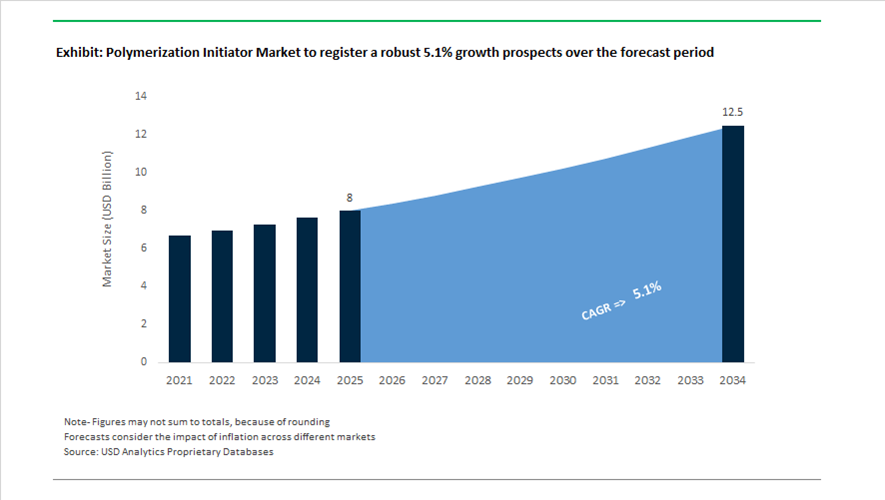

Polymerization Initiator Market Valued at $8 Billion in 2025, Forecast to Reach $12.5 Billion by 2034 at 5.1% CAGR

The global polymerization initiator market is valued at $8 billion in 2025 and is projected to reach $12.5 billion by 2034, registering a CAGR of 5.1%. Market expansion is driven by rising consumption of organic peroxides, azo initiators, persulfates, metal alkyl co-catalysts, modified methylaluminoxane (MMAO), and specialty curing agents across polyolefins, PVC, thermosets, elastomers, EV battery components, aerospace binders, and high-performance cables. Increasing electrification, lightweight automotive materials, advanced composites, and high-clarity plastics are elevating the need for precision-controlled radical generation and cross-linking systems.

In January 2024, Nouryon completed a 50% capacity increase at its Green Bay, Wisconsin facility for key polymer ingredients, including colloidal silica and associated processing chemicals supporting high-clarity plastics. In late 2024, United Initiators implemented green synthesis pathways for persulfates across European sites, reducing carbon footprint by approximately 15%. These developments reinforced the shift toward low-carbon initiator production, sustainable peroxide chemistry, and environmentally optimized radical initiators.

Strategic consolidation accelerated in 2025. In July 2025, NOF Corporation acquired a controlling stake in a domestic Japanese organic peroxide manufacturer, securing supply continuity for automotive rubber and high-growth Asian thermoplastic markets. In August 2025, Syrgis Performance Products completed the acquisition of Norac’s organic peroxides business, adding over $50 million in annual revenue and strengthening its North American specialty initiator portfolio. In 2025, Arclin finalized the integration of Polymer Solutions Group, enabling internal production of customized initiator and additive packages for construction resins and transportation composites. These transactions reflect increasing vertical integration across organic peroxide manufacturing, specialty initiator blending, and customized resin formulation.

Technology launches in late 2025 emphasized safety and process optimization. In October 2025 at K 2025, Arkema introduced Luperox® NeatCure®, a dust-free granular organic peroxide engineered to accelerate curing in extrusion and injection molding while significantly improving workplace handling safety. In the same month, Nouryon inaugurated a dedicated Organic Peroxides Innovation Center in Shanghai to develop region-specific formulations for thermoset and thermoplastic producers. Also in October 2025, Nouryon announced expanded metal alkyl capacity and new MMAO production capability in China, strengthening supply for advanced polyolefin catalyst systems where MMAO functions as a critical co-catalyst and initiator component.

Regional capacity expansions are extending into 2026. In August 2025, a leading Japanese chemical producer aligned with NOF’s expansion strategy announced a major organic peroxide production line upgrade scheduled for completion by mid-2026 to serve the EV battery and electronics sectors. In February 2026, BASF introduced Irgastab® Cable KV 10 to support peroxide cross-linking systems in high-voltage polyethylene cables by preventing premature scorch during manufacturing. In the same month, Evonik strengthened global production infrastructure for hydroxyl-terminated polybutadienes (HTPB), essential for aerospace-grade binders and advanced initiator systems used in defense and propulsion polymers.

