Market Overview: Food-Use Phase-Out, EV Insulation Demand, and Process Optimization Accelerate Azodicarbonamide Market

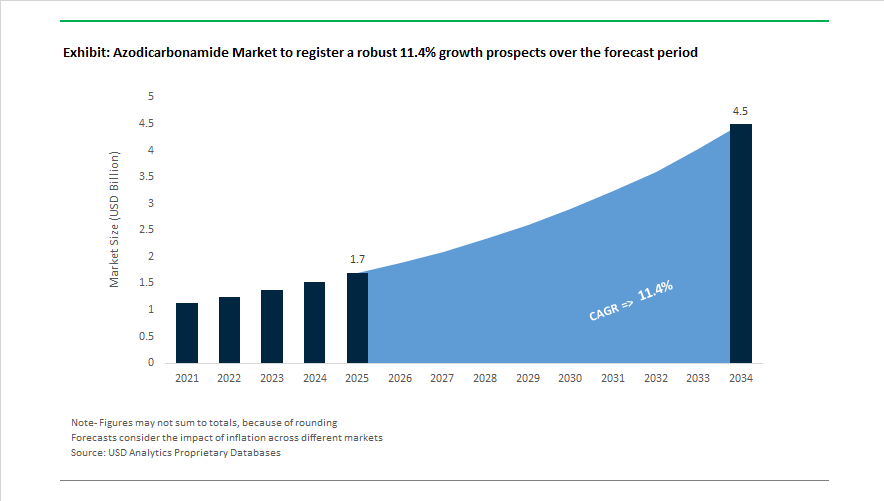

The azodicarbonamide market is valued at $1.7 billion in 2025 and is projected to reach $4.5 billion by 2034, expanding at a 11.4% CAGR. Market momentum is now concentrated in industrial azodicarbonamide blowing agents, ADC foaming agents, polymer foam additives, EVA foam production, PVC foaming additives, rubber blowing agents, and low-density polyolefin insulation foams. Structural change began during 2024–2025 when China’s GB 2760-2024 standard removed ADC from the national food additive list, effectively ending food-grade azodicarbonamide production in the world’s largest chemical manufacturing base. This regulatory shift followed earlier prohibitions in Europe and Australia and redirected global supply chains toward industrial-grade ADC for plastics, footwear, synthetic leather, and insulation materials. During the same period, vertically integrated producers such as Jiangsu SOPO and Jiangxi Selon mitigated feedstock volatility through control of hydrazine and urea inputs, stabilizing pricing when global urea spot values declined in mid-2024.

Industrial demand strengthened across Asia through 2024–2025. South Korea’s Kum Yang reported strong exports to Indonesia and Vietnam, reflecting rapid growth in EVA foam blowing agents used in footwear and sports equipment. Technology development accelerated in September 2025 when Shuntai New Materials introduced high-efficiency ADC foaming agents delivering gas yields of 200–220 ml per gram, improving cell uniformity and increasing finished product pass rates. Innovation also gained visibility at the November 2025 PVC Additives Technology Conference in China, where Hebei Guangxing Chemical highlighted advanced ADC formulations for PVC construction foams. Equipment upgrades across Vietnam and Indonesia in 2025 expanded the manufacturing base capable of processing premium ADC grades, strengthening Southeast Asia’s role in global export supply chains. At the same time, R&D progress enabled odor-reduced ADC grades for synthetic leather, supporting premium apparel applications requiring neutral sensory profiles.

Strategic portfolio realignment and regulatory review shaped the global outlook in 2025–February 2026. LANXESS divested its Urethane Systems business to UBE Corporation in April 2025 and later announced a global production optimization plan in August 2025, including closure of its Widnes site by the end of 2026. Sustainability performance reporting also influenced supplier positioning, with Nouryon confirming emission reductions and renewable energy adoption in May 2025. In February 2026, the U.S. Food and Drug Administration initiated a formal post-market safety reassessment of ADC, adding further scrutiny to its dual-use status. Meanwhile, ADC demand surged in EV battery pack insulation during 2024–2025, as low-density foams met UL-94 V-0 fire safety standards required for thermal-runaway mitigation.

Trends and Opportunities Reshaping Demand in the Azodicarbonamide (ADA) Market

Market Trend: Industry Restructuring Following the Global Phase-Out in Food Applications

Azodicarbonamide is undergoing one of the sharpest regulatory-driven repositionings in the specialty chemicals category. What was once a dual-use ingredient for food and industrial applications is now almost entirely an industrial-only chemical. As regulatory frameworks prioritize consumer exposure reduction, ADA is being actively withdrawn from bakery and flour-processing ecosystems across major economies.

India is now the largest example of full regulatory exclusion. In December 2025, the Ministry of Health confirmed that under the Food Safety and Standards Regulations, ADA is not approved for use in any category of food. Enforcement campaigns by FSSAI effectively removed ADA from bakery supply chains, replacing it with safer alternatives such as ascorbic acid and BHA.

The divergence between U.S. and OECD markets is strategically critical. While the U.S. FDA maintains ADA as GRAS (up to 45 ppm), market pressure — rather than law — has removed it from nearly every national bakery chain and private-label retailer. This uncouples regulatory legality from commercial viability, signaling that ADA’s food-grade category has structurally collapsed.

Compliance metrics from European agencies now show a 98% ADA-free certification rate in bakery exports, demonstrating that even where ADA was theoretically allowed, exporters have eliminated it to simplify market access. For ADA producers, this trend translates into a permanent shift: food-grade ADA has effectively reached end-of-life.

Market Trend: Purity-Led Consolidation and Reinvestment in Industrial ADA Capacity

As the food market disappears, ADA manufacturers are consolidating assets and moving toward high-purity formulations designed for polymeric foaming and advanced material processing.

India has emerged as the new global production hub. In August 2025, the DPL Group reported a surge in domestic demand for 99% purity ADA, enabling India to strengthen its export position across EVA foam footwear, consumer appliances, and automotive lightweighting.

High-purity ADA’s relevance is tied to material science performance. Lower-grade ADA can create voids, uneven cell structures, and failure rates in finished polymeric foams. 2025 foam-processing trials show that 99% ADA delivers significantly improved closed-cell uniformity, which is now mandatory for premium sports equipment and noise-absorption panels in automotive interiors.

Simultaneously, multinational manufacturers including Arkema, Lanxess, and Adeka have redirected R&D into formulated blowing-agent blends, adding activators such as zinc salts to reduce decomposition temperature and energy requirements. This shift reflects a broader restructuring trend: ADA is being re-engineered not as a volume commodity, but as an engineered additive with process-specific customization.

Market Opportunity: Lightweight Flame-Resistant PVC Foams for Construction and Infrastructure

The construction sector, driven by global urbanization and decarbonization policies, represents the largest structural growth area for industrial ADA. PVC foams created through ADA blow-molding are now widely used in lightweight partition panels, ceilings, insulation boards, and protective cable casings.

Technical insights published in February 2025 highlight that ADA-induced foaming can reduce PVC density by up to 40%, allowing for material cost savings while maintaining compressive strength — a critical parameter for high-rise building envelopes.

ADA’s strategic advantage in construction is its compatibility with intumescent (fire-retardant) systems. When used in PVC insulation layers, ADA supports char-forming behavior during fire exposure, enabling compliance with Euroclass B-s1, d0 safety standards increasingly required in new-build projects.

This demand is being heavily accelerated in APAC, where government-funded infrastructure pipelines in India, Indonesia, and Vietnam continue to add millions of square meters of residential and commercial floor space. For ADA suppliers, construction-linked PVC applications represent a price-stable, recurring procurement channel that replaces high-volume but low-margin bakery demand.

Market Opportunity: High-Purity ADA as a Precision Chemical for Aerospace and Defense Polymers

Beyond foaming technology, ADA is quietly gaining relevance in advanced polymer synthesis, which offers significantly higher margins and strategic importance.

In aerospace-grade materials, ADA is used as a dehydrogenation agent in the synthesis of Poly(p-phenylene benzobisoxazole) (PBO) — a high-modulus fiber used in ballistic armor, aerospace tethering lines, and space-grade structural materials. PBO’s thermal resistance, reportedly exceeding 650°C, is critical for hypersonic aircraft components and next-generation defense contracting.

Additionally, ADA-mediated cross-linking improves dielectric stability in polyimide films used in satellites, where radiation exposure makes standard polymer films prone to degradation. This category is experiencing investment tailwinds from the expanding global space economy.

To serve this segment, suppliers are now commercializing "Electronic Grade ADA", designed with zero-defect impurity controls for semiconductor and aerospace use. The specification requirement is so strict that even trace metallic ions are considered catastrophic to high-voltage components. As semiconductor fabs and satellite integrators tighten procurement qualification, ADA producers who adopt semiconductor-grade quality systems will secure multi-year locked-in supply contracts.

Azodicarbonamide Market Share and Segmentation Insights

Application Market Share: Chemical Blowing Agents Dominate While Flour Treatment Nears Structural Exit

In 2025, chemical blowing agents account for 72% of total azodicarbonamide (ADC) market revenue, reinforcing ADC’s position as the industry benchmark for foamed plastics and rubber production. Its high gas yield, controlled decomposition temperature, and ability to generate uniform fine-cell structures make it indispensable in PVC, polyethylene, polypropylene, and elastomer foaming applications. However, European markets are witnessing substitution pressure from endothermic blowing agents and CO₂-based physical foaming technologies aligned with sustainability mandates. Polymer crosslinking remains a high-value niche, enhancing rheology and thermal stability in wire and cable jacketing and pipe insulation, though volumes remain constrained. Flour bleaching and dough conditioning is in severe structural decline, banned across the EU and multiple Asia-Pacific countries due to semicarbazide (SEM) concerns, persisting mainly in the US and Middle East under FDA GRAS status. Laboratory reagent applications are negligible and stagnant.

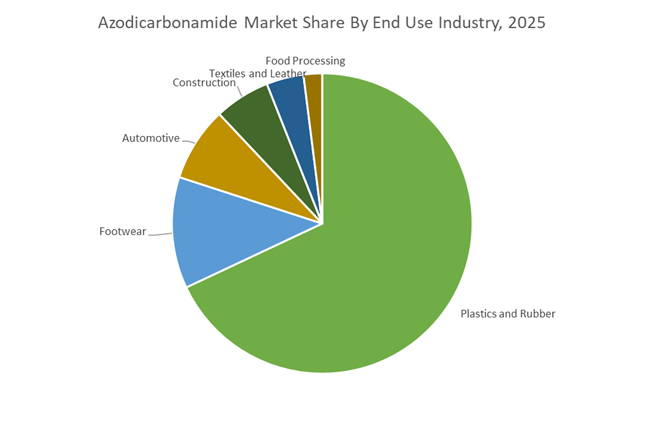

End-Use Industry Market Share: Plastics and Rubber Anchor Demand Amid Regulatory and Clean-Label Headwinds

By end-use, plastics and rubber represent 68% of global ADC consumption in 2025, driven by demand for flexible PVC flooring, crosslinked polyethylene foam, and nitrile rubber gaskets. Asia-Pacific accounts for over 60% of global volume, with China serving as the manufacturing hub for foamed polymer components. Footwear remains a traditional stronghold, where ADC enables lightweight, cushioned midsoles in athletic shoes and sandals, though premium segments are gradually shifting toward EVA bead physical foaming technologies. Automotive applications remain stable, supporting acoustic insulation foams and battery casing seals in both ICE and EV platforms. Construction remains underpenetrated, as rigid insulation increasingly favors hydrocarbon-blown polyurethane systems. Textiles and synthetic leather applications are mature but steady, while food processing is functionally terminal, with multinational bakeries eliminating ADC to meet global clean-label commitments, driving the segment toward sub-1% share by 2030.

Azodicarbonamide Market Competitive Landscape

The global azodicarbonamide (ADC) market in 2026 is characterized by technological refinement, vertical integration into hydrazine hydrate supply chains, and increasing regulatory scrutiny around occupational safety and environmental compliance. Leading producers are focusing on precision-controlled decomposition temperatures, ultra-fine particle engineering, and activated ADC blends for temperature-sensitive polymers. Demand remains strong across EVA footwear, PVC construction materials, synthetic leather, automotive interiors, and lightweight insulation foams. Strategic investments in wastewater treatment, eco-grade formulations, and masterbatch integration are reshaping competitive positioning, particularly in Asia-Pacific, which remains the dominant production and export hub for ADC blowing agents.

Technological convergence in ADC and battery materials by Kum Yang Co., Ltd.

Kum Yang is a global leader in azodicarbonamide blowing agents through its CELLCOM AC series, offering customized ADC grades with precisely controlled decomposition temperatures and particle size distributions. Its advanced R&D infrastructure enables tailored solutions for EVA shoe soles, PVC wallpaper, and PE insulation foams. In 2025 and 2026, the company strategically leveraged strong cash flow from its blowing agent business to fund expansion into secondary battery materials, including silicon anodes, and initiated construction of a Gigafactory in Busan. This “Technological Convergence” strategy positions Kum Yang as both a dominant ADC producer and a key participant in the electric vehicle supply chain.

High-purity low-residue ADC leadership from Otsuka Chemical Co., Ltd.

Otsuka Chemical leads the premium segment with its UNIFOAM® AZ series, recognized for high gas yield and minimal mold plate-out in precision injection molding. The company specializes in high-purity, low-residue azodicarbonamide tailored for electronics-grade and automotive interior applications, where odor neutrality and fine-cell morphology are critical. In late 2025, Otsuka expanded eco-grade ADC production designed to reduce ammonia release during processing, aligning with 2026 workplace air quality standards. Through its Lautan Otsuka Chemical joint venture in Indonesia, Otsuka integrates Japanese technology with Southeast Asian manufacturing scale, strengthening its regional supply hub across the APAC automotive and plastics markets.

Cost-advantaged vertical integration by Jiangxi Selon Industrial Co., Ltd.

Jiangxi Selon Industrial is a primary global volume driver in the azodicarbonamide export market, supported by full vertical integration into hydrazine hydrate production. This integration provides significant cost advantages and resilience against precursor price volatility. In early 2026, the company upgraded its Leping City facility with advanced wastewater treatment and hydrazine recovery systems to comply with China’s Green Smelting mandates. Selon reported strong export growth into Southeast Asian footwear and textile hubs, supplying ADC for the expanding vegan leather segment. Its strategic focus on environmental leadership ensures operational continuity amid tightening Chinese environmental regulations affecting competing producers.

Activated low-temperature ADC solutions from Ajanta Chemical Industries

Ajanta Chemical Industries is the leading Indian azodicarbonamide supplier, serving infrastructure and construction-driven PVC demand across South Asia and the Middle East. Its portfolio includes activated ADC blends that decompose at lower temperatures, typically between 140°C and 160°C, making them suitable for temperature-sensitive rubber and PVC compounds. In 2025, Ajanta expanded its Specialty Additives division to supply synergists and kickers such as zinc oxide and urea, offering turnkey foaming systems for SMEs. The development of a granular, non-dusting ADC variant in late 2025 further aligns with evolving 2026 occupational health and plastics compounding safety standards.

Ultra-fine ADC expansion strategy at Weifang Yaxing Chemical Co., Ltd.

Weifang Yaxing Chemical leverages scale and cluster-based efficiencies in Shandong to remain highly competitive in global ADC pricing. In late 2025, the company shifted toward ultra-fine powder grades aimed at high-end synthetic leather and luxury automotive upholstery applications. Yaxing integrates azodicarbonamide production with its extensive chlorinated polyethylene business, enabling bundled additive solutions for PVC processors and cable manufacturers. Its strategic focus on stabilized ADC blends helps prevent premature decomposition during transportation in high-heat regions such as the Middle East, supporting reliable export performance in temperature-sensitive markets.

Precision-controlled ADC masterbatches from Zhejiang Hytitan New Material Co., Ltd.

Hytitan represents a next-generation azodicarbonamide manufacturer focused on customized masterbatch solutions and sustainable foam innovation. The company markets REACH- and RoHS-compliant eco-conscious ADC grades engineered for higher gas yield and reduced usage rates. Its precision-controlled expansion technology enables uniform cell density, reducing raw material consumption in foam components by up to five%. Hytitan’s product portfolio emphasizes pre-dispersed ADC masterbatches, eliminating powder handling risks for automotive part injectors and plastics converters. Advanced in-house testing laboratories allow close OEM collaboration in developing lightweighting additives for 2026 model-year vehicles across automotive and consumer goods segments.

China Azodicarbonamide Market: From Food Additive Exit to Industrial-Grade Consolidation

China has decisively repositioned azodicarbonamide as a purely industrial chemical, following the January 2025 enforcement of GB 2760-2024, which removed ADC from the national list of approved food additives. This regulatory phase-out redirected the country’s vast installed capacity toward polymer foaming, synthetic leather, and electronics housing applications. By late 2025, export governance tightened further as the Ministry of Commerce integrated high-purity blowing agents into its enhanced export review framework to protect domestic supply chains supporting New Energy Vehicle manufacturing.

Industrial modernization is reinforcing this shift. A government-backed $8 billion investment program announced in 2025 is upgrading textile and vegan leather clusters, incentivizing low-emission ADC grades for synthetic substrates. Production has also been consolidated into state-monitored Green Chemical Zones in Jiangsu and Shandong, where real-time monitoring of hydrazine-hydrate precursors is mandated from 2026 to control environmental runoff. On the performance front, domestic producers such as Jiangxi Selon Industrial and Jiangsu SOPO scaled ultra-pure ADC grades exceeding 99% purity in 2025 to support high-speed PVC extrusion for electronics housings, underscoring China’s move toward precision industrial foaming rather than volume commodity supply.

India Azodicarbonamide Market: Infrastructure-Led Demand and EV-Centric Customization

India’s azodicarbonamide demand trajectory is being shaped by infrastructure expansion and EV localization, supported by targeted policy instruments. In mid-2025, the government confirmed INR 40 crore for new Plastic Parks, catalyzing domestic consumption of ADC in foamed PVC pipes, insulation boards, and construction materials. Parallelly, the Production Linked Incentive scheme for specialty chemicals has encouraged Indian manufacturers such as Ajanta Chemical Industries and Nikunj Chemicals to expand capacity, reducing reliance on imports for automotive interior components.

Innovation is increasingly application-specific. In late 2025, Indian formulators introduced custom ADC grades optimized for EVA molded sheets used in battery cushioning and thermal insulation for electric two-wheelers. At the same time, regulatory alignment with global food safety trends is closing legacy markets. Updated 2025 guidelines from the FSSAI restricting ADC in flour processing have effectively eliminated food-sector demand, accelerating a full pivot toward industrial foaming, footwear, and automotive polymers. India’s ADC market is therefore consolidating around construction scale and EV-driven specialization.

United States Azodicarbonamide Market: Food Reformulation Pressure and Lightweighting Research

In the United States, azodicarbonamide is increasingly defined by regulatory scrutiny and industrial research, rather than legacy food applications. Anticipation of the California Food Safety Act, effective January 2027, triggered aggressive reformulation across bakery supply chains during 2025, removing ADC and opening space for clean-label alternatives. This momentum was reinforced in May 2025 when the FDA initiated a new post-market review framework, placing ADC on a high-priority safety re-evaluation list.

Conversely, industrial and energy applications are expanding. The U.S. Department of Energy provided research grants in late 2025 for ADC-enhanced polymer composites aimed at reducing vehicle curb weight by around 15% in heavy-duty electric trucks. In packaging, state-level mandates in the Northeast effective from 2026 are pushing foam producers toward lower-VOC blowing systems, where specialized ADC masterbatches offer better compliance than traditional liquid agents. The U.S. market is thus splitting clearly between regulatory exit in food and R&D-led growth in advanced materials.

South Korea Azodicarbonamide Market: Precision Foaming for Battery and Optics Applications

South Korea’s azodicarbonamide landscape is strongly technology-driven, aligned with the country’s battery and electronics ecosystems. In late 2025, Kum Yang Co., Ltd. announced a next-generation ADC blowing agent engineered for solid-state battery enclosures, emphasizing uniform cell morphology to enhance thermal stability at high discharge rates. This positions ADC as a functional enabler in advanced energy storage rather than a generic foaming chemical.

Manufacturing sophistication is also rising. By 2026, major chemical hubs transitioned to AI-driven decomposition monitoring, enabling ADC activation within a narrow 220 to 225 degree Celsius window. This precision ensures zero-residue foaming, critical for optics packaging and high-spec electronic components. South Korea’s approach highlights process control and performance reliability as the core competitive differentiators.

European Union (Germany and France) Azodicarbonamide Market: Compliance Monitoring and Energy Efficiency

In the European Union, azodicarbonamide remains under regulatory surveillance rather than outright prohibition. As of early 2026, the European Chemicals Agency continues to monitor ADC under the REACH Candidate List of Substances of Very High Concern. Any article containing more than 0.1% ADC by weight must be declared in the SCIP database, increasing transparency obligations for converters and OEMs.

Despite this scrutiny, industrial use continues through efficiency-driven innovation. German processors reported in 2025 that new-generation ADC grades with tailored activators reduced oven electricity consumption by 18% in recycled PVC profile production by lowering activation temperatures. This aligns with Europe’s broader decarbonization agenda, positioning ADC as a process efficiency tool rather than a volume growth chemical.

Azodicarbonamide Industry Positioning by Country

Azodicarbonamide Market County Level Snapshot

|

Country / Region

|

Regulatory Direction

|

Industrial Focus

|

|

China

|

Food ban, export controls

|

Ultra-pure ADC for PVC, electronics, synthetic leather

|

|

India

|

Food restriction, PLI support

|

Construction foams and EV battery components

|

|

United States

|

Food safety re-evaluation

|

Lightweight composites and low-VOC packaging foams

|

|

South Korea

|

Technology-led adoption

|

Precision foaming for batteries and optics

|

|

EU (Germany/France)

|

SVHC monitoring under REACH

|

Energy-efficient foaming in recycled PVC

|

Azodicarbonamide Market Report Scope

Azodicarbonamide Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2034)

|

$4.5 Billion

|

|

Market Growth Rate

|

11.4%

|

|

Segments

|

By Grade (Industrial Grade, Ultra Pure Grade, Modified Grades, Food Grade), By Application (Chemical Blowing Agent, Flour Bleaching and Dough Conditioning, Polymer Crosslinking Agent, Laboratory Reagent), By End Use Industry (Plastics and Rubber, Automotive, Construction, Footwear, Textiles and Leather, Food Processing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kum Yang Co Ltd, Otsuka Chemical Co Ltd, Arkema, Lanxess AG, Honeywell International Inc, Weifang Yaxing Chemical, Jiangsu SOPO Group, Jiangxi Selon Industrial, Ajanta Chemical Industries, Abtonsmart Chemicals Group, Nikunj Chemicals, Shandong Rike Chemical, Adeka Corporation, Sinopec Group, Evonik Industries AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Azodicarbonamide Market Segmentation

By Grade

- Industrial Grade

- Ultra Pure Grade

- Modified Grades

- Food Grade

By Application

- Chemical Blowing Agent

- Flour Bleaching and Dough Conditioning

- Polymer Crosslinking Agent

- Laboratory Reagent

By End Use Industry

- Plastics and Rubber

- Automotive

- Construction

- Footwear

- Textiles and Leather

- Food Processing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Azodicarbonamide Industry

- Kum Yang Co Ltd

- Otsuka Chemical Co Ltd

- Arkema

- Lanxess AG

- Honeywell International Inc

- Weifang Yaxing Chemical

- Jiangsu SOPO Group

- Jiangxi Selon Industrial

- Ajanta Chemical Industries

- Abtonsmart Chemicals Group

- Nikunj Chemicals

- Shandong Rike Chemical

- Adeka Corporation

- Sinopec Group

- Evonik Industries AG

*- List not Exhaustive