Hybrid Membrane Systems Market Outlook with 2025–2034 Growth Projections

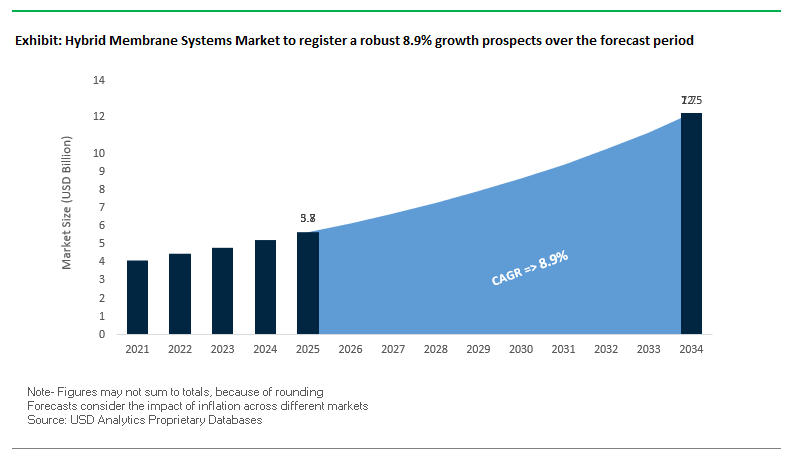

The global hybrid membrane systems market is projected to reach $5.8 billion in 2025 and further expand to $12.5 billion by 2034, registering a CAGR of 8.9%. This growth is driven by rising demand for sustainable water treatment technologies, increasing industrial adoption, and global focus on energy-efficient separation processes.

Hybrid membrane systems combine multiple filtration methods such as reverse osmosis (RO), ultrafiltration (UF), and nanofiltration (NF), ensuring high efficiency and cost-effectiveness. With applications ranging from desalination to biopharmaceutical processing, the market is strategically positioned to address the challenges of water scarcity, industrial discharge compliance, and ESG-driven sustainability goals.

Key Insights for Industry Stakeholders

- Asia-Pacific Dominance: China and India led the membranes market in 2024, propelled by rapid industrialization and stricter wastewater discharge regulations.

- Polymeric Membrane Leadership: Polymeric membranes retained dominance due to cost-effectiveness and wide compatibility, especially in RO, UF, and NF systems.

- End-Use Strength: Water and wastewater treatment accounted for the largest market share in 2024, with high penetration across municipal and industrial sectors.

- Technology Preference: RO and FO collectively held the largest share among filtration methods in 2024, underlining their critical role in desalination and advanced purification.

Market Analysis: Recent Developments in Hybrid Membrane Systems

The hybrid membrane systems industry has experienced an influx of strategic collaborations, innovations in high-performance membranes, and sustainability-driven investments. Between mid-2024 and 2025, multiple landmark developments reshaped the competitive and technological outlook.

In June 2025, Kurita Water Industries was listed on the Nature Stock Index (NAI), strengthening its ESG credentials and reflecting the global trend of aligning industrial water treatment with sustainable benchmarks. Earlier in January 2025, Toray Industries introduced a high-efficiency membrane module for biopharmaceutical manufacturing, delivering over double the performance of conventional systems by minimizing clogging a key pain point in advanced filtration.

In March 2025, Memsift Innovations partnered with the Murugappa Group to launch the Gosep ultrafiltration membrane, designed to lower operational costs and enhance water treatment efficiency. A few months earlier, in November 2024, Evoqua Water Technologies secured a new patent targeting animal manure wastewater treatment, highlighting diversification of hybrid membranes into niche but critical applications.

The desalination sector has also seen significant momentum. In August 2024, Veolia Water Technologies and Morocco commenced construction of a large-scale desalination facility with an 822,000 m³ daily capacity, powered by renewable energy reinforcing hybrid systems’ role in national-scale water security strategies. Likewise, in June 2024, Dow Water & Process Solutions inaugurated a manufacturing facility for its TEQUATIC™ PLUS fine particle filter, while in September 2024, Dow partnered with Haier to supply FILMTEC™ RO membranes for residential water purification systems, demonstrating growing consumer-side adoption.

Adding to material innovations, October 2024 saw Toray complete its acquisition of Zoltek, integrating carbon-fiber composites into its R&D pipeline for next-generation hybrid membranes. These strategic advancements highlight a market evolving rapidly through both industrial-scale deployments and cutting-edge material science.

Emerging Trends and Growth Opportunities in the Hybrid Membrane Systems Market

Growth of Hybrid MBR Systems for Water Reuse and Reclamation

A defining trend in the hybrid membrane systems market is the rising adoption of hybrid membrane bioreactor (MBR) systems that integrate MBR with nanofiltration (NF) or reverse osmosis (RO). This multi-barrier approach enhances organic contaminant removal and produces reclaimed water that meets stringent urban and industrial reuse standards. According to Frontiers in Membrane Science and Technology, hybrid MBR-RO systems outperform standalone configurations, making them critical for groundwater recharge and circular water economy models. The ability to achieve high-quality effluent for industrial reuse is propelling market demand globally.

Development of Energy-Efficient Hybrid FO-RO Systems for Desalination

Another major trend is the integration of forward osmosis (FO) with reverse osmosis (RO) to reduce energy consumption and fouling in desalination plants and high-salinity wastewater treatment. FO’s low-pressure, low-fouling characteristics make it an effective pre-treatment step, allowing RO membranes to operate more efficiently and last longer. A report by the U.S. Department of Energy (DOE) highlights an FO-membrane distillation (MD) hybrid project powered by industrial waste heat, which demonstrated over 60% reductions in both energy costs and carbon emissions. These findings position hybrid FO-RO and FO-MD as game-changing technologies for energy-efficient desalination and industrial wastewater reuse.

Rising Adoption in Industrial Wastewater Treatment and On-Site Reuse

Hybrid membrane systems are rapidly gaining traction in industrial wastewater treatment, where conventional single-process systems fall short. Industries such as oil & gas, chemicals, and food & beverage face increasingly stringent discharge regulations and are turning to UF + RO or UF + NF + AOP hybrids to meet compliance while cutting costs. A global case study from a leading water technology provider reported that a sugar refinery adopting a UF + RO hybrid recovered high-quality water for reuse in cooling towers and boilers, significantly lowering freshwater intake and wastewater disposal expenses. This demonstrates that hybrid systems not only meet regulatory mandates but also deliver tangible economic benefits.

Integration with Advanced Oxidation Processes (AOPs) for Micropollutant Removal

A critical growth opportunity lies in the integration of membranes with advanced oxidation processes (AOPs) such as photocatalysis or ozonation. According to a Water Research review, hybrid AOP-membrane systems effectively degrade micropollutants and persistent organic compounds, making downstream filtration more efficient while reducing membrane fouling. This dual treatment strategy is particularly valuable for producing ultrapure water in pharmaceutical, semiconductor, and high-tech applications. As industries face mounting concerns over emerging contaminants, AOP-membrane hybrids are emerging as a next-generation solution for advanced water treatment and reuse.

Market Share Analysis of the Hybrid Membrane Systems Market

Market Share by Type: Membrane-Non-Membrane Systems Lead with 70% Share

By type, membrane-non-membrane hybrid systems dominate the market with 70% projected share in 2025, primarily because they address treatment challenges that membranes alone cannot. These include RO/NF combined with evaporators or crystallizers for Zero Liquid Discharge (ZLD), UF/NF integrated with activated carbon or AOPs for micropollutant removal, and MBR combined with anaerobic digestion for energy recovery. Their dominance reflects the industry’s push toward sustainability, resource recovery, and regulatory compliance. Conversely, membrane-membrane hybrids (30%), such as UF + RO, FO + RO, and NF + ED, play a strategic role in desalination and selective ion recovery, extending membrane lifespan and improving system efficiency.

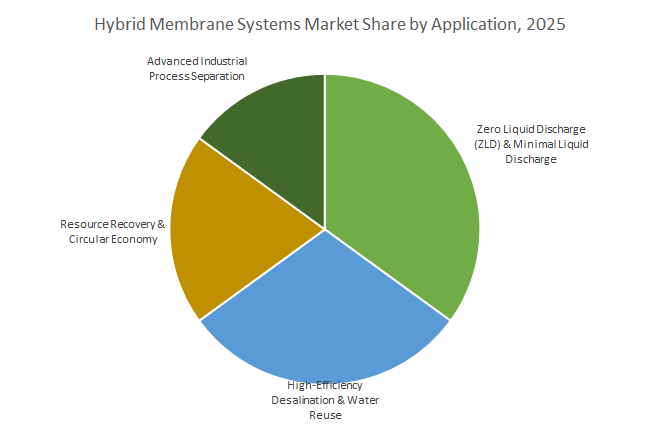

Market Share by Application: ZLD and Minimal Liquid Discharge at the Forefront

In application terms, Zero Liquid Discharge (ZLD) and Minimal Liquid Discharge (MLD) account for 35% share in 2025, making them the largest and fastest-growing segment of the hybrid membrane systems market. This growth is driven by strict environmental mandates in power generation, textiles, and chemicals, where only hybrids (e.g., RO + Crystallizer + CCRO) can achieve complete discharge compliance. High-efficiency desalination and water reuse (30%) remain another key segment, with UF/MF + RO as the global standard and emerging hybrids like FO + RO gaining traction for higher recovery and reduced fouling. Resource recovery (20%) is a rising frontier, with NF + ED hybrids enabling lithium, potassium, and magnesium extraction from brines, transforming wastewater into a revenue-generating stream. Finally, advanced industrial process separations (15%) such as NF + chromatography in food & beverage or hybrids for pharmaceuticals support industries requiring ultra-precise separations beyond the capability of single technologies.

Market Share by System Integration Level: Custom-Engineered Solutions Dominate at 80%

The custom-engineered hybrid systems segment dominates with 80% market share, reflecting the unique and complex nature of wastewater streams and client requirements. Large-scale industrial and municipal projects require tailored engineering to optimize technology integration for compliance, efficiency, and cost control. However, the pre-engineered/packaged hybrid systems segment (20%) is expanding, particularly for standardized use cases like industrial reuse (UF/MF + RO skids) and ZLD applications in upstream oil & gas. These pre-designed units offer faster deployment, lower upfront costs, and repeatable performance, making them increasingly attractive for mid-sized industries with defined water reuse or discharge needs.

United States: Government-Backed Innovations Driving Hybrid Membrane Adoption

The United States stands at the forefront of hybrid membrane system development, propelled by robust government funding and strong R&D initiatives. The U.S. Department of Energy (DOE) actively funds projects that integrate multiple membrane technologies to optimize industrial water reuse. Notably, RTI International is developing a hybrid system that synergistically combines forward osmosis (FO) with membrane distillation (MD) technology, utilizing waste heat to enhance energy efficiency for high-TDS industrial wastewater applications. Complementing these efforts, the National Science Foundation (NSF) supports research centers dedicated to innovating new membranes for water purification, chemical separations, and biopharmaceutical processing.

For instance, the University of California, San Diego has developed a hybrid system combining biodegradable polymer cores with genetically modified cell membranes, showcasing significant advances in biomimetic membrane applications. Corporate participation further accelerates commercialization; Veolia, in collaboration with DOE-funded projects, is demonstrating hybrid FO/MD systems for industrial wastewater, ensuring a direct pipeline from academic research to industrial deployment. This strong government-industry-academia synergy positions the U.S. as a leading market for hybrid membrane systems, particularly in industrial wastewater treatment, water reuse, and advanced biopharmaceutical applications.

China: Regulatory Policies and Industrial Expansion Driving Hybrid Membrane Demand

China’s hybrid membrane systems market is significantly influenced by stringent environmental regulations and rapid industrial expansion. The Ministry of Ecology and Environment (MEE) enforces strict wastewater discharge standards, compelling industrial operators to adopt advanced treatment technologies capable of comprehensive water purification. Hybrid systems, often combining membrane bioreactors (MBR) with reverse osmosis (RO) or nanofiltration (NF), have emerged as critical solutions to achieve zero-liquid discharge (ZLD) objectives, particularly in high-demand sectors such as textiles and petrochemicals. The push for advanced wastewater management aligns with ongoing investments in R&D; a 2024 study highlighted the development of hollow-fiber ultrafiltration (UF) membranes with enhanced antifouling properties. Innovations in individual membrane components directly enhance hybrid system efficiency, improving reliability, recovery rates, and operational longevity. Consequently, regulatory pressure, industrial expansion, and technological innovation collectively drive the robust adoption of hybrid membrane systems across China.

Germany: Technological Leadership in Industrial Hybrid Membrane Systems

Germany maintains a leadership position in hybrid membrane systems through advanced industrial wastewater treatment and continuous technological innovation. A 2025 study confirmed Germany’s nanofiltration membrane segment as the largest in Europe, reflecting strong adoption of hybrid solutions designed for environmental sustainability and efficient water management. Companies like Separionics are pioneering hybrid systems that integrate electro-membranes, such as electrodialysis, with pressure-driven membranes like RO, enabling efficient desalination and industrial water treatment. Separionics’ hybrid RO and electrical sorption system deployed in Tanzania exemplifies Germany’s global reach and technological expertise. Leading corporations such as MANN+HUMMEL focus on delivering innovative membrane and digital solutions tailored to industrial process water management, green energy applications, and hybrid system optimization. Germany’s focus on precision engineering, sustainability, and hybrid configurations underlines its prominent role in the European and global hybrid membrane systems market.

India: Government Programs and Infrastructure Investment Boosting Hybrid Membrane Deployment

India is witnessing accelerated adoption of hybrid membrane systems, driven by government initiatives, infrastructure investment, and corporate participation. Programs such as the "Jal Jeevan Mission" aim to provide safe and affordable drinking water, while the Department of Science & Technology’s Water Technology Initiative supports R&D in nanomaterial-based filtration, which is critical for hybrid systems. Infrastructure investments are also a major driver; for example, Ghaziabad Nagar Nigam issued India’s first Certified Green Municipal Bond, raising ₹150 crore to establish a state-of-the-art Tertiary Sewage Treatment Plant (TSTP). This facility utilizes hybrid membrane filtration systems for wastewater treatment and industrial reuse, highlighting India’s commitment to sustainable water management. Leading Indian companies like Thermax are actively developing hybrid systems for industrial wastewater applications, combining technologies for enhanced water recovery, energy efficiency, and scalability. Collectively, government programs, private sector initiatives, and infrastructure development are catalyzing hybrid membrane system adoption across India.

Japan: Academic and Corporate R&D Accelerating Global Hybrid Membrane Solutions

Japan remains a key technology provider in the global hybrid membrane systems market, driven by cutting-edge academic and corporate research. The Membrane Engineering Group at Kobe University is pioneering functional membranes for water and atmospheric applications, providing a foundation for next-generation hybrid systems. Japanese corporations, particularly Toray Industries, continue to innovate in reverse osmosis (RO) membrane technology, supplying high-performance membranes for large-scale desalination and water purification projects, such as the Saudi Arabia desalination plant. The Ministry of the Environment further supports sustainable infrastructure, allocating USD 1.2 billion in 2024 for wastewater treatment systems integrated with MBR and other hybrid membrane technologies. Japan’s combined emphasis on research, industrial application, and government support solidifies its position as a global leader in hybrid membrane solutions.

Australia: Water Scarcity and Recycling Initiatives Driving Hybrid Membrane Innovation

Australia’s hybrid membrane systems market is strongly influenced by water scarcity, recycling initiatives, and academic research. The Australian Water Recycling Centre of Excellence has funded projects demonstrating the performance and cost benefits of ceramic membranes in treating high-organic secondary effluent, often integrated into hybrid systems for optimal results. Research institutions such as the Institute for Sustainable Industries and Liveable Cities (ISILC) at Victoria University focus on increasing water recovery from desalination and reducing fouling and scaling in membranes, addressing key operational challenges in hybrid configurations. Australia’s focus on sustainable water management, combined with government-backed research and recycling initiatives, fosters the adoption of advanced hybrid membrane systems in municipal, industrial, and agricultural applications.

Competitive Landscape: Leading Players in Hybrid Membrane Systems

The hybrid membrane systems market is characterized by intense competition among multinational corporations, specialized technology providers, and regional innovators. Industry leaders are focusing on R&D investments, large-scale infrastructure projects, ESG-driven strategies, and digital integration to strengthen their global market presence.

Kurita Water Industries Ltd. – Driving ESG-Centered Water Solutions

Kurita Water Industries leverages its heritage in boiler water treatment chemicals and has expanded into advanced water and wastewater treatment facilities. With a strong R&D base in Japan, Kurita delivers ultrapure water production systems and process treatment solutions across industries such as pulp & paper and petrochemicals. Recent expansions in China and Europe, alongside its inclusion in the Nature Stock Index (June 2025), emphasize its ESG-aligned growth strategy and global penetration.

Dow Water & Process Solutions – Expanding Advanced Filtration Leadership

Dow is a leader in materials science-driven water purification technologies, anchored by its DOW FILMTEC™ RO membranes, widely considered an industry standard. Its portfolio spans RO, nanofiltration, ion exchange resins, and advanced technical expertise for system design. In June 2024, Dow launched its TEQUATIC™ PLUS fine particle filter manufacturing facility, boosting capacity to meet industrial demand. Strategic partnerships, such as the Haier collaboration (September 2024), also reflect Dow’s expansion into residential purification solutions.

Evoqua Water Technologies LLC – Innovating Wastewater Treatment Solutions

Evoqua specializes in municipal and industrial water treatment with strong roots in North America and global reach across 170+ facilities. Its two business arms Integrated Solutions & Services and Applied Product Technologies deliver tailored membrane-based solutions. With a history of acquisitions (notably Siemens Water Technologies), Evoqua strengthens its global portfolio. Its November 2024 patent for animal manure wastewater treatment underscores its innovation in addressing challenging wastewater streams.

SUEZ Water Technologies & Solutions – Integrating Digital and Biological Systems

Operating in over 130 countries, SUEZ combines chemical, equipment, and digital solutions to deliver integrated water management. Its portfolio includes advanced technologies like LEAPmbr and ZeeLung. The acquisition of GE Water & Process Technologies has significantly expanded its global footprint. SUEZ’s investment in predictive analytics and data-driven treatment optimization positions it as a leader in integrating digital transformation with hybrid membrane systems.

Veolia Water Technologies – Scaling Global Desalination Leadership

Veolia is a global leader in ecological transformation and desalination, managing more than 13 million m³/day treatment capacity across 44 countries. Its technologies span thermal distillation and RO-based desalination, integrated with digital optimization and energy-efficient designs. In August 2024, Veolia launched Africa’s largest desalination project in Morocco, reinforcing its dominance in national-scale water security projects. Veolia’s multi-performance strategy ensures alignment with economic, social, and ESG metrics.

Toray Industries, Inc. – Advancing Material Science in Hybrid Membranes

Toray brings deep expertise in polymer chemistry and advanced composites, positioning itself as a key innovator in hybrid membranes. It manufactures a wide range of RO, UF, NF, and MF membranes, with applications spanning seawater desalination, brackish water, and pharmaceuticals. In January 2025, Toray introduced a high-performance separation module for the biopharmaceutical industry, while its October 2024 acquisition of Zoltek expands carbon-fiber integration into next-gen membranes. With operations in over 20 countries, Toray continues to drive global leadership in sustainable and high-performance membrane technology.

Hybrid Membrane Systems Market Report Scope

Hybrid Membrane Systems Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.8 Billion

|

|

Market Size (2034)

|

$12.5 Billion

|

|

Market Growth Rate

|

8.9%

|

|

Segments

|

By Type (Membrane-Membrane Hybrid Systems, Membrane-Non-Membrane Hybrid Systems), By Application (Zero Liquid Discharge (ZLD) & Minimal Liquid Discharge, High-Efficiency Desalination & Water Reuse, Resource Recovery & Circular Economy, Advanced Industrial Process Separation), By System Integration Level (Custom-Engineered Systems, Pre-Engineered/Packaged Systems), By End-User (Desalination, Municipal Wastewater Treatment & Reuse, Industrial Wastewater Treatment, Potable Water Treatment, Brine & Concentrate Management)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SUEZ, Veolia, DuPont de Nemours, Inc., Toray Industries, Inc., Pentair plc, Xylem Inc., Asahi Kasei Corporation, Kubota Corporation, The Dow Chemical Company, MANN+HUMMEL, Evoqua Water Technologies, Koch Separation Solutions, LG Chem, Aquatech International, Thermax Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hybrid Membrane Systems Market Segmentation

By Type

- Membrane-Membrane Hybrid Systems

- Membrane-Non-Membrane Hybrid Systems

By Application

- Zero Liquid Discharge (ZLD) & Minimal Liquid Discharge

- High-Efficiency Desalination & Water Reuse

- Resource Recovery & Circular Economy

- Advanced Industrial Process Separation

By System Integration Level

- Custom-Engineered Systems

- Pre-Engineered/Packaged Systems

By End-User

- Desalination

- Municipal Wastewater Treatment & Reuse

- Industrial Wastewater Treatment

- Potable Water Treatment

- Brine & Concentrate Management

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Hybrid Membrane Systems Industry include-

- SUEZ

- Veolia

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Pentair plc

- Xylem Inc.

- Asahi Kasei Corporation

- Kubota Corporation

- The Dow Chemical Company

- MANN+HUMMEL

- Evoqua Water Technologies

- Koch Separation Solutions

- LG Chem

- Aquatech International

- Thermax Limited

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Hybrid Membrane Systems landscape with a full-stack market view sizing, adoption curves, and bankability while our analysis reviews technology pairings (e.g., RO–UF, FO–RO, NF–ED), integration levels, and end-use economics; it highlights breakthrough material science, ESG-linked procurement, and digital optimization that lift recovery, cut kWh/m³, and de-risk compliance. Built for utilities, EPCs, OEMs, and industrial owners, this report is an essential resource for comparing TCO/ROI across ZLD/MLD, desalination, and resource-recovery use cases, aligning capex with policy incentives, and prioritizing vendor shortlists through evidence-backed performance benchmarks. Scope Includes-

- Segmentation: By Type (Membrane–Membrane Hybrid Systems, Membrane–Non-Membrane Hybrid Systems); By Application (Zero Liquid Discharge (ZLD) & Minimal Liquid Discharge, High-Efficiency Desalination & Water Reuse, Resource Recovery & Circular Economy, Advanced Industrial Process Separation); By System Integration Level (Custom-Engineered Systems, Pre-Engineered/Packaged Systems); By End-User (Desalination, Municipal Wastewater Treatment & Reuse, Industrial Wastewater Treatment, Potable Water Treatment, Brine & Concentrate Management).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies (Profiles of 15+ companies): SUEZ; Veolia; DuPont de Nemours, Inc.; Toray Industries, Inc.; Pentair plc; Xylem Inc.; Asahi Kasei Corporation; Kubota Corporation; The Dow Chemical Company; MANN+HUMMEL; Evoqua Water Technologies; Koch Separation Solutions; LG Chem; Aquatech International; Thermax Limited.

Methodology

USDAnalytics employed a triangulated approach: (1) bottom-up aggregation from 1,000+ identified facilities/pilots and awarded projects, normalized for capacity, recovery, and energy intensity; (2) top-down reconciliation with country capex pipelines, tariff structures, and policy mandates; and (3) expert validation via 35+ interviews across OEMs, EPCs, operators, and regulators. We developed techno-economic models for hybrid trains (UF+RO, FO+RO, NF+ED, RO+crystallizer), standardizing pretreatment, flux, recovery, CIP/AOP regimes, and waste-heat integration to yield LCOwater/LCOrecovery and sensitivity bands. Vendor scorecards assess membrane performance (permeability, selectivity, fouling rebound), pack density, skid modularity, and digital controls. Forecasts apply cohort adoption curves, replacement cycles, and scenario analysis for energy prices, discharge limits, and ESG financing.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Hybrid Membrane Systems Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights for Industry Stakeholders

1.3. Global Market Snapshot

2. Hybrid Membrane Systems Market Outlook (2025–2034)

2.1. Market Overview: Growth Driven by Sustainable and Energy-Efficient Solutions

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $5.8 Billion

2.2.2. Forecasted Market Size (2034): $12.5 Billion

2.2.3. Projected Compound Annual Growth Rate (CAGR): 8.9%

2.3. Emerging Trends and Growth Opportunities

2.3.1. Growth of Hybrid MBR Systems for Water Reuse and Reclamation

2.3.2. Development of Energy-Efficient Hybrid FO-RO Systems for Desalination

2.3.3. Rising Adoption in Industrial Wastewater Treatment and On-Site Reuse

2.3.4. Integration with Advanced Oxidation Processes (AOPs) for Micropollutant Removal

3. Recent Developments Reshaping the Market

3.1. Market Analysis: Strategic Collaborations and Innovations

3.1.1. Kurita Water Industries Listed on Nature Stock Index (June 2025)

3.1.2. Toray Industries Introduces High-Efficiency Biopharmaceutical Membrane Module (January 2025)

3.1.3. Memsift Innovations Partners with Murugappa Group on New Membrane Launch (March 2025)

3.1.4. Evoqua Water Technologies Secures Patent for Manure Wastewater Treatment (November 2024)

3.1.5. Veolia and Morocco Commence Large-Scale Desalination Facility Construction (August 2024)

3.1.6. Dow Launches Manufacturing Facility for TEQUATIC™ PLUS Filter (June 2024)

3.1.7. Toray Completes Acquisition of Zoltek (October 2024)

4. Competitive Landscape: Leading Players

4.1. Market Overview: Focus on R&D, ESG, and Digital Integration

4.2. Profiles of Leading Players

4.2.1. Kurita Water Industries Ltd.

4.2.2. Dow Water & Process Solutions

4.2.3. Evoqua Water Technologies LLC

4.2.4. SUEZ Water Technologies & Solutions

4.2.5. Veolia Water Technologies

4.2.6. Toray Industries, Inc.

5. Hybrid Membrane Systems Market – Segmentation Insights

5.1. By Type

5.1.1. Membrane-Non-Membrane Hybrid Systems

5.1.2. Membrane-Membrane Hybrid Systems

5.2. By Application

5.2.1. Zero Liquid Discharge (ZLD) & Minimal Liquid Discharge

5.2.2. High-Efficiency Desalination & Water Reuse

5.2.3. Resource Recovery & Circular Economy

5.2.4. Advanced Industrial Process Separation

5.3. By System Integration Level

5.3.1. Custom-Engineered Systems

5.3.2. Pre-Engineered/Packaged Systems

5.4. By End-User

5.4.1. Desalination

5.4.2. Municipal Wastewater Treatment & Reuse

5.4.3. Industrial Wastewater Treatment

5.4.4. Potable Water Treatment

5.4.5. Brine & Concentrate Management

6. Country Analysis and Outlook: Hybrid Membrane Systems Market

6.1. United States: Government-Backed Innovations Driving Adoption

6.2. China: Regulatory Policies and Industrial Expansion

6.3. Germany: Technological Leadership in Industrial Hybrid Systems

6.4. India: Government Programs and Infrastructure Investment

6.5. Japan: Academic and Corporate R&D Accelerating Solutions

6.6. Australia: Water Scarcity and Recycling Initiatives Driving Innovation

6.7. Other Key Countries Analyzed

6.7.1. North America (Canada, Mexico)

6.7.2. Europe (UK, France, Spain, Italy, Russia, Rest of Europe)

6.7.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

6.7.4. South America (Brazil, Argentina, Rest of South America)

6.7.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Hybrid Membrane Systems Market Size Outlook by Region (2025-2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Type

7.1.2. By Application

7.2. Europe Market Size Outlook to 2034

7.2.1. By Type

7.2.2. By Application

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Type

7.3.2. By Application

7.4. South America Market Size Outlook to 2034

7.4.1. By Type

7.4.2. By Application

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Type

7.5.2. By Application

8. Company Profiles: Additional Leading Players

8.1. SUEZ

8.2. Veolia

8.3. DuPont de Nemours, Inc.

8.4. Toray Industries, Inc.

8.5. Pentair plc

8.6. Xylem Inc.

8.7. Asahi Kasei Corporation

8.8. Kubota Corporation

8.9. The Dow Chemical Company

8.10. MANN+HUMMEL

8.11. Evoqua Water Technologies

8.12. Koch Separation Solutions

8.13. LG Chem

8.14. Aquatech International

8.15. Thermax Limited

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures