Industrial Water Treatment Chemicals Market: Growth Analysis, Value Projections, and Industry Forecast to 2034

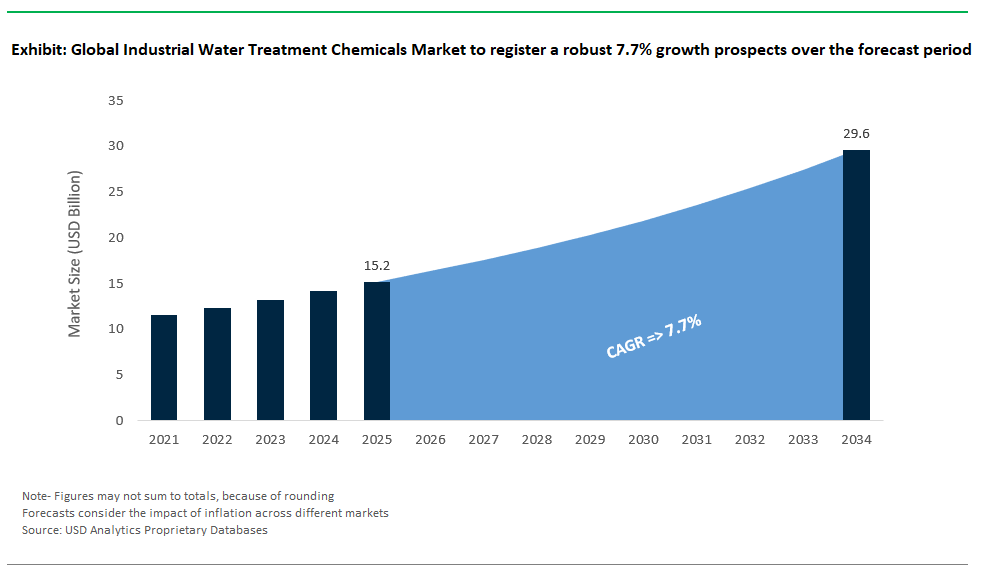

The industrial water treatment chemicals market is valued at $15.2 billion in 2025 and projected to reach $29.6 billion by 2034, reflecting a CAGR of 7.7%. The sector remains foundational to operational continuity across energy, manufacturing, and resource-intensive sectors, with chemical formulations engineered to address a diverse spectrum of scaling, corrosion, biological fouling, and effluent compliance challenges. In open-loop cooling systems, standard practice involves blended treatments combining scale and corrosion inhibitors dosed at 50–200 ppm, aligning with CTI Guidelines to manage calcium carbonate precipitation and galvanic degradation in multi-metal piping systems.

Microbial fouling, particularly in biofilm-prone areas such as fill media and basin walls, is typically mitigated using biocides like glutaraldehyde, which achieves 4-log biofilm reduction within 15–75 ppm dosage ranges, even under organic load stress. In closed-loop systems, which demand long-term corrosion protection under low-oxygen, low-flow conditions, molybdate-based inhibitors are favored for their anodic protection properties used at concentrations of 100–300 ppm, validated under ASTM D1384 protocols for carbon and mild steel.

Beyond system conditioning, chemical treatments are also playing a critical role in environmental compliance, particularly in managing chemical oxygen demand (COD) in industrial effluents. Advanced oxidation processes such as Fenton’s reagent are capable of degrading over 90% of recalcitrant organic loads, enabling facilities to meet increasingly stringent discharge limits without resorting to complex biological polishing steps.

With tightening regulatory frameworks, water reuse mandates, and decarbonization pressures driving operational transformation, chemical suppliers are under increasing pressure to deliver high-efficiency, multi-functional products that integrate seamlessly with automation, monitoring, and zero-liquid discharge (ZLD) architectures. This is positioning industrial water treatment chemicals not just as consumables, but as integral components of risk-managed, efficiency-optimized water systems.

