Global IoT in Water Treatment Systems Market Overview

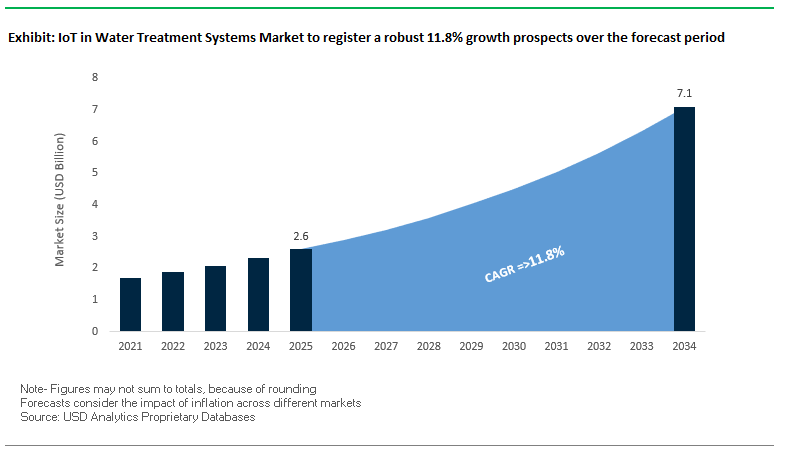

The global IoT in water treatment systems market is expected to grow from $2.6 billion in 2025 to $7.1 billion by 2034, registering a robust CAGR of 11.8%. The market is driven by the increasing integration of IoT technology across industrial and municipal water treatment systems, which enhances operational efficiency, enables real-time water quality monitoring, and supports predictive maintenance strategies. Utilities and industrial operators are leveraging IoT solutions to optimize chemical dosing, reduce energy consumption, and ensure the safety and reliability of water supply networks.

IoT-enabled systems are particularly critical in addressing water scarcity, resource optimization, and sustainability goals. By combining AI, cloud platforms, and sensor networks, water operators can detect contaminants, forecast equipment failures, and optimize water reuse processes, aligning with circular economy principles. This digital transformation is also catalyzed by emerging contaminants like PFAS, requiring rapid, technology-driven interventions.

Key Insights for Industry Stakeholders:

- Enhanced Operational Efficiency: IoT optimizes filtration, chemical dosing, and overall plant operations.

- Proactive Maintenance: Predictive maintenance reduces downtime and emergency repair costs.

- Real-Time Contaminant Detection: Continuous monitoring ensures water safety and regulatory compliance.

- Increased Water Reuse: IoT supports wastewater recycling and circular water economy models.

- Decarbonization & Energy Optimization: AI and digital platforms contribute to energy savings and reduced carbon footprint.

Market Analysis: Recent Developments in IoT in Water Treatment Systems

The IoT in water treatment systems market has seen significant collaborations, acquisitions, and technology deployments to enhance operational efficiency and digital capabilities. In August 2025, RSE and Siemens signed a Memorandum of Understanding to integrate Siemens’ AI and automation technologies into RSE’s modular water treatment systems, targeting accelerated decarbonization and optimized operations. In July 2025, Veolia launched one of the largest PFAS treatment plants in Delaware, U.S., demonstrating the industry’s proactive response to emerging contaminants using advanced IoT-enabled solutions.

In May 2025, Diehl Metering acquired PREVENTIO GmbH, a startup specializing in leakage management and predictive maintenance, to strengthen real-time leak detection capabilities. Siemens and KETOS entered a strategic partnership in March 2025 to enhance industrial and municipal water quality management via AI-driven analytics and IoT-enabled platforms. In February 2025, Veolia partnered with Mistral AI to develop the Veolia Secure GPT, integrating generative AI to optimize resource management and operational efficiency.

Strategic acquisitions have also bolstered the market’s digital focus. Xylem Inc. acquired Idrica in December 2024, enhancing data analytics and digital utility management. In August 2024, ABB unveiled next-generation electromagnetic flowmeters with modular IoT connectivity, while Schneider Electric secured a January 2024 contract to automate India’s largest water treatment plant in Mumbai, leveraging EcoStruxure solutions to improve operational efficiency for 22 million residents.

Key Trends Driving the IoT Water Treatment Market

Government Initiatives Driving Smart Water Infrastructure

The IoT in water treatment systems market is strongly influenced by government-led initiatives promoting smart water infrastructure. India’s Jal Jeevan Mission exemplifies a national-level program deploying IoT sensors for real-time monitoring of water supply, including flow meters and chlorine analyzers. These systems allow officials to monitor water quantity, quality, and pressure, enabling timely leak detection and corrective action. Academic studies, such as the 2024 MDPI Water review, emphasize that regulatory bodies like India’s CPCB are accelerating the adoption of IoT systems to ensure compliance with stricter discharge standards. Such initiatives highlight the growing role of smart water management technologies in improving rural and urban water security.

AI and Machine Learning Integration for Predictive Analytics

The integration of AI and machine learning with IoT is transforming water treatment operations. Research from 2025 demonstrates that AI algorithms can analyze large-scale sensor data to optimize distribution, detect leaks, and predict equipment failures in real-time. Utilities leveraging this technology can transition from reactive maintenance to proactive asset management. Studies indicate that AI-enabled IoT can reduce non-revenue water (NRW) by 20–50%, preventing millions of gallons of water loss annually. This trend underscores the strategic importance of predictive analytics and intelligent water treatment systems for operational efficiency and revenue protection.

Corporate and Industrial Adoption for Efficiency and Resource Recovery

Industrial adoption of IoT in water treatment is driven by efficiency and sustainability goals. A 2021 case study from an Indian beverage plant showed that real-time monitoring identified overconsumption hotspots, enabling projects that reduced water usage by 11% daily. IoT facilitates the circular economy by enabling safe reuse of treated water in processes such as cooling and sanitation. This demonstrates that IoT systems not only enhance operational efficiency but also support sustainability initiatives and corporate water stewardship.

Strategic Opportunities in IoT Water Treatment Systems

The market presents significant opportunities in hardware, software, and services for predictive water management, leak detection, and resource optimization. Utilities and industries increasingly demand end-to-end IoT solutions, combining sensors, AI analytics, cloud platforms, and digital twins. Providers offering integration, consulting, and managed services can capture high-margin opportunities by enabling intelligent operations, energy optimization, and compliance monitoring, positioning IoT as a key enabler of resilient, data-driven water infrastructure.

Market Share Analysis of IoT in Water Treatment Systems Market

Market Share by Component: Hardware Dominates, Software Growth Accelerates

The Hardware segment (54.2%) dominates, comprising sensors, smart meters, actuators, gateways, and communication modules the physical foundation digitizing water systems. Software (32.8%), including IoT analytics, AI/ML platforms, dashboards, and asset management suites, represents the fastest-growing segment, converting raw sensor data into actionable insights for predictive maintenance and process optimization. Services (16.9%), encompassing system integration, consulting, and managed services, are essential for successful deployment, particularly for complex industrial and municipal water systems.

Market Share by Application: Asset Management and Leakage Detection Lead Adoption

Asset Management & Predictive Maintenance (22.5%) is the largest application, protecting high-value equipment like pumps and motors and minimizing downtime. Leakage Detection & Management (20.9%) is critical for reducing non-revenue water through real-time pressure and flow monitoring. Water Quality Monitoring ensures regulatory compliance and public health by continuously tracking pH, turbidity, chlorine, and TOC levels. Remote Operation & Control (13.2%), Chemical Dosing Management, and Energy Management deliver operational savings, while Sludge Management and Customer Engagement & Billing provide additional optimization and transparency. This segmentation highlights IoT’s role in enhancing efficiency, sustainability, and regulatory compliance.

Market Share by Technology: Connectivity and AI Power IoT Water Systems

Connectivity (35.7%) is the largest segment, enabling communication via LPWAN, Cellular (4G/5G), and Wi-Fi networks. Cloud Platforms (26.9%) provide scalable data storage, computation, and hosting for analytics applications. AI & Machine Learning (22.5%) offer anomaly detection, predictive analytics, and operational optimization, while Digital Twins (11.8%) create virtual models for simulation and forecasting. Together, these technologies form a fully integrated IoT ecosystem, allowing utilities to transition from reactive monitoring to intelligent water management.

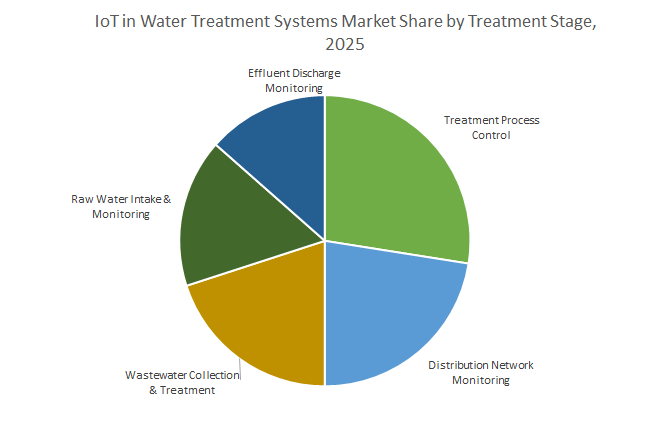

IoT in Water Treatment Systems Market Share by Treatment Stage, 2025

United States: Infrastructure Modernization Driving IoT Water Treatment Adoption

The United States IoT in water treatment systems market is witnessing rapid expansion, primarily fueled by large-scale government initiatives and stringent regulatory compliance requirements. The U.S. Environmental Protection Agency (EPA) is leveraging the Bipartisan Infrastructure Law (BIL), which allocates more than $50 billion toward drinking water, wastewater, and stormwater infrastructure. This funding strongly supports the integration of IoT-enabled sensors, real-time monitoring solutions, and AI-driven water analytics to reduce non-revenue water loss and ensure water safety.

The EPA’s finalization of Maximum Contaminant Levels (MCLs) for PFAS contaminants is another crucial driver, as utilities now require continuous IoT monitoring systems to remain compliant. On the corporate front, Badger Meter’s acquisition of Trimble’s remote water monitoring hardware and software in 2024 highlights the consolidation of IoT solutions across real-time telemetry, smart metering, and predictive analytics. Supported by EPA Section 106 grants and R&D initiatives such as those from the Water Research Foundation (WRF), the U.S. market is firmly positioned for leadership in smart and sustainable water management.

China: IoT-Driven Smart Water Management Under Government Megaprojects

The China IoT in water treatment systems market is experiencing robust growth, driven by national programs like the “Water Ten Plan”, the “Sponge City” initiative, and the 14th Five-Year Plan, which collectively integrate IoT and AI into water governance. By 2025, rural China’s centralized water supply rate and tap water penetration rate are projected to reach nearly 90%, showcasing the country’s commitment to modernizing its water infrastructure.

China’s financial ecosystem is also aligned with sustainability, as institutions such as the Bank of China are introducing “Water-saving Loans” to fund projects integrating IoT-enabled smart water management. Corporates like Siemens China and Huawei are spearheading technological innovations, offering IoT-enabled water quality monitoring and AI-based pollutant detection platforms. The primary market drivers include managing urban flooding, optimizing industrial wastewater reuse, and addressing agricultural runoff all reliant on real-time IoT monitoring solutions.

India: IoT Transforming Rural and Urban Water Governance

India represents one of the fastest-growing markets for IoT in water treatment systems, with the Jal Jeevan Mission deploying sensor-based IoT devices across six lakh villages to ensure reliable rural drinking water supply. The National Hydrology Project (NHP) has already installed thousands of real-time data acquisition systems (RTDAS) to enhance surface and groundwater monitoring efficiency.

On the urban front, the Swachh Bharat Mission–Urban (SBM-U 2.0) emphasizes zero untreated wastewater discharge, fueling the adoption of IoT for wastewater management. Private collaborations are accelerating this growth, such as Pani Energy’s 2024 partnership with Murugappa Water Technology & Solutions, which integrates AI-powered IoT platforms for smarter treatment facilities. With the dual mandate of river rejuvenation and industrial effluent monitoring, India is rapidly emerging as a leader in IoT-enabled water quality and wastewater monitoring.

Germany: EU Directives Driving IoT-Enabled Wastewater Innovation

The Germany IoT in water treatment market is strongly shaped by regulatory and technological forces. The revised EU Urban Wastewater Treatment Directive (2025) mandates a “4th purification stage” to eliminate micropollutants, pushing utilities toward IoT-based treatment technologies for compliance.

Germany is also a pioneer in digital water transformation. The Federal Environment Agency (UBA) reports growing adoption of digital twins, AI-powered predictive maintenance, and IoT platforms to optimize climate-resilient water management. Research organizations such as Fraunhofer IGB are developing advanced digital infrastructures for seamless integration of sensor data and smart process automation. The market is thus anchored in a regulatory-driven demand for compliance and a technological push toward digital water intelligence.

Singapore: Smart PUB Roadmap Leading Global IoT Deployment

Singapore stands as a global benchmark in IoT-enabled water management, with the PUB’s Smart Water Meter Programme at the forefront. This initiative will install smart meters across residential, commercial, and industrial sectors, with an investment of SGD $120 million to cover deployment and long-term IoT-enabled maintenance.

PUB is also collaborating with Itron and SP Group to connect nearly 300,000 meters to IoT networks, achieving significant water conservation efficiencies. Additionally, Singapore is a hub for cutting-edge treatment innovations, such as Hydroleap’s Advanced Electrochemical Treatment (AET) technology, which delivers chemical-free wastewater treatment while reducing operational man-hours by up to 95%. With its strong emphasis on reducing non-revenue water and achieving long-term water security in a scarcity-driven environment, Singapore continues to lead the global market in IoT water treatment integration.

Japan: IoT Addressing Workforce Challenges and Disaster Resilience

The Japan IoT in water treatment systems market is rapidly evolving, focusing on aging infrastructure, workforce shortages, and disaster resilience. In 2025, research highlighted the deployment of IoT sensors and wireless systems to monitor real-time turbidity levels, enabling early pollution detection. Hitachi’s Sense–Think–Act digital framework and Kubota’s IoT-enabled remote management solutions are addressing structural inefficiencies by enabling predictive maintenance and reducing dependency on physical workforce presence.

With frequent natural disasters such as earthquakes and floods, IoT is increasingly being integrated into disaster-prepared water infrastructure to ensure reliable supply and treatment. As Japan navigates demographic and environmental challenges, IoT plays a central role in safeguarding water quality, optimizing resource efficiency, and maintaining resilience.

Competitive Landscape of IoT in Water Treatment Systems Market

The IoT in water treatment systems market is highly competitive, with key players focusing on digital integration, predictive analytics, IoT-enabled monitoring, and smart water solutions to deliver efficient and sustainable water management. Companies differentiate themselves by providing scalable IoT platforms, AI-driven analytics, and real-time monitoring solutions that improve operational efficiency and regulatory compliance.

Xylem Inc. drives digital water solutions with IoT-enabled platforms

Xylem offers a comprehensive ecosystem of smart water technologies integrated with IoT and digital services. Its Xylem Vue platform provides data-driven decision support and network optimization, while the Sensus brand leads in smart meters and monitoring solutions. Strategic moves include the 2024 acquisition of Evoqua Water Technologies and Idrica in late 2024, strengthening Xylem’s digital portfolio and enabling IoT-enabled solutions across the water lifecycle.

SUEZ S.A. enhances water network management with AI and IoT

SUEZ leverages its AQUADVANCED® digital suite to monitor water networks in real time, manage pressure, and simulate events, supported by AI-driven analytics like the IAcoustique algorithm for leak detection. With over 7 million smart meters deployed globally, SUEZ integrates IoT technology to deliver predictive, data-driven solutions, demonstrated in ongoing projects in Cannes, France, and other regions.

Veolia Environnement S.A. integrates generative AI for smarter water management

Veolia combines its environmental expertise with Hubgrade, an AI-enabled platform for centralized control of water and energy infrastructure. The February 2025 partnership with Mistral AI highlights the integration of generative AI to optimize operations. Expansions in March 2024 and June 2023 in Malaysia and China, respectively, showcase Veolia’s mobile IoT-enabled assets for flexible water treatment across industrial applications.

Schneider Electric SE digitizes large-scale water treatment plants

Schneider Electric uses its EcoStruxure platform to deliver IoT-enabled automation for water and wastewater plants, focusing on efficiency and sustainability. Its January 2024 contract to automate Mumbai’s largest water treatment facility demonstrates the platform’s capabilities, helping achieve up to 30% energy savings and supporting decarbonization targets.

Siemens AG drives modular IoT water solutions and decarbonization

Siemens integrates AI, automation, and IoT through the Siemens Xcelerator platform, offering process automation, predictive maintenance, and smart grid solutions. Partnerships with RSE in August 2025 and KETOS in March 2025 highlight Siemens’ focus on decarbonization, resource efficiency, and real-time water intelligence for industrial and municipal clients.

IoT in Water Treatment Systems Market Report Scope

IoT in Water Treatment Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$7.1 Billion

|

|

Market Growth Rate

|

11.8%

|

|

Segments

|

By Component (Hardware, Software, Services), By Application (Water Quality Monitoring, Asset Management & Predictive Maintenance, Leakage Detection & Management, Energy Management & Optimization, Chemical Dosing Management, Remote Operation & Control, Sludge Management, Customer Engagement & Billing), By Technology (Connectivity, Cloud Platforms, Digital Twins, AI & Machine Learning), By End-User (Municipal Water & Wastewater Treatment, Industrial Treatment, Power Generation, Oil & Gas, Chemicals & Petrochemicals, Food & Beverage, Pharmaceuticals, Pulp & Paper, Commercial & Residential), By Treatment Stage (Raw Water Intake & Monitoring, Treatment Process Control, Distribution Network Monitoring, Wastewater Collection & Treatment, Effluent Discharge Monitoring)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Xylem Inc., Itron Inc., Siemens, ABB Ltd., Schneider Electric, Trimble Inc., SUEZ, Veolia, Kubota Corporation, Badger Meter, Bivocom, Hach (Danaher Corporation), Kurita Water Industries Ltd., EVOQUA Water Technologies, Hitachi, Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

IoT in Water Treatment Systems Market Segmentation

By Component

- Hardware

- Software

- Services

By Application

- Water Quality Monitoring

- Asset Management & Predictive Maintenance

- Leakage Detection & Management

- Energy Management & Optimization

- Chemical Dosing Management

- Remote Operation & Control

- Sludge Management

- Customer Engagement & Billing (Smart Metering)

By Technology

- Connectivity

- Cellular (4G/LTE, 5G, NB-IoT, LTE-M)

- LPWAN (LoRaWAN, Sigfox)

- Wi-Fi

- Radio Frequency (RF)

- Satellite

- Cloud Platforms

- Digital Twins

- AI & Machine Learning

By End-User

- Municipal Water & Wastewater Treatment

- Industrial Treatment

- Power Generation

- Oil & Gas

- Chemicals & Petrochemicals

- Food & Beverage

- Pharmaceuticals

- Pulp & Paper

- Commercial & Residential

By Treatment Stage

- Raw Water Intake & Monitoring

- Treatment Process Control

- Distribution Network Monitoring

- Wastewater Collection & Treatment

- Effluent Discharge Monitoring

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the IoT in Water Treatment Systems Industry include-

- Xylem Inc.

- Itron Inc.

- Siemens

- ABB Ltd.

- Schneider Electric

- Trimble Inc.

- SUEZ

- Veolia

- Kubota Corporation

- Badger Meter

- Bivocom

- Hach (Danaher Corporation)

- Kurita Water Industries Ltd.

- EVOQUA Water Technologies

- Hitachi, Ltd.

*- List not Exhaustive

Research Coverage

The IoT in Water Treatment Systems Market Report by USDAnalytics investigates how sensor-rich networks, cloud platforms, and AI algorithms are transforming plant control from reactive monitoring to predictive, closed-loop optimization; it highlights breakthroughs in real-time water quality analytics, digital twins, and energy-aware dosing; delivers analysis reviews on cybersecurity, PFAS-driven compliance, and ops-ex models; and maps adoption playbooks across municipal and industrial users. By translating data streams into measurable outcomes uptime, kWh/m³, chemical intensity, and reuse ratios this report is an essential resource for utility leaders, plant managers, and ESG strategists seeking to scale intelligent, low-carbon, and resilient water operations. Scope Includes-

- By Component: Hardware; Software; Services

- By Application: Water Quality Monitoring; Asset Management & Predictive Maintenance; Leakage Detection & Management; Energy Management & Optimization; Chemical Dosing Management; Remote Operation & Control; Sludge Management; Customer Engagement & Billing (Smart Metering)

- By Technology: Connectivity (Cellular 4G/LTE/5G/NB-IoT/LTE-M; LPWAN LoRaWAN/Sigfox; Wi-Fi; RF; Satellite); Cloud Platforms; Digital Twins; AI & Machine Learning

- By End-User: Municipal Water & Wastewater; Industrial; Power Generation; Oil & Gas; Chemicals & Petrochemicals; Food & Beverage; Pharmaceuticals; Pulp & Paper; Commercial & Residential

- By Treatment Stage: Raw Water Intake & Monitoring; Treatment Process Control; Distribution Network Monitoring; Wastewater Collection & Treatment; Effluent Discharge Monitoring

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): Xylem Inc.; Itron Inc.; Siemens; ABB Ltd.; Schneider Electric; Trimble Inc.; SUEZ; Veolia; Kubota Corporation; Badger Meter; Bivocom; Hach (Danaher Corporation); Kurita Water Industries Ltd.; Evoqua Water Technologies; Hitachi, Ltd.

Methodology

USDAnalytics applies a mixed-methods design: C-suite and plant-level interviews, integrator surveys, and site walk-throughs are combined with secondary validation from permits, tenders, technical standards, and vendor filings. We build bottom-up models of connected assets (sensors, gateways, controllers) and software seats by application, reconcile with top-down spend, and triangulate using rollout disclosures, SLA metrics, and utilization logs. Forecasts (2025–2034) incorporate regulatory timelines (e.g., PFAS/MCLs), battery and firmware lifecycles, network availability (LPWAN/5G), and energy price scenarios. Competitive benchmarking scores platforms on interoperability, cybersecurity posture, analytics depth, and total cost per monitored m³ to deliver decision-grade projections.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: IoT in Water Treatment Systems Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. IoT in Water Treatment Systems Market Overview (2025–2034)

2.1. Introduction

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $2.6 Billion

2.2.2. Forecasted Market Size (2034): $7.1 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 11.8%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Operational Efficiency, Real-Time Monitoring, and Predictive Maintenance

2.3.2. Challenges: Cybersecurity Risks and High Implementation Costs

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments

3.1. Government Initiatives Driving Smart Water Infrastructure

3.2. AI and Machine Learning Integration for Predictive Analytics

3.3. Corporate and Industrial Adoption for Efficiency and Resource Recovery

3.4. Recent Developments & Strategic Moves (2024–2025)

3.4.1. Strategic Partnerships and Acquisitions

3.4.2. New Product and Platform Launches

4. IoT in Water Treatment Systems Market – Segmentation Insights

4.1. By Component

4.1.1. Hardware (54.2% Market Share)

4.1.2. Software (32.8% Market Share)

4.1.3. Services (16.9% Market Share)

4.2. By Application

4.2.1. Asset Management & Predictive Maintenance (22.5% Market Share)

4.2.2. Leakage Detection & Management (20.9% Market Share)

4.2.3. Water Quality Monitoring

4.2.4. Remote Operation & Control (13.2% Market Share)

4.2.5. Chemical Dosing Management

4.2.6. Energy Management & Optimization

4.2.7. Sludge Management

4.2.8. Customer Engagement & Billing (Smart Metering)

4.3. By Technology

4.3.1. Connectivity (35.7% Market Share)

4.3.1.1. Cellular (4G/LTE, 5G, NB-IoT, LTE-M)

4.3.1.2. LPWAN (LoRaWAN, Sigfox)

4.3.1.3. Wi-Fi & Others

4.3.2. Cloud Platforms (26.9% Market Share)

4.3.3. AI & Machine Learning (22.5% Market Share)

4.3.4. Digital Twins (11.8% Market Share)

4.4. By End-User

4.4.1. Municipal Water & Wastewater Treatment

4.4.2. Industrial Treatment

4.4.3. Commercial & Residential

4.4.4. Other Industrial Sectors (Power Generation, Oil & Gas, etc.)

4.5. By Treatment Stage

4.5.1. Raw Water Intake & Monitoring

4.5.2. Treatment Process Control

4.5.3. Distribution Network Monitoring

4.5.4. Wastewater Collection & Treatment

4.5.5. Effluent Discharge Monitoring

5. Country Analysis and Outlook: IoT in Water Treatment Systems Market

5.1. United States: Infrastructure Modernization & Regulatory Compliance

5.2. China: Government Megaprojects & Smart Water Management

5.3. India: Rural & Urban Water Governance Transformation

5.4. Germany: EU Directives & Wastewater Innovation

5.5. Singapore: Smart PUB Roadmap & Global Leadership

5.6. Japan: Addressing Workforce Challenges & Disaster Resilience

6. IoT in Water Treatment System Market Size Outlook by Region (2025-2034)

6.1. North America IoT in Water Treatment Systems Market Size Outlook to 2034

6.1.1. By Component

6.1.2. By Application

6.1.3. By Country (US, Canada, Mexico)

6.2. Europe IoT in Water Treatment Systems Market Size Outlook to 2034

6.2.1. By Component

6.2.2. By Application

6.2.3. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific IoT in Water Treatment Systems Market Size Outlook to 2034

6.3.1. By Component

6.3.2. By Application

6.3.3. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America IoT in Water Treatment Systems Market Size Outlook to 2034

6.4.1. By Component

6.4.2. By Application

6.4.3. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa IoT in Water Treatment Systems Market Size Outlook to 2034

6.5.1. By Component

6.5.2. By Application

6.5.3. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Competitive Landscape: Key Companies

7.1. Xylem Inc.

7.1.1. Company Overview

7.1.2. Digital Water Solutions with IoT-Enabled Platforms

7.2. SUEZ S.A.

7.2.1. Company Overview

7.2.2. AI and IoT for Network Management

7.3. Veolia Environnement S.A.

7.4. Schneider Electric SE

7.5. Siemens AG

7.6. Other Prominent Companies

7.6.1. Itron Inc.

7.6.2. Kubota Corporation

7.6.3. Badger Meter

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures