Global Ion Exchange Membranes Market Overview: Growth Driven by Clean Energy, Resource Recovery, and Water Purification

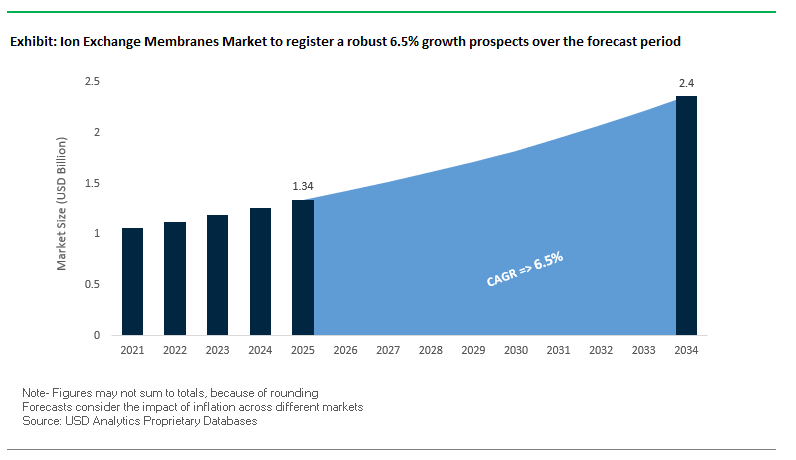

The global ion exchange membranes market is projected to expand from USD 1.34 billion in 2025 to USD 2.4 billion by 2034, achieving a CAGR of 6.5%. This steady growth is driven by the rising adoption of electrochemical technologies, the acceleration of the hydrogen economy, and the increasing demand for advanced water purification and resource recovery solutions. For industry Stakeholders, ion exchange membranes are becoming a critical enabler of energy transition and sustainable industrial practices. Their role in green hydrogen production, desalination, wastewater reuse, and recovery of valuable resources such as lithium positions them as a cornerstone of the circular economy. At the same time, innovations in polymer science are extending membrane durability and performance, ensuring efficiency even under harsh operating conditions.

Key Insights for Stakeholders

- Electrochemical Adoption: Growing use of electrodialysis and diffusion dialysis in industries for wastewater treatment and brine concentration.

- Hydrogen Economy Push: Proton exchange membranes (PEMs) are indispensable in electrolyzers for green hydrogen generation.

- Resource Recovery: Ion exchange membranes are increasingly applied in lithium extraction and valuable metal recovery from industrial brines.

- Water Scarcity Solutions: Effective in desalination and PFAS removal, helping address global drinking water challenges.

- Materials Innovation: New advanced polymers and composite membranes with superior ion selectivity and chemical resistance are extending lifespan and lowering costs.

Market Analysis: Recent Developments in the Ion Exchange Membranes Industry

The ion exchange membranes industry has seen rapid advancements in 2024 and 2025, with companies aligning innovations to the green energy transition and circular economy goals. In May 2025, an EU-funded consortium led by a major chemicals company began scaling up a pioneering green hydrogen project, leveraging ion exchange membranes to boost electrolysis efficiency. Shortly after, in June 2025, AGC launched its new FORBLUE™ SELEMION series, featuring grafted polymerization technology to deliver membranes with lower resistance and improved durability, specifically for electrodialysis, diffusion dialysis, and electrolysis.

By July 2025, LANXESS highlighted its Lewatit® ion exchange resins at the International Sugar Expo in New Delhi, emphasizing their role in sugar decolorization and cost-efficient purification. That same month, Nouryon partnered with India’s Central Road Research Institute to host the International Conference on Bitumen Emulsion (ICBE), showcasing its focus on infrastructure and sustainable road construction. In August 2025, DuPont received recognition when its AmberLite™ P2X110 resin, designed for PEM electrolyzers, won the 2024 Sustainability Product of the Year award, confirming its impact on clean hydrogen production.

PFAS removal also emerged as a critical application in August 2025, when a new mobile water treatment unit in Belgium equipped with LANXESS’s Lewatit TP 108 DW resin began purifying up to 190,000 liters per hour, addressing one of the most pressing drinking water challenges. Strategic leadership changes shaped the landscape as well, with SUEZ appointing Xavier Girre as CEO in August 2025, reinforcing its global water management ambitions. Looking back, in September 2024, Nouryon expanded its sodium chlorate capacity in Brazil to meet pulp and paper demand, showcasing the role of ion exchange technologies across diverse industries. Collectively, these developments highlight a market that is simultaneously advancing water treatment efficiency, enabling clean energy, and supporting global industrial transformation.

Key Market Trends Reshaping the Ion Exchange Membranes Industry

The Ion Exchange Membranes (IEM) market is rapidly evolving due to stricter regulations, material innovation, and the accelerating shift toward sustainable energy solutions. One of the most prominent trends is the growing adoption of IEMs in water and wastewater treatment, where they are increasingly used in desalination, PFAS removal, and industrial effluent treatment. The U.S. Environmental Protection Agency (EPA) lists ion exchange membranes among the best available technologies for addressing emerging contaminants, leading to expanded pilot projects and municipal-scale deployments. Material science breakthroughs are another strong trend, as new hydrocarbon-based anion exchange membranes (AEMs) demonstrate enhanced ion conductivity and chemical stability at lower cost compared to perfluorinated materials. Studies published in ACS Applied Materials & Interfaces confirm a shift toward durable, eco-friendly hydrocarbon membranes, driving wider commercialization in cost-sensitive applications. Beyond water, the hydrogen economy is redefining the IEM landscape, as they are integral to electrochemical technologies like proton exchange membrane (PEM) fuel cells, electrolyzers, and redox flow batteries. Companies are investing heavily in advanced membranes capable of withstanding higher current densities and temperatures, which can improve green hydrogen efficiency while lowering costs. Finally, industrial separations are becoming an important growth avenue, with IEMs enabling selective recovery of chemicals, acids, and biologics. For instance, specialty chemical producers have reported up to 49% capacity improvements in chlor-alkali production through advanced brine purification membranes, showcasing how optimization of existing applications continues to deliver both cost savings and sustainability benefits.

Emerging Opportunities Unlocking Market Growth Potential

The opportunities in the ion exchange membranes market are expanding beyond traditional chlor-alkali processes into high-growth sectors such as clean energy, water security, and industrial recovery. A major opportunity lies in hydrogen and energy applications, where IEMs serve as the backbone of water electrolyzers for green hydrogen production, PEM fuel cells for transportation, and flow batteries for grid-scale storage. With governments investing billions into decarbonization initiatives, demand for durable and cost-effective membranes is set to surge. Another opportunity is in advanced wastewater and drinking water purification, particularly in addressing hard-to-remove contaminants like PFAS, nitrates, and heavy metals. With municipalities under pressure to meet new federal and state regulations, adoption of ion exchange membranes in large-scale water projects is accelerating. Emerging prospects in food and biopharmaceutical processing also present untapped potential, as IEMs enable precision separation of proteins, salts, and acids without introducing harmful chemicals. This aligns with the rising demand for clean-label products and high-purity compounds. Additionally, chemical processing industries are exploring bipolar membranes (BPMs) for eco-efficient acid and base generation from saline waste streams, reducing both chemical consumption and environmental footprint. These opportunities position ion exchange membranes as a cross-industry enabler, with applications spanning from clean energy to resource recovery and high-purity manufacturing.

Market Share Analysis of the Ion Exchange Membranes Market

Market Share by Material

By 2025, hydrocarbon-based ion exchange membranes are expected to hold the largest share at approximately 45%, reflecting their balance of cost-effectiveness, mechanical durability, and versatility in electrodialysis for water treatment and food processing. Partially or fully fluorinated membranes, such as PFSA-based Nafion™, are projected at 35% share, continuing to dominate in high-performance applications like proton exchange membrane (PEM) fuel cells and electrolyzers due to their unmatched stability and conductivity, despite high costs. Anion Exchange Membranes (AEMs), projected to capture 12% of the market, represent the fastest-growing material class, driven by their ability to operate in alkaline environments and support low-cost catalyst systems, thereby reducing the overall cost of fuel cells and electrolyzers. Composite and hybrid membranes, at 8% share, are gaining adoption in applications requiring tailored performance, including enhanced thermal and chemical stability. Together, this segmentation highlights a dual trend: hydrocarbons driving cost-sensitive adoption, while fluorinated and emerging AEMs power high-value energy applications.

Market Share by Function

The ion exchange membranes market by function will remain led by cation exchange membranes (CEMs), expected to capture 55% share in 2025. Their established role in electrodialysis, proton transport, and electrolysis processes secures their dominance across industries. Anion exchange membranes (AEMs), projected at 35%, are rapidly gaining ground, fueled by advances in material stability and their role in alkaline fuel cells and water electrolyzers, which enable reduced reliance on costly precious-metal catalysts. Bipolar membranes (BPMs), with 10% market share, represent a small but strategically important niche, as they enable innovative chemical conversions such as splitting salt streams into valuable acids and bases without the need for external chemical input. This growing demand for eco-efficient processes in chemical industries positions BPMs as a future growth lever, even if their market size remains relatively modest compared to CEMs and AEMs.

Market Share by Application

Application-wise, electrodialysis and electrodialysis reversal (ED/EDR) are projected to lead the market with 40% share by 2025, cementing their role as the workhorse technologies for desalination, brackish water treatment, and food & beverage processing. Fuel cells are expected to account for 20%, driven by surging demand for clean transportation and stationary energy solutions as nations accelerate hydrogen adoption. Electrolysis applications, projected at 18%, will see explosive growth due to their central role in producing green hydrogen, with ion exchange membranes serving as the critical enabler of efficient electrochemical splitting of water. Battery separators and flow batteries, at 15%, reflect the growing importance of grid-scale renewable energy storage, where ion exchange membranes enhance durability and reduce cross-contamination between electrolytes. The remaining 7% share is held by diffusion dialysis and other specialized separations, including acid recovery and pharmaceutical purification. Collectively, this distribution underscores how the market is diversifying rapidly, with traditional water desalination maintaining leadership but energy-related applications emerging as the fastest-growth engines.

market Share by Application, 2025.png)

China: Regulatory Compliance and Hydrogen Fuel Cell Expansion Driving Market Growth

China’s ion exchange membranes market is strongly influenced by strict environmental regulations, technological advancements, and emerging energy applications. The Ministry of Ecology and Environment (MEE) enforces stringent industrial wastewater discharge standards, compelling manufacturers to adopt advanced ion exchange membranes to comply with emission limits. In 2024, Chinese researchers introduced a hollow-fiber ultrafiltration (UF) membrane with superior antifouling properties, addressing a major challenge in industrial wastewater treatment and improving membrane bioreactor (MBR) efficiency while reducing maintenance costs. Furthermore, the nation’s rapidly expanding hydrogen fuel cell sector is a key driver for ion exchange membrane adoption. Chinese companies are investing in ultra-thin reinforced proton exchange membranes to enhance power density in fuel cell stacks, supporting applications in stationary energy storage and automotive markets. These combined regulatory, technological, and energy-driven initiatives position China as a critical growth hub for ion exchange membrane technologies.

Saudi Arabia: Strategic Desalination Investments and Ion Exchange Integration

Saudi Arabia continues to strengthen its ion exchange membranes market through extensive investments in desalination infrastructure and advanced membrane technologies. The Saudi Water Partnership Company (SWPC) leads new desalination projects heavily reliant on reverse osmosis (RO), where ion exchange membranes play a critical pre-treatment role to prevent scaling and enhance operational efficiency. Companies like Ion Exchange are actively delivering advanced membrane bioreactor (MBR) systems, often integrated with ion exchange technology, to support wastewater management and water reuse initiatives. The Kingdom’s Saline Water Conversion Corporation (SWCC) is pioneering energy-efficient RO membranes, exemplified in projects such as Jubail 3A, where ion exchange is integral to maximizing membrane longevity and overall performance. Saudi Arabia’s strategic focus on membrane-based water solutions highlights the growing adoption of ion exchange membranes in large-scale industrial and municipal applications.

United States: Government Support and Advanced Research Driving Adoption

The United States ion exchange membranes market is supported by significant government funding, cutting-edge academic research, and private-sector innovation. The Bipartisan Infrastructure Law allocates over $50 billion to the Environmental Protection Agency (EPA) for modernizing water infrastructure, with a focus on emerging contaminants like PFAS, which require advanced ion exchange filtration solutions. Research centers funded by the National Science Foundation (NSF), including the Membrane Applications Science and Technology (MAST) Center, focus on developing next-generation membranes for water purification, chemical separations, and biopharmaceutical processes. Corporations such as DuPont Water Solutions and Chemours are advancing perfluorinated ion exchange membranes for industrial applications and the expanding green hydrogen market. This combination of public funding, academic innovation, and corporate initiatives underscores the U.S. as a leading market for high-performance ion exchange membrane technologies.

India: Government Programs and Technological Investments Expanding Market Presence

India’s adoption of ion exchange membranes is accelerated by government initiatives, infrastructure investments, and advanced manufacturing capabilities. The Jal Jeevan Mission and the Department of Science & Technology's Water Technology Initiative drive the implementation of nano-material and filtration technologies to provide safe and affordable drinking water in rural regions. In August 2024, VA TECH WABAG secured a seven-year O&M contract for the 110 MLD SWRO Nemmeli Desalination Plant in Chennai, valued at approximately INR 415 crores, highlighting substantial investments in membrane-based water infrastructure. Additionally, Ion Exchange (India) operates a state-of-the-art membrane manufacturing unit in Verna, Goa, producing HYDRAMEM-branded membranes to expand domestic market share and export capacity. India’s strategic focus on government-backed programs and local manufacturing underscores its growing significance in the global ion exchange membranes market.

Japan: Innovation and Strategic Collaborations in Clean Energy and Water Treatment

Japan remains a key player in ion exchange membrane innovation through academic research, corporate development, and strategic collaborations. Toray Industries continues to develop high-performance RO membranes for desalination projects, including large-scale implementations in Saudi Arabia, reinforcing Japan’s role as a global technology provider. Fujifilm maintains a diverse portfolio of ion exchange membranes applied across drinking water, pharmaceutical, food processing, and wastewater treatment sectors, reflecting a broad technological focus. Additionally, Asahi Kasei’s investments in next-generation ion exchange membrane companies for hydrogen energy applications demonstrate a strategic orientation toward clean energy markets, enhancing Japan’s global influence in advanced membrane technologies.

Germany: Industrial Wastewater Applications and Hydrogen Economy Expansion

Germany’s ion exchange membranes market is driven by industrial wastewater treatment expertise, technological innovation, and participation in the hydrogen economy. Companies such as PWT Wassertechnik specialize in advanced membrane solutions, including ion exchange, to treat and recycle industrial water while meeting stringent European environmental standards. German firms are also scaling anion exchange membranes for modular electrolyzers, exemplified by Enapter, targeting PFAS-free membranes in the green hydrogen sector. Multinational companies like MANN+HUMMEL are innovating in membrane and digital solutions to address water challenges and industrial process optimization. Germany’s integrated approach to industrial applications and renewable energy positions it as a leading market for high-performance ion exchange membranes.

Competitive Landscape – Leading Companies Driving the Ion Exchange Membranes Market

The competitive landscape of the ion exchange membranes market is shaped by global leaders who are combining technical innovation with strategic expansion. Companies such as DuPont, LANXESS, SUEZ, Asahi Kasei, and AGC are investing in sustainability, digital tools, and materials science advancements to strengthen their market positions. Their offerings range from green hydrogen solutions to PFAS removal technologies, reflecting the breadth of ion exchange membrane applications across industries.

DuPont Water Solutions – Sustainability Leadership with Hydrogen and Lithium Innovations

DuPont remains at the forefront of the ion exchange membranes market with a clear focus on solving water and energy challenges. Its AmberLite™ P2X110 resin, designed for green hydrogen electrolyzers, recently earned the 2024 Sustainability Product of the Year award, highlighting its impact on clean energy. Beyond hydrogen, DuPont’s FilmTec™ LiNE-XD nanofiltration membranes were finalists for the 2024 Edison Awards, underscoring their role in lithium recovery. Complementing its product leadership, the WAVE digital design software allows engineers to model and optimize treatment systems, integrating ion exchange membranes into broader solutions that enhance operational efficiency.

LANXESS AG – Strength in Industrial Purification and Rapid PFAS Solutions

LANXESS’s Lewatit® ion exchange resins are widely applied in water treatment, food processing, and industrial purification. Its Lewatit® S series is certified for food and beverage use, playing a vital role in sugar demineralization and decolorization. In August 2025, the company partnered with De Watergroep in Belgium, deploying a mobile unit with Lewatit TP 108 DW resin to remove PFAS from drinking water at a large scale, showcasing its ability to rapidly respond to environmental challenges. With operations in 32 countries, LANXESS combines global reach with specialized solutions, making it a trusted name in purification technologies.

SUEZ Water Technologies & Solutions – Digitalized and Integrated Water Management Leader

SUEZ leverages ion exchange membranes as part of its integrated approach to municipal and industrial water treatment. The company emphasizes digitalization, providing tools for remote monitoring and operational optimization, which are increasingly critical for large-scale infrastructure projects. It has a strong track record in public-private partnerships, such as its urban water distribution contract in Kochi City, India. With Xavier Girre appointed CEO in August 2025, SUEZ is strengthening its leadership focus on sustainability, circular economy initiatives, and global water innovation.

Asahi Kasei Corporation – Specialized Biopharmaceutical and Life Science Membranes

Asahi Kasei applies ion exchange and membrane technology primarily in biopharmaceutical filtration, with its Planova™ virus removal filters serving as a benchmark in sterile drug manufacturing. In 2025, the company completed its third Planova™ filter assembly plant in Japan, scaling production to meet surging global demand in healthcare. Its “Trailblaze Together” management plan reflects a shift toward higher-value, innovation-driven products, while its inclusion in global ESG indices underscores its commitment to sustainability. By focusing on critical pharmaceutical and life science applications, Asahi Kasei has secured a strong niche in the ion exchange membrane space.

AGC Chemicals – Energy-Efficient Fluorinated Ion Exchange Membranes

AGC is a key player with its FORBLUE™ FLEMION™ membranes, renowned for high chemical stability and extensive use in chlor-alkali electrolysis. In June 2025, AGC expanded its portfolio with the FORBLUE™ SELEMION series, offering durable membranes for electrodialysis, diffusion dialysis, and acid recovery. The company emphasizes energy efficiency, with its F-9060 grade membranes engineered for low electrical resistance, helping industries reduce power costs. AGC further supports customers with technical services such as brine and membrane analysis, ensuring long-term stable performance of its systems in demanding industrial environments.

Ion Exchange Membranes Market Report Scope

Ion Exchange Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.34 Billion

|

|

Market Size (2034)

|

$2.4 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

Material (Hydrocarbon-based Membranes, Partially/Halogenated Membranes, Composite/Hybrid Membranes, Anion Exchange Membranes), Function (Cation Exchange Membranes, Anion Exchange Membranes, Bipolar Membranes), Structure (Homogeneous Membranes, Heterogeneous Membranes, Interpolymer Membranes, Supported Membranes), Application (Electrodialysis, Electrodialysis Reversal, Electrolysis, Fuel Cells, Battery Separators & Flow Batteries, Diffusion Dialysis, Others), End-User (Energy & Power, Chemical Processing, Water & Wastewater Treatment, Food & Beverage, Healthcare & Pharmaceuticals, Electronics & Semiconductors, Other Industries)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SUEZ, DuPont de Nemours, Inc., Veolia, Toray Industries, Inc., Asahi Kasei Corporation, The Dow Chemical Company, Kuraray Co., Ltd., LG Chem, SOLVAY, LANXESS, PENTAIR, Ion Exchange (India) Ltd., FUJIFILM Corporation, W. L. Gore & Associates, Inc., Mitsubishi Chemical Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ion Exchange Membranes Market Segmentation

By Material

- Hydrocarbon-based Membranes

- PFSA

- SPEEK

- SPSF

- PBI

- Partially/Halogenated Membranes

- Composite/Hybrid Membranes

- Anion Exchange Membranes (AEM)

By Function

- Cation Exchange Membranes (CEM)

- Anion Exchange Membranes (AEM)

- Bipolar Membranes (BPM)

By Structure

- Homogeneous Membranes

- Heterogeneous Membranes

- Interpolymer Membranes

- Supported Membranes

By Application

- Electrodialysis (ED/EDR)

- Electrodialysis Reversal (EDR)

- Electrolysis

- Fuel Cells

- Battery Separators & Flow Batteries

- Diffusion Dialysis

- Others

By End-User

- Energy & Power

- Chemical Processing

- Water & Wastewater Treatment

- Food & Beverage

- Healthcare & Pharmaceuticals

- Electronics & Semiconductors

- Other Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Ion Exchange Membranes Industry include-

- SUEZ

- DuPont de Nemours, Inc.

- Veolia

- Toray Industries, Inc.

- Asahi Kasei Corporation

- The Dow Chemical Company

- Kuraray Co., Ltd.

- LG Chem

- SOLVAY

- LANXESS

- PENTAIR

- Ion Exchange (India) Ltd.

- FUJIFILM Corporation

- W. L. Gore & Associates, Inc.

- Mitsubishi Chemical Corporation

*- List not Exhaustive

Research Coverage

This report investigates the global ion exchange membranes market, delivering rigorous analysis reviews of demand drivers across clean energy, resource recovery, and advanced water purification. It highlights 2024–2025 breakthroughs in polymer architectures (hydrocarbon AEMs, reinforced PEMs, composite/hybrid stacks), operational durability at higher current densities, and emerging use-cases spanning PFAS removal, lithium recovery, and electrochemical manufacturing. The study maps competitive moves, technology roadmaps for ED/EDR, electrolysis, fuel cells, and flow batteries, and quantifies how hydrogen-economy buildouts and circular-economy mandates are reshaping procurement and total cost of ownership. With country-level policy lenses, capex signals, and end-user adoption curves, this report is an essential resource for product strategists, procurement leaders, and investors aligning materials choices to reliability, efficiency, and lifecycle compliance. Developed by USDAnalytics, it integrates technology benchmarking with outcome-oriented decision frameworks to convert technical performance into commercial advantage. Scope Includes-

- Segmentation: By Material (Hydrocarbon-based, PFSA, SPEEK, SPSF, PBI, Partially/Halogenated, Composite/Hybrid, AEM), By Function (CEM, AEM, BPM), By Structure (Homogeneous, Heterogeneous, Interpolymer, Supported), By Application (ED/EDR, Electrolysis, Fuel Cells, Battery Separators & Flow Batteries, Diffusion Dialysis, Others), By End-User (Energy & Power, Chemical Processing, Water & Wastewater, Food & Beverage, Healthcare & Pharmaceuticals, Electronics & Semiconductors, Other Industries)

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024; forecasts 2025–2034.

- Companies: Profiles of 15+ companies like SUEZ, DuPont, Veolia, Toray, Asahi Kasei, Dow, Kuraray, LG Chem, Solvay, LANXESS, Pentair, Ion Exchange (India), Fujifilm, W. L. Gore, Mitsubishi Chemical

Methodology

We employ a mixed-methods approach combining primary interviews (membrane manufacturers, EPCs, electrolyzer OEMs, water utilities, and end-users) with secondary intelligence (standards, filings, patents, technical papers). Market sizing uses top-down triangulation (end-use capex/outlay, installed base, retrofit cycles) and bottom-up bill-of-materials for ED/EDR, PEM/AEM electrolysis, fuel cells, and storage. Forecasts apply technology learning curves, yield-loss models, and sensitivity to electricity prices, brine chemistry, and contaminant profiles. Competitor benchmarking integrates performance metrics (IEC, ASR, selectivity, chemical stability), cleaning intervals, and stack-level LCOE/LCOH effects. Country models reflect policy cadence, procurement modes, and infrastructure readiness. All outputs pass cross-validation, scenario stress-tests, and consistency checks against historical adoption and announced capacity additions.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Ion Exchange Membranes Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Stakeholders

1.3. Global Market Snapshot

2. Ion Exchange Membranes Market Outlook (2025–2034)

2.1. Introduction: Growth Drivers and Industry Transformation

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $1.34 Billion

2.2.2. Forecasted Market Size (2034): $2.4 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 6.5%

2.3. Key Market Trends Reshaping the Industry

2.3.1. Growing Adoption in Water and Wastewater Treatment

2.3.2. Material Science Breakthroughs

2.3.3. Impact of the Hydrogen Economy

2.3.4. Industrial Separations and Chemical Recovery

2.4. Emerging Opportunities Unlocking Market Growth Potential

3. Recent Developments and Strategic Shifts

3.1. Market Trend: Clean Energy and Sustainability

3.1.1. EU-Funded Green Hydrogen Project

3.1.2. DuPont's Sustainability Product of the Year Award

3.2. Market Trend: Product Innovation and Portfolio Expansion

3.2.1. AGC's FORBLUE™ SELEMION Series Launch

3.2.2. LANXESS's Application in PFAS Removal

3.2.3. Nouryon's Strategic Expansion in Brazil

3.3. Market Opportunity: Strategic Collaborations and Leadership

3.3.1. LANXESS at the International Sugar Expo in New Delhi

3.3.2. SUEZ Appoints New CEO, Xavier Girre

4. Competitive Landscape: Leading Companies

4.1. Market Overview: From Technical Specialists to Integrated Solutions

4.2. Key Competitive Factors

4.2.1. Technical Innovation and R&D Investment

4.2.2. Application Expertise and Product Portfolio

4.2.3. Global Presence and Strategic Partnerships

4.3. Profiles of Top Players

4.3.1. DuPont Water Solutions

4.3.2. LANXESS AG

4.3.3. SUEZ Water Technologies & Solutions

4.3.4. Asahi Kasei Corporation

4.3.5. AGC Chemicals

5. Ion Exchange Membranes Market – Segmentation Insights

5.1. By Material

5.1.1. Hydrocarbon-based Membranes

5.1.2. Partially/Halogenated Membranes

5.1.3. Anion Exchange Membranes (AEM)

5.1.4. Composite/Hybrid Membranes

5.2. By Function

5.2.1. Cation Exchange Membranes (CEM)

5.2.2. Anion Exchange Membranes (AEM)

5.2.3. Bipolar Membranes (BPM)

5.3. By Application

5.3.1. Electrodialysis (ED/EDR)

5.3.2. Fuel Cells

5.3.3. Electrolysis

5.3.4. Battery Separators & Flow Batteries

5.3.5. Diffusion Dialysis & Other Specialized Separations

6. Country Analysis and Outlook: Ion Exchange Membranes Market

6.1. China: Regulatory Compliance and Hydrogen Fuel Cell Expansion

6.2. Saudi Arabia: Strategic Desalination Investments

6.3. United States: Government Support and Advanced Research

6.4. India: Government Programs and Technological Investments

6.5. Japan: Innovation and Strategic Collaborations

6.6. Germany: Industrial Wastewater Applications and Hydrogen Economy

6.7. Other Key Countries

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, Australia, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Ion Exchange Membranes Market Size Outlook by Region (2025-2034)

7.1. North America Ion Exchange Membranes Market Size Outlook to 2034

7.1.1. By Material

7.1.2. By Function

7.1.3. By Application

7.2. Europe Ion Exchange Membranes Market Size Outlook to 2034

7.2.1. By Material

7.2.2. By Function

7.2.3. By Application

7.3. Asia Pacific Ion Exchange Membranes Market Size Outlook to 2034

7.3.1. By Material

7.3.2. By Function

7.3.3. By Application

7.4. South America Ion Exchange Membranes Market Size Outlook to 2034

7.4.1. By Material

7.4.2. By Function

7.4.3. By Application

7.5. Middle East and Africa Ion Exchange Membranes Market Size Outlook to 2034

7.5.1. By Material

7.5.2. By Function

7.5.3. By Application

8. Company Profiles: Additional Leading Players

8.1. SUEZ

8.2. DuPont de Nemours, Inc.

8.3. Veolia

8.4. Toray Industries, Inc.

8.5. Asahi Kasei Corporation

8.6. The Dow Chemical Company

8.7. Kuraray Co., Ltd.

8.8. LG Chem

8.9. SOLVAY

8.10. LANXESS

8.11. PENTAIR

8.12. Ion Exchange (India) Ltd.

8.13. FUJIFILM Corporation

8.14. W. L. Gore & Associates, Inc.

8.15. Mitsubishi Chemical Corporation

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures