Market Analysis and Value Forecast: Boiler Water Treatment Chemicals Sector Shows Steady Growth

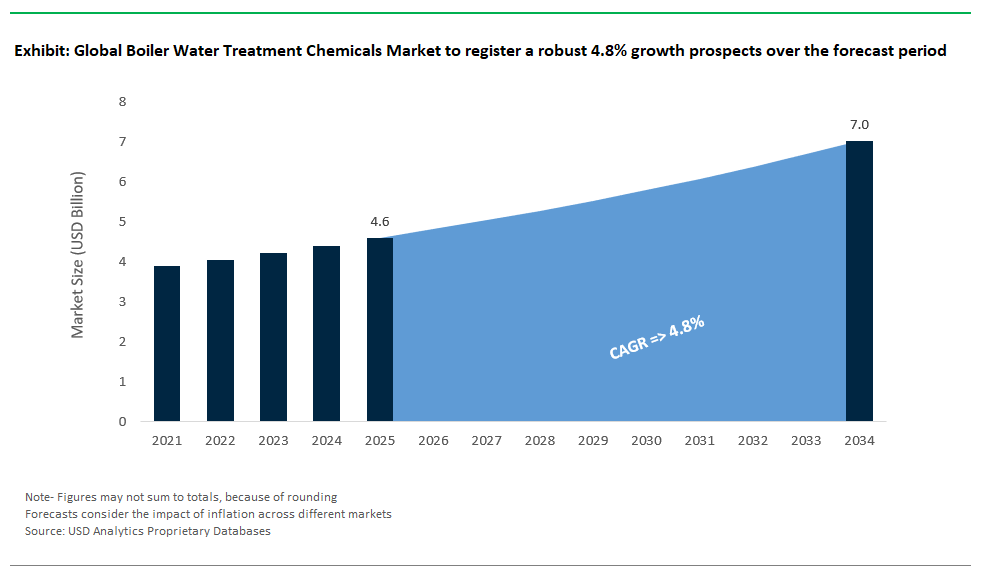

The boiler water treatment chemicals market is valued at $4.6 billion in 2025 and is projected to reach $7 billion by 2034, reflecting a CAGR of 4.8%. This sector is essential for maintaining industrial process integrity. New chemical solutions are emerging in response to rising thermal efficiency standards, pressure ratings, and environmental compliance requirements. As high-pressure drum (HPD) and once-through boilers become more common in power generation and heavy manufacturing, chemical treatment practices must ensure reliable operations while prioritizing environmental and worker safety.

Oxygen scavenging is still a key area of focus. Historically, hydrazine (N₂H₄) has dominated this space because it can lower dissolved oxygen to under 7 ppb. However, due to its classification as a likely human carcinogen, there is a shift towards safer alternatives like carbohydrazide and erythorbic acid.

Managing silica is also important, especially in HPD environments. Following ASME guidelines means keeping silica levels below 0.02 mg/L to prevent volatile carryover and fouling of turbine blades. Magnesium-based coagulants help prevent scale build-up in both makeup and condensate return lines.

Meanwhile, blowdown optimization strategies are becoming more advanced. Cycle concentrations are now routinely extended to 5–50 times through targeted antiscalant programs, which typically use phosphonates in the 2–10 mg/L range to prevent scales of calcium phosphate, iron, and silica. This is crucial as water reuse and high-recovery boiler feed applications introduce more variability in feedwater quality. The demand for non-toxic, high-efficiency formulations is rising due to decarbonization goals affecting energy infrastructure investments. This market is increasingly shaped by the need for solutions that allow better control over corrosion, scaling, and carryover, while ensuring safety and minimizing blowdown losses. Chemical suppliers are investing in both formulation chemistry and digital dosing systems, as well as real-time analytics that fit with smart boiler management practices.

Evolving Market Dynamics and Emerging Opportunities in Boiler Water Treatment Chemicals

Market Trend: Bio-Based and Non-Toxic Boiler Treatment Chemistries Gain Ground Amid Regulatory and ESG Pressures

The global boiler water treatment chemicals market is shifting toward green, non-toxic formulations. Industrial operators and utility managers are facing stricter environmental regulations and stronger ESG demands from corporate stakeholders. Traditional chemical methods, which rely heavily on phosphate-based scale inhibitors, chromate corrosion preventives, and hydrazine oxygen scavengers, are being phased out due to their persistence in the environment, toxicity, and regulatory issues. Instead, bio-derived and enzymatic alternatives are gaining traction, supported by their performance and compliance benefits. Ecolab’s launch of OptiSperse™ Bio in 2024, a plant-based polymer formulation, has proven to be 30% more effective at inhibiting calcium and magnesium scaling compared to older phosphates. This alternative also extends chemical dosing intervals and has received EPA Safer Choice certification. Similarly, Suez’s Phos-Free™ enzymatic program, used in EU thermal plants, has replaced chromate-based corrosion inhibitors, showing a 50% reduction in sludge toxicity. This is significant under the EU’s Industrial Emissions Directive (2024), which officially bans the use of chromates and hydrazine. Beyond formulations, AI-based chemical optimization tools now enable real-time adjustments to pH and amines, cutting down on blowdown waste. As digital automation and green chemistry progress, boiler water treatment is evolving from a simple corrosion and scale control measure to an important part of the decarbonization and sustainability process. Corporate sustainability policies from major tech companies like Microsoft and Google now require green chemistry compliance from their steam-generating suppliers. Chemical vendors that do not innovate regarding safety and traceability risk falling out of procurement channels.

Market Opportunity: Advanced Oxygen Scavengers for Ultra-Low-Pressure and Specialty Boilers Fuel a New Growth Frontier

A new opportunity is emerging in the boiler water treatment chemicals market focused on developing and deploying effective non-toxic oxygen scavengers for ultra-low-pressure and specialized boiler systems. As industries move towards hydrogen-ready power plants, biomass-fired boilers, and clean steam systems in pharmaceuticals and food processing, traditional sulfite or hydrazine-based scavengers are often insufficient or fail to meet regulations. Innovative solutions like Nalco’s OxiTrap have significantly reduced dosage needs by up to 90% while keeping oxygen levels below corrosive thresholds in clean steam boilers operating under 5 psi. This makes them well-suited for pharmaceutical and bioprocessing environments. In semiconductor applications, where oxygen must be below 0.1 ppb, JFE Engineering’s carbon-coated iron catalysts are emerging as the only safe non-toxic option. Additionally, closed-loop chemical recovery technologies are providing benefits related to the circular economy in large industrial sites. Solenis’ ReNew™ platform, for instance, uses electrodialysis to recover up to 95% of used amines from boiler blowdown, reducing the need for fresh chemicals and cutting wastewater discharge. This is a win-win for plants under scrutiny over Scope 1 and 2 emissions. With Asia’s coal-fired boiler fleet transitioning to biomass combustion and an increase in micro-boiler installations in hydrogen-ready settings, oxygen scavengers are shifting from commodity status to a high-specification market. This change is expected to create over $800 million in additional chemical demand by 2025, especially from sectors that prioritize safety, purity, and sustainability in boiler operations.

Competitive Landscape: Boiler Water Treatment Chemicals

Boiler water treatment chemicals are crucial for preventing scale buildup, corrosion, and inefficiencies in steam-generating systems, including low-pressure industrial boilers and high-pressure power plants. The chemical lineup usually includes oxygen scavengers like catalyzed sulfites, DEHA, and carbohydrazide; scale inhibitors such as phosphonates, polymers, and chelants; alkalinity builders; condensate line treatments like neutralizing and filming amines; sludge conditioners; and antifoams. Leading suppliers offer these chemicals along with programs that include real-time monitoring and control to keep systems running well.

Ecolab (Nalco Water) leads the industry with its 3D TRASAR™ system. This system allows for real-time chemical monitoring and automated dosing, backed by remote diagnostics via Ecolab ONE™. The Nalco 360™ Boiler Program addresses all types of steam systems, focusing on efficiency and compliance with regulations for industries like food processing and power generation. SUEZ provides its GenGard™ and Hydrex™ lines, which focus on complex systems like HRSGs and industrial boilers, enhanced by the SpectraGuard™ control systems. Kurita offers a broad range that includes Kuriverter™ scavengers and proprietary polymers for high-pressure and high-purity environments, making it a significant player in thermal power and electronics. Solenis is recognized for its cost-effective Drewtreat™ and Drewamine™ product lines, used in the pulp and paper and refining industries, along with the OptiSens™ platform.

BASF and Italmatch (BWA) supply essential treatment components such as high-purity phosphonates, dispersants, and oxygen scavengers, which downstream formulators widely use. BASF concentrates more on chemical building blocks rather than complete programs, while Italmatch is a global leader in phosphonate technologies that are fundamental to many formulations. Kemira provides specialized KemGuard™ treatments that are especially suitable for pulp and paper boilers facing challenging feedwaters, while Veolia incorporates its Hydrex™ chemical line into full-system solutions, which are supported by SmartLink™ digital platforms for optimizing assets.

ChemTreat, a part of Danaher, sets itself apart with a service-intensive model that includes customized programs and field support across various industrial sectors. Buckman blends its proprietary Busan™ and Guardian™ chemistries with its Bulab 360™ platform to tackle complex conditions in pulp and manufacturing facilities. In India and other emerging markets, Thermax Global and Ion Exchange provide locally adapted boiler chemicals such as the TBC and ZeroBlow™ ranges, along with equipment and monitoring, serving a wide range of industries including textiles, sugar, and refineries. Accepta Ltd completes the market as a trustworthy supplier of pre-formulated boiler water treatment chemicals for smaller industrial and institutional applications, offering effective off-the-shelf solutions without integrated monitoring.

Overall, competition depends on a blend of chemical performance in tough boiler conditions, support for compliance with regulations such as FDA for food steam, capabilities for system monitoring and automation, technical knowledge, and cost-effectiveness to maintain boiler integrity and efficiency.

Boiler Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

Scale & Corrosion Inhibitors Lead Chemical Types; Ion Exchange Resins Experience Fastest Growth

In the Boiler Water Treatment Chemicals market, Scale & Corrosion Inhibitors hold the largest market share, accounting for approximately 27.9% in 2025. Their dominance is primarily due to their indispensable role in protecting boilers from scale formation and corrosion two of the most common operational challenges leading to downtime and increased maintenance costs. These inhibitors help maintain thermal efficiency, reduce fuel consumption, and prolong boiler life, making them essential across industries. Meanwhile, Ion Exchange Resins emerge as the fastest-growing chemical type, registering an impressive 6.2% CAGR through 2034. Their rapid adoption is driven by heightened demand for ultra-high-purity water treatment in sensitive industrial applications, notably within pharmaceuticals, electronics manufacturing, and power plants. Other chemicals, such as Oxygen Scavengers, continue to witness steady adoption, primarily to mitigate pitting corrosion. Cleaning & Descaling Chemicals also demonstrate consistent growth at 9% CAGR, reflecting increasing awareness of preventive maintenance practices and regular boiler upkeep across industries.

Power Generation Dominates End-User Industries; Pharmaceutical Sector Grows Fastest

Within end-user industries, Power Generation leads the Boiler Water Treatment Chemicals market, capturing approximately 39.7% market share in 2025. The sector's dominance is driven by extensive boiler usage in thermal power plants, where reliable steam production, efficient heat transfer, and minimized downtime are paramount for operational excellence. Chemicals such as corrosion inhibitors, oxygen scavengers, and alkalinity builders remain crucial for maintaining boiler performance, safety, and compliance with stringent regulatory standards in the power generation sector. In contrast, the Pharmaceutical industry represents the fastest-growing segment, expanding at a notable 7.1% CAGR during 2025–2034. Growth in this sector is driven by stringent regulatory guidelines mandating high water purity standards, requiring specialized chemical treatments for contamination-free steam production used in pharmaceutical manufacturing processes. Additionally, the Food & Beverage water treatment industry maintains a steady growth trajectory, with an estimated CAGR of 9%, fueled by rigorous hygiene and sanitation requirements. Oil & Gas continues to heavily utilize oxygen scavengers and scale inhibitors for reliable steam generation and process integrity.

.png)

China Fuels Boiler Water Treatment Chemicals Market with Power Sector Expansion and Environmental Mandates

China continues to dominate the global boiler water treatment chemicals market, propelled by relentless industrial growth and unprecedented investments in power generation infrastructure. The country’s ongoing addition of coal and gas-fired power plants is directly elevating demand for specialized water treatment chemicals, as these facilities require high volumes of boiler water conditioning to prevent scale, corrosion, and fouling. China’s power sector remains one of the world’s largest consumers of water, making boiler water treatment essential for operational safety and energy efficiency.

Government-led priorities for environmental protection are also stimulating market innovation, with a push toward advanced corrosion and scale inhibitors to reduce the environmental impact of industrial wastewater discharges. Beyond power, rapidly growing sectors such as textiles, paper, and food & beverage are driving demand for tailored boiler water treatment solutions. This convergence of industrial expansion and environmental policy is cementing China’s leadership in the global market for boiler water treatment chemicals.

United States Advances Boiler Water Treatment Chemicals Market through Innovation and Digitalization

The United States remains a dynamic force in the boiler water treatment chemicals market, leveraging mature industrial sectors and a commitment to cutting-edge technology. Major U.S. players are pioneering solutions such as low-phosphate treatment programs, as highlighted by ChemTreat’s 2024 launch aimed at reducing environmental impact and improving boiler efficiency. Digitalization is reshaping the industry, with companies like Suez Water Technologies rolling out AI-driven monitoring systems that optimize chemical dosing and predictive maintenance, ensuring real-time boiler protection.

The market benefits from robust demand in sectors with high-purity requirements, including pharmaceuticals, which rely on sophisticated chemical treatments to meet strict water quality standards for steam production. Customized solutions for the power and oil & gas industries address specific operational and water quality challenges, further fueling the U.S. market’s role as a trendsetter in high-performance, sustainable boiler water treatment chemicals.

India Accelerates Boiler Water Treatment Chemicals Market with Industrial Growth and Local Production

India’s boiler water treatment chemicals market is experiencing rapid expansion, driven by the country’s accelerating power generation capacity and ongoing industrialization. The proliferation of thermal and nuclear plants key consumers of boiler systems creates a direct and proportional rise in demand for advanced treatment chemicals. Government initiatives like "Make in India" and the rollout of new industrial corridors are spurring growth across manufacturing sectors, notably in food and beverage, where efficient steam generation is critical.

Indian companies are investing in both new facilities and advanced technologies, exemplified by the commercial launch of a hydrazine hydrate (HH) plant in Gujarat a pivotal supply for oxygen scavenger chemicals in 2022. With strict environmental regulations compelling the adoption of effluent treatment plants (ETPs), Indian industry is focused on both water conservation and quality assurance, ensuring strong ongoing demand for boiler water treatment chemicals tailored to local needs.

Germany Champions Sustainable and High-Efficiency Boiler Water Treatment Chemicals

Germany is at the vanguard of sustainable and high-efficiency boiler water treatment chemicals, leveraging a blend of industrial strength and regulatory rigor. German companies and research institutions are developing eco-friendly, phosphate-free formulations in response to stringent environmental laws. Notably, Ecolab’s February 2025 launch of an advanced phosphate-free inhibitor program promises to cut chemical usage by 25% in ultra-supercritical power plant boilers.

Strategic collaborations, such as Solvay’s partnership with major European steel producers, are facilitating real-time, sensor-driven dosing systems for continuous boiler water quality optimization. Germany’s focus on high-performance heating systems and steam generators ensures the boiler water treatment segment remains a cornerstone of the national water treatment chemicals market, reinforcing the country’s leadership in both innovation and environmental stewardship.

Japan Sets High Standards for Boiler Water Treatment Chemicals with Technological Sophistication

Japan’s boiler water treatment chemicals market is defined by technological leadership and a strong focus on high-purity water for industrial and power generation applications. The segment benefits from the development of advanced solutions including sludge controllers, antifoams, and oxygen scavengers engineered to maximize boiler efficiency and lifespan. Leading Japanese firms like Kurita Water Industries are investing in research centers dedicated to next-generation, sustainable water treatment chemistries with integrated digital technologies.

Japan’s diverse manufacturing base and extensive power sector rely on high-purity water to safeguard high-pressure boilers against scale and corrosion, driving continuous innovation. Hybrid approaches that combine traditional and digital treatments underscore Japan’s commitment to both operational excellence and reduced environmental impact, solidifying its position as a global reference for boiler water treatment.

United Kingdom Modernizes Boiler Water Treatment Chemicals Market with Integrated Solutions and Sustainability Focus

The United Kingdom is modernizing its boiler water treatment chemicals market through a blend of sustainability initiatives and advanced technological integration. Government-led water management strategies are indirectly raising the bar for boiler treatment standards in both industrial and power sectors. The market is shifting towards comprehensive solutions that combine chemical treatments with advanced technologies such as reverse osmosis (RO) and continuous electrodeionization (CEDI), achieving the highest purity levels for high-pressure boiler applications.

Veolia Water Technologies UK exemplifies the industry’s holistic approach, providing pre-treatment, internal treatment, and digital monitoring to maximize boiler system longevity and performance. The power generation sector remains a key market driver, as efforts intensify to improve water treatment and recovery efficiency across the UK’s aging infrastructure.

Brazil Strengthens Boiler Water Treatment Chemicals Demand with Industrial and Infrastructure Growth

Brazil’s boiler water treatment chemicals market is closely linked to the nation’s industrial development and ongoing investment in infrastructure projects. Awarded contracts for new and upgraded water and wastewater treatment plants reflect strong demand for reliable boiler water treatment, particularly in regions with high industrial and energy generation density. The cooling and boiler segment is the largest revenue generator within the country’s industrial water treatment chemicals market, underlining its essential role in supporting steam and power production.

Growth in pivotal sectors such as food & beverage, pulp & paper, and oil & gas is driving sustained investment in advanced boiler water treatment solutions. As Brazil’s manufacturing and energy industries continue to expand, the importance of chemical treatment for safe, efficient, and compliant boiler operation is only set to grow.

South Korea Drives Boiler Water Treatment Chemicals Market with Technological Advances and Safety Focus

South Korea’s market for boiler water treatment chemicals is shaped by rapid industrialization, a strong emphasis on safety, and ongoing expansion in power generation. The country’s robust manufacturing, chemical processing, and energy sectors depend on sophisticated chemical treatments to maintain efficient and trouble-free boiler operation. Technological advancements are a defining feature, with South Korean companies pioneering scientifically engineered chemicals that proactively combat scale, corrosion, and sludge.

With the government prioritizing power sector expansion including both thermal and nuclear plants there is a corresponding surge in demand for boiler water treatment chemicals to protect critical infrastructure. The cooling and boiler segment stands as the largest revenue source in the industrial water treatment chemicals market, reflecting the indispensable role these chemicals play in South Korea’s industrial ecosystem.

Boiler Water Treatment Chemicals Market Report Scope

Boiler Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.6 Billion

|

|

Market Size (2034)

|

$7 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Type of Chemical (Scale and Corrosion Inhibitors, Oxygen Scavengers, pH Boosters/Alkalinity Builders, Coagulants and Flocculants, Defoamers and Defoaming Agents, Sludge Conditioners, Chelating Agents, Cleaning and Descaling Chemicals, Ion Exchange Resins, Other Specialty Chemicals), By Application (Basic Chemicals, Blended/Specialty Chemicals), By End-User Industry (Power Generation, Oil and Gas, Chemical and Petrochemical, Food and Beverage, Pulp and Paper, Textile and Dye Industry, Sugar Mill, Pharmaceutical, Other End-user Industries

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab (U.S.), SUEZ SA (France), Kurita Water Industries Ltd. (Japan), Solenis (U.S.), BASF SE (Germany), Kemira Oyj (Finland), Veolia Water Technologies (France), ChemTreat, Inc. (U.S.), Buckman (U.S.), Thermax Global (India), Italmatch Chemicals (BWA Water Additives), Ion Exchange LLC, Accepta Ltd,

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Boiler Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Scale and Corrosion Inhibitors

- Scale Inhibitors

- Corrosion Inhibitors

- Oxygen Scavengers

- pH Boosters/Alkalinity Builders

- Coagulants and Flocculants

- Defoamers and Defoaming Agents

- Sludge Conditioners

- Chelating Agents

- Cleaning and Descaling Chemicals

- Ion Exchange Resins

- Other Specialty Chemicals

By Application

- Basic Chemicals

- Blended/Specialty Chemicals

By End-User Industry

- Power Generation

- Oil and Gas

- Chemical and Petrochemical

- Food and Beverage

- Pulp and Paper

- Textile and Dye Industry

- Sugar Mill

- Pharmaceutical

- Other End-user Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Boiler Water Treatment Chemicals Market

- Ecolab (U.S.)

- SUEZ SA (France)

- Kurita Water Industries Ltd. (Japan)

- Solenis (U.S.)

- BASF SE (Germany)

- Kemira Oyj (Finland)

- Veolia Water Technologies (France)

- ChemTreat, Inc. (U.S.)

- Buckman (U.S.)

- Thermax Global (India)

- Italmatch Chemicals (BWA Water Additives)

- Ion Exchange LLC

- Accepta Ltd

* List Not Exhaustive

Research Coverage

This report delivers a comprehensive analysis of the Boiler Water Treatment Chemicals Market, covering growth drivers, market size, and detailed segmentation by chemical type, application, end-user industry, and geography. It examines trends in green, non-toxic chemistries, advanced oxygen scavengers, and digital dosing solutions in response to rising regulatory, ESG, and efficiency pressures across industrial sectors. The study explores key market opportunities in power generation, food & beverage, and pharmaceutical applications, along with country-level insights into regulatory dynamics, innovation, and local production. USDAnalytics equips industry leaders, technology providers, and policymakers with actionable, data-driven intelligence to navigate market shifts and capitalize on emerging opportunities in boiler water treatment.

Scope Highlights:

- Segmentation:

- By Type of Chemical: Scale & Corrosion Inhibitors, Oxygen Scavengers, pH Boosters/Alkalinity Builders, Coagulants & Flocculants, Defoamers, Sludge Conditioners, Chelating Agents, Cleaning & Descaling Chemicals, Ion Exchange Resins, Other Specialty Chemicals

- By Application: Basic Chemicals, Blended/Specialty Chemicals

- By End-User Industry: Power Generation, Oil & Gas, Chemical & Petrochemical, Food & Beverage, Pulp & Paper, Textile & Dye Industry, Sugar Mill, Pharmaceutical, Other End-user Industries

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Key Players: Ecolab, SUEZ SA, Kurita Water Industries, Solenis, BASF SE, Kemira Oyj, Veolia Water Technologies, ChemTreat, Buckman, Thermax Global, Italmatch Chemicals (BWA Water Additives), Ion Exchange LLC, Accepta Ltd (list not exhaustive)

Methodology

USDAnalytics employs a rigorous, multi-layered research approach for the Boiler Water Treatment Chemicals Market, combining primary interviews with global suppliers, utility managers, and regulatory authorities, alongside extensive secondary research from technical literature, market databases, and industry reports. Market sizing and forecasts are developed through proprietary modeling, triangulated with historic data (2021–2024) and scenario-based projections to 2034. Each segment is analyzed for market share, growth catalysts, technology adoption, and regulatory trends, with emphasis on innovations in green chemistry, smart dosing, and compliance requirements. Peer review and sensitivity analysis ensure all insights are reliable and actionable for stakeholders seeking strategic clarity in this evolving market.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements