.8% Market Share)

4.2. By System Type

4.2.1. Membrane Systems (RO, UF, NF) (26.9% Market Share)

4.2.2. Package/Containerized Plants (22.5% Market Share)

4.2.3. Filtration Systems (16.9% Market Share)

4.2.4. Wastewater & Recycling Systems (12.6% Market Share)

4.2.5. Point-of-Entry (POE)/Whole-House Systems

4.2.6. Point-of-Use (POU) Systems

4.2.7. Disinfection Systems

4.2.8. Softening & Conditioning Systems

4.3. By End-User

4.3.1. Industrial (54.2% Market Share)

4.3.2. Commercial (32.8% Market Share)

4.3.3. Residential (16.9% Market Share)

4.4. By Application

4.4.1. Drinking Water Purification

4.4.2. Process Water Treatment

4.4.3. Wastewater Treatment

4.4.4. Water Reuse & Recycling

4.5. By Lease Term

4.5.1. Short-Term Lease (< 2 years)

4.5.2. Medium-Term Lease (2–5 years)

4.5.3. Long-Term Lease (> 5 years)

5. Country Analysis and Outlook: Water Treatment System Leasing Market

5.1. United States: PFAS Regulations and Infrastructure Funding

5.2. China: Government-Led Water Governance

5.3. India: Government Missions and PPP Models

5.4. Germany: Digital Transformation for Advanced Treatment

5.5. Singapore: Innovation-Driven Leasing Solutions

5.6. Australia: Long-Term Investments and Digital Solutions

6. Market Size Outlook by Region (2025-2034)

6.1. North America Water Treatment System Leasing Market Size Outlook to 2034

6.1.1. By Lease Type

6.1.2. By System Type

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe Water Treatment System Leasing Market Size Outlook to 2034

6.2.1. By Lease Type

6.2.2. By System Type

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Water Treatment System Leasing Market Size Outlook to 2034

6.3.1. By Lease Type

6.3.2. By System Type

6.3.3. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Water Treatment System Leasing Market Size Outlook to 2034

6.4.1. By Lease Type

6.4.2. By System Type

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Water Treatment System Leasing Market Size Outlook to 2034

6.5.1. By Lease Type

6.5.2. By System Type

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Company Profiles: Leading Players

7.1. Veolia Water Technologies

7.1.1. Company Overview

7.1.2. Global Fleet of Mobile Systems

7.2. Xylem Inc.

7.2.1. Company Overview

7.2.2. Integrated and Digitally-Enabled Solutions

7.3. Evoqua Water Technologies (A Xylem Brand)

7.4. SUEZ S.A.

7.5. Pall Corporation

7.6. Other Key Players

7.6.1. DuPont de Nemours, Inc.

7.6.2. Aquatech International

7.6.3. Kubota Corporation

7.6.4. Kurita Water Industries Ltd.

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures