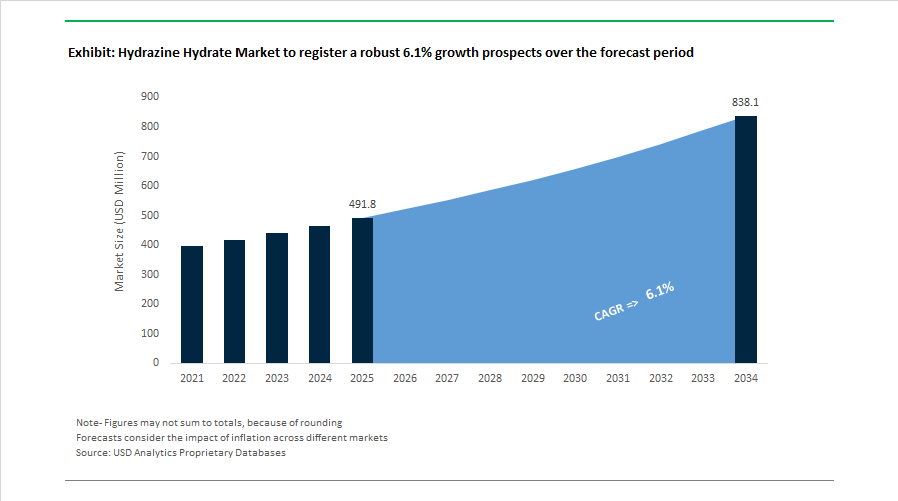

Hydrazine Hydrate Market to Reach $838 Million by 2034 at 6.1% CAGR Driven by Pharma-Grade Expansion, Agrochemical Standards, and Regulatory Tightening

The Hydrazine Hydrate Market is projected to grow from $491.8 Million in 2025 to $838 Million by 2034, registering a CAGR of 6.1%. Market expansion is being supported by rising demand for high-purity hydrazine derivatives in pharmaceutical synthesis, agrochemical intermediates, polymer blowing agents, and water treatment chemicals. Increasing domestic production capacity in Asia, modernization of specialty chemical infrastructure in Europe, and evolving hazardous chemical regulations are reshaping global supply dynamics. Manufacturers are prioritizing process safety, vertical integration, and advanced purification systems to meet tightening compliance frameworks and export-grade quality standards.

In April 2024, AB Botek introduced its adiDAO Microencapsulation technology, highlighting the growing integration of specialty chemical processing techniques involving hydrazine-based intermediates in enzyme protection and advanced nutrition formulations. During 2024, Matrix Fine Chemicals operationalized a high-security hazardous materials warehouse in Southern Germany, strengthening European logistics for hydrazine hydrate distribution under stringent storage and transport regulations. By late 2024, Gujarat Alkalies and Chemicals Ltd reached full-scale commercial production at its Dahej facility, marking India’s first large-scale hydrazine hydrate plant. The project targets a reduction of the country’s 17,000-ton annual import dependency by more than 60%, significantly altering regional trade flows. From 2024 through 2025, India enforced stricter Bureau of Indian Standards for agrochemical intermediates, compelling domestic hydrazine manufacturers to upgrade purification systems and analytical compliance capabilities to sustain export competitiveness.

Capacity expansion and portfolio optimization accelerated through 2025. In early 2025, SS Blowchem commissioned a new 2,800 TPA hydrazine hydrate and azodicarbonamide production facility in Rajasthan, addressing rising demand for polymer blowing agents used in lightweight automotive and construction foams. On April 1, 2025, Lonza implemented its “One Lonza” operating model, integrating its Advanced Synthesis platform to streamline complex hydrazine-based pharmaceutical manufacturing services. In April 2025, LANXESS divested its Urethane Systems business to UBE Corporation, reallocating capital toward its Saltigo division, which utilizes hydrazine derivatives in high-value agrochemical and pharmaceutical intermediates. In November 2025, Yibin Tianyuan Group accelerated its vertically integrated chlorine-titanium-phosphorus value chain strategy to stabilize feedstock costs and secure downstream hydrazine hydrate production. In December 2025, China enacted its first comprehensive Dangerous Chemicals Safety Law, scheduled to take full effect in May 2026, introducing strict executive accountability and enhanced operational safety requirements for hydrazine producers.

Modernization and sustainability benchmarking defined early 2026. In January 2026, Lonza completed a multi-year upgrade of its specialty chemical facilities, enhancing production of high-purity hydrazine derivatives for antibody-drug conjugates and advanced APIs following strong financial performance in 2025. In February 2026, Arkema received the EcoVadis Gold Medal, ranking in the top 2% for sustainability performance, a critical differentiator as pharmaceutical and water treatment customers increasingly require ESG-verified supply chains. The hydrazine hydrate industry is evolving toward safer manufacturing environments, domestic capacity security, pharmaceutical-grade purity optimization, and vertically integrated raw material sourcing, reinforcing its strategic position in global specialty chemicals and advanced synthesis markets.

Hydrazine Hydrate Market Trends and Opportunities

Regulatory Capacity Retrenchment and European Supply Chain Realignment

The hydrazine hydrate market in Europe is undergoing a structural contraction driven by regulatory escalation and loss of feedstock competitiveness. The substance’s continued classification as a Substance of Very High Concern under the REACH framework has materially increased compliance costs, legal exposure, and administrative overhead for manufacturers and downstream users. As of November 2025, hydrazine hydrate remains listed on the ECHA Candidate List, triggering mandatory disclosure obligations under Article 33 when concentrations exceed 0.1% by weight. For many producers, this has shifted hydrazine from a production asset to a liability, accelerating the move away from local synthesis toward import-and-dilute or tolling models.

This regulatory pressure is being compounded by broader petrochemical de-industrialization across Europe. The region’s hydrazine value chain historically relied on integrated upstream assets to offset the energy intensity of synthesis. However, structural exits are dismantling this advantage. The scheduled February 2026 closure of ExxonMobil’s 830,000-ton ethylene cracker in Scotland and Dow’s planned exit from German cracker assets by 2027 are emblematic of a wider retreat from high-energy chemistry. As integrated ammonia, peroxide, and ketone streams disappear, European hydrazine production costs have become structurally uncompetitive relative to Asia.

As a result, procurement patterns are shifting decisively. Supply data from early 2025 indicates that European pharmaceutical, agrochemical, and power-sector buyers increased reliance on Asian-origin hydrazine hydrate by an estimated 15 to 20% year on year. This realignment is not cyclical but strategic, signaling a long-term reconfiguration of global trade flows where Europe increasingly acts as a demand center rather than a production hub for hydrazine hydrate.

Consolidation of Polymer Foaming Demand Under the Montreal Protocol Final Phase

While production is retrenching in Europe, global demand fundamentals for hydrazine hydrate are being reinforced by regulatory tailwinds in polymer foaming applications. The Montreal Protocol has entered its final and most consequential phase, with developing Article 5 countries mandated to achieve a 67.5% reduction in HCFC consumption by December 2025 and a complete phase-out by 2030. This has permanently removed legacy ozone-depleting blowing agents from the market, creating a durable demand floor for azodicarbonamide-based systems.

Hydrazine hydrate remains the indispensable upstream precursor for azodicarbonamide, which continues to dominate as the chemical blowing agent of choice for PVC, EVA, and cross-linked polyethylene foams. In 2025, accelerating energy-efficiency retrofits across North America and China stabilized demand for high-performance insulation foams used in building envelopes, HVAC ducting, and district heating networks. ADC-blown XLPE and PVC foams are central to meeting tightening Net Zero building codes due to their consistent cell structure, thermal resistance, and mechanical stability.

Automotive lightweighting is reinforcing this trend. Tier-1 suppliers reported in late 2024 that the transition toward 800-volt electric vehicle platforms is driving higher adoption of foamed structural components to offset battery mass. Hydrazine-derived initiators are critical in these applications because they deliver uniform gas evolution and precise cellular morphology, which are essential for safety-critical interior and under-hood components. This positions polymer foaming as a structurally resilient end-use segment for hydrazine hydrate despite broader chemical market volatility.

High-Nitrogen Energetic Materials for Defense Modernization

Defense modernization programs are opening a specialized, high-margin growth corridor for hydrazine hydrate. The global shift toward insensitive munitions has increased demand for energetic materials that combine high detonation performance with enhanced stability under shock, heat, and impact. Hydrazine hydrate plays a pivotal role as a precursor in advanced nitrogen-rich compounds, particularly triazole and tetrazole derivatives.

Research published during 2024–2025 by the Munitions Safety Information Analysis Center highlights hydrazine’s role in synthesizing hydrazinium 5-aminotetrazolate, a compound containing more than 83% nitrogen by mass. With a reported detonation velocity exceeding 9,500 meters per second, this material outperforms conventional HMX while offering markedly improved insensitivity characteristics. Such performance profiles align directly with modern defense requirements for safer storage, transport, and deployment.

Policy support is reinforcing this opportunity. The 2024 update to the U.S. National Defense Industrial Strategy explicitly prioritizes domestic supply chains for critical energetic precursors, identifying hydrazine hydrate as a foundational building block. Parallel demand stability is emerging from space applications. NASA’s Commercial Lunar Payload Services missions scheduled through 2025 continue to rely on hydrazine-based monopropellants for lander descent engines, sustaining demand for ultra-high-purity grades above 99%.

High-Purity Oxygen Scavengers for Closed-Loop Digital Power Plants

In the utility sector, hydrazine hydrate is benefiting from the convergence of asset life extension, digitalization, and stricter reliability metrics. Aging nuclear and high-pressure fossil plants are increasingly managed through closed-loop chemistry control strategies designed to minimize corrosion, metal transport, and forced outages. Within these systems, high-purity hydrazine hydrate remains a critical oxygen scavenger.

Thermal plant audits conducted in 2025 indicate that maintaining hydrazine residuals between 0.05 and 0.2 parts per million is essential for passivating high-pressure boiler tubing. This treatment suppresses iron oxide transport to turbines, a factor linked to reductions in unplanned downtime of approximately 12% annually. In nuclear facilities, hydrazine hydrate is increasingly deployed alongside film-forming amines during wet lay-up procedures. Guidance from the International Atomic Energy Agency suggests this hybrid approach is becoming the global best practice for preventing localized corrosion during extended maintenance outages.

A further opportunity is emerging at the intersection of chemistry and automation. Power producers are adopting digital dosing skids that integrate real-time dissolved oxygen sensors with precision hydrazine injection. By 2026, utilities deploying these systems are expected to reduce chemical overfeed by roughly 15% while achieving full compliance with hazardous material handling protocols. For chemical service providers, this shifts hydrazine hydrate from a commodity input to a value-added, digitally enabled service offering within modern power plant ecosystems.

Hydrazine Hydrate Market Share and Segmentation Insights

Medium Concentration Hydrazine Hydrate Leads the Market Through Industrial Handling Efficiency

Medium Concentration hydrazine hydrate accounted for 48.60% of the Hydrazine Hydrate Market share in 2025, making it the most widely used concentration level across industrial applications. Medium concentration solutions, typically within the 55–65% hydrazine hydrate range, provide the optimal balance between chemical stability, operational safety, and cost efficiency, allowing them to meet the requirements of major end-use sectors including water treatment, agrochemical production, polymer foaming agents, and specialty chemical synthesis. These concentrations are easier to transport, store, and handle compared to high concentration or anhydrous hydrazine formulations, which require stricter safety protocols due to their higher reactivity. In 2025, global trade and regulatory harmonization have led to the standardization of hydrazine hydrate concentrations at approximately 55% and 64%, which has improved supply chain efficiency for chemical distributors and industrial buyers. Standardized concentrations enable manufacturers to streamline bulk logistics, storage infrastructure, and procurement processes, while higher concentration grades remain specialized products used primarily in aerospace propellants and high-value chemical synthesis.

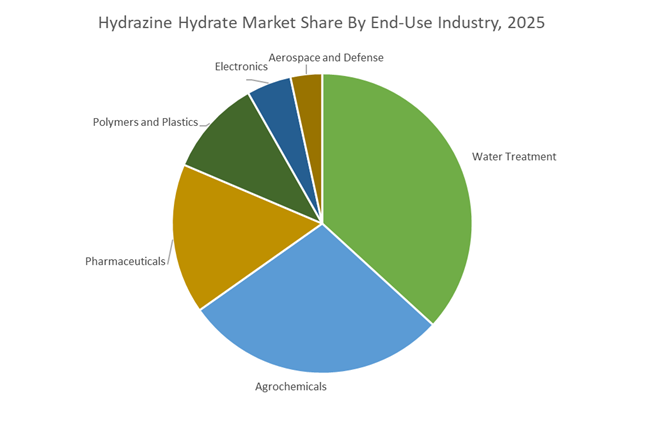

Water Treatment Drives the Largest Demand for Hydrazine Hydrate

Water Treatment represented 36.80% of the Hydrazine Hydrate Market share in 2025, establishing it as the largest end-use industry for hydrazine-based chemicals. Hydrazine hydrate is widely used as an oxygen scavenger in high-pressure boiler water treatment systems, where it removes dissolved oxygen from feedwater to prevent corrosion in boilers, steam lines, and condensate systems. The chemical reacts with dissolved oxygen to produce nitrogen and water, eliminating oxygen without introducing dissolved solids that could otherwise increase boiler blowdown frequency and reduce thermal efficiency. As a result, hydrazine-based oxygen scavengers are extensively used in power generation facilities, petrochemical plants, refineries, and industrial manufacturing operations that rely on high-pressure steam systems. In 2025, the water treatment sector is experiencing growing competition from alternative oxygen scavenger chemistries, including carbohydrazide and diethylhydroxylamine (DEHA), which offer lower toxicity and simplified handling requirements in certain applications. However, hydrazine continues to maintain strong adoption in high-pressure boiler systems, where its volatile nature allows it to protect both boiler components and downstream condensate return systems.

Competitive Landscape in Hydrazine Hydrate Market

Arkema S.A. Expands Specialty Hydrazine and Renewable Manufacturing Footprint

Arkema S.A. remains a primary global producer of hydrazine hydrate, leveraging its Thiochemicals platform to supply high-purity and specialty grades. During 2025 and 2026, Arkema reported successful start-up of three major capacity expansions across Asia and the United States, contributing an additional €60 million in EBITDA compared to 2024. The company is accelerating renewable energy integration across specialty material sites under its zero-carbon pathway strategy to offset inflationary pressure and enhance margin stability. Arkema supplies ultra-high purity hydrazine for oxygen scavenging and corrosion inhibition in high-pressure steam systems used in power generation and industrial boilers. Its 2026 portfolio reorganization integrates hydrazine derivatives into the Specialty Materials segment, targeting batteries, additive manufacturing, and healthcare applications.

LANXESS AG Strengthens Advanced Intermediates and ECO Variants

LANXESS AG has completed its transformation into a pure-play specialty chemicals company following the divestiture of its Urethane Systems business in 2025. Under the FORWARD action plan, the company achieved a 31.7% EBITDA increase in early 2025 through cost discipline and optimized capacity utilization in its Advanced Intermediates segment. LANXESS supplies significant volumes of hydrazine hydrate for azodicarbonamide blowing agent production, which supports lightweight automotive and construction materials. Through its subsidiary Saltigo, the company is launching ECO-labeled intermediates that reduce product carbon footprints by up to 40% via renewable electricity and green chlorine integration. This sustainability-driven strategy enhances its position in the European hydrazine hydrate and polymer additive markets.

Otsuka-MGC Chemical Advances Propellant-Grade and Pharmaceutical Applications

Otsuka-MGC Chemical Company, Inc., a joint venture between Otsuka Chemical and Mitsubishi Gas Chemical, is recognized for technological excellence in high-purity hydrazine production. The company specializes in propellant-grade hydrazine for commercial satellite launch vehicles and regional aerospace programs across Asia-Pacific. In early 2026, expanded on-site solar power installations were implemented to support carbon-neutral manufacturing objectives. The group has also strengthened pharmaceutical supply resilience through broader corporate alliances, reflecting its commitment to manufacturing stability. Otsuka-MGC produces specialized hydrazine derivatives for anticancer and anti-tuberculosis drug intermediates, capitalizing on sustained growth in pharmaceutical-grade hydrazine demand across regulated markets.

Lonza Group AG Secures Aerospace Propellant Supply Leadership

Lonza Group AG occupies a strategic niche as a primary Western supplier of propellant-grade hydrazine for aerospace and defense applications. The company prioritizes long-term contracts supporting U.S. government space programs and military aviation platforms. Its hydrazine hydrate portfolio includes high-concentration grades between 60% and 85%, widely used in emergency power units for aircraft such as single-engine fighters. Lonza leverages its pharmaceutical CDMO expertise to refine hydrazine-based API synthesis pathways, ensuring compliance with stringent regulatory standards. By maintaining production capabilities outside Asia, Lonza reinforces supply chain security for mission-critical propulsion and defense systems.

Hunan Zhuzhou Chemical Industry Group Drives Volume and Catalytic Innovation

Hunan Zhuzhou Chemical Industry Group is one of the largest global producers by volume, contributing significantly to Asia-Pacific’s dominant share of hydrazine hydrate production. The company supplies extensive quantities to the agrochemical and polymer industries, particularly for azodicarbonamide blowing agents used in lightweight EV components. In 2026, the group is scaling eco-friendly catalytic oxidation processes that may reduce environmental impact by up to 50% compared to traditional urea-based synthesis routes. Capacity expansion in reagent-grade hydrazine supports China’s growing fine chemical and laboratory reagent markets. Its export-oriented production model positions the company as a major global supplier of industrial and polymer-grade hydrazine.

Nippon Carbide Industries Integrates Hydrazine Chemistry into Advanced Materials

Nippon Carbide Industries Co., Inc. focuses on high-precision hydrazine derivatives for electronics, safety films, and advanced optical materials. The company integrates hydrazine chemistry into functional films and retroreflective materials used in smart mobility systems and autonomous vehicle sensors. In 2025 and 2026, it launched advanced polymerization initiators derived from hydrazine for high-clarity optical plastics in mobile displays and electronic components. Investments in closed-loop water treatment systems enhance compliance with stringent Japanese environmental discharge standards. Nippon Carbide maintains a specialized distribution network serving semiconductor and electronics manufacturers in South Korea and Taiwan, strengthening its presence in high-value precision markets.

China: Energy Reclassification, Green Synthesis, and Export-Oriented Scaling

China’s hydrazine hydrate industry is undergoing a structural reset driven by energy policy reclassification, low-carbon mandates, and export-led downstream demand. The National Energy Law that took effect in April 2025 formally reclassified hydrogen-related chemicals, including hydrazine derivatives, as energy resources. This regulatory shift has eased historical production constraints and encouraged chemical complexes to integrate hydrazine-based energy storage and hydrogen carrier applications within broader clean energy systems. In parallel, the Ministry of Industry and Information Technology accelerated its low-carbon industrial plan for 2025–2026, resulting in green hydrazine pilot projects in Shaanxi and Inner Mongolia. These pilots replace coal-based synthesis routes with cleaner catalytic pathways aligned with industrial hydrogen decarbonization targets.

Capacity expansion continues to underpin China’s export strategy. Tianjin Dagu Chemical brought an additional 20,000 tons per year of hydrazine hydrate capacity online across 2024–2025 to serve blowing agent demand in Southeast Asian polymer markets. Agrochemicals remain a strong pull. Under 2025 modernization goals, China prioritized synthesis of pyrazole and triazole intermediates that rely on hydrazine as a core building block, driving a 12% increase in high-purity consumption for herbicides exported to Latin America. Safety and digitalization are tightening in parallel. New provincial rules effective 2026 in Jiangsu mandate AI-based real-time vapor monitoring across hydrazine plants to mitigate toxicity risks and strengthen worker protection, raising the compliance bar for producers.

India: Import Substitution, Capacity Acceleration, and Standards Enforcement

India’s hydrazine hydrate industry is transitioning from import dependence toward domestic self-reliance, supported by capacity investments and formal quality controls. Under the Atmanirbhar initiative, Gujarat Alkalies and Chemicals Ltd. ramped up a new large-scale facility through 2024–2025 designed to meet nearly 60% of domestic demand, displacing imports that previously totaled about 17,000 tons annually. Capacity acceleration is extending beyond Gujarat. In December 2025, a project in the RIICO Industrial Area at Hanumangarh revised investment to ₹1,250 million, expanding capacity from 195 metric tons per month to 1,000 metric tons per month, signaling confidence in sustained domestic offtake.

Regulatory enforcement is formalizing demand quality. Effective early 2026, the Bureau of Indian Standards implemented mandatory certification for industrial hydrazine to standardize purity levels used in state-run thermal power plants and other public assets. Downstream growth remains robust in agrochemicals and polymer processing. Indian producers such as SS Blowchem commissioned new facilities in 2025 with 2,800 tons per annum capacity for hydrazine-derived azodicarbonamide, supporting footwear manufacturing and automotive seating foams. Collectively, these developments position India for regulated, scale-driven growth with rising value addition.

Germany: Closed-Loop Automation, Pharma Custom Synthesis, and Safe Logistics

Germany’s hydrazine hydrate industry is defined by stringent exposure controls, high-value pharmaceutical synthesis, and specialized logistics. The updated EU Industrial Emissions Directive (2024/869), with key compliance milestones in 2025, imposed tighter occupational exposure limits for carcinogens such as hydrazine. This has compelled German manufacturers to adopt fully closed-loop, automated production systems that minimize manual handling and fugitive emissions, raising capital intensity but improving long-term compliance certainty.

Strategic focus is shifting toward custom synthesis for pharmaceuticals. In 2025, LANXESS, through its subsidiary Saltigo, showcased new hydrazine-based synthesis routes at Chemspec Europe aimed at anti-cancer drug precursors and other high-value intermediates. Supporting this specialization, chemical logistics providers in Southern Germany completed new hazardous-goods warehouses in 2025 engineered specifically for high-purity hydrazine and volatile derivatives. These assets strengthen secure storage, controlled transport, and compliance with strict EU handling protocols.

South Korea: Semiconductor Localization and Defense-Oriented Energy R&D

South Korea’s hydrazine hydrate market is increasingly strategic, anchored in semiconductor supply security and defense research. Following the government’s semiconductor support package exceeding USD 20 billion announced in 2024, the country prioritized domestic production of ultra-pure 6N-grade hydrazine for use as a reducing agent in advanced wafer fabrication. This move reduces exposure to external supply risks and aligns hydrazine quality with sub-advanced node manufacturing requirements.

Beyond electronics, energy density advantages are driving research interest. The Ministry of Science and ICT included hydrazine-based fuel cells in its 2025 roadmap, funding R&D for portable power systems intended for defense applications. In these use cases, energy density and rapid deployment outweigh conventional hydrogen storage considerations, positioning hydrazine as a niche but strategic energy carrier.

United States: Aerospace Propellants and Process Safety Reformulation

The United States hydrazine hydrate industry remains anchored in aerospace propulsion and stringent environmental oversight. During 2025–2026, the U.S. Department of Defense and NASA renewed long-term procurement contracts for anhydrous and propellant-grade hydrazine. These agreements support increased satellite launch cadence and the Artemis lunar missions, sustaining demand for high-purity, tightly specified grades.

Regulatory scrutiny is shaping manufacturing pathways. The U.S. Environmental Protection Agency continues its Toxic Substances Control Act review of hydrazine, pushing producers toward catalyst-assisted synthesis routes that reduce hazardous by-products and improve waste profiles. This emphasis on process safety and by-product minimization is influencing capital upgrades and operating practices across U.S. facilities.

Switzerland: HPAPI Expansion and Advanced Oncology Applications

Switzerland plays a specialized role in the hydrazine hydrate value chain through pharmaceutical intermediates. Between 2024 and 2025, Lonza Group completed the expansion of its Highly Potent API suite in Visp. This investment significantly increased capacity for hydrazine-based intermediates used in antibody-drug conjugate payloads and other oncology applications. Switzerland’s focus on controlled environments, regulatory rigor, and high-margin therapeutics positions hydrazine as a critical reagent in advanced drug manufacturing rather than bulk chemical markets.

Summary Table: Country-Level Strategic Signals in the Hydrazine Hydrate Industry

Hydrazine Hydrate Market County Level Snapshot

|

Country

|

Primary Policy or Strategy

|

Core Demand Drivers

|

Structural Implication

|

|

China

|

Energy law reclassification, green pilots

|

Polymers, agrochemicals, energy storage

|

Export-led scale with digital safety

|

|

India

|

Atmanirbhar capacity, BIS mandates

|

Power, foams, agrochemicals

|

Import substitution and standardization

|

|

Germany

|

IED compliance, pharma focus

|

Custom APIs, secure logistics

|

High-compliance, high-value production

|

|

South Korea

|

Semiconductor localization, defense R&D

|

Wafer fabrication, portable power

|

Strategic niche applications

|

|

United States

|

Aerospace contracts, TSCA review

|

Propellants, space missions

|

Safety-driven process optimization

|

|

Switzerland

|

HPAPI expansion

|

Oncology intermediates

|

High-margin pharmaceutical specialization

|

Hydrazine Hydrate Market Report Scope

Hydrazine Hydrate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$491.8 Million

|

|

Market Size (2034)

|

$838 Million

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Concentration Level (Low Concentration, Medium Concentration, High Concentration, Anhydrous Grade), By Grade (Industrial Grade, Reagent Grade, Technical Grade, Propellant Grade), By Function (Reducing Agent, Oxygen Scavenger, Polymerization Initiator, Chemical Intermediate), By End-Use Industry (Water Treatment, Pharmaceuticals, Agrochemicals, Polymers and Plastics, Aerospace and Defense, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Arkema S.A., LANXESS AG, Lonza Group AG, Otsuka Chemical Co., Ltd., Mitsubishi Gas Chemical Company, Inc., Yibin Tianyuan Group, Weifang Yaxing Chemical, Gujarat Alkalies and Chemicals Ltd., Nippon Carbide Industries Co., Inc., Japan Finechem Inc., Zhuzhou Chemical Industry Group, Thermo Fisher Scientific Inc., Merck KGaA, HPL Additives Limited, Matrix Fine Chemicals GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydrazine Hydrate Market Segmentation

By Concentration Level

- Low Concentration

- Medium Concentration

- High Concentration

- Anhydrous Grade

By Grade

- Industrial Grade

- Reagent Grade

- Technical Grade

- Propellant Grade

By Function

By End-Use Industry

- Water Treatment

- Pharmaceuticals

- Agrochemicals

- Polymers and Plastics

- Aerospace and Defense

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hydrazine Hydrate Industry

- Arkema S.A.

- LANXESS AG

- Lonza Group AG

- Otsuka Chemical Co., Ltd.

- Mitsubishi Gas Chemical Company, Inc.

- Yibin Tianyuan Group

- Weifang Yaxing Chemical

- Gujarat Alkalies and Chemicals Ltd.

- Nippon Carbide Industries Co., Inc.

- Japan Finechem Inc.

- Zhuzhou Chemical Industry Group

- Thermo Fisher Scientific Inc.

- Merck KGaA

- HPL Additives Limited

- Matrix Fine Chemicals GmbH

*- List not Exhaustive