Digital Innovation and Sustainability Drive the Evolution of Industrial Water Treatment Chemicals Market

Market Trend: Smart, Sustainable, and Digitally Optimized Treatment Chemicals Redefine Industrial Water Management

The industrial water treatment chemicals market is undergoing a fundamental evolution as sustainability imperatives, regulatory mandates, and Industry 4.0 technologies converge to reshape the chemical selection and dosing paradigm. Traditional manual dosing of commodity inhibitors, coagulants, and disinfectants is rapidly being displaced by precision, AI-driven systems integrated with sustainable, bio-derived formulations. A defining regulatory catalyst is the EPA’s 2024 PFAS rule, which bans many fluorinated surfactants long used in cooling and process water applications. This has led to accelerated adoption of green alternatives like Ecolab’s EnviroTru. In parallel, the EU’s Corporate Sustainability Reporting Directive (CSRD) mandates real-time disclosure of water usage, discharge quality, and chemical inputs, propelling the integration of IoT-enabled chemical monitoring and metering. Industry leaders are responding with tools that dynamically optimizes corrosion inhibitor dosages based on sensor feedback cutting overuse and preventing under-dosing that leads to asset degradation. Siemens’ Process Water Analytics platform predicts scale deposition and biofouling risks, reducing unplanned shutdowns in power and refining applications. This digital transformation dovetails with the rise of the circular water economy, where chemical formulations must support advanced reuse systems such as Zero Liquid Discharge (ZLD). Dow’s Texas plant exemplifies this shift, combining antiscalants with electrodialysis to recycle its process water and generate annual savings of few millions. In the mining sector, green flocculants are enabling both water reuse and critical mineral recovery meeting rising demand for lithium, rare earths, and copper under global energy transition mandates. As water becomes a strategic input in decarbonized manufacturing, industrial water treatment chemicals are no longer commodity additives they’re enablers of compliance, efficiency, and competitive differentiation.

Market Opportunity: Hydrogen Economy and Carbon Capture Infrastructure Drive High-Value Chemical Demand

The next major frontier for industrial water treatment chemical growth lies in supporting new energy systems particularly green hydrogen production, carbon capture and storage (CCUS), and high-performance data infrastructure each of which introduces extreme water quality and chemical control requirements. In electrolytic hydrogen production, ultrapure water is a non-negotiable feedstock, with conductivity targets below 0.1 µS/cm to avoid catalyst poisoning. Suez’s HyPure™ ion exchange resins, engineered for trace contaminant removal, offer double the resin life at half the cost of traditional demineralization routes a game-changer as EU Hydrogen Bank subsidies drive $500M+ in new electrolyzer capacity by 2030. Similarly, in CCUS systems, chemical degradation in CO₂ absorber columns creates scaling, foaming, and solvent loss challenges. Solvay’s AmineGuard™ inhibitor platform is extending amine solvent life by 2x and cutting annual OPEX by $1.5 million per plant. Even outside the energy sector, adjacent industries such as data centers are emerging as high-value chemical consumers. Microsoft’s hyperscale Dublin campus, for instance, uses Nalco’s 3D TRASAR™ microbial control system in closed-loop cooling systems to mitigate Legionella risks without introducing chlorine-based corrosion threats demonstrating that chemical precision, safety, and digital integration command premium pricing. Across sectors, the demand for treatment chemicals that enable energy transition infrastructure, support zero-downtime mandates, and align with ESG reporting frameworks is creating a bifurcated market: while bulk chemical margins shrink, specialty, high-performance, and digitally bundled offerings are capturing strategic budget allocations. This is the era where smart chemistry enables smart infrastructure.

Competitive Landscape: Industrial Water Treatment Chemicals Market

The industrial water treatment chemicals market features a few dominant players providing complete solutions, along with several specialized companies focused on product innovation and specific application performance. Ecolab, through Nalco Water, has a strong presence by offering a full range of specialty chemicals along with automation platforms like 3D TRASAR. This combination of chemistry with digital monitoring and onsite service enables Ecolab to serve various industries, from power generation to refining. They help clients optimize water use, manage scaling and corrosion, and comply with stricter discharge regulations.

In chemical manufacturing, BASF and SNF Floerger are vital to the market's supply chain. BASF uses its global production network to deliver important compounds like scale inhibitors, dispersants, and organic biocides to both end-users and independent formulators. SNF, on the other hand, holds a large share of the synthetic flocculant market, especially polyacrylamide-based products for sludge dewatering, clarifiers, and solids separation. Its integrated model and global production reach make it a key supplier in sectors such as mining, oil and gas, and textiles, where handling high solids is essential.

Solenis and Kemira work at the challenging intersection of water treatment and process chemistry. Both companies are known for customizing solutions to address specific industry needs. Solenis focuses on water-intensive industries like pulp and paper and petrochemicals, offering high-performance polymers and coagulants supported by site-optimization programs. Kemira excels in wet-end process chemistry and municipal-industrial effluent treatment, using advanced polymer and coagulant technologies to meet strict phosphorus discharge standards and reduce sludge volumes.

Kurita Water Industries emphasizes innovation, particularly in Asia and the electronics sector. The company focuses on accurate chemical dosing, high-frequency monitoring, and energy-efficient formulas, which are important for industries needing ultrapure water, like semiconductors and power plants. Kurita also promotes strategies that reduce chemical use without sacrificing system protection.

Meanwhile, the merger of Veolia Water Technologies and SUEZ has brought together two of the largest industrial water solution portfolios in the world. Their combined platform now includes traditional treatment chemicals, advanced membrane filtration, biological treatment, and integrated digital tools like AQUADVANCED for remote system control. Their strength lies in providing complete water management across complex industrial systems, from raw water intake to tertiary effluent reuse.

Lastly, Dow's water technologies division supports the chemical market from a materials science perspective. Although Dow does not supply finished chemical blends, it provides essential infrastructure such as ion exchange resins, reverse osmosis membranes, and ultrafiltration media. These materials enable chemical treatment programs to meet goals for purity, throughput, and recovery in sectors like chemicals, food processing, and pharmaceuticals.

Industrial Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

By Type of Chemical: Corrosion & Scale Inhibitors Lead While Ion Exchange Resins Grow Fastest

Corrosion and scale inhibitors hold the largest share of the industrial water treatment chemicals market, accounting for approximately 21.9% of the market in 2025. These chemicals are essential for preventing fouling and metal degradation in boilers, heat exchangers, and cooling systems, ensuring operational continuity, energy efficiency, and equipment longevity. Their critical function in both high- and low-pressure systems makes them indispensable across industries such as power generation, petrochemicals, and manufacturing. On the other hand, ion exchange resins are emerging as the fastest-growing category, projected to expand at a CAGR of 8.1% from 2025 to 2034. Their growth is fueled by rising demand for ultrapure water in electronics, semiconductors, and pharmaceuticals, where stringent water quality standards require highly efficient ion removal technologies. Membrane antiscalants also show robust performance with strong adoption in reverse osmosis (RO) and nanofiltration (NF) systems across industrial desalination and recycling setups. Cleaning and descaling chemicals, oxygen scavengers, defoamers, and sludge conditioners continue to support various stages of industrial water treatment, while biocides remain integral for controlling microbial growth in closed and open-loop systems.

By Application: Cooling Water Treatment Dominates While Water Reuse/Recycling Grows Fastest

Cooling water treatment leads all application segments, capturing approximately 32.6% of the industrial water treatment chemicals market in 2025. The dominance of this segment stems from its widespread use in large-scale industrial cooling towers, HVAC systems, and recirculating loops across energy-intensive sectors. The need for effective chemical control of scaling, corrosion, and microbial growth drives consistent demand for multi-component formulations. In contrast, the water reuse and recycling segment is expanding at the fastest pace, with an anticipated CAGR of 9.2% through 2034. This rapid growth is attributed to global shifts toward sustainable water management, driven by tightening discharge norms, freshwater scarcity, and corporate commitments to zero-liquid discharge and closed-loop operations. Desalination also demonstrates strong momentum, especially in water-stressed geographies, where membrane systems require advanced chemical support to maintain system integrity. Meanwhile, wastewater treatment and process water conditioning continue to see increased chemical use in response to rising industrial output and stricter effluent quality standards, positioning these segments as vital pillars of the market’s overall growth.

