Membrane Separation Materials Market Outlook: Growth, CAGR, and Industry Insights

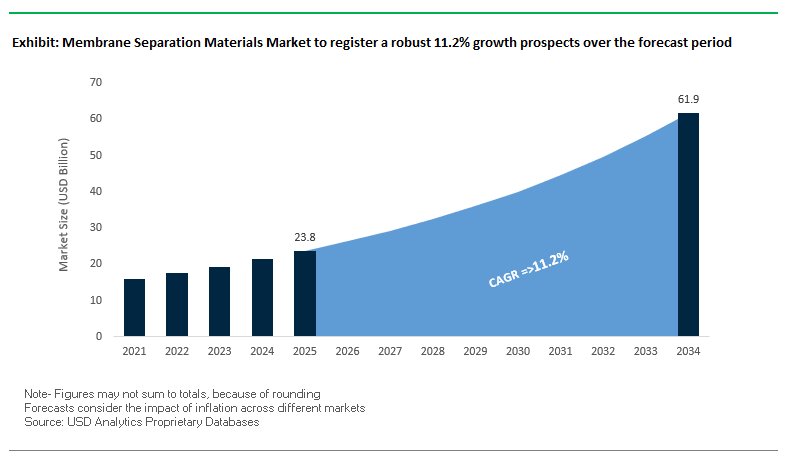

The Membrane Separation Materials Market is projected to grow from USD 23.8 billion in 2025 to USD 61.9 billion by 2034, registering a strong CAGR of 11.2%. This growth is underpinned by escalating global water scarcity, the transition to cleaner energy systems, and the rising adoption of high-performance membranes across industries such as pharmaceuticals, food & beverage, power generation, and biogas purification.

Industry Stakeholders are prioritizing scalable, sustainable, and energy-efficient separation technologies, with membrane separation emerging as a cornerstone of both water and industrial process management. The sector is witnessing accelerated adoption due to its chemical-free operation, high recovery rates, and lower energy consumption compared to traditional separation methods like distillation and evaporation.

Key Market Insights Driving Growth

- Water Scarcity & Treatment Needs: Billions globally lack access to safe drinking water (WHO/UNICEF), driving large-scale deployment of membrane separation materials in municipal and industrial water treatment.

- Industrial Efficiency & Circular Economy: Regulations mandating water reuse, resource recovery, and lithium extraction from brines are propelling demand for advanced membranes.

- Pharmaceutical & Biopharma Growth: Membranes are critical in sterile filtration, virus removal, and drug purification for advanced biologics and Antibody-Drug Conjugates (ADCs).

- Gas Separation for Energy Transition: Polymeric and polyaramide membranes are increasingly deployed for CO₂ removal from natural gas and biogas upgrading, enabling renewable fuel use.

- Energy Efficiency: Low-pressure RO and high-flux UF membranes offer substantial electricity savings, making them attractive for cost-sensitive industries.

Recent Market Developments Strengthening the Membrane Separation Materials Industry

The membrane separation materials market has been marked by significant product innovations, partnerships, and restructuring moves that highlight its role in water security, industrial efficiency, and clean energy transition.

In August 2025, DuPont Water Solutions won a BIG Sustainability Award for its FilmTec™ Fortilife™ membranes, recognized for enabling more efficient industrial wastewater treatment. A month earlier, in July 2025, Toray Industries supplied reverse osmosis membranes to Saudi Arabia’s Shuaibah 3 IWP desalination plant, a milestone in converting energy-intensive desalination into an eco-friendlier process. That same month, SUEZ commissioned China’s largest industrial membrane-based seawater desalination plant, ensuring long-term water security for industrial zones.

Strategic consolidation is reshaping the market. In June 2025, Nanostone Water and Solecta merged to form Acuriant Technologies, integrating polymeric and ceramic membrane technologies to solve complex separation challenges. Around the same time, LG Chem divested its water solutions business including RO membranes to Glenwood Private Equity, signaling a sharper focus on core materials and energy solutions.

On the product front, Veolia launched its TERION™ S system in May 2025, combining RO and EDI for compact, high-purity water production. Earlier, in September 2024, SUEZ unveiled new high-performance UF membranes for municipal and industrial purification, while Evonik introduced the Sepuran Green G5X biogas membrane, the world’s highest-capacity module in its category, supporting the global shift toward renewable gas.

Key Trends and Opportunities Transforming the Membrane Separation Materials Market

Innovation in Advanced Polymeric Membranes to Overcome Limitations

Polymeric membranes remain the cornerstone of the global membrane separation materials market, but continuous innovation is reshaping their performance profile. A major trend is the incorporation of functional nanomaterials such as graphene oxide and carbon nanotubes into polymer matrices, which enhances hydrophilicity, anti-fouling, and operational stability. According to a review published in ACS Applied Materials & Interfaces, modified PVDF membranes demonstrated significant improvements in fouling resistance and lifespan compared to conventional membranes. This trend highlights how next-generation composite polymeric membranes are addressing the traditional trade-off between permeability and selectivity, making them more efficient for water treatment and industrial separations.

Rising Adoption of Ceramic Membranes in Harsh Environments

Ceramic and inorganic membranes are rapidly gaining market traction due to their superior chemical, thermal, and mechanical durability in challenging operating conditions. While their higher cost has historically limited adoption, advances in manufacturing are gradually lowering price barriers. A case study published in the Journal of Membrane Science detailed the deployment of silicon carbide (SiC) ceramic membranes in treating high-temperature oily wastewater at refineries, demonstrating their ability to maintain flux stability where polymeric membranes degrade. This trend underscores ceramic membranes’ growing role in industries such as oil & gas, petrochemicals, and high-strength wastewater treatment.

Sustainability and Bio-Based Membranes Supporting Circular Economy Goals

The drive toward sustainable and circular economy practices is significantly influencing the membrane separation materials market. Researchers supported by the National Institutes of Health (NIH) have demonstrated the successful fabrication of membranes using recycled polyethylene terephthalate (PET) bottles and cellulose derived from waste streams. These recycled-material membranes showed comparable separation performance to commercial membranes while dramatically reducing environmental footprints. As environmental regulations tighten globally, bio-based and recyclable membranes are emerging as strategic solutions for companies aiming to minimize lifecycle impacts.

Mixed-Matrix Membranes (MMMs) Enhancing Gas Separation Performance

Mixed-matrix membranes (MMMs) are one of the fastest-growing material innovations, combining polymeric flexibility with the selectivity of inorganic fillers such as zeolites and metal-organic frameworks (MOFs). Their use is particularly strong in gas separation applications, including natural gas purification and carbon capture. Research published in The Journal of Membrane Science revealed that MMMs incorporating MOFs into polymer matrices improved CO2/CH4 selectivity by over 50% compared to pure polymer membranes. With global emphasis on carbon reduction and energy-efficient gas processing, MMMs are positioned as a disruptive innovation in the membrane separation materials market.

Expanding Role in Global Water & Wastewater Treatment

The single largest opportunity for membrane separation materials lies in water and wastewater treatment, driven by urbanization, industrialization, and stricter regulatory discharge standards. The growing reliance on desalination and advanced treatment technologies is boosting the demand for high-performance polymeric and ceramic membranes. Companies that innovate around anti-fouling coatings and longer operational lifespans will be well-positioned to capture this demand surge.

High-Value Applications in Life Sciences and Biopharmaceuticals

The life sciences and healthcare sector represents a lucrative growth opportunity for advanced membranes. From sterile filtration in pharmaceutical manufacturing to hemodialysis membranes in medical devices, the demand for membranes tailored to stringent regulatory standards is expanding. As the biopharmaceutical industry scales globally, membrane materials that provide consistent, validated performance will be critical.

Emerging Potential in Energy and Environmental Applications

Energy and environment-focused opportunities are gaining momentum, particularly in carbon capture, biogas upgrading, and hydrogen purification. Membrane technologies are increasingly viewed as cost-effective and modular alternatives to traditional separation methods. With rising investment in clean energy, demand for mixed-matrix and ceramic membranes capable of handling aggressive gas streams will grow significantly beyond 2025.

Industrial Processing Diversification Enhancing Market Reach

Industrial processing applications, including food & beverage, chemical processing, and petrochemicals, present expanding opportunities for membrane materials. Whether for juice clarification, dairy ultrafiltration, or solvent recovery in chemical industries, membrane-based separation improves both efficiency and sustainability. With growing focus on resource recovery and process optimization, this segment offers significant opportunities for material innovation.

Market Share Analysis of the Membrane Separation Materials Market

Market Share by Type: Polymeric Membranes Retain Leadership While Ceramics Surge

By 2025, polymeric membranes will command 65% of the global market, driven by their cost-effectiveness, scalability, and well-established production base. Materials such as PVDF, PS, PES, and cellulose acetate dominate water and wastewater treatment applications. However, ceramic and inorganic membranes, holding 20%, are the fastest-growing category due to their superior performance in extreme conditions. Hybrid and composite membranes (12%) are also advancing, blending the best properties of polymers and ceramics for high-value niches. Emerging categories, including graphene oxide and carbon nanotube membranes (3%), are in early commercialization but hold long-term disruptive potential.

Market Share by Technology: Reverse Osmosis Leads While UF and MF Dominate Volume

The market by technology is led by reverse osmosis (RO) with 30% share, largely due to its indispensable role in desalination and ultrapure water production. RO systems command high value because of their pressure-driven design and ability to remove dissolved salts. Ultrafiltration (UF, 25%) and Microfiltration (MF, 20%) represent the workhorse technologies, widely deployed for bacteria and particle removal in municipal water treatment and food processing. Nanofiltration (NF, 15%) occupies a unique middle ground, particularly for water softening and targeted contaminant removal. The “Other” technologies (10%) category, including electrodialysis, membrane distillation, and pervaporation, is critical for niche applications such as brackish water treatment, solvent recovery, and concentration of heat-sensitive products.

Market Share by Application: Water & Wastewater Anchors Demand, Life Sciences Drive Value

Applications of membrane separation materials are anchored by water and wastewater treatment (45%), fueled by global concerns around freshwater scarcity and stricter discharge norms. This remains the core growth driver of the market. Industrial processing (30%) follows closely, encompassing food & beverage, pharmaceuticals, and chemical processing, where efficiency and sustainability are key motivators. Life sciences and healthcare (15%) is a high-value segment, covering sterile filtration, drug purification, and medical-grade applications such as hemodialysis. Finally, the energy and environment sector (10%) is gaining prominence, with rising adoption in carbon capture, biogas purification, and hydrogen energy applications. Collectively, these segments highlight both the scale and diversification of opportunities shaping the future of the membrane separation materials market.

Membrane Separation Materials Market – Country Analysis

China: Regulatory Compliance Driving Membrane Adoption

China’s membrane separation materials market is heavily influenced by strict environmental regulations and industrial growth. The Ministry of Ecology and Environment (MEE) enforces stringent wastewater discharge norms, encouraging industries to adopt advanced membrane filtration systems to meet emission standards. In 2024, Chinese researchers developed a new hollow-fiber ultrafiltration (UF) membrane with enhanced antifouling properties, improving efficiency and reducing maintenance costs for membrane bioreactors (MBRs). Key applications include the textile sector, where membrane-based recycling systems recover over 95% of process water from dyeing effluents with high total dissolved solids (TDS), effectively treated by ultra-high-pressure reverse osmosis membranes. Additionally, government investments under the 14th Five-Year Plan to expand natural gas production are driving the demand for nanofiltration membranes in the oil and gas sector.

United States: Government Support and Technological Innovation

The U.S. membrane separation materials market benefits from significant government funding and strong R&D initiatives. The Bipartisan Infrastructure Law allocates over $50 billion to the EPA for upgrading water infrastructure, specifically targeting emerging contaminants like PFAS that require advanced membrane materials. NSF-funded research centers are developing innovative membranes for water purification, chemical separations, and biopharmaceutical processing, boosting technological advancements in the sector. Corporate initiatives by DuPont Water Solutions and The Chemours Company are pioneering perfluorinated ion exchange membranes for chemical processing and the growing green hydrogen market. Moreover, in September 2023, Membrane Technology and Research, Inc. inaugurated the world’s largest membrane-based carbon capture plant in Gillette, Wyoming, showcasing a significant application of gas separation membranes.

India: Rural Water Initiatives and Infrastructure Investments

India’s membrane separation materials market is driven by government-led initiatives and infrastructure projects. The “Jal Jeevan Mission” promotes the adoption of advanced filtration technologies in rural areas, supported by the Department of Science & Technology’s Water Technology Initiative. Infrastructure investment is highlighted by the Ghaziabad Nagar Nigam’s issuance of India’s first Certified Green Municipal Bond, raising ₹150 crore for a Tertiary Sewage Treatment Plant (TSTP) that employs advanced membrane filtration materials for industrial wastewater reuse. Beyond municipal treatment, VA TECH WABAG’s seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant in Chennai, valued at INR 415 crores, underscores the growing financial commitment to membrane-based infrastructure. Indian researchers are also developing cost-effective chlorine disinfection methods that integrate with membrane systems, enhancing potable water treatment capabilities.

Germany: Industrial Leadership and Advanced Ceramic Membranes

Germany is a leader in membrane separation materials for industrial wastewater and water reuse. PWT Wassertechnik specializes in a wide range of membrane processes that ensure strict compliance with European environmental regulations. In 2024, Cerafiltec partnered to construct a large-scale ceramic membrane bioreactor (MBR), signaling a shift toward durable, high-performance membrane materials. Companies like MANN+HUMMEL are developing innovative membrane and digital solutions addressing global water challenges, including applications in industrial processes and green energy. These technological and corporate initiatives position Germany at the forefront of membrane separation materials innovation.

Japan: Academic Innovation and Global Technology Leadership

Japan’s market for membrane separation materials is driven by cutting-edge research and international project involvement. The Membrane Engineering Group at Kobe University is developing novel functional membranes, including biomimetic and highly porous designs. Toray Industries continues to lead in high-performance RO membranes for large-scale desalination projects, including those in Saudi Arabia, where membrane separation materials are critical for achieving ultra-pure water quality. Strategic investments by Asahi Kasei in emerging membrane technology companies highlight Japan’s focus on clean energy applications, particularly for the hydrogen economy, reinforcing the country’s role as a global technology provider.

Australia: Water Recycling and Research-Driven Solutions

Australia faces significant water stress, positioning it as a leader in water recycling and reuse. Facilities like the Sydney Water Wollongong Water Resource Recovery Facility employ a combination of microfiltration and reverse osmosis membranes to treat wastewater for irrigation and other industrial applications. Academic research at the Institute for Sustainable Industries and Liveable Cities (ISILC) at Victoria University focuses on enhancing desalination recovery rates and minimizing membrane fouling and scaling, addressing critical challenges in the membrane separation materials market. These initiatives reinforce Australia’s commitment to sustainable water management and advanced membrane technology adoption.

Competitive Landscape: Global Leaders Driving Membrane Separation Materials Innovation

The membrane separation materials market is highly competitive, with global leaders leveraging material science expertise, large-scale project execution, and sustainable innovations to strengthen their market share. Companies are pursuing a mix of R&D investments, product launches, acquisitions, and digital integration to deliver customized, high-efficiency solutions.

DuPont Water Solutions: Integrated Portfolio and Industrial Wastewater Leadership

DuPont has positioned itself as a global leader with a comprehensive portfolio that includes reverse osmosis, ultrafiltration, ion exchange, and nanofiltration membranes. Its FilmTec™ Fortilife™ membranes are gaining traction for industrial wastewater reuse, while the LiNE-XD nanofiltration series supports lithium extraction from brines, reinforcing DuPont’s role in the energy transition. Digital tools like WAVE PRO empower engineers to optimize designs, while recognition such as the 2024 Water Technology Company of the Year award underscores its innovation leadership.

SUEZ Water Technologies & Solutions: Scaling Large-Scale Desalination and Circular Economy Projects

Now part of Veolia, SUEZ provides end-to-end water and waste solutions, with membranes central to its desalination and wastewater treatment portfolio. In July 2025, it commissioned China’s largest industrial seawater desalination plant, showcasing its ability to handle large-scale projects. SUEZ also supports circular economy initiatives, such as biogas production from wastewater. With Xavier Girre’s appointment as CEO in June 2025, the company is set to deepen its leadership in sustainable water management.

Toray Industries, Inc.: Material Science and Energy-Efficient Membranes

Toray leverages its polymer science expertise to produce membranes with superior mechanical strength and chemical resistance. Its hollow-fiber ultrafiltration modules offer significant energy savings, especially in food and beverage processing. With strong partnerships in the Middle East, Toray is a key RO supplier for mega desalination projects like Yanbu 4 and Shuaibah 3 IWP. The company’s Water Research Center in India further reinforces its R&D-driven approach.

Koch Separation Solutions (Kovalus): Custom-Engineered Filtration Solutions

Rebranded as Kovalus Separation Solutions, Koch specializes in engineered membrane systems tailored for complex wastewater streams. Its PURON® reinforced hollow-fiber membranes are known for durability and fouling resistance, serving sectors such as food, automotive, and life sciences. With plans to open a new assembly facility in Mexico, Kovalus is expanding production capacity by 50%, ensuring stronger supply chain support for global clients.

Asahi Kasei Corporation: Biopharma Filtration and Green Hydrogen Applications

Asahi Kasei holds a strong presence in life sciences filtration with its Planova™ virus removal filters, essential for biologics manufacturing. Its Microza® hollow-fiber membranes received a Gold EcoVadis rating, reflecting leadership in sustainable manufacturing. In April 2024, it introduced a WFI membrane system as an energy-efficient alternative to distillation. A major ¥35 billion investment is also underway to expand membranes for alkaline water electrolyzers, strengthening the green hydrogen supply chain.

3M Separation and Purification Sciences: Diversified Applications and Biopharma Growth

3M integrates its advanced separation technologies across pharmaceuticals, food & beverage, and industrial manufacturing. In May 2023, it invested $146 million to expand biopharma filtration capacity, ensuring supply for growing biologics demand. With its healthcare business being spun off into a dedicated public company, 3M’s Separation and Purification Sciences Division is positioned to sharpen its focus on healthcare-driven membrane innovation and market leadership.

Membrane Separation Materials Market Report Scope

Membrane Separation Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$23.8 Billion

|

|

Market Size (2034)

|

$61.9 Billion

|

|

Market Growth Rate

|

11.2%

|

|

Segments

|

Type (Polymeric Membranes, Ceramic & Inorganic Membranes, Hybrid & Composite Membranes, Others), Technology (Reverse Osmosis, Nanofiltration, Ultrafiltration, Microfiltration, Other Technologies), Application (Water & Wastewater Treatment, Industrial Processing, Life Sciences & Healthcare, Energy & Environment)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., SUEZ, Veolia, Toray Industries, Inc., Pentair plc, Xylem Inc., Asahi Kasei Corporation, Kubota Corporation, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, LG Chem, Koch Industries, V.A. TECH WABAG Ltd., Merck KGaA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Membrane Separation Materials Market Segmentation

By Type

- Polymeric Membranes

- Ceramic & Inorganic Membranes

- Hybrid & Composite Membranes

- Others

By Technology

- Reverse Osmosis (RO)

- Nanofiltration (NF)

- Ultrafiltration (UF)

- Microfiltration (MF)

- Other Technologies

By Application

- Water & Wastewater Treatment

- Industrial Processing

- Life Sciences & Healthcare

- Energy & Environment

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Membrane Separation Materials Industry include-

- DuPont de Nemours, Inc.

- SUEZ

- Veolia

- Toray Industries, Inc.

- Pentair plc

- Xylem Inc.

- Asahi Kasei Corporation

- Kubota Corporation

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- LG Chem

- Koch Industries

- V.A. TECH WABAG Ltd.

- Merck KGaA

*- List not Exhaustive

Research Coverage

This report investigates the membrane separation materials market, delivering analysis reviews on demand shifts across water, energy, and high-value processing while mapping cost curves and adoption inflection points. It highlights breakthroughs in advanced polymers, ceramics, and hybrid chemistries; mixed-matrix architectures for gas separations; and low-pressure, high-flux sheets that compress energy and cleaning intensity. The study also highlights consolidation moves, digital design enablement, and circular-economy use cases (reuse, resource recovery, biogas upgrading) that are re-shaping supplier playbooks. By translating performance metrics (permeance, selectivity, fouling resistance, chemical/thermal windows) into lifecycle economics and bankable procurement criteria, USDAnalytics positions decision-makers to standardize materials across multi-site portfolios this report is an essential resource for product strategists, sourcing leaders, and investors building resilient separation platforms. Scope Includes-

- Segmentation: By Type (Polymeric Membranes; Ceramic & Inorganic Membranes; Hybrid & Composite Membranes; Others), By Technology (Reverse Osmosis; Nanofiltration; Ultrafiltration; Microfiltration; Other Technologies), By Application (Water & Wastewater Treatment; Industrial Processing; Life Sciences & Healthcare; Energy & Environment)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic 2021–2024; Forecast 2025–2034.

- Companies: Profiles of 15+ companies

Methodology

We apply a mixed-methods framework combining primary interviews (OEMs, material scientists, EPCs, utilities/industrial operators, QA/RA) with secondary intelligence (standards, patents, technical literature, filings). Market sizes are triangulated top-down from end-use capacity additions (desalination, reuse, semiconductor/biopharma, gas processing) and bottom-up via bill-of-materials models by material family (polymeric, ceramic, hybrid), normalized for flux (LMH), selectivity, TMP, fouling/cleaning cadence, and replacement intervals. Forecasts incorporate learning rates, electricity/chemicals sensitivity, regulatory cadence (discharge/reuse, carbon), and scenario envelopes for MMM penetration and ceramic price declines. Competitor benchmarks assess durability envelopes, permeability–selectivity trade-offs, anti-fouling performance, and cost per 1,000 m³ (liquids) / cost per Nm³ (gases). Outputs undergo cross-validation with commissioning data, supplier guidance, and announced capacity/mergers.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Membrane Separation Materials Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Membrane Separation Materials Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Insights

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $23.8 Billion

2.2.2. Forecasted Market Size (2034): $61.9 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 11.2%

2.3. Key Trends and Opportunities

2.3.1. Innovation in Advanced Polymeric Membranes

2.3.2. Rising Adoption of Ceramic Membranes

2.3.3. Sustainability and Bio-Based Membranes

2.3.4. Mixed-Matrix Membranes (MMMs) for Gas Separation

2.3.5. Expanding Role in Global Water & Wastewater Treatment

2.3.6. High-Value Applications in Life Sciences and Biopharmaceuticals

2.3.7. Emerging Potential in Energy and Environmental Applications

3. Recent Developments and Strategic Shifts

3.1. Market Trend: Sustainability and Project Milestones

3.1.1. DuPont Water Solutions Wins BIG Sustainability Award

3.1.2. Toray Industries Supplies Membranes for Saudi Arabia Desalination

3.1.3. SUEZ Commissions China’s Largest Industrial Desalination Plant

3.2. Corporate Strategy: Mergers and Portfolio Shifts

3.2.1. Nanostone and Solecta Merge to Form Acuriant Technologies

3.2.2. LG Chem Divests Water Solutions Business

3.3. Product Innovation and Launches

3.3.1. Veolia Launches Compact TERION™ S System

3.3.2. SUEZ Unveils New High-Performance UF Membranes

3.3.3. Evonik Introduces High-Capacity Biogas Membrane

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Material Science to Integrated Solutions

4.2. Key Competitive Factors

4.2.1. Integrated Water Treatment Portfolios

4.2.2. R&D in New Materials and Digital Tools

4.2.3. Strategic Acquisitions and Partnerships

4.3. Profiles of Top Players

4.3.1. DuPont Water Solutions

4.3.2. SUEZ Water Technologies & Solutions

4.3.3. Toray Industries, Inc.

4.3.4. Koch Separation Solutions (Kovalus)

4.3.5. Asahi Kasei Corporation

4.3.6. 3M Separation and Purification Sciences

5. Membrane Separation Materials Market – Segmentation Insights

5.1. By Type

5.1.1. Polymeric Membranes

5.1.2. Ceramic & Inorganic Membranes

5.1.3. Hybrid & Composite Membranes

5.1.4. Others

5.2. By Technology

5.2.1. Reverse Osmosis (RO)

5.2.2. Nanofiltration (NF)

5.2.3. Ultrafiltration (UF)

5.2.4. Microfiltration (MF)

5.2.5. Other Technologies

5.3. By Application

5.3.1. Water & Wastewater Treatment

5.3.2. Industrial Processing

5.3.3. Life Sciences & Healthcare

5.3.4. Energy & Environment

6. Country Analysis and Outlook: Membrane Separation Materials Market

6.1. China: Regulatory Compliance and Industrial Growth

6.2. United States: Government Support and Technological Innovation

6.3. India: Rural Water Initiatives and Infrastructure Investments

6.4. Germany: Industrial Leadership and Advanced Ceramic Membranes

6.5. Japan: Academic Innovation and Global Technology Leadership

6.6. Australia: Water Recycling and Research-Driven Solutions

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Membrane Separation Materials Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Technology

7.1.3. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Technology

7.2.3. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Technology

7.3.3. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Technology

7.4.3. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Technology

7.5.3. By Application

8. Company Profiles: Additional Leading Players

8.1. DuPont de Nemours, Inc.

8.2. SUEZ

8.3. Veolia

8.4. Toray Industries, Inc.

8.5. Pentair plc

8.6. Xylem Inc.

8.7. Asahi Kasei Corporation

8.8. Kubota Corporation

8.9. The Dow Chemical Company

8.10. MANN+HUMMEL

8.11. Evoqua Water Technologies

8.12. LG Chem

8.13. Koch Industries

8.14. V.A. TECH WABAG Ltd.

8.15. Merck KGaA

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures