Global Membrane Separation Market Overview – Strong Growth Driven by Water Scarcity, Industrial Expansion, and Technological Innovation

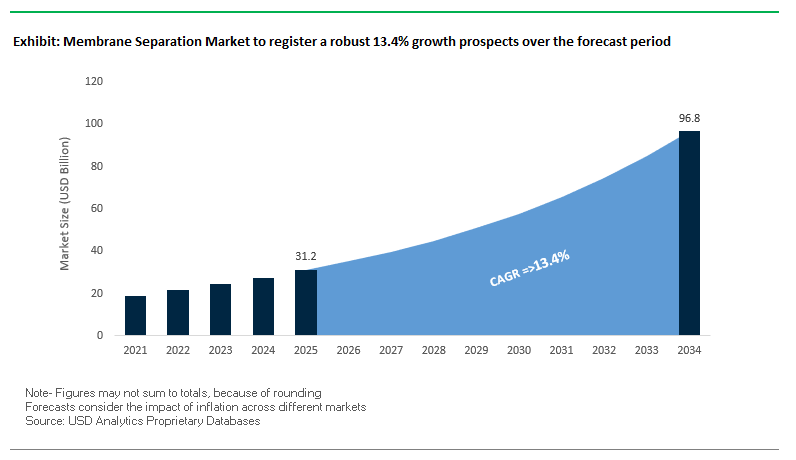

The global membrane separation market is set to expand significantly, with a market valuation of USD 31.2 billion in 2025 projected to reach USD 96.8 billion by 2034, reflecting a robust CAGR of 13.4%. This rapid growth trajectory is fueled by escalating urbanization, industrialization, and rising concerns over water scarcity, which have intensified the demand for advanced water purification and wastewater treatment solutions. Industry Stakeholders are increasingly looking at membrane technologies as a cornerstone of sustainable industrial operations and urban water supply systems, given their energy efficiency and effectiveness in handling complex separation challenges. The market also benefits from growing R&D investments, government-led water reuse programs, and rising adoption in life sciences and biopharmaceutical filtration.

Key Insights for Industry Stakeholders

- Urbanization and Wastewater Treatment Gap: WHO/UNICEF data from 2020 revealed that only 56% of domestic wastewater worldwide was safely treated, underscoring a massive growth opportunity for membrane technologies.

- Rising Water Reuse Infrastructure: Municipal wastewater facilities in the UK already manage 7.3 billion cubic meters annually, highlighting untapped potential for integrating membranes into large-scale water reclamation projects.

- Energy-Efficient Solutions: Advancements in reverse osmosis and related systems are cutting operational costs by reducing feed pressure requirements, positioning energy efficiency as a major competitive advantage.

- Innovation Surge: In 2024, global R&D spending on advanced membranes grew by 15%, strengthening the pipeline of next-generation materials and systems for industrial and pharmaceutical applications.

Market Analysis – Recent Developments Reshaping the Membrane Separation Industry

The membrane separation industry has witnessed a series of transformative developments in 2025, reflecting both technological breakthroughs and strategic corporate shifts. In March 2025, True North Venture Partners merged its portfolio companies Nanostone Water and Solecta to form Acuriant Technologies, creating a powerful new player focused on solving complex separation challenges in water treatment, dairy, and life sciences. In April 2025, Asahi Kasei launched its “Trailblaze Together” medium-term management plan, signaling a strong commitment to sustainable growth and innovation. This was followed by May 2025, when Asahi Kasei Medical completed its third assembly plant for Planova™ virus removal filters in Nobeoka, Japan—an expansion aimed at meeting surging demand in pharmaceutical and life science sectors.

Meanwhile, technology innovation remains a core focus across the industry. In June 2025, California-based Active Membranes, with support from the National Alliance for Water Innovation, announced a breakthrough reverse-osmosis membrane with an electrically conductive coating. Field pilots in Ventura County demonstrated a 30% improvement in water production by minimizing fouling and scaling—an advancement that directly addresses one of the most pressing operational challenges for utilities. Similarly, Pentair plc announced a leadership transition in July 2025, appointing Lance Bonner as Executive Vice President, as the company continues executing its 80/20 strategy for long-term margin improvements.

Asahi Kasei continues to strengthen its global positioning through diversification and ESG alignment. In August 2025, the company was selected for continued inclusion in global sustainability indices such as the FTSE4Good Index Series and FTSE Blossom Japan Index, reinforcing its commitment to environmental, social, and governance standards. In the same month, it revealed plans to double its production of PIMEL™ photosensitive polyimide by 2030, catering to the high-growth semiconductor packaging sector, including applications in AI servers. These initiatives highlight how membrane separation companies are increasingly blending core water-related offerings with cross-sector innovations.

Key Market Trends Shaping Membrane Separation Technologies

The membrane separation market is undergoing a rapid transformation fueled by stricter regulations, technological advancements, and industry-wide adoption in critical sectors. One of the most significant trends is the growing demand for industrial water and wastewater treatment, driven by escalating environmental regulations and increasing water scarcity. According to the U.S. Environmental Protection Agency (EPA), mandates under the Clean Water Act are compelling industries to deploy advanced solutions such as reverse osmosis (RO) and ultrafiltration (UF), recognized as “Best Available Technologies” for removing complex pollutants. This regulatory landscape is propelling large-scale deployment across sectors including chemicals, power generation, and food & beverage.

Another emerging trend is the innovation in advanced membrane materials and fabrication methods, where mixed-matrix membranes (MMMs), bio-inspired structures, and nanomaterial integrations are redefining performance. Academic research, including studies published in ACS Applied Materials & Interfaces, shows how the incorporation of graphene oxide and MOFs enhances both selectivity and permeability, enabling breakthrough efficiency in gas separation and CO₂ removal. Furthermore, biopharmaceutical applications are witnessing surging adoption of membrane technologies, as they offer scalability, high precision, and gentle operating conditions for sensitive biomolecules. Case studies from global pharmaceutical leaders highlight significant improvements in protein purification and monoclonal antibody production, with operational savings and yield improvements of over 15%.

In addition, the role of membrane separation in gas purification and carbon capture is rapidly expanding, with the U.S. Department of Energy backing multi-million-dollar demonstration projects targeting over 90% CO₂ capture efficiency at reduced energy costs. Together, these trends underscore how membrane separation technologies are moving beyond water treatment to play a central role in global sustainability, healthcare, and industrial innovation.

Emerging Opportunities Unlocking Market Growth

Water and wastewater treatment remains the backbone of the market and presents significant opportunities in emerging high-value applications. One of the most promising opportunities lies in carbon capture and sustainable energy solutions, where polymer-based membranes are being integrated into pilot-scale power plants to decarbonize operations at lower energy costs compared to traditional amine-based scrubbing. With governments pushing aggressive net-zero targets, this creates a multibillion-dollar opportunity for membrane manufacturers. Another area of opportunity is the biopharmaceutical and medical sector, where rising demand for biologics, vaccines, and personalized medicine is driving reliance on membrane filtration for virus removal, sterile processing, and ultrapure water systems. The scalability of membrane solutions provides pharmaceutical firms with operational flexibility while ensuring regulatory compliance.

Food and beverage manufacturers also represent a growing opportunity, as consumer preference shifts toward non-thermal, clean-label processing. Membranes are now widely used for juice concentration, dairy protein fractionation, and wine clarification, all of which align with global health-conscious consumption trends. In addition, industrial applications beyond water treatment, such as petrochemicals, pulp & paper, and electronics, are creating untapped growth potential, especially with the adoption of zero-liquid discharge (ZLD) systems and the rising need for ultrapure water in semiconductor manufacturing. Collectively, these opportunities indicate that the membrane separation market is transitioning from a niche water-focused technology into a cross-industry enabler of sustainability, efficiency, and innovation.

Market Share Analysis of the Membrane Separation Market

Market Share by Technology

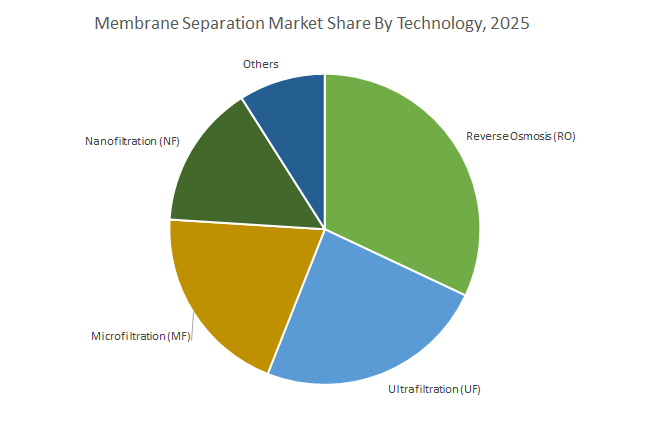

The membrane separation market by technology is projected to remain dominated by reverse osmosis (RO), capturing around 32% of the market share in 2025. RO’s dominance stems from its indispensable role in seawater desalination and the production of high-purity water, both critical in addressing the escalating global water scarcity crisis. Alongside this, nanofiltration (NF) is expected to witness the fastest growth, expanding at a CAGR of 10.2%. NF has gained traction as a sustainable alternative for water softening and partial demineralization in food & beverage and bioprocessing industries, as it effectively removes divalent ions without the high energy demand of RO. Ultrafiltration (UF) and microfiltration (MF), holding shares of 24% and 20% respectively, serve as indispensable workhorses for pre-treatment in RO systems and find extensive use in wastewater recovery, biopharmaceutical sterile processing, and food production. The “others” category, while smaller at 9%, includes forward osmosis and electrodialysis, which are gradually gaining attention in niche markets such as brine concentration and industrial effluent recovery.

Market Share by Module Design

The module design segment of the membrane separation market highlights the centrality of spiral wound modules, which are forecasted to account for approximately 55% of the total market share by 2025. Spiral wound designs dominate due to their compactness, high surface-area-to-volume ratio, and suitability for high-pressure applications in RO and NF, particularly in desalination plants and large-scale industrial water treatment. Hollow fiber modules, with a projected 28% share, remain critical in municipal wastewater treatment and membrane bioreactors (MBRs), owing to their backwashability and reliability. They also hold significant importance in medical applications such as hemodialysis. Meanwhile, plate and frame and tubular modules, although smaller in market share at 10% and 7% respectively, are vital for high-solid or high-fouling feed streams such as dairy processing, fruit juice clarification, pulp & paper, and industrial sludge treatment. Their easy-cleaning characteristics and ability to process viscous streams ensure their continued relevance in specialized industrial processes.

Market Share by Application

From an application perspective, the water and wastewater treatment segment is expected to maintain its leadership, commanding 42% of the global membrane separation market by 2025. This segment’s dominance reflects the global urgency surrounding water scarcity, population growth, and tightening discharge regulations, which have made membrane-based treatment indispensable for municipal and industrial reuse. Food and beverage applications, projected at 16% market share, represent one of the fastest-growing and highest-value areas, as membranes provide non-thermal, efficient processing options for juice concentration, dairy protein separation, and brewery filtration. Pharmaceutical and medical uses, projected at 14%, remain equally critical, given their role in sterile drug production, biopharmaceutical purification, and life-saving healthcare equipment such as dialysis machines. The chemical and petrochemical sector continues to rely on membranes for product separation, recovery, and process water treatment, while the “others” category encompasses growth opportunities in pulp & paper, semiconductors, and electronics. Ultra-high-purity water requirements in electronics manufacturing and zero-liquid discharge (ZLD) mandates across industries are expected to drive this segment’s future momentum.

China: Regulatory Compliance and Technological Innovations Driving Growth

China is aggressively advancing its membrane separation market through stringent regulatory frameworks, technological innovations, and strategic investments. The Ministry of Ecology and Environment (MEE) mandates that all industrial entities discharging atmospheric and water pollutants obtain emission permits, driving widespread adoption of advanced membrane technologies for wastewater and industrial effluent treatment. In 2024, Chinese researchers developed a hollow-fiber ultrafiltration (UF) membrane with enhanced antifouling properties, tackling a critical challenge in long-term industrial wastewater management. Government investments under the 14th Five-Year Plan (2021-2025) to expand natural gas infrastructure are fueling the demand for nanofiltration and membrane technologies in oil and gas applications. Additionally, initiatives in Guangdong province leverage advanced membrane systems for industrial wastewater reuse in cooling towers and non-potable applications, significantly reducing freshwater consumption.

Saudi Arabia: Strategic Investments in Desalination and RO Technology

Saudi Arabia is cementing its leadership in membrane separation through large-scale investments in desalination infrastructure and advanced reverse osmosis (RO) technology. Projects like the Jubail 3A desalination plant, spearheaded by ACWA Power, produce 600,000 cubic meters of freshwater daily using cutting-edge RO systems, representing a $658 million investment. The Saline Water Conversion Corporation (SWCC) is pioneering energy-efficient RO membranes, exemplified by the Yanbu 4 desalination plant producing 450,000 cubic meters per day, aligning with the nation’s sustainability goals. Additionally, government-backed initiatives led by the Saudi Water Partnership Company (SWPC), including the Rabigh 4 desalination project, underscore the Kingdom’s strategic shift toward membrane-based water treatment, reinforcing the role of membrane technologies in national water security.

United States: Government Funding and Advanced Research Accelerating Adoption

The United States is a prominent market for membrane separation technologies, propelled by substantial government funding, academic innovations, and corporate initiatives. The Bipartisan Infrastructure Law allocates over $50 billion to the Environmental Protection Agency (EPA) to modernize water infrastructure, with a particular focus on addressing emerging contaminants such as PFAS, requiring high-performance membrane filtration solutions. Research centers funded by the National Science Foundation (NSF), such as the Membrane Applications Science and Technology (MAST) Center, are developing next-generation membranes for water purification, chemical separations, and biopharmaceutical applications. In 2024, Membrane Technology & Research received an $8 million grant to advance membrane research. Additionally, companies like Veolia Water Technologies have deployed treatment systems ensuring PFAS levels remain below regulatory thresholds for over 140,000 Americans, highlighting private-sector contributions to the adoption of advanced membrane solutions.

India: Government Initiatives and Infrastructure Investments Supporting Expansion

India’s membrane separation market is experiencing strong growth due to government-driven initiatives, infrastructure investments, and expanding applications. The Jal Jeevan Mission, alongside the Department of Science & Technology's Water Technology Initiative, promotes research in nanomaterials and filtration technologies to provide safe and affordable drinking water, particularly in rural regions. Urban projects such as Mumbai’s Worli sewage treatment plant, utilizing Veolia’s membrane bioreactor (MBR) technology with a capacity of 500 MLD, exemplify advanced urban water management. In August 2024, VA TECH WABAG secured a seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant in Chennai, valued at approximately INR 415 crores, demonstrating significant investment in maintaining and expanding membrane-based water treatment infrastructure.

Japan: Pioneering Membrane R&D and Global Technology Exports

Japan is at the forefront of membrane innovation, driven by strong academic and corporate R&D initiatives. Research from Kobe University’s Membrane Engineering Group highlights ongoing development of novel biomimetic and highly porous membranes for water and atmospheric applications. Japanese corporations, such as Toray Industries, continue to lead in high-performance RO membranes for desalination and water purification. Their recent contributions to large-scale projects in Saudi Arabia underscore Japan’s strategic role as a global technology provider in the membrane separation sector, strengthening international adoption of Japanese-developed membrane solutions.

Germany: Industrial Wastewater Solutions and Advanced Filtration Technologies

Germany leads the European membrane separation market through advanced industrial wastewater treatment solutions and technological innovations. Companies like PWT Wassertechnik specialize in microfiltration, ultrafiltration, and reverse osmosis systems to treat and reuse industrial effluents while ensuring compliance with stringent environmental regulations. MANN+HUMMEL, a multinational German firm, focuses on innovative membrane, filtration, and digital solutions for industrial processes and green energy applications. The country’s robust industrial base, combined with advanced technological development, positions Germany as a key market for membrane separation solutions in industrial and process water treatment.

Australia: Water Recycling Initiatives and Academic Research Driving Adoption

Australia, facing significant water scarcity, has emerged as a leader in membrane-based water recycling and reuse. Facilities like the Sydney Water Wollongong Water Resource Recovery Facility utilize combined microfiltration and reverse osmosis systems to repurpose wastewater for irrigation and non-potable applications. Research initiatives at the Institute for Sustainable Industries and Liveable Cities (ISILC), Victoria University, focus on improving water recovery from desalination and reducing membrane fouling and scaling, addressing critical challenges in long-term water management. These efforts highlight Australia’s strategic use of membrane separation technologies to enhance sustainability and resilience in water-stressed regions.

Competitive Landscape – Leading Companies Driving Membrane Separation Advancements

The competitive landscape of the membrane separation market is characterized by a mix of global leaders and specialized innovators, each leveraging unique strengths in technology, application expertise, and regional presence. Companies are not only expanding their portfolios but also investing heavily in R&D, digitalization, and sustainability-driven initiatives. Below is a detailed look at the strategies and offerings of five key players shaping the market.

DuPont Water Solutions – Innovation Through Digital Integration and Advanced RO Technologies

DuPont Water Solutions stands as one of the most influential players in the membrane separation market, offering a comprehensive range of technologies including RO, NF, UF, and IX. Its Water Application Value Engine (WAVE) software provides customers with advanced system design capabilities, ensuring optimal performance. DuPont has strengthened its portfolio with FilmTec™ Fortilife™ RO elements, engineered for high-resilience in fouling-prone waters. Its Global Water Technology Center in Tarragona, Spain, enables collaboration with customers for real-world testing of multi-technology systems. A recent pilot project in India demonstrated DuPont’s minimal liquid discharge (MLD) approach, achieving a 75% reduction in cleaning costs and 10% energy savings, exemplifying strong ROI for industrial users.

SUEZ Water Technologies & Solutions – Global Scale with Focus on Smart Water Management

SUEZ has a commanding presence, with an estimated 10,000 water plants in Asia alone, showcasing its deep penetration in municipal and industrial water treatment. Its Singapore-based R&D center is spearheading development of next-generation membrane bioreactors, targeting reductions in energy-intensive wastewater treatment processes. SUEZ also invests in digital water management tools, enabling remote monitoring and predictive diagnostics. Recent pilots with PUB Singapore demonstrate its application of smart metering and stormwater management solutions. By integrating membranes with holistic water management services, SUEZ continues to position itself as a global partner for sustainable urban water solutions.

Toray Industries, Inc. – Materials Science Expertise Driving High-Performance Membranes

Toray Industries leverages its advanced polymer science expertise to deliver a broad portfolio of RO, NF, UF, and MF membranes. Its long-standing strength in materials engineering enables the creation of durable, high-performance membranes tailored for municipal and industrial process water applications. Toray has recently expanded its global manufacturing footprint to meet rising demand, underlining its strategic commitment to scale. With a strong balance of innovation and large-scale production capacity, Toray remains a trusted name in membrane technologies for both urban water supply and industrial use.

Pentair plc – Operational Excellence and Strategic Expansion in Water Solutions

Pentair continues to sharpen its competitive edge through a strong focus on operational efficiency, having generated $100 million in net productivity benefits in 2024 via its 80/20 strategy. Its product portfolio spans RO membranes, control valves, and pressure tanks, with growing applications in both residential and commercial water treatment. While its pool segment has been a major revenue driver, the company is increasingly applying its expertise in circulation and filtration to industrial and municipal water treatment opportunities. The July 2025 leadership appointment of Lance Bonner reinforces Pentair’s forward-looking governance as it aims to sustain momentum in margin improvements and expansion.

Asahi Kasei Corporation – Expanding Role in Biopharmaceutical and Specialty Membrane Applications

Asahi Kasei has carved a distinct niche in the membrane market through its Planova™ virus removal filters, which are critical in biopharmaceutical manufacturing. The company has expanded into complete water-for-injection (WFI) systems, widening its healthcare applications. In May 2025, Asahi Kasei Medical completed its third assembly plant in Japan, boosting production capacity to meet increasing global demand. The company’s strategic sustainability positioning was further validated in August 2025, with inclusion in major ESG indices. By combining healthcare specialization with cross-industry innovation—such as expanding PIMEL™ polyimide production for the semiconductor sector—Asahi Kasei demonstrates a diversified, forward-looking growth model.

Membrane Separation Market Report Scope

Membrane Separation Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$31.2 Billion

|

|

Market Size (2034)

|

$96.8 Billion

|

|

Market Growth Rate

|

13.4%

|

|

Segments

|

By Technology (Microfiltration, Ultrafiltration, Nanofiltration, Reverse Osmosis, Others), By Material (Polymeric Membranes, Ceramic, Composite, Metallic, Others), Module Design (Spiral Wound, Hollow Fiber, Plate and Frame, Tubular), Application (Water and Wastewater Treatment, Food and Beverage, Pharmaceutical, Chemical and Petrochemical, Pulp and Paper, Healthcare and Medical, Electronics, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SUEZ, DuPont de Nemours, Inc., Veolia, Pentair plc, Xylem Inc., Toray Industries, Inc., Asahi Kasei Corporation, Koch Industries, Kubota Corporation, The Dow Chemical Company, MANN+HUMMEL, Hydranautics (a Nitto Group Company), LG Chem, EVOQUA Water Technologies, V.A. TECH WABAG Ltd.,

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Membrane Separation Market Segmentation

By Technology

- Microfiltration

- Ultrafiltration

- Nanofiltration

- Reverse Osmosis

- Others (Pervaporation, Gas Separation, Electrodialysis)

By Material

- Polymeric Membranes

- Ceramic

- Composite

- Metallic

- Others

By Module Design

- Spiral Wound

- Hollow Fiber

- Plate and Frame

- Tubular

By Application

- Water and Wastewater Treatment

- Food and Beverage

- Pharmaceutical

- Chemical and Petrochemical

- Pulp and Paper

- Healthcare and Medical

- Electronics

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Membrane Separation Industry include-

- SUEZ

- DuPont de Nemours, Inc.

- Veolia

- Pentair plc

- Xylem Inc.

- Toray Industries, Inc.

- Asahi Kasei Corporation

- Koch Industries

- Kubota Corporation

- The Dow Chemical Company

- MANN+HUMMEL

- Hydranautics (a Nitto Group Company)

- LG Chem

- EVOQUA Water Technologies

- V.A. TECH WABAG Ltd.

*- List not Exhaustive

Research Coverage

This report investigates the global membrane separation market, delivering a comprehensive view of industry dynamics, breakthroughs in filtration technologies, and strategic corporate developments. It provides in-depth analysis reviews of key segments, highlights regulatory drivers such as global water scarcity and environmental mandates, and tracks innovation in nanomaterials, mixed-matrix membranes, and reverse osmosis advancements. The study also reviews recent corporate mergers, product launches, and government initiatives, showcasing how the industry is rapidly evolving beyond water treatment into pharmaceuticals, food processing, energy, and electronics. With detailed insights on emerging opportunities in carbon capture, healthcare, and industrial reuse, this report is an essential resource for industry professionals, policymakers, and investors navigating the future of separation technologies. Produced by USDAnalytics, the study blends market intelligence with competitive benchmarking to help stakeholders identify growth opportunities, manage risks, and shape long-term strategies. Scope Includes-

- Segmentation: By Technology (Microfiltration, Ultrafiltration, Nanofiltration, Reverse Osmosis, Others), By Material (Polymeric, Ceramic, Composite, Metallic, Others), By Module Design (Spiral Wound, Hollow Fiber, Plate & Frame, Tubular), By Application (Water & Wastewater, Food & Beverage, Pharmaceutical, Chemical & Petrochemical, Pulp & Paper, Healthcare, Electronics, Others).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies: Analysis and profiles of 15+ leading companies, including DuPont Water Solutions, SUEZ, Toray Industries, Asahi Kasei, Pentair, Veolia, and others.

Methodology

The research methodology for the Global Membrane Separation Market combines primary research through interviews with industry stakeholders, technology providers, and regulatory experts, with secondary research from reliable databases, government reports, academic publications, and company filings. Market size estimates and forecasts are derived using a top-down and bottom-up triangulation approach, supported by value-chain analysis and Porter’s Five Forces assessment. Regional adoption trends were validated through case studies and country-specific policy reviews, while growth projections were stress-tested against macroeconomic factors, technology adoption cycles, and regulatory frameworks. This robust methodology ensures accurate, transparent, and actionable insights for decision-makers.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Membrane Separation Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

2. Membrane Separation Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $31.2 Billion

2.2.2. Forecasted Market Size (2034): $96.8 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 13.4%

2.3. Key Market Trends Shaping Technologies

2.3.1. Growth in Industrial Water and Wastewater Treatment

2.3.2. Innovation in Advanced Membrane Materials

2.3.3. Expansion in Biopharmaceutical and Gas Purification

2.4. Emerging Opportunities Unlocking Market Growth

3. Recent Developments and Strategic Shifts

3.1. Market Trend: Mergers and Acquisitions

3.1.1. True North Venture Partners’ Formation of Acuriant Technologies

3.1.2. Pentair plc’s Leadership Transition and 80/20 Strategy

3.2. Market Trend: Technological Breakthroughs

3.2.1. Active Membranes’ Breakthrough Electrically Conductive RO Membrane

3.2.2. Asahi Kasei’s Capacity Expansion for Planova™ Filters

3.3. Market Opportunity: Cross-Sector Innovation and ESG Alignment

3.3.1. Asahi Kasei's Diversification into Semiconductor Packaging

3.3.2. Inclusion in Global Sustainability Indices

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Materials Science to System Integration

4.2. Key Competitive Factors

4.2.1. Technology Portfolio and R&D Investment

4.2.2. Global Presence and Regional Expertise

4.2.3. Operational Excellence and Sustainability Initiatives

4.3. Profiles of Top Players

4.3.1. DuPont Water Solutions

4.3.2. SUEZ Water Technologies & Solutions

4.3.3. Toray Industries, Inc.

4.3.4. Pentair plc

4.3.5. Asahi Kasei Corporation

5. Membrane Separation Market – Segmentation Insights

5.1. By Technology

5.1.1. Reverse Osmosis (RO)

5.1.2. Nanofiltration (NF)

5.1.3. Ultrafiltration (UF)

5.1.4. Microfiltration (MF)

5.1.5. Others

5.2. By Module Design

5.2.1. Spiral Wound

5.2.2. Hollow Fiber

5.2.3. Plate and Frame

5.2.4. Tubular

5.3. By Application

5.3.1. Water and Wastewater Treatment

5.3.2. Food and Beverage

5.3.3. Pharmaceutical and Medical

5.3.4. Chemical and Petrochemical

5.3.5. Others

6. Country Analysis and Outlook: Membrane Separation Market

6.1. China: Regulatory Compliance and Technological Innovations

6.2. Saudi Arabia: Strategic Investments in Desalination

6.3. United States: Government Funding and Advanced Research

6.4. India: Government Initiatives and Infrastructure Investments

6.5. Japan: Pioneering Membrane R&D and Global Exports

6.6. Germany: Industrial Wastewater Solutions

6.7. Australia: Water Recycling Initiatives

6.8. Other Key Countries

7. Membrane Separation Market Size Outlook by Region (2025-2034)

7.1. North America Membrane Separation Market Size Outlook to 2034

7.1.1. Market Size by Technology

7.1.2. Market Size by Module Design

7.1.3. Market Size by Application

7.2. Europe Membrane Separation Market Size Outlook to 2034

7.2.1. Market Size by Technology

7.2.2. Market Size by Module Design

7.2.3. Market Size by Application

7.3. Asia Pacific Membrane Separation Market Size Outlook to 2034

7.3.1. Market Size by Technology

7.3.2. Market Size by Module Design

7.3.3. Market Size by Application

7.4. South America Membrane Separation Market Size Outlook to 2034

7.4.1. Market Size by Technology

7.4.2. Market Size by Module Design

7.4.3. Market Size by Application

7.5. Middle East and Africa Membrane Separation Market Size Outlook to 2034

7.5.1. Market Size by Technology

7.5.2. Market Size by Module Design

7.5.3. Market Size by Application

8. Company Profiles

8.1. SUEZ

8.2. DuPont de Nemours, Inc.

8.3. Veolia

8.4. Xylem Inc.

8.5. Toray Industries, Inc.

8.6. Asahi Kasei Corporation

8.7. Koch Industries

8.8. Kubota Corporation

8.9. The Dow Chemical Company

8.10. MANN+HUMMEL

8.11. Hydranautics (a Nitto Group Company)

8.12. LG Chem

8.13. EVOQUA Water Technologies

8.14. V.A. TECH WABAG Ltd.

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures