Water Desalination Chemicals Market: Growth Analysis and Value Forecast to 2034

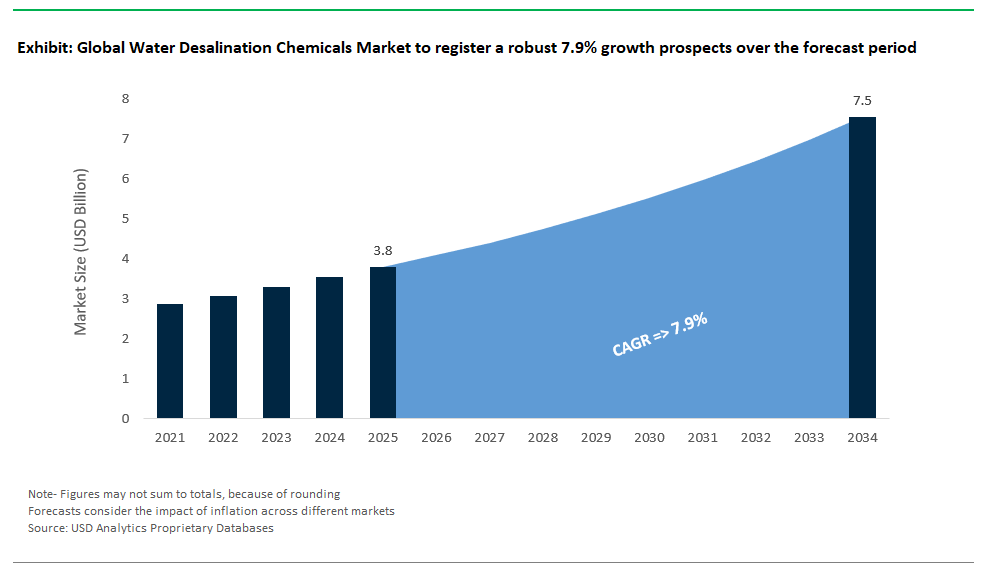

The water desalination chemicals market is valued at $3.8 billion in 2025 and projected to reach $7.5 billion by 2034, with a CAGR of 7.9%. The market is increasingly integral to the stable operation of large-scale seawater reverse osmosis (SWRO) plants, where water quality targets and operational resilience must be achieved under high salinity, variable source conditions, and growing regulatory scrutiny. At the core of pretreatment regimens are phosphonate–polyacrylate antiscalant blends, which are dosed at 2–6 ppm to manage calcium carbonate scaling even under aggressive saturation conditions such as LSI levels up to 2.8 and control barium sulfate formation at Saturation Index (SI) values of 1.5, per IDA operational benchmarks. These formulations are indispensable in multi-stage recovery configurations, where membrane feed pressures and scaling potential are both elevated.

Biofouling control is equally critical, particularly in warmer coastal regions with elevated biological loads. Chloramine-tolerant, non-oxidizing biocides like DBNPA are commonly applied in 0.2–1.0 ppm shock doses, achieving 4-log reductions in biofilm ATP levels while preserving membrane integrity in chlorinated upstream systems, per ASTM protocols. On the post-treatment side, desalinated water often requires boron polishing and remineralization to meet both health and corrosion control standards.

Secondary RO passes, operated at pH levels above 10 using NaOH dosing, are effective in reducing boron concentrations below the WHO guideline of 0.5 ppm (J. Membr. Sci.), while remineralization strategies typically involving calcite dissolution are tuned to achieve final LSI targets between 0.2 and 0.5, ensuring downstream distribution system stability (AWWA B455).

As global water-stressed regions scale up desalination capacity, there is growing emphasis on chemical solutions that extend membrane lifespan, minimize cleaning cycles, and support long-term plant efficiency under variable feedwater conditions. Suppliers that can offer formulation robustness, membrane material compatibility, and real-time dosing optimization are central to high-value desalination projects where chemical programs are operationally determinative.

Green Antiscalants and Digital Solutions Transform the Water Desalination Chemicals Market

Market Trend: Green Antiscalants & AI-Driven Dosing Revolutionize Desalination Efficiency

The global water desalination chemicals market is undergoing a paradigm shift, as pressure mounts for sustainable, energy-efficient, and digitally controlled solutions. Central to this evolution is the replacement of traditional phosphonate-based antiscalants with bio-derived, low-toxicity alternatives. Sokalan® Natura uses plant-based polymers to mitigate silica and calcium sulfate scaling at elevated temperatures (>60°C). Deployed at Saudi Arabia’s Jubail 3A SWRO plant, it reduced chemical consumption by 30%, extending membrane life while enhancing throughput. Simultaneously, the EU’s phosphonate ban is catalyzing a $150M market for biodegradable replacements across Mediterranean facilities. On the digital front, AI is emerging as a game-changer Veolia’s AI dynamically adjusts antiscalant and antifoam dosing, cutting OPEX and minimizing chemical overuse. These innovations are not merely operational upgrades they respond to rising regulatory and environmental scrutiny, with jurisdictions like California’s Ocean Plan 2024 limiting synthetic chemical discharge into marine environments. More critically, data from the International Desalination Association (IDA) confirms that just 1 mm of scale buildup increases energy consumption by 15%, making smart, green chemistry not just a sustainability measure but a bottom-line imperative. As the sector transitions to carbon-conscious and digitally optimized SWRO infrastructure, suppliers of bio-based, AI-compatible antiscalants and defoamers are positioned for significant global expansion.

Growth Opportunity: Brine Valorization & Circular Desalination Unlock New Revenue Streams

The next frontier in desalination lies in transforming waste brine into a resource, with growing emphasis on critical mineral recovery and ultra-pure water production. A flagship innovation is EnergyX’s LiTAS™ Desal, which uses selective antiscalants to concentrate lithium from RO reject brine achieving up to 90% lithium recovery in pilot projects across Chile’s coastal lithium corridor. With lithium demand soaring and desal brines rich in dissolved minerals, the chemical market for desal-lithium applications is projected to exceed $500 million by 2030 (Benchmark Minerals). Equally transformative is IDE Technologies’ BrineRefiner, which leverages crystallization modifiers to yield food-grade sodium chloride from hypersaline streams an innovation that monetizes waste at $50/tonne, while enabling zero-liquid discharge (ZLD). In parallel, the green hydrogen economy is opening new pathways: Siemens uses ultra-low TOC antiscalants to cut costs compared to traditional ion exchange. With Saudi Arabia’s NEOM project investing $1.5 billion into desalination-brine mining integration and facilities like ACCIONA’s Barcelona plant earning million USD in carbon credits the shift toward circular desalination is becoming commercially and environmentally compelling. As brine evolves from a liability into a high-value feedstock, chemical manufacturers that can tailor antiscalants, defoamers, and crystallization agents for selective mineral recovery, regulatory compliance, and downstream purity requirements stand to redefine the economics of desalination.

Competitive Landscape: Water Desalination Chemicals (Seawater & Brackish Water)

The global desalination chemicals market is highly specialized. It features a mix of companies that provide integrated solutions, focus on membrane protection, and innovate raw materials. These companies compete in various settings, which include large seawater reverse osmosis (SWRO) facilities and high-recovery brackish water systems, as well as thermal desalination plants. Ecolab (Nalco Water), Veolia (which includes legacy SUEZ), and Kurita lead the market. They offer integrated solutions that combine special chemistries with digital optimization tools. For example, Ecolab’s 3D TRASAR™ technology allows real-time management of scaling, fouling, and chemical dosing. This is vital for high-recovery SWRO systems, where maintaining operations and energy efficiency is crucial.

Solenis stands out as a dedicated water treatment innovator. It focuses on high-silica and seawater environments, offering well-known non-phosphorus antiscalants like PHOSFREE®. This product meets both regulatory requirements and technical needs in sensitive marine outfall areas. In contrast, Avista Technologies and King Lee Technologies occupy niche markets by concentrating on membrane preservation, especially in challenging feedwater situations. Their products gain validation from leading RO membrane manufacturers, which helps establish their credibility in critical operations where scaling and fouling are major concerns.

Kurita Water Industries excels in reducing fouling and scaling with high-performance polymers and organic dispersants. They also provide digital dosing control systems that suit utilities aiming to minimize chemical use. Italmatch Chemicals offers strong solutions in silica/silicate control through its GEODESAL™ range. They also supply additives tailored for specific requirements, such as improving boron rejection. This need is rising in multiple Gulf and Southeast Asian SWRO projects.

Veolia Water Technologies (formerly SUEZ) and BASF approach the market from different perspectives. Veolia combines its Hydrex™ chemical line with complete plant design and expertise in thermal desalination, especially with legacy MSF/MED setups. On the other hand, BASF specializes in upstream chemical building blocks. These include specialty polymers for antiscalants, hydrogen peroxide for controlling biofouling, and coagulants for pre-treatment. They support downstream formulators and OEMs.

Specialty suppliers like LANXESS are essential for advanced polishing applications, particularly with high-selectivity ion exchange resins (e.g., Lewatit®) that remove boron from RO permeate. Accepta Ltd. and regional firms serve small and mid-scale markets with affordable formulations that are technically supported. These are designed for varying feedwater quality and local regulatory demands.

Throughout the value chain, product differentiation depends on addressing severe scaling issues (like CaSO₄, CaCO₃, silica, and Mg), resisting high salinity and temperature, and complying with increasingly strict environmental standards regarding phosphorus and residual toxicity. There is also a growing focus on biocidal control, optimizing oxidizing (like NaOCl and ClO₂) and non-oxidizing (such as DBNPA and isothiazolinones) chemistries for membrane compatibility. As desalination projects grow in complexity and regulations become stricter worldwide, competition is intensifying not just on formulation effectiveness but also on digital capabilities, energy efficiency, and long-term membrane asset protection.

Water Desalination Chemicals Market – Segmentation Insights (2025–2034)

By Type of Chemical: Antiscalants Lead the Market While Membrane Cleaning Chemicals Grow Fastest

Antiscalants hold the largest share in the water desalination chemicals market, accounting for approximately 39.3% of total demand in 2025. Their dominance is driven by the critical need to prevent scale formation from calcium, magnesium, and silica in high-recovery reverse osmosis (RO) systems. As desalination plants increasingly operate at higher recovery rates and treat more mineral-laden feedwaters, the use of robust antiscalant formulations has become essential for membrane protection and long-term performance. These chemicals help reduce fouling, minimize downtime, and extend membrane life making them foundational to efficient RO plant operations. In contrast, membrane cleaning chemicals represent the fastest-growing segment, expanding at a 8.9% CAGR through 2034. The rise of biofouling and inorganic scaling, particularly in seawater reverse osmosis (SWRO) systems, is fueling demand for advanced cleaning agents capable of restoring membrane performance without compromising material integrity. Biocides and disinfectants are also experiencing strong growth, driven by the need for non-oxidizing, membrane-compatible agents such as DBNPA and isothiazolinones that address microbial contamination without degrading membrane surfaces. Coagulants, dechlorinators, and pH adjusters continue to support pre-treatment and protection phases, while specialty formulations cater to unique plant configurations and operational challenges.

.png)

By Desalination Technology: Membrane-Based RO Systems Dominate While Thermal Methods Maintain Niche

Membrane-based technologies primarily reverse osmosis (RO) and nanofiltration (NF) dominate the desalination chemicals market, contributing approximately 79.2% of total market share in 2025. These systems are favored for their energy efficiency, scalability, and lower capital costs compared to thermal desalination. RO plants, in particular, require a wide range of chemical treatments from antiscalants and biocides to membrane cleaners and pH adjusters resulting in significantly higher chemical consumption per cubic meter of treated water. The rapid global expansion of brackish and seawater RO projects, particularly in the Middle East, North Africa, and Asia-Pacific, continues to drive strong demand for chemical solutions that support high recovery rates, reduce fouling, and maintain consistent water quality. Meanwhile, thermal technologies multi-stage flash (MSF) and multi-effect distillation (MED) account for around 27.6% of the market and remain relevant in high-salinity or waste-heat-integrated applications. These systems typically use fewer chemicals, focusing on oxygen scavengers, defoamers, and scale inhibitors. The emergence of hybrid desalination systems combining RO and MED technologies is gradually increasing demand for multifunctional and compatible chemical treatments, offering a new avenue for market diversification and innovation.

Saudi Arabia Reinvents Desalination Chemistry with Vision 2030 and RO Leadership

Saudi Arabia remains the world’s undisputed leader in desalination capacity, setting the pace for global trends in desalination chemicals. The Saline Water Conversion Corporation (SWCC) is spearheading a transition from legacy, energy-intensive technologies like Multi-Stage Flash (MSF) and Multi-Effect Distillation (MED) toward cutting-edge Reverse Osmosis (RO) solutions. This shift is sharply increasing demand for advanced RO membrane chemicals antiscalants, biocides, and membrane cleaners needed to maximize efficiency, prolong membrane lifespan, and maintain plant reliability.

Strategic investments are ramping up, with Vision 2030 driving over $10 billion in new desalination infrastructure and a significant share dedicated to chemicals and process optimization. International suppliers are localizing manufacturing, as evidenced by Italmatch Chemicals’ new JV in Jubail, positioning themselves to serve the kingdom’s ambitious growth and sustainability goals. Additionally, R&D in eco-friendly inhibitors and green chemistry aligns with Saudi Arabia’s decarbonization agenda, making the market a proving ground for next-generation, low-impact desalination chemicals.

United States Drives Desalination Chemicals Market with Federal Funding and Innovation in Brine Management

The U.S. desalination chemicals market is experiencing dynamic growth, propelled by a robust regulatory environment, federal infrastructure funding, and a strong culture of technological innovation. New EPA regulations on PFAS are driving rapid adoption of RO technologies spurring demand for specialty antiscalants, membrane cleaners, and biocides tailored to tackle emerging contaminants. Billions in funding through the Infrastructure Investment and Jobs Act are accelerating deployment of advanced desalination plants across both municipal and industrial sectors.

Research is producing game-changing advances, such as Stanford’s electrochemical brine valorization method, which converts waste into marketable chemicals reducing both disposal costs and environmental impact. These innovations complement a broader industry trend toward chemical solutions that boost membrane performance and minimize operational expenses. The U.S. market remains a testbed for next-gen desalination chemicals, especially those targeting sustainable and economically viable water reuse.

China Scales Desalination Chemicals Market with Automated Plants and Government-Led Expansion

China is rapidly emerging as a global powerhouse in desalination chemicals, fueled by government mandates to combat severe water scarcity, particularly in key coastal provinces. Major projects like the 2025 commissioning of the SUEZ-Wanhua industrial seawater RO plant demonstrate the country’s capacity for large-scale, energy-efficient desalination. These developments are driving surging demand for sophisticated chemical solutions, especially those needed to manage high turbidity and complex feedwater.

Automation is a core focus, with fully automated plants requiring precise chemical dosing and monitoring systems. Advanced coagulants, flocculants, and antiscalants are critical to protecting downstream RO membranes and maintaining high recovery rates. China’s continued investment in desalination infrastructure, combined with rising environmental and quality standards, ensures robust growth for suppliers of innovative, high-performance desalination chemicals.

Israel Leads in Advanced Membrane Chemicals and Biofouling Solutions for Sustainable Desalination

Israel’s desalination sector is a model of efficiency and innovation, making the nation a prime consumer and developer of high-performance desalination chemicals. The country relies on mega-plants like Sorek and Ashkelon, which demand state-of-the-art pretreatment and membrane cleaning agents for consistent, large-scale production of potable water even in arid environments.

Israeli R&D is pioneering new approaches to membrane maintenance, such as bio-based pretreatment chemicals and biological control strategies to combat biofouling one of the biggest challenges in RO systems. The use of desalinated water for agriculture underscores the importance of sustainable chemical solutions that ensure water safety for multiple end uses. Israel’s relentless drive for process efficiency and environmental stewardship cements its status as a global reference for desalination chemical innovation.

Australia Grows Desalination Chemicals Market with Drought-Driven Demand and Environmental Stewardship

Australia’s water desalination chemicals market is expanding rapidly as the country faces recurring droughts and increasingly turns to desalination as a core water supply strategy. Major plants in Sydney and Perth are setting new benchmarks for energy efficiency, employing pressure exchangers, double-pass membranes, and advanced chemical dosing to maximize output and minimize fouling.

High-recovery membrane processes are central to the Australian market, requiring robust antiscalants and specialty cleaning chemicals. There is also a strong emphasis on environmental impact, with new plant designs and chemical formulations focused on minimizing disruption to local ecosystems. Australia’s experience in integrating desalination into urban water grids is fueling a steady rise in demand for both traditional and next-generation chemical solutions.

Spain Ramps Up Desalination Chemicals Demand amid Drought and EU Recovery Investments

Spain’s desalination chemicals market is booming as the country grapples with historic drought and rolls out a major government investment program for water resilience. Over €200 million in new funding is spurring the construction of new seawater desalination capacity especially along the Catalan coast and the retrofitting of older plants to boost efficiency. This translates to substantial demand for pretreatment, antiscalant, and cleaning chemicals to maintain system performance.

Energy efficiency is a key concern, with technology providers such as Energy Recovery supplying advanced pressure exchangers for RO projects. The market is also moving toward smarter, greener chemical solutions as plants are upgraded to meet both energy and water quality targets. Spain’s proactive approach to water security and infrastructure modernization is solidifying its place as a major market for desalination chemicals in Europe.

United Arab Emirates Accelerates Greener Desalination Chemistry with National Water Security Strategy

The UAE is aggressively scaling up desalination capacity, making it one of the world’s top consumers of desalination chemicals. The Water Security Strategy 2036 is driving investments in both new plants and technology upgrades, with an explicit focus on reducing carbon emissions. This has fueled a wave of projects in Abu Dhabi, Dubai, and Umm Al Qaiwain, each creating substantial demand for chemicals particularly in advanced RO plants.

UAE companies and global partners are collaborating to develop innovative, environmentally friendly chemical solutions that enable efficient, low-impact desalination. Growing use of desalinated water for agriculture and other sensitive applications means the market increasingly favors green chemistry that ensures both water quality and environmental compliance. The UAE’s blend of investment, innovation, and sustainability goals is setting regional standards for the future of desalination chemistry.

India Surges Ahead in Desalination Chemicals with Government-Led Infrastructure Expansion

India’s market for desalination chemicals is on a rapid upward trajectory, spurred by acute water scarcity, robust industrial demand, and national initiatives like the Jal Jeevan Mission. Major urban projects, such as the Minjur Seawater Desalination Plant, highlight the strategic reliance on desalination for urban and industrial water needs. The market is also witnessing strong growth in cost-effective, energy-efficient chemical formulations aimed at reducing operational costs and enhancing membrane durability.

India’s growing industrial base spanning chemicals, petroleum, and pharmaceuticals relies heavily on high-quality process water, further boosting demand for specialty chemicals that address fouling, scaling, and microbial contamination in desalination systems. As both public and private sectors invest in new capacity and upgrades, India is quickly emerging as a key global growth engine for desalination chemicals.

Water Desalination Chemicals Market Report Scope

Water Desalination Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.8 Billion

|

|

Market Size (2034)

|

$7.5 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Type of Chemical (Antiscalants, Coagulants and Flocculants, Biocides and Disinfectants, pH Adjusters/Neutralizers, Dechlorinators/Oxygen Scavengers, Membrane Cleaning Chemicals, Other Specialty Chemicals), By Desalination Technology (Membrane-based Desalination, Thermal Desalination), By Water Source (Seawater Desalination, Brackish Water Desalination, Wastewater Desalination/Reuse), By End-Use Application (Municipal Water Treatment, Industrial Water Treatment

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Avista Technologies, Inc. (U.S.), Kurita Water Industries Ltd. (Japan), BASF SE (Germany), SUEZ SA (France), Veolia Water Technologies (France), Italmatch Chemicals S.p.A. (Italy), King Lee Technologies (U.S.), LANXESS AG (Germany), Accepta Ltd. (UK),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Water Desalination Chemicals Market Segmentation

By Type of Chemical

- Antiscalants

- Coagulants and Flocculants

- Biocides and Disinfectants

- pH Adjusters/Neutralizers

- Dechlorinators/Oxygen Scavengers

- Membrane Cleaning Chemicals

- Other Specialty Chemicals

By Desalination Technology

- Membrane-based Desalination

- Reverse Osmosis (RO)

- Nanofiltration (NF)

- Ultrafiltration (UF)

- Electrodialysis (ED)

- Membrane Distillation (MD)

- Thermal Desalination

- Multi-Stage Flash (MSF) Distillation

- Multi-Effect Distillation (MED)

- Vapor Compression Distillation (VC)

- Hybrid Systems

By Water Source

- Seawater Desalination

- Brackish Water Desalination

- Wastewater Desalination/Reuse

By End-Use Application

- Municipal Water Treatment

- Industrial Water Treatment

- Power Generation

- Oil and Gas

- Chemical and Petrochemical

- Food and Beverage

- Pharmaceutical

- Electronics and Semiconductors

- Mining and Metallurgy

- Other Manufacturing Industries

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Water Desalination Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Avista Technologies, Inc. (U.S.)

- Kurita Water Industries Ltd. (Japan)

- BASF SE (Germany)

- SUEZ SA (France)

- Veolia Water Technologies (France)

- Italmatch Chemicals S.p.A. (Italy)

- King Lee Technologies (U.S.)

- LANXESS AG (Germany)

- Accepta Ltd. (UK)

* List Not Exhaustive

Research Coverage

This report investigates the global Water Desalination Chemicals Market, providing thorough analysis reviews of key growth drivers, digital dosing breakthroughs, and the transformative role of green antiscalants in seawater and brackish water desalination. USDAnalytics highlights emerging opportunities in brine valorization, circular desalination, and the rapid adoption of AI-enabled chemical optimization for membrane longevity and operational efficiency. This report is an essential resource for utilities, EPC contractors, plant operators, chemical suppliers, and investors seeking to navigate the evolving regulatory landscape, sustainability imperatives, and value chain innovation defining the desalination chemicals industry worldwide.

Scope Highlights:

- Segmentation:

- By Type of Chemical: Antiscalants, Coagulants and Flocculants, Biocides and Disinfectants, pH Adjusters/Neutralizers, Dechlorinators/Oxygen Scavengers, Membrane Cleaning Chemicals, Other Specialty Chemicals

- By Desalination Technology: Membrane-based Desalination (Reverse Osmosis, Nanofiltration, Ultrafiltration, Electrodialysis, Membrane Distillation), Thermal Desalination (Multi-Stage Flash, Multi-Effect, Vapor Compression, Hybrid Systems)

- By Water Source: Seawater Desalination, Brackish Water Desalination, Wastewater Desalination/Reuse

- By End-Use Application: Municipal Water Treatment, Industrial Water Treatment (Power Generation, Oil and Gas, Chemical and Petrochemical, Food and Beverage, Pharmaceutical, Electronics and Semiconductors, Mining and Metallurgy, Other Manufacturing Industries)

- Geographic Scope: Covers 25+ countries across North America, Europe, Asia Pacific, South America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecasts from 2025 to 2034.

- Companies Profiled: Ecolab Inc. (U.S.), Solenis LLC (U.S.), Avista Technologies, Inc. (U.S.), Kurita Water Industries Ltd. (Japan), BASF SE (Germany), SUEZ SA (France), Veolia Water Technologies (France), Italmatch Chemicals S.p.A. (Italy), King Lee Technologies (U.S.), LANXESS AG (Germany), Accepta Ltd. (UK).

Methodology

This report applies a comprehensive, multi-layered methodology, combining primary interviews with leading industry experts and extensive secondary research from trusted databases and regulatory resources. USDAnalytics employs advanced market modeling and competitive benchmarking to project market size, segmentation, and trends. Analytical rigor is applied to validate supply-demand balances, technology adoption rates, and regional growth patterns. Forecasts and insights are cross-referenced with plant-level data and proprietary market intelligence, ensuring actionable recommendations and credible analysis for all stakeholders in the water desalination chemicals sector.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements

Table of Contents: Water Desalination Chemicals Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Findings

1.3. Global Market Snapshot

2. Water Desalination Chemicals Market Landscape & Outlook (2025–2034)

2.1. Introduction to Water Desalination Chemicals Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $3.8 Billion

2.2.2. Forecasted Market Size and CAGR (2034): $7.5 Billion at 7.9% CAGR

2.3. Key Operational Drivers and Chemical Requirements

2.3.1. Pretreatment: Antiscalant Blends for High-Salinity Conditions

2.3.2. Biofouling Control: Chloramine-Tolerant Biocides

2.3.3. Post-Treatment: Boron Polishing and Remineralization Strategies

2.4. Market Evolution: Focus on Membrane Lifespan and Efficiency

2.5. Strategic Importance in High-Value Desalination Projects

3. Breakthrough Innovations in the Water Desalination Chemicals Market

3.1. Trend: Green Antiscalants & AI-Driven Dosing Revolutionize Desalination Efficiency

3.1.1. Shift to Bio-Derived, Low-Toxicity Alternatives (e.g., Sokalan® Natura)

3.1.2. AI-Driven Dosing Optimization for OPEX Reduction

3.1.3. Catalyzed by Regulatory and Environmental Scrutiny

3.2. Opportunity: Brine Valorization & Circular Desalination Unlock New Revenue Streams

3.2.1. Critical Mineral Recovery from RO Reject Brine (e.g., EnergyX’s LiTAS™ Desal)

3.2.2. Production of Food-Grade Sodium Chloride (e.g., IDE’s BrineRefiner)

3.2.3. Chemical Solutions for the Green Hydrogen Economy

4. Competitive Landscape: Water Desalination Chemicals Market

4.1. Overview of Market Dynamics and Drivers

4.2. Market Leaders: Integrated Solutions & Digital Optimization

4.2.1. Ecolab (Nalco Water): 3D TRASAR™ Technology for Real-Time Management

4.2.2. Veolia (SUEZ): Hydrex™ Chemical Line and Plant Design Expertise

4.2.3. Kurita Water Industries: High-Performance Polymers and Digital Dosing

4.3. Dedicated Water Treatment Innovators

4.3.1. Solenis LLC: Non-Phosphorus Antiscalants (PHOSFREE®)

4.3.2. Avista Technologies, Inc. and King Lee Technologies: Membrane Preservation

4.4. Specialty Chemical Suppliers

4.4.1. Italmatch Chemicals S.p.A.: Silica/Silicate Control and Boron Rejection

4.4.2. BASF SE: Upstream Chemical Building Blocks and Specialty Polymers

4.4.3. LANXESS AG: Ion Exchange Resins for Advanced Polishing

4.4.4. Accepta Ltd.: Affordable Formulations for Mid-scale Markets

4.5. Key Competitive Factors: Formulation, Digital Capabilities, and Environmental Compliance

5. Market Share and Segmentation Insights: Water Desalination Chemicals Market

5.1. By Type of Chemical

5.1.1. Antiscalants: Largest Market Share (39.3% in 2025)

5.1.2. Membrane Cleaning Chemicals: Fastest-Growing Segment (8.9% CAGR)

5.1.3. Biocides and Disinfectants

5.1.4. Coagulants and Flocculants

5.1.5. pH Adjusters/Neutralizers

5.1.6. Dechlorinators/Oxygen Scavengers

5.1.7. Other Specialty Chemicals

5.2. By Desalination Technology

5.2.1. Membrane-based Desalination: Dominant Share (79.2% in 2025)

5.2.2. Thermal Desalination: Niche Market (27.6% in 2025)

5.3. By Water Source

5.3.1. Seawater Desalination

5.3.2. Brackish Water Desalination

5.3.3. Wastewater Desalination/Reuse

5.4. By End-Use Application

5.4.1. Municipal Water Treatment

5.4.2. Industrial Water Treatment

6. Country Analysis and Outlook of Water Desalination Chemicals Market

6.1. Saudi Arabia: Vision 2030 and RO Leadership

6.2. United States: Federal Funding and Brine Management Innovation

6.3. China: Automated Plants and Government-Led Expansion

6.4. Israel: Advanced Membrane Chemicals and Biofouling Solutions

6.5. Australia: Drought-Driven Demand and Environmental Stewardship

6.6. Spain: Drought and EU Recovery Investments

6.7. United Arab Emirates: National Water Security Strategy and Greener Chemistry

6.8. India: Government-Led Infrastructure Expansion

6.9. Other Countries Analyzed

- 6.9.1. North America (Canada, Mexico)

- 6.9.2. Europe (France, Spain, Italy, Russia, Rest of Europe)

- 6.9.3. Asia Pacific (South Korea, South East Asia, Rest of Asia)

- 6.9.4. South America (Argentina, Rest of South America)

- 6.9.5. Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

7. Water Desalination Chemicals Market Size Outlook by Region (2025-2034)

7.1. North America Water Desalination Chemicals Market Size Outlook to 2034

7.1.1. By Type of Chemical

7.1.2. By Desalination Technology

7.1.3. By Water Source

7.1.4. By End-User Industry

7.2. Europe Water Desalination Chemicals Market Size Outlook to 2034

7.2.1. By Type of Chemical

7.2.2. By Desalination Technology

7.2.3. By Water Source

7.2.4. By End-User Industry

7.3. Asia Pacific Water Desalination Chemicals Market Size Outlook to 2034

7.3.1. By Type of Chemical

7.3.2. By Desalination Technology

7.3.3. By Water Source

7.3.4. By End-User Industry

7.4. South America Water Desalination Chemicals Market Size Outlook to 2034

7.4.1. By Type of Chemical

7.4.2. By Desalination Technology

7.4.3. By Water Source

7.4.4. By End-User Industry

7.5. Middle East and Africa Water Desalination Chemicals Market Size Outlook to 2034

7.5.1. By Type of Chemical

7.5.2. By Desalination Technology

7.5.3. By Water Source

7.5.4. By End-User Industry

8. Company Profiles: Leading Players in Water Desalination Chemicals Market

8.1. Ecolab Inc. (U.S.)

8.2. Solenis LLC (U.S.)

8.3. Avista Technologies, Inc. (U.S.)

8.4. Kurita Water Industries Ltd. (Japan)

8.5. BASF SE (Germany)

8.6. SUEZ SA (France)

8.7. Veolia Water Technologies (France)

8.8. Italmatch Chemicals S.p.A. (Italy)

8.9. King Lee Technologies (U.S.)

8.10. LANXESS AG (Germany)

8.11. Accepta Ltd. (UK)

8.12. (List Not Exhaustive)

9. Methodology

9.1. Research Scope

9.2. Market Research Approach

9.3. Market Sizing and Forecasting Model

9.4. Research Coverage

9.5. Data Horizon

9.6. Deliverables

10. Appendix

10.1. Acronyms and Abbreviations

10.2. List of Tables

10.3. List of Figures