The polymerization initiator market is increasingly defined by high-purity organic peroxide production, metal alkyl and MMAO co-catalyst expansion, dust-free curing technologies, green persulfate synthesis, and initiator systems tailored for EV batteries, aerospace composites, and high-voltage power cables. Capacity investments in Asia, sustainability-driven process upgrades in Europe, and consolidation in North America are reshaping supply security and competitive positioning across the global polymer manufacturing value chain.

Key Trends and High-Impact Opportunities in the Polymerization Initiator Market

Strategic Shift Toward Low-Migration and High-Purity Initiator Systems

The polymerization initiator market is undergoing a fundamental redesign driven by migration limits imposed by EU REACH updates and the Swiss Ordinance on Materials and Articles. Initiators have shifted from being performance-only additives to compliance-critical components, particularly in food-contact packaging, medical coatings, and advanced electronics. Traditional low-molecular-weight photoinitiators such as benzophenone are being systematically replaced by macromolecular, polymerizable, or oligomeric initiator systems that chemically anchor into the polymer backbone and eliminate extractables.

Industrial formulation trials conducted during 2025 demonstrate the tangible impact of this transition. Acrylate-modified benzophenone derivatives reduced residual migratory content from approximately 0.8 mg/kg to 0.03 mg/kg, a 96% reduction, while simultaneously increasing curing speeds by around 20% in high-speed flexible packaging lines. This dual benefit is accelerating adoption among packaging converters operating at line speeds exceeding 400 m/min, where both regulatory compliance and throughput efficiency are non-negotiable.

A second wave of innovation is emerging around self-anchoring initiator architectures. Dual-functionalized oxime ester systems incorporating allyl or vinyl groups have demonstrated migration reductions from baseline levels of roughly 81% for conventional initiators to below 3%. These systems now meet the purity thresholds required for medical-grade coatings and high-resolution display manufacturing, including 8K panels where trace outgassing can cause pixel defects. In parallel, the electronics sector is increasingly qualifying oligomeric photoinitiators for solder masks and photoresists. Products such as IGM Resins’ Omnipol series are being adopted for 5G and emerging 6G infrastructure, where ionic purity and low volatility are essential to long-term device reliability in vacuum and high-frequency environments.

Rapid Industrialization of Controlled Radical Polymerization Initiators

Controlled Radical Polymerization has transitioned from laboratory-scale novelty to industrially relevant chemistry. RAFT and ATRP initiator systems are now being deployed to manufacture polymers with precisely defined architectures, enabling block copolymers, gradient materials, and living polymer chains that cannot be achieved through conventional free-radical initiation.

In 2025, photoredox-catalyzed RAFT polymerization entered pilot-scale deployment for vat photopolymerization technologies such as SLA and DLP. This approach enables spatial control over polymer growth, allowing manufacturers to print components with localized mechanical gradients, embedded functional zones, and multi-material interfaces within a single build. These capabilities are particularly valuable in additive manufacturing for medical devices, tooling inserts, and lightweight structural components.

Parallel R&D efforts are focused on wavelength-matched initiator systems optimized for 385–405 nm LED sources, now standard in industrial 3D printers. These architecture-specific initiators reduce energy consumption, improve penetration depth in thick or fiber-filled resins, and enhance cure uniformity in reinforced composites. As additive manufacturing scales from prototyping to serial production, initiator selection is becoming a strategic lever for part performance, production economics, and printer uptime.

Redox Initiator Systems for Agricultural Superabsorbent Polymers

The global push for water-efficient agriculture has created a structurally attractive volume opportunity for water-soluble polymerization initiators. Superabsorbent polymers used as soil conditioners rely on redox initiation systems capable of triggering polymerization in aqueous environments at ambient temperatures, eliminating the energy costs associated with thermal initiation.

Industrial-scale production of cross-linked polyacrylamide hydrogels increasingly depends on potassium persulfate and sodium bisulfite redox pairs. Performance evaluations published in 2025 show that redox-initiated hydrogels achieve tensile strengths of approximately 1.55 MPa, significantly outperforming thermally initiated analogs. This mechanical robustness enables the hydrogel network to survive repeated hydration and dehydration cycles in soil, a critical requirement for multi-season agricultural applications.

Sustainability mandates are further expanding this opportunity. Government-backed programs such as USDA water-efficiency initiatives are accelerating demand for biodegradable SAPs derived from starch-graft-acrylic acid systems. This creates a greenfield market for initiators compatible with bio-based backbones, allowing hydrogels to degrade into non-toxic residues after a single growing season while delivering meaningful improvements in soil water retention and nutrient efficiency.

High-Temperature Initiators for Performance Engineering Plastics

The electrification of transport and expansion of high-voltage systems are driving demand for engineering plastics capable of operating under extreme thermal and electrical stress. Materials such as PEEK, PPS, and polyimides require polymerization initiators that remain stable and reactive at temperatures ranging from 250°C to 400°C, without generating residues that compromise dielectric performance.

High-temperature organic peroxides and ionic initiator systems are emerging as critical enablers for these polymers. Specialized peroxide grades designed for clean decomposition are being adopted to prevent carbonaceous residues that can reduce insulation resistance in EV traction motors and power electronics. These initiators play a direct role in ensuring consistent molecular weight, crystallinity, and long-term thermal stability of the polymer matrix.

Recent research published in March 2025 highlights a nuanced opportunity in copper-rich environments such as motor windings. While copper can accelerate thermal oxidation in PEEK, certain PPS formulations exhibit retarded degradation in the presence of copper. This divergence is driving demand for initiator and stabilizer systems that can be co-optimized to maximize service life in 800V EV architectures, positioning high-temperature initiator suppliers as strategic partners rather than commodity chemical vendors.

Polymerization Initiator Market Share and Segmentation Insights

Organic Peroxides Lead Polymerization Initiator Technologies in Commercial Polymer Production

Organic peroxides accounted for 42.8% of the Polymerization Initiator Market by type in 2025, reflecting their versatility in free radical polymerization processes used across major polymer production routes. These initiators are widely used in manufacturing low-density polyethylene, polyvinyl chloride, polystyrene, acrylic polymers, and unsaturated polyester resins due to their controlled decomposition profiles and compatibility with high-temperature polymerization conditions. Organic peroxide initiators allow manufacturers to regulate polymer chain initiation and molecular weight distribution in large-scale industrial reactors. In 2025, advanced peroxide formulations with optimized decomposition temperatures are enabling more precise polymerization control, improving polymer quality while enhancing process efficiency in high-temperature polymer manufacturing environments.

Polyethylene Applications Drive Global Demand for Polymerization Initiators

Polyethylene represented 28.40% of the Polymerization Initiator Market by application in 2025, supported primarily by the high-pressure production of low-density polyethylene. LDPE polymerization in autoclave and tubular reactor systems requires organic peroxide initiators to generate free radicals under extreme reaction conditions exceeding 2000 bar pressure and elevated temperatures. The large global production base of LDPE used in flexible packaging, wire and cable insulation, and industrial films drives significant initiator consumption. In 2025, advances in tubular reactor technology are influencing initiator system design, with multi-zone injection strategies using peroxides with different decomposition temperatures enabling improved temperature control, optimized molecular weight distribution, and higher reactor conversion efficiency in modern LDPE production systems.

Polymerization Initiator Market Competitive Landscape

The global polymerization initiator market is advancing toward high-purity organic peroxides and azo initiators, driven by EHS compliance, precision polymer engineering, and demand from EV, medical, and electronics sectors. Competition is defined by dust-free formulations, nitrile-free alternatives, and integration with advanced polymerization technologies.

Arkema Leads with Dust-Free Peroxide Innovation and Recyclable Resin Integration

Arkema S.A. is a global leader in polymerization initiators, advancing organic peroxide technology with a strong focus on safety and performance. Its Luperox® NeatCure® granular initiators, launched in 2025, offer dust-free handling and improved safety in extrusion and molding operations. The company demonstrated strong integration with Elium® thermoplastic resin at JEC World 2026, enabling recyclable composite structures for aerospace and wind energy applications. Arkema’s expertise in cross-linking peroxides supports faster curing cycles and enhanced production efficiency. Its expansion into high-performance polymers such as Zenimid™ polyimides and Kepstan® PEKK highlights the importance of precise initiation in extreme thermal environments. Strategy centers on sustainable polymerization, safety-driven innovation, and high-performance composite applications.

Nouryon Expands Asia Footprint with Metal Alkyls and MMAO Initiator Capacity

Nouryon is strengthening its position in polymerization initiators through aggressive expansion in Asia-Pacific, particularly China’s EV and solar markets. The company is doubling its triethylaluminum (TEA) capacity at its Jiaxing facility, a key co-catalyst in polyolefin production. It also plans to produce MMAO by 2027, supporting next-generation polyolefin elastomers used in solar encapsulation. The upcoming Organic Peroxides Innovation Center in Tianjin (2026) will accelerate localized R&D and application development. Nouryon’s integrated platform includes Perkadox® and Trigonox® initiators supported by advanced research infrastructure. Strategy emphasizes regional expansion, co-catalyst integration, and EV-driven polymer demand.

United Initiators Targets High-Purity Applications with Solar and Persulfate Solutions

United Initiators is a specialized leader in high-purity polymerization initiators, particularly persulfates and organic peroxides. Its CUROX® SOLAR range is engineered for EVA cross-linking in photovoltaic modules, ensuring long-term durability and optical performance. The company is expanding into precision industrial applications, promoting high-purity sodium and potassium persulfates for analytical and electronics use. Its TBHP and persulfate portfolio supports controlled radical polymerization across agrochemical and specialty resin synthesis. United Initiators remains critical to LDPE and PVC production through temperature-controlled radical initiation systems. Strategy focuses on purity-driven differentiation, renewable energy applications, and precision radical chemistry.

Evonik Focuses on Specialty Peroxides and Advanced Polymer Networks

Evonik Industries is optimizing its polymerization initiator portfolio toward high-margin specialty peroxide grades. Its joint venture with Fuhua in China is producing high-purity initiators for semiconductor and advanced electronics materials. Despite a 7% sales decline, Evonik maintained strong financial performance with €1.87 billion EBITDA in 2025 and a positive 2026 outlook. The creation of SYNEQT allows greater focus on advanced materials, including initiators for hydrogen economy applications and 3D printing polymers. Its crosslinkers support high-performance membranes, foams, and stimuli-responsive polymer systems. Strategy centers on specialty peroxide innovation, electronics-grade purity, and advanced material applications.

BASF Integrates CFRP Technology and XLPE Initiator Systems for Energy Applications

BASF SE is leveraging Controlled Free Radical Polymerization (CFRP) to enhance initiator performance in coatings and advanced materials. Its Nanjing production line strengthens supply of high-performance dispersants and polymerization systems for Asia-Pacific markets. The Irgastab® Cable KV 10 system highlights BASF’s role in peroxide-initiated XLPE production for high-voltage cable insulation. Through its VALERAS® platform, BASF is aligning initiators with sustainability and recyclability goals in plastics. The company also implemented pricing adjustments in 2026 due to tightening acrylate supply chains. Strategy emphasizes integrated polymerization systems, energy infrastructure applications, and sustainable chemistry.

FUJIFILM Wako Leads Azo Initiator Segment with Nitrile-Free and Low-Temperature Solutions

FUJIFILM Wako Pure Chemical Corporation dominates the azo initiator segment with high-purity, low-toxicity solutions. Its VA-044 initiator is widely used in emulsion polymerization for acrylamide and styrene, offering controlled radical generation at low temperatures. The company is advancing nitrile-free azo initiators as safer alternatives to AIBN, addressing tightening EHS regulations. With projected leadership in the 700-ton global water-soluble initiator market, Wako maintains a strong presence in biomedical and electronics applications. Its products are critical for electrophoresis gels and tissue-clearing technologies requiring ultra-low impurity levels. Strategy focuses on precision initiation, safety innovation, and high-purity specialty applications.

China: Policy-Led Scale-Up and Safety-Centric Initiator Localization

China’s polymerization initiator industry in 2025 is being reshaped by direct industrial policy intervention, capacity localization, and heightened safety oversight. In September 2025, the Ministry of Industry and Information Technology released the Work Plan for Stabilizing Growth in the Petrochemical and Chemical Industry (2025–2026), explicitly prioritizing high-end polyolefin initiators as part of a targeted 5% annual increase in industrial added value. This policy signal has accelerated investment in specialty initiator infrastructure. In October 2025, Nouryon announced the expansion of its Jiaxing facility to double capacity for triethylaluminum and other metal alkyl initiators, while also confirming the 2026 commissioning of an Organic Peroxides Innovation Center in Tianjin. These developments strengthen domestic supply security for highly reactive initiators used in advanced polyolefin systems.

Demand-side pull is intensifying from downstream energy and mobility sectors. To support rapid growth in photovoltaic installations, Nouryon confirmed plans to localize production of modified methylaluminoxane by 2027, a critical initiator component for polyolefin elastomers used in solar encapsulation films. In parallel, BASF commissioned a Controlled Free Radical Polymerization line in Nanjing in November 2025, enhancing the availability of advanced dispersants for automotive coatings that rely on tightly controlled initiator chemistry. Innovation capacity has also matured, with Nouryon’s Jiaxing R&D laboratory reaching full operational status in 2025, focusing on safer synthesis routes and higher process efficiency. Regulatory enforcement remains stringent. Under MIIT’s 2025 mandate, chemical parks are undergoing digital transformation audits that require AI-driven monitoring of volatile organic peroxide storage, reinforcing China’s shift toward safety-intensive, technology-led initiator manufacturing.

Germany: Sustainability Metrics, Regulatory Clarity, and Specialty Initiator Leadership

Germany’s polymerization initiator market in 2025 reflects a convergence of sustainability performance, regulatory recalibration, and high-value customer alignment. In November 2025, United Initiators achieved an EcoVadis Silver Medal with a score of 76 points, placing it in the 93rd percentile globally and signaling a sector-wide emphasis on ethical sourcing, process safety, and emissions management in organic peroxide production. Regulatory pressure temporarily eased when the European Commission confirmed the postponement of the REACH revision to 2026, granting manufacturers additional time to manage new registration requirements affecting polymer-bound and specialty initiators.

Competitiveness initiatives are also shaping the operating environment. Germany is actively engaged in negotiations around the Omnibus VI package proposed in July 2025, which aims to simplify chemical marketing rules while strengthening the position of small and mid-sized specialty initiator producers. Commercial partnerships underscore Germany’s role as a premium supplier market. United Initiators was named Supplier of the Year by allnex in July 2025 for its contributions to resilient initiator solutions used in industrial coatings and composite resins. At the strategic level, German chemical leaders aligned with the 2025 Technology Roadmap emphasizing transition finance mechanisms to decarbonize energy-intensive organic peroxide manufacturing. Together, these factors position Germany as a reference market for sustainable, compliance-ready initiator systems serving high-specification applications.

United States: Cost Pressures, Advanced Composites, and Energy Storage Pull

The United States polymerization initiator industry in 2025 is characterized by margin pressure, application-driven innovation, and expanding demand from advanced materials and energy storage research. In mid-2025, major U.S.-based initiator producers implemented portfolio-wide price adjustments, citing rising transportation and energy costs alongside compliance expenses linked to PFAS-free material transitions. Despite these pressures, innovation momentum remains strong. At CAMX 2025 in August, U.S. manufacturers showcased low-temperature initiator systems designed to improve cure cycle efficiency in aerospace composites and additive manufacturing resins, reflecting growing adoption of initiator-controlled processing in high-performance materials.

Environmental and governance transparency is increasingly influencing buyer selection. United Initiators published its second ESG report in late 2025, highlighting measurable reductions in the environmental footprint of its Elyria and Houston facilities. On the technology frontier, federal research grants awarded in 2025 prioritized solid-state and gel polymer electrolyte development for next-generation batteries. These programs are driving demand for ultra-high-purity initiators used in in-situ polymerization of battery separators and electrolyte matrices. As a result, the U.S. market is evolving toward a dual focus on compliance-driven cost management and innovation-led demand from aerospace, additive manufacturing, and energy storage ecosystems.

India: Policy Incentives and Downstream Polymer Expansion

India’s polymerization initiator market is undergoing structural expansion supported by policy incentives and rapid downstream petrochemical development. As of December 26, 2025, the Department of Pharmaceuticals and the Department of Chemicals continued inviting applications under the Production Linked Incentive Scheme, explicitly covering critical chemical intermediates such as polymerization initiators. This policy framework is encouraging domestic capacity additions and reducing reliance on imported persulfate, azo, and peroxide systems. Concurrently, petrochemical hub expansions led by HMEL and Reliance Industries in 2025 integrated dedicated units for polyacrylamide-based gels, triggering increased demand for localized initiator supply.

Sustainability and efficiency considerations are becoming differentiators. Songwon’s Panoli plant achieved 63% renewable energy sourcing in 2025, establishing a benchmark for low-carbon initiator production in South Asia. Demand modernization is further supported by the government’s ₹3,000 crore MSME subsidy scheme, which targets technological upgrades across 15,000 plastic processing units. These upgrades favor high-efficiency initiators that reduce polymerization waste and energy consumption. Collectively, India’s market trajectory is shaped by incentive-driven localization, downstream polymer diversification, and rising sustainability expectations.

Japan: Regulatory Precision and Medical-Grade Initiator Demand

Japan’s polymerization initiator industry in 2025 is defined by regulatory rigor and leadership in medical and low-carbon applications. The Ministry of Economy, Trade and Industry released its 2025 notification schedule for new chemical substances, requiring detailed physicochemical data for all new polymerization initiators exceeding one tonne per year. This framework reinforces Japan’s reputation for stringent pre-market evaluation and traceability in specialty chemicals. Demand for high-purity initiators remains strong in healthcare polymers. In January 2025, Japanese manufacturers finalized agreements for bio-stimulatory polymer fillers marketed under Lumina™, relying on initiators that meet exacting medical safety and consistency standards.

Long-term strategy is closely aligned with decarbonization objectives. Japan updated its Technology Roadmap for Transition Finance in 2025, directing funding toward innovative low-carbon initiator chemistries that support the country’s 2050 carbon-neutral target. This alignment between regulatory oversight, medical-grade demand, and transition finance positions Japan as a premium market for initiators where quality assurance and sustainability credentials are critical to supplier selection.

Comparative Snapshot of Country-Level Dynamics in Polymerization Initiators

Polymerization Initiator Market County Level Snapshot

|

Country

|

Strategic Focus Areas in 2025

|

Implications for Initiator Suppliers

|

|

China

|

High-end polyolefin initiators, AI safety monitoring, solar-driven demand

|

Rapid localization with stringent safety and digital compliance

|

|

Germany

|

Sustainability scoring, regulatory pause, specialty partnerships

|

Preference for compliant, high-value organic peroxide systems

|

|

United States

|

Cost pass-through, composites innovation, battery R&D

|

Demand for high-purity and low-temperature initiators

|

|

India

|

PLI incentives, petrochemical hub expansion, MSME upgrades

|

Rising domestic demand for efficient and localized initiators

|

|

Japan

|

New substance notifications, medical polymers, transition finance

|

Premium market for ultra-high-purity, low-carbon initiators

|

Polymerization Initiator Market Report Scope

Polymerization Initiator Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8 Billion

|

|

Market Size (2034)

|

$12.5 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Type (Organic Peroxides, Azo Initiators, Persulfates, Photo Initiators, Specialty Initiators), By Application (Polyethylene, Polyvinyl Chloride, Polystyrene, Acrylics & PMMA, Polypropylene, Unsaturated Polyester Resins), By End-Use Industry (Packaging, Automotive, Construction, Electronics, Medical)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nouryon, Arkema SA, United Initiators, BASF SE, Pergan GmbH, Shin-Etsu Chemical Co. Ltd., Adeka Corporation, Wacker Chemie AG, Evonik Industries AG, Songwon Industrial Co. Ltd., LyondellBasell Industries NV, Dow Inc., Vanderbilt Chemicals LLC, Sinopec, Akzo Nobel NV

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polymerization Initiator Market Segmentation

By Type

- Organic Peroxides

- Azo Initiators

- Persulfates

- Photo Initiators

- Specialty Initiators

By Application

- Polyethylene

- Polyvinyl Chloride

- Polystyrene

- Acrylics & PMMA

- Polypropylene

- Unsaturated Polyester Resins

By End-Use Industry

- Packaging

- Automotive

- Construction

- Electronics

- Medical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polymerization Initiator Industry

- Nouryon

- Arkema SA

- United Initiators

- BASF SE

- Pergan GmbH

- Shin-Etsu Chemical Co. Ltd.

- Adeka Corporation

- Wacker Chemie AG

- Evonik Industries AG

- Songwon Industrial Co. Ltd.

- LyondellBasell Industries NV

- Dow Inc.

- Vanderbilt Chemicals LLC

- Sinopec

- Akzo Nobel NV

*- List not Exhaustive