Water Infrastructure Asset Management Market Overview

The global water infrastructure asset management market is projected to grow from $11.2 billion in 2025 to $23.1 billion by 2034, exhibiting a strong CAGR of 8.4%. This growth is driven by the urgent need to modernize aging water infrastructure, reduce non-revenue water, enhance climate resilience, and leverage digital technologies for operational efficiency. Utilities worldwide are adopting advanced solutions such as digital twins, IoT-based monitoring, and AI analytics to optimize water asset performance and maintenance strategies.

The market is also influenced by increasing investments in water infrastructure modernization and a focus on sustainability. For instance, digital twins allow utilities to simulate extreme weather events, pipeline failures, and demand fluctuations, helping to anticipate risks and maintain service continuity. Meanwhile, the deployment of IoT-connected devices over 20 million globally as of 2024 enables real-time monitoring, predictive maintenance, and rapid response to operational issues.

Key Insights for Industry Stakeholders:

- Aging infrastructure and modernization needs are driving demand for digital asset management solutions.

- Smart water solutions, such as digital twins and IoT monitoring, help reduce non-revenue water and operational costs.

- Climate change resilience is a major focus, with predictive tools allowing scenario planning for extreme events.

- Regulatory and privatization reforms in emerging markets are accelerating technology adoption.

- Real-time data collection enables utilities to optimize maintenance and resource allocation effectively.

Market Analysis: Recent Developments in Water Infrastructure Asset Management

The water infrastructure asset management market has witnessed notable developments in recent years. In August 2025, the European Investment Bank (EIB) signed a €250 million financing agreement with EYDAP, Athens Water Supply and Sewerage Company, to modernize water infrastructure using smart meters and digital systems. Simultaneously, New Zealand passed its “Local Water Done Well” reform legislation, impacting water asset management and privatization frameworks.

In May 2025, Argentina issued a decree to oversee privatization of its state-owned utility AySA, which is expected to introduce new asset management practices and attract private investment. The March 2025 World Bank report highlighted the slow adoption of digital solutions in the water sector, underscoring opportunities for technology providers offering AI, IoT, and digital twin-based management tools.

Infrastructure automation projects have also advanced, with Schneider Electric automating India’s largest water treatment plant in Mumbai (January 2024) using EcoStruxure solutions, enhancing operational efficiency for 22 million residents. Meanwhile, In-Situ Inc.’s acquisition of ChemScan (November 2023) strengthened real-time monitoring capabilities for drinking water and wastewater. Partnerships and platform deployments such as SUEZ and SAMP (October 2023) and SUEZ’s Smart Water Grid Analytics Platform for PUB, Singapore (June 2023) illustrate the growing integration of predictive digital tools for proactive infrastructure management.

Key Trends Driving Adoption of Advanced Water Infrastructure Management

Digital Transformation Enables Predictive Asset Management

The water infrastructure asset management market is increasingly driven by the adoption of AI, IoT, and predictive analytics for proactive asset management. A 2025 academic review highlights how AI models can process sensor and historical data to predict infrastructure failures with greater accuracy than traditional reactive methods. Companies such as Xylem are implementing "smart sewer" solutions that reduce Combined Sewer Overflow (CSO) volumes by up to 80%, saving utilities hundreds of millions in capital expenditure that would have otherwise been required for new infrastructure. This trend underscores a shift from reactive maintenance to data-driven, predictive strategies that enhance efficiency, reliability, and sustainability of water systems.

Climate Resilience and Sustainable Infrastructure Drive Investments

Climate change and extreme weather events are compelling utilities and municipalities to adopt resilient and sustainable water infrastructure solutions. The U.S. EPA, supported by the Infrastructure Investment and Jobs Act of 2021, is allocating significant funds to modernize water systems, including $4 billion for PFAS management and $11.7 billion for lead service line replacement. The World Bank reports that water-related losses could account for up to 6% of GDP by 2050 in certain regions, emphasizing the economic imperative for resilient infrastructure. These pressures drive market demand for comprehensive water infrastructure asset management platforms capable of integrating real-time data, forecasting risks, and ensuring operational continuity under extreme conditions.

Public-Private Partnerships Accelerate Modernization

Public-Private Partnerships (PPPs) are increasingly critical to bridging the financing gap in water infrastructure modernization. India’s CPHEEO demonstrates the effectiveness of hybrid annuity-based PPP models in cities like Ayodhya and Prayagraj, where private capital and expertise are leveraged to build modern wastewater systems with performance-based operations and long-term public oversight. According to the World Bank, achieving the UN’s Sustainable Development Goals for water and sanitation requires $131–$140 billion annually nearly double current public funding levels making PPPs a key mechanism to scale deployment of advanced asset management solutions.

Strategic Opportunities in Water Infrastructure Asset Management

The Water Infrastructure Asset Management Market offers strong growth opportunities for solution providers offering integrated software, services, and IoT-enabled hardware platforms. Predictive maintenance, digital twins, and cloud-based analytics enable utilities to reduce unplanned outages, optimize CAPEX and OPEX, and ensure regulatory compliance. Governments and private utilities focusing on resilient, climate-ready infrastructure present lucrative opportunities for vendors offering end-to-end asset management solutions. Expanding applications across water supply, wastewater, and stormwater systems, coupled with increasing PPP adoption, create a robust market environment for technology integration, consultancy services, and long-term managed solutions.

Market Share Analysis of Water Infrastructure Asset Management Systems

Component-Wise Market Share: Software Leads with Services and Hardware Support

By component, Software dominates with 44.1% of the market, encompassing CMMS, EAM, GIS-integrated platforms, and predictive analytics tools, which form the core intelligence for asset management programs. Services (35.7%), including consulting, system integration, data migration, and condition assessment, are critical for realizing the full value of these platforms. Hardware (16.9%), comprising sensors, IoT devices, inspection robots, and acoustic loggers, enables accurate field data collection. While hardware represents a smaller share, its rapid adoption is driving data-rich, scalable infrastructure management, highlighting the interdependence of software, services, and hardware for modern utilities.

Technology-Driven Market Share: Predictive Analytics and GIS as Core Enablers

Predictive analytics (22.5%) is the leading technology segment, leveraging AI and machine learning to forecast asset failures and optimize maintenance schedules. Geospatial data management (GIS) (20.9%) provides foundational mapping and spatial insights critical for asset planning, while SCADA systems deliver real-time operational data on flow, pressure, and performance. IoT & cloud computing (13.2%) enables scalable data collection and access, feeding analytics platforms, and digital twins offer simulation and system optimization capabilities. These technologies collectively facilitate a proactive approach to infrastructure resilience, efficiency, and sustainability.

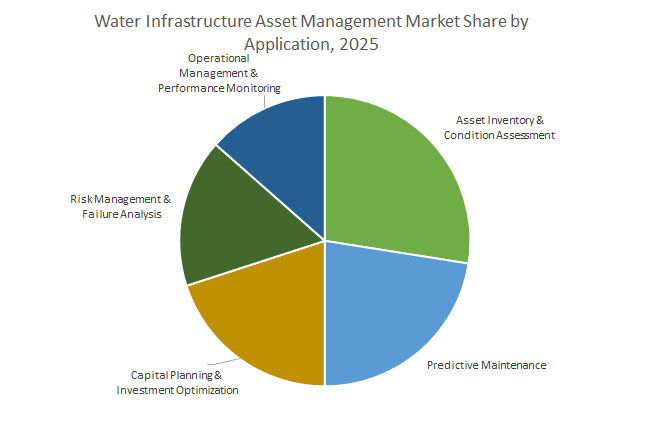

Application-Wise Market Share: Asset Inventory and Predictive Maintenance Lead

Asset inventory & condition assessment (26.9%) is the largest application segment, as utilities need a complete register of assets and their operational state before implementing advanced management strategies. Predictive maintenance (22.5%) delivers tangible ROI by reducing downtime, extending asset life, and minimizing emergency repairs. Capital planning & investment optimization (20.9%) helps utilities prioritize CAPEX, justify budgets, and improve financial planning. Risk management & failure analysis focuses on high-likelihood, high-consequence assets, while operational management & performance monitoring (13.2%) provides real-time efficiency insights for critical assets like pumps and valves.

Asset Type Market Share: Water Supply Assets Remain the Largest Focus

By asset type, Water Supply Assets (58%) lead, reflecting the criticality of delivering safe, continuous drinking water. Failures in pipelines, pumps, valves, storage tanks, and treatment plants have immediate health and economic consequences, driving investment in robust management systems. Wastewater & Stormwater Assets (44.1%) represent a substantial and growing segment, driven by EPA enforcement, CSO regulations, and aging infrastructure challenges. Municipalities prioritize monitoring and maintaining these assets to prevent environmental incidents, comply with regulations, and manage combined sewer overflows effectively.

United States: Digital Asset Management and Risk-Based Planning Drive Modernization

The United States water infrastructure asset management market is experiencing significant growth due to federal funding, regulatory initiatives, and technological innovation. The U.S. Environmental Protection Agency (EPA) leverages the Bipartisan Infrastructure Law (BIL), providing over $50 billion to states to modernize aging water infrastructure. This funding promotes the adoption of digital technologies, including advanced asset management software and risk-based planning tools, to optimize maintenance and reduce operational costs. Regulatory requirements, highlighted in the EPA’s 2024 "State Asset Management Initiatives" report, incentivize utilities to develop comprehensive asset management plans, often awarding State Revolving Fund (SRF) priority points for compliant utilities. Technological advancements are further driven by the Water Research Foundation (WRF) and the American Water Works Association (AWWA), which are supporting research on condition assessment, monitoring, and determination of effective asset life. Key applications include replacement of aging infrastructure, non-revenue water reduction, and ensuring compliance with stringent environmental regulations.

China: Smart Infrastructure and Data-Driven Governance for Urban Water Security

China’s market growth is fueled by ambitious urban development initiatives and large-scale infrastructure projects. The "Sponge City" program aims for over 80% of urban areas to meet stormwater management standards by 2030, requiring advanced asset management for both engineered and natural water systems. Large investments, such as the $170 billion hydropower dam project on the Yarlung Zangbo River initiated in July 2025, highlight the critical need for sophisticated asset management systems to ensure water security and flood mitigation. Regulatory reforms, including the "Strictest Water Resources Management System," are driving data-driven governance, requiring real-time monitoring and advanced decision-making tools. Key applications are focused on urban flooding control, sustainable rainwater management, and maintaining water quality in rapidly urbanizing regions.

Australia: Sustainable Water Management and Technological Integration

Australia’s water infrastructure asset management market is supported by major investments, regulatory commitments, and technological adoption. Sydney Water’s $34 billion 10-year investment plan, including the $100–250 million Mamre Road Precinct Stormwater project, demonstrates a commitment to asset renewal and infrastructure expansion. Government initiatives aligned with the national Net Zero Plan drive the integration of technology for decarbonized and efficient water management. Advanced water efficiency programs, including automated irrigation systems and water sensors, underscore the broader trend of leveraging digital technologies for asset monitoring and operational optimization. Market applications focus on infrastructure replacement, sustainable water management in water-scarce regions, and decarbonization of water services.

Germany: AI-Driven Digitalization and Regulatory Compliance

Germany’s water infrastructure asset management market is shaped by stringent EU directives, technological innovation, and climate adaptation strategies. The revised EU Urban Wastewater Treatment Directive (January 2025) mandates expansion to a "4th purification stage" for micropollutant removal, requiring efficient asset management systems for compliance and operational optimization. German institutions, including the DVGW Innovation Programme Water and Kompetenzzentrum Wasser Berlin (KWB), are leading research in AI-based sewer forecasting, modeling, and digitalization to address capital deficits and improve resilience. Key applications include modernization of aging infrastructure, climate adaptation, and enhancing water supply system reliability.

United Kingdom: Service-Based Solutions and Asset Optimization

The UK market is driven by regulatory frameworks, corporate innovations, and infrastructure modernization initiatives. The Water Industry National Environment Programme (WINEP) outlines environmental obligations and allocates £22.1 billion for asset improvements, including water treatment plants and sludge management projects. Service-based digital solutions, such as Siemens’ Water Quality Analytics as a Service (WQAaaS) introduced in 2024, support utilities with real-time insights to optimize operations, reduce costs, and enhance asset longevity. Key applications include modernization of aging infrastructure, improving service resilience, and integrating digital monitoring into long-term asset planning.

Japan: Advanced Monitoring and Decentralized Water Solutions

Japan’s water infrastructure asset management market growth is supported by government initiatives, research, and high-tech innovation. The Ministry of Land, Infrastructure, Transport and Tourism (MLIT) B-DASH Project focuses on developing next-generation sewage sludge fuel and fertilizer conversion technologies, which require sophisticated asset management systems. Japanese companies and academic institutions, including Toray Industries Inc., are developing advanced sensor technologies for industrial and greywater treatment, enabling real-time monitoring and digital asset management. Key applications include water conservation, decentralized on-site recycling solutions, and optimization of residential and commercial water infrastructure.

Competitive Landscape of Water Infrastructure Asset Management Market

The water infrastructure asset management market is highly competitive, with leading players focusing on digitalization, IoT integration, and climate-resilient solutions. Companies offer holistic portfolios spanning operational technology, analytics platforms, and smart asset management services.

Xylem Inc. leads in integrated digital water asset management solutions

Xylem Inc. integrates advanced analytics and digital services with water infrastructure equipment to optimize asset performance. Their Sensus smart meters and Visenti analytics platform provide real-time data for leak detection and network optimization. Strategic acquisitions of Vacom Systems and Idrica enhance Xylem’s digital capabilities. In August 2025, the company reported Q2 revenue of $2.3 billion, driven by organic growth and digital solutions adoption.

SUEZ S.A. pioneers predictive water network management

SUEZ S.A. offers end-to-end water cycle services with its flagship AQUADVANCED® digital suite, enabling real-time leak detection, pressure management, and predictive simulations. The company partnered with SAMP to deploy digital twin technology and won a June 2023 contract with PUB, Singapore, showcasing its commitment to advanced, predictive water management solutions. SUEZ is expanding in strategic markets, including Asia, with new projects in the Philippines and China.

Schneider Electric SE advances IoT-enabled infrastructure automation

Schneider Electric leverages its expertise in automation and energy management to digitize water treatment operations. Its EcoStruxure platform provides IoT-enabled process and energy optimization. Notably, January 2024 saw the automation of Mumbai’s largest water treatment plant, enhancing efficiency for millions of residents. Schneider focuses on sustainability, enabling up to 30% energy savings and CO2 reduction in water infrastructure operations.

Bentley Systems Inc. transforms water network engineering through digital twins

Bentley Systems delivers software solutions for water network modeling and infrastructure management. Their OpenFlows software supports hydraulic modeling, while the iTwin platform consolidates GIS, SCADA, and CMMS data into actionable digital twins. Bentley’s solutions facilitated AEGEA, Brazil, in flood response planning during 2024 climate emergencies, demonstrating real-world utility for proactive asset management.

Veolia Environnement S.A. integrates AI-driven water asset management

Veolia Environnement provides comprehensive water, waste, and energy management solutions. Its Hubgrade platform leverages AI and analytics for remote monitoring, predictive maintenance, and process optimization. Veolia focuses on condition-based maintenance and risk mitigation, improving asset lifespan and operational efficiency while ensuring water service continuity, including through natural disaster preparedness and process engineering innovations.

Water Infrastructure Asset Management Market Report Scope

Water Infrastructure Asset Management Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.2 Billion

|

|

Market Size (2034)

|

$23.1 Billion

|

|

Market Growth Rate

|

8.4%

|

|

Segments

|

By Component (Hardware, Software, Services), By Technology (Predictive Analytics, Geospatial Data Management, Condition Assessment Technologies, Acoustic Leak Detection, Pipeline Inspection, Structural Health Monitoring, SCADA Systems, IoT & Cloud Computing, Digital Twins), By Application (Asset Inventory & Condition Assessment, Predictive Maintenance, Risk Management & Failure Analysis, Capital Planning & Investment Optimization, Operational Management & Performance Monitoring), By Asset Type (Water Supply Assets, Wastewater & Stormwater Assets), By End-User (Municipal Utilities, Industrial Facilities, Government Agencies), By Deployment Mode (Cloud-based, On-premise)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Xylem Inc., Veolia, SUEZ, Evoqua Water Technologies, Trimble Inc., Bentley Systems, Incorporated, Schneider Electric, Itron Inc., Oracle Corporation, Rockwell Automation, Inc., Emerson Electric Co., Siemens, Autodesk, WSP, Hach (Danaher Corporation)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Infrastructure Asset Management Market Segmentation

By Component

- Hardware

- Sensors & Meters

- Data Loggers & Transmitters

- Communication Devices

- Software

- Services

By Technology

- Predictive Analytics

- Geospatial Data Management

- Condition Assessment Technologies

- Acoustic Leak Detection

- Pipeline Inspection

- Structural Health Monitoring

- SCADA Systems

- IoT & Cloud Computing

- Digital Twins

By Application

- Asset Inventory & Condition Assessment

- Predictive Maintenance

- Risk Management & Failure Analysis

- Capital Planning & Investment Optimization

- Operational Management & Performance Monitoring

By Asset Type

- Water Supply Assets

- Treatment Plants

- Storage Tanks & Reservoirs

- Pumping Stations

- Transmission & Distribution Mains

- Wastewater & Stormwater Assets

- Collection Systems & Sewers

- Wastewater Treatment Plants

- Pump Stations

- Stormwater Drainage Systems

By End-User

- Municipal Utilities

- Industrial Facilities

- Government Agencies

By Deployment Mode

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Water Infrastructure Asset Management Industry include-

- Xylem Inc.

- Veolia

- SUEZ

- Evoqua Water Technologies

- Trimble Inc.

- Bentley Systems, Incorporated

- Schneider Electric

- Itron Inc.

- Oracle Corporation

- Rockwell Automation, Inc.

- Emerson Electric Co.

- Siemens

- Autodesk

- WSP

- Hach (Danaher Corporation)

*- List not Exhaustive

Research Coverage USDAnalytics

This report investigates the Global Water Infrastructure Asset Management Market, highlighting breakthroughs in digital twins, AI-driven predictive maintenance, IoT telemetry, and GIS-centric decision support; it analysis reviews modernization funding, privatization reforms, and climate-resilience toolchains that are redefining lifecycle strategies for supply, wastewater, and stormwater assets. It highlights performance gains from non-revenue water reduction, risk-based renewals, and real-time monitoring, translating them into measurable CAPEX/OPEX outcomes for utilities and operators. By mapping component, technology, application, and asset-type trajectories through 2034, this report is an essential resource for municipal leaders, regulators, EPCs, and technology providers seeking defensible investment plans and implementation roadmaps backed by USDAnalytics’ comparative benchmarks and ROI models. Scope Includes-

- By Component: Hardware (Sensors & Meters; Data Loggers & Transmitters; Communication Devices), Software, Services

- By Technology: Predictive Analytics; Geospatial Data Management; Condition Assessment; Acoustic Leak Detection; Pipeline Inspection; Structural Health Monitoring; SCADA; IoT & Cloud Computing; Digital Twins

- By Application: Asset Inventory & Condition Assessment; Predictive Maintenance; Risk Management & Failure Analysis; Capital Planning & Investment Optimization; Operational Management & Performance Monitoring

- By Asset Type: Water Supply Assets; Treatment Plants; Storage Tanks & Reservoirs; Pumping Stations; Transmission & Distribution Mains; Wastewater & Stormwater Assets (Collection Systems & Sewers; Wastewater Treatment Plants; Pump Stations; Stormwater Drainage Systems)

- By End-User: Municipal Utilities; Industrial Facilities; Government Agencies

- By Deployment Mode: Cloud-based; On-premise

- Geographic Scope: “Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.”

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Analysis/ profiles of 15+ companies, include the list of given companies): Xylem Inc.; Veolia; SUEZ; Evoqua Water Technologies; Trimble Inc.; Bentley Systems, Incorporated; Schneider Electric; Itron Inc.; Oracle Corporation; Rockwell Automation, Inc.; Emerson Electric Co.; Siemens; Autodesk; WSP; Hach (Danaher Corporation).

Methodology

USDAnalytics employs a bottom-up model anchored in utility budgets, sensor deployments, smart-meter penetration, CMMS/EAM licenses, and project pipelines, with top-down validation using national funding programs, PPP commitments, and regulatory milestones. Primary inputs include interviews with utility asset managers, network modelers, integrators, and OEMs; secondary inputs span tender awards, digital-twin case studies, SCADA and GIS implementation reports, and climate-risk guidance. Forecasts (2025–2034) integrate scenario weights for drought/flood incidence, NRW baselines, energy prices, and pipe failure curves; sensitivity analyses quantify ROI under varying leak rates, inspection intervals, service-line mix, and telemetry coverage. A lifecycle TCO/ROI framework compares reactive vs. predictive regimes across software, services, and hardware stacks to surface the most capital-efficient renewal paths.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Water Infrastructure Asset Management Market

1. Executive Summary

1.1. Market Highlights & Key Projections

1.2. Global Market Snapshot

1.3. Key Findings

2. Water Infrastructure Asset Management Market Outlook (2025–2034)

2.1. Introduction: From Reactive Maintenance to Predictive Asset Management

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $11.2 Billion

2.2.2. Forecasted Market Size (2034): $23.1 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 8.4%

2.3. Market Drivers and Challenges

2.3.1. Drivers: Aging Infrastructure, Non-Revenue Water, and Regulatory Mandates

2.3.2. Challenges: High Capital Costs and Slow Adoption in Traditional Utilities

2.4. Key Insights for Industry Stakeholders

3. Key Market Trends and Recent Developments (2024–2025)

3.1. Market Trend: Digital Transformation Enables Predictive Asset Management

3.2. Market Trend: Climate Resilience and Sustainable Infrastructure Drive Investments

3.3. Market Trend: Public-Private Partnerships Accelerate Modernization

3.4. Recent Developments & Strategic Moves

4. Water Infrastructure Asset Management Market – Segmentation Insights (2025–2034)

4.1. By Component

4.1.1. Software (44.1% Market Share)

4.1.2. Services (35.7% Market Share)

4.1.3. Hardware (16.9% Market Share)

4.2. By Technology

4.2.1. Predictive Analytics (22.5% Market Share)

4.2.2. Geospatial Data Management (GIS) (20.9% Market Share)

4.2.3. Condition Assessment Technologies

4.2.4. SCADA Systems

4.2.5. IoT & Cloud Computing (13.2% Market Share)

4.2.6. Digital Twins

4.3. By Application

4.3.1. Asset Inventory & Condition Assessment (26.9% Market Share)

4.3.2. Predictive Maintenance (22.5% Market Share)

4.3.3. Capital Planning & Investment Optimization (20.9% Market Share)

4.3.4. Risk Management & Failure Analysis

4.3.5. Operational Management & Performance Monitoring (13.2% Market Share)

4.4. By Asset Type

4.4.1. Water Supply Assets (58% Market Share)

4.4.2. Wastewater & Stormwater Assets (44.1% Market Share)

4.5. By End-User

4.5.1. Municipal Utilities

4.5.2. Industrial Facilities

4.5.3. Government Agencies

4.6. By Deployment Mode

4.6.1. Cloud-based

4.6.2. On-premise

5. Country Analysis and Outlook: Water Infrastructure Asset Management Market

5.1. United States: Digital Asset Management and Risk-Based Planning Drive Modernization

5.2. China: Smart Infrastructure and Data-Driven Governance for Urban Water Security

5.3. Australia: Sustainable Water Management and Technological Integration

5.4. Germany: AI-Driven Digitalization and Regulatory Compliance

5.5. United Kingdom: Service-Based Solutions and Asset Optimization

5.6. Japan: Advanced Monitoring and Decentralized Water Solutions

6. Market Size Outlook by Region (2025-2034)

6.1. North America Water Infrastructure Asset Management Market Size Outlook to 2034

6.1.1. By Component

6.1.2. By Technology

6.1.3. By Application

6.1.4. By Asset Type

6.1.5. By End-User

6.1.6. By Deployment Mode

6.1.7. By Country (U.S., Canada, Mexico)

6.2. Europe Water Infrastructure Asset Management Market Size Outlook to 2034

6.2.1. By Component

6.2.2. By Technology

6.2.3. By Application

6.2.4. By Asset Type

6.2.5. By End-User

6.2.6. By Deployment Mode

6.2.7. By Country (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

6.3. Asia Pacific Water Infrastructure Asset Management Market Size Outlook to 2034

6.3.1. By Component

6.3.2. By Technology

6.3.3. By Application

6.3.4. By Asset Type

6.3.5. By End-User

6.3.6. By Deployment Mode

6.3.7. By Country (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

6.4. South America Water Infrastructure Asset Management Market Size Outlook to 2034

6.4.1. By Component

6.4.2. By Technology

6.4.3. By Application

6.4.4. By Asset Type

6.4.5. By End-User

6.4.6. By Deployment Mode

6.4.7. By Country (Brazil, Argentina, Rest of South America)

6.5. Middle East and Africa Water Infrastructure Asset Management Market Size Outlook to 2034

6.5.1. By Component

6.5.2. By Technology

6.5.3. By Application

6.5.4. By Asset Type

6.5.5. By End-User

6.5.6. By Deployment Mode

6.5.7. By Country (Saudi Arabia, UAE, South Africa, Egypt, Rest of MEA)

7. Company Profiles: Leading Players

7.1. Xylem Inc.

7.1.1. Company Overview

7.1.2. Digital Water & Asset Management Solutions

7.1.3. Recent Developments and Strategic Acquisitions

7.2. SUEZ S.A.

7.2.1. Company Overview

7.2.2. AQUADVANCED® Digital Suite and Services

7.2.3. Recent Developments and Strategic Partnerships

7.3. Schneider Electric SE

7.4. Bentley Systems, Incorporated

7.5. Veolia Environnement S.A.

7.6. Other Key Players

7.6.1. Trimble Inc.

7.6.2. Itron Inc.

7.6.3. Oracle Corporation

7.6.4. Rockwell Automation, Inc.

7.6.5. Emerson Electric Co.

7.6.6. Siemens

7.6.7. Hach (Danaher Corporation)

7.6.8. Autodesk

7.6.9. WSP

8. Methodology

8.1. Research Scope

8.2. Market Research Approach

8.3. Data Sources and Validation

8.4. Assumptions and Limitations

9. Appendix

9.1. Acronyms and Abbreviations

9.2. List of Tables

9.3. List of Figures