.png)

United States Sets the Pace in Industrial Water Treatment Chemicals Market with Regulatory Focus and Digital Innovation

The United States leads the global industrial water treatment chemicals market, underpinned by substantial infrastructure investments and cutting-edge technological adoption. The U.S. Environmental Protection Agency (EPA) is at the forefront, prioritizing advanced chemical solutions for the treatment of persistent contaminants such as PFAS and 1,4-dioxane. This regulatory environment is accelerating R&D into specialized chemicals capable of degrading tough pollutants and enabling water reuse, essential for industrial sustainability. The U.S. is also embracing digital transformation, with companies deploying AI-driven predictive maintenance and monitoring systems for real-time chemical dosing optimization, resulting in reduced consumption, higher efficiency, and lower operational costs.

Cooling and boiler water treatment remains a key market, driving consistent demand for scale inhibitors, corrosion inhibitors, and oxygen scavengers to safeguard industrial assets. Meanwhile, the focus on advanced chemical solutions for industrial wastewater is intensifying, as industries must meet stringent discharge standards and pursue water recycling initiatives. These dynamics are positioning the United States as both a technological leader and a key growth engine for the global industrial water treatment chemicals sector.

China Drives Industrial Water Treatment Chemicals Market with Policy Integration and High-Tech Solutions

China’s industrial water treatment chemicals market is surging, propelled by rapid industrialization and a top-down policy framework that embeds water governance in national strategy. The "Water Ten Plan" and "Dual Carbon" goals have galvanized investment in advanced water treatment technologies, including AI-driven process control, membrane localization, and low-carbon solutions. The government is channeling significant funding to upgrade both municipal and industrial wastewater facilities, requiring adoption of advanced chemical treatments to meet increasingly strict discharge standards.

Innovation is a central theme in China, with domestic enterprises developing eco-friendly, cost-effective chemical solutions such as electron beam technology for treating complex industrial effluents. These advancements support water reuse and resource recovery, crucial for achieving China’s dual goals of economic growth and environmental protection. As a result, China’s market is both a major consumer and a hotbed of innovation for industrial water treatment chemicals worldwide.

Germany Leads Sustainable Industrial Water Treatment Chemicals Market with High-Performance and Circular Solutions

Germany’s industrial water treatment chemicals market is defined by its strong regulatory framework and commitment to sustainability. Compliance with the German Water Resources Act and the EU Water Framework Directive compels industries to adopt high-performance, eco-friendly chemical treatments that support strict discharge and resource efficiency mandates. German firms like EnviroChemie are leading the charge with system solutions and laboratory-developed chemicals tailored for industrial water treatment and reuse.

A core market trend is the emphasis on circular economy models and zero-liquid discharge (ZLD) systems, which rely on efficient chemicals to recover valuable materials from wastewater. The BWT AQAtherm product line showcases specialized solutions for heating systems, using low-salt treated water to mitigate corrosion and microbiological growth. Germany’s combination of innovation, regulation, and a robust industrial base makes it a bellwether for the global shift towards sustainable, resource-efficient water treatment chemicals.

India Accelerates Industrial Water Treatment Chemicals Market with Policy Incentives and Water Reuse Mandates

India’s industrial water treatment chemicals market is expanding rapidly, supported by progressive government policies and a national agenda focused on water conservation and reuse. The Central Pollution Control Board (CPCB) has introduced stringent new discharge standards for sewage treatment, effective 2025, making advanced chemical solutions mandatory for compliance. A landmark mandate requires all thermal power plants within 50 km of a sewage treatment facility to use treated sewage water for non-potable purposes, creating a large, guaranteed demand for water treatment chemicals.

Financial incentives including subsidies for recycling plants, tax deductions, and soft loans are spurring investments in water treatment infrastructure and technology. India’s Confederation of Indian Industry (CII) is also prioritizing corrosion prevention with its “National Mission on War Against Corrosion.” This convergence of regulation, incentives, and industrial growth is transforming India into a major market for advanced and sustainable industrial water treatment chemicals.

Japan Innovates Industrial Water Treatment Chemicals Market with Resource Recovery and High-Purity Solutions

Japan’s industrial water treatment chemicals market is characterized by technological sophistication and a relentless drive for high-purity, resource-efficient solutions. Japanese companies are global leaders in customized chemical and technology offerings for industries such as power, pulp and paper, and food and beverage. Oji Holdings’ expertise in papermaking, for example, enables them to optimize chemical dosing with advanced jar testing and tailored formulations.

A key market trend is the push for resource recovery exemplified by “Rephosmaster,” a technology that recovers high-purity phosphorus from sewage for reuse. Japan’s focus extends to pioneering water treatment technologies for extreme environments, including pilot projects for lunar water purification. These initiatives underscore Japan’s commitment to sustainable innovation and the circular economy in industrial water management.

Brazil Expands Industrial Water Treatment Chemicals Market with Infrastructure Overhaul and Private Investment

Brazil’s industrial water treatment chemicals market is undergoing robust growth, propelled by the nation’s new sanitation regulatory framework and ambitious universal access targets for potable water by 2033. Large-scale public-private partnerships are driving the construction and modernization of water and wastewater treatment facilities, all of which require sophisticated chemical solutions. The oil and gas industry is a major demand driver, with consistent needs for corrosion and scale inhibitors to maintain infrastructure integrity in both onshore and offshore operations.

Brazil’s National Policy for Water Resources is promoting decentralized, participatory management, and water use charges, encouraging industries to adopt efficient, eco-friendly chemical treatments. As new industrial chemical regulations are developed, the market is expected to become even more competitive and innovation-driven.

United Kingdom Modernizes Industrial Water Treatment Chemicals Market with Regulatory Investment and Circular Strategies

The United Kingdom is reshaping its industrial water treatment chemicals market through regulatory reform, infrastructure investment, and a focus on environmental stewardship. The government’s “Plan for Water” and Ofwat’s £104 billion investment plan (2025–2030) are doubling down on infrastructure upgrades and new chemical technologies designed to halve sewage spills and tackle pollutants such as microplastics and PFAS. Companies are deploying advanced filtration and chemical treatments to meet tough new discharge limits.

The UK market is also advancing circular economy strategies, with growing adoption of resource recovery processes such as pyrolysis and hydrothermal oxidation (HTO) for sewage sludge. These integrated approaches create opportunities for specialized chemicals that support both compliance and value recovery, positioning the UK as a leader in sustainable industrial water management.

South Korea Advances Industrial Water Treatment Chemicals Market with Automation and Precision Dosing

South Korea’s market for industrial water treatment chemicals is experiencing rapid growth, underpinned by industrial expansion and the rise of automation. Manufacturing, power generation, and chemicals are the primary sectors driving demand, with the cooling and boiler segments being especially significant. The implementation of Industry 4.0 solutions and automatic dosing technologies enables more precise and efficient use of treatment chemicals, supporting both operational efficiency and environmental compliance.

South Korea’s power sector including thermal and nuclear plants is a key market, with ongoing infrastructure investments requiring high-quality chemical solutions to maintain system reliability. The country’s stable political environment and advanced infrastructure attract foreign investment, making South Korea a competitive and innovative hub for industrial water treatment technologies.

Industrial Water Treatment Chemicals Market Report Scope

Industrial Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.2 Billion

|

|

Market Size (2034)

|

$29.6 Billion

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Softeners, Oxygen Scavengers, Defoamers and Antifoaming Agents, Sludge Conditioners, Membrane Performance Enhancers/Antiscalants, Cleaning and Descaling Chemicals, Ion Exchange Resins, Other Specialty Chemicals), By Application (Boiler Water Treatment, Cooling Water Treatment, Process Water Treatment, Wastewater Treatment, Water Reuse and Recycling, Desalination), By End-User Industry (Power Generation, Oil and Gas, Chemical and Petrochemical, Food and Beverage, Pulp and Paper, Mining and Metallurgy, Textile, Pharmaceutical, Automotive, Electronics and Semiconductors, Other Manufacturing Industries

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), BASF SE (Germany), Solenis LLC (U.S.), SUEZ SA (France), Kemira Oyj (Finland), Kurita Water Industries Ltd. (Japan), The Dow Chemical Company (U.S.), Veolia Water Technologies (France), SNF Floerger (France), Buckman (U.S.),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Inorganic Coagulants

- Organic Coagulants

- Flocculants

- Corrosion and Scale Inhibitors

- Inorganic Inhibitors

- Organic Inhibitors

- Biocides and Disinfectants

- Oxidizing Biocides

- Non-Oxidizing Biocides

- pH Adjusters and Softeners

- Acids

- Bases

- Water Softeners

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- Sludge Conditioners

- Membrane Performance Enhancers/Antiscalants

- Cleaning and Descaling Chemicals

- Ion Exchange Resins

- Other Specialty Chemicals

By Application

- Boiler Water Treatment

- Cooling Water Treatment

- Process Water Treatment

- Wastewater Treatment

- Water Reuse and Recycling

- Desalination

By End-User Industry

- Power Generation

- Thermal Power Plants

- Nuclear Power Plants

- Hydroelectric Power Plants

- Renewable Energy

- Oil and Gas

- Upstream

- Midstream

- Downstream

- Chemical and Petrochemical

- Food and Beverage

- Pulp and Paper

- Mining and Metallurgy

- Textile

- Pharmaceutical

- Automotive

- Electronics and Semiconductors

- Other Manufacturing Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Industrial Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- BASF SE (Germany)

- Solenis LLC (U.S.)

- SUEZ SA (France)

- Kemira Oyj (Finland)

- Kurita Water Industries Ltd. (Japan)

- The Dow Chemical Company (U.S.)

- Veolia Water Technologies (France)

- SNF Floerger (France)

- Buckman (U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the industrial water treatment chemicals market with comprehensive analysis reviews, breakthrough technology insights, and strategic forecasts, highlighting the evolution of smart chemistry, ESG alignment, and digital innovation across end-user industries. Leveraging USDAnalytics’ proprietary data and expert perspectives, this report details the competitive dynamics, market drivers, and transformative trends—from regulatory pressures and energy transition to zero-liquid discharge and AI-driven dosing optimization. It highlights how corrosion and scale inhibitors, biocides, and membrane antiscalants are powering compliance and efficiency in sectors such as power generation, oil and gas, mining, and manufacturing. This report is an essential resource for decision-makers, technology providers, and investors seeking actionable intelligence, competitive benchmarking, and future-ready market opportunities across more than 25 countries.

Scope Highlights:

- Segmentation:

- By Type of Chemical: Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Softeners, Oxygen Scavengers, Defoamers and Antifoaming Agents, Sludge Conditioners, Membrane Performance Enhancers/Antiscalants, Cleaning and Descaling Chemicals, Ion Exchange Resins, Other Specialty Chemicals

- By Application: Boiler Water Treatment, Cooling Water Treatment, Process Water Treatment, Wastewater Treatment, Water Reuse and Recycling, Desalination

- By End-User Industry: Power Generation, Oil and Gas, Chemical and Petrochemical, Food and Beverage, Pulp and Paper, Mining and Metallurgy, Textile, Pharmaceutical, Automotive, Electronics and Semiconductors, Other Manufacturing Industries

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Key Players: Ecolab Inc. (U.S.), BASF SE (Germany), Solenis LLC (U.S.), SUEZ SA (France), Kemira Oyj (Finland), Kurita Water Industries Ltd. (Japan), The Dow Chemical Company (U.S.), Veolia Water Technologies (France), SNF Floerger (France), Buckman (U.S.).

Methodology

USDAnalytics applies a robust, multi-layered research methodology integrating direct industry interviews, plant-level data, and validation from regulatory and technical sources. Forecasts and market sizing are derived from proprietary analytics, bottom-up modeling, and comparative scenario mapping to ensure reliability. Each segment is evaluated for qualitative drivers and quantitative trends, providing industrial stakeholders with accurate, actionable insights and forward-looking intelligence for the global industrial water treatment chemicals market.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements