Market Outlook for Swimming Pool Disinfectants and Biocides: Growth Analysis and Forecast

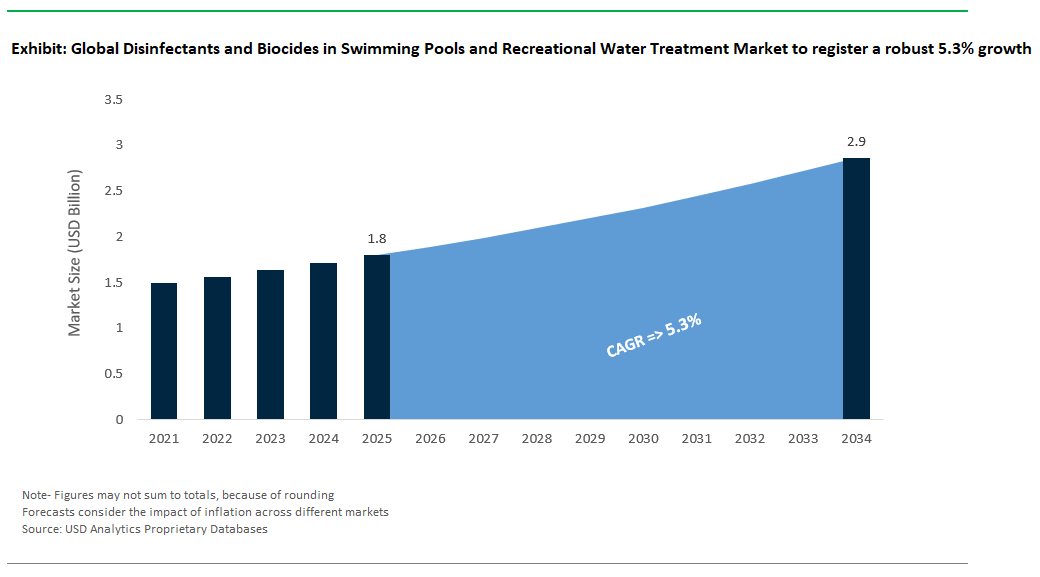

Disinfectants and Biocides in Swimming Pools and Recreational Water Treatment Market is valued at $1.8 billion in 2025 and projected to reach $2.9 billion by 2034, with a CAGR of 5.3%. The market has evolved significantly beyond legacy chlorine-centric treatment protocols, shaped by escalating concerns over disinfection byproducts (DBPs), indoor air quality, and user comfort. While chlorine remains dominant for its broad-spectrum efficacy and cost-effectiveness, its limitations in forming chloramines and trihalomethanes (THMs) have driven a shift toward alternative and supplemental disinfection strategies.

Bromine tablets, for instance, have emerged as a preferred option in spas and indoor facilities due to their stable efficacy at 2–4 ppm residual levels and their significantly lower chloramine formation, up to 50% less compared to chlorine. In high-use and enclosed aquatic environments, advanced oxidation processes (AOPs) such as UV/chlorine integration are increasingly adopted. A UV dose of 60 mJ/cm² is marketed to degrade over 99% of volatile chloramines, reducing combined chlorine levels by more than 80%, thereby improving air quality and minimizing ocular and respiratory irritation (NSF/ANSI 50 standards).

Maintaining disinfection efficacy while ensuring user safety also hinges on precise oxidation-reduction potential (ORP) control. Meanwhile, growing pressure to limit DBP exposure especially THMs like chloroform has led to the adoption of activated carbon filtration systems, which reduce THM concentrations by 70–90% and help facilities meet the WHO’s threshold for drinking water equivalency.

As end users prioritize both health outcomes and recreational experience, the market is expanding beyond single-disinfectant paradigms toward integrated systems that balance efficacy, safety, and environmental compliance. Suppliers that offer not only disinfectant formulations but also sensor-integrated dosing systems and full-cycle water quality analytics are increasingly favored by commercial pool chains, waterparks, and municipal aquatic programs seeking long-term disinfection stability under dynamic bather loads.

Evolving Disinfection Methods and Digital Innovation in the Recreational Water Treatment Chemicals Market

Market Trend: Shift Toward Non-Chlorine and Sustainable Disinfection

The swimming pools and recreational water treatment market is witnessing a paradigm shift away from traditional chlorine-based disinfection toward sustainable, non-toxic, and user-friendly alternatives. Rising public awareness of health concerns associated with chloramines notably respiratory irritants linked to asthma and eye irritation has pushed both regulators and industry leaders toward innovation. Regulatory mandates like California’s AB 620, targeting chloramine reductions in public aquatic centers, further drive UV and ozone adoption. At the same time, Ecolab’s AquaBalance™ BIO, combining plant-derived quaternary compounds and enzymatic boosters, has received FDA approval for indoor therapy pools, offering a bromine-free alternative that eliminates lingering odors and irritants. In Europe, the 2024 restriction on trichloroisocyanuric acid (TCCA) has catalyzed interest in saltwater chlorination and electrolyzed oxidizing systems. Sustainability credentials also play a growing role UV disinfection systems cut chemical transport emissions by 50%, earning ISO 14067 carbon footprint certifications. With cost parity achieved saltwater chlorination at $0.05/m³ OPEX vs. $0.08 for chlorine eco-friendly systems are not just cleaner but also economically viable. As leisure venues, cruise lines, and residential customers seek healthier experiences, non-chlorine disinfection is rapidly becoming the new industry standard.

Growth Opportunity: Smart & Autonomous Water Quality Management

The next wave of growth in the recreational water treatment chemicals market lies in digital disinfection management and autonomous dosing systems. Leading the charge is Hayward’s OmniLogic SmartSense, which integrates ORP and pH sensors with AI-driven machine learning to automatically adjust biocide dosing in real time. This technology has been rolled out to over 1,200 water parks across the U.S., saving up to 20% in chemical consumption while ensuring consistent pathogen control. Moreover, business models are evolving companies like PoolRx have successfully commercialized SaaS platforms that offer predictive dosing insights and remote system management. High-traffic recreational venues such as Olympic pools and cruise ships are turning to next-gen chlorine-free solutions. In the residential space, Pentair uses magnesium and copper ions and is gaining traction among high-income homeowners, delivering 60% chemical reduction with premium system pricing. First movers benefit from several competitive edges: hospitality chains pay a 15% premium for chloramine-free systems, and companies like Fluence Analytics monetize water quality data for municipalities and regulatory compliance. As digitalization, health consciousness, and sustainability converge, the opportunity to bundle smart chemical management with safer biocides represents the most lucrative pathway forward in this evolving market.

Competitive Landscape: Disinfectants and Biocides in Swimming Pools and Recreational Water Treatment Market

The global market for disinfectants and biocides used in swimming pools and recreational water treatment is competitive and complex. Key players hold strong positions in the chemical supply chains and distribution channels. These companies stand out through their integration strategies, manufacturing locations, unique formulations, and increased use of smart delivery and automation systems.

Lonza Group is the world’s largest producer of chlorinated isocyanurates, essential for swimming pool disinfection. The company has also expanded its offerings with polyhexamethylene biguanide (PHMB) systems for chlorinated-free users. Lonza’s integration allows it to control both raw material production and branded formulations, which is vital for global retail and private-label supply.

In North America, Olin Corporation is a major player in sodium hypochlorite and bulk liquid chlorine production. Its chlor-alkali operations provide significant distribution to municipal and institutional pool operators. Axiall Corporation, now part of Westlake Chemical, enhances this network as a top producer of calcium hypochlorite, also providing popular pool care brands like HTH™ and Poolife™. Together, these companies serve both professional services and retail markets, utilizing extensive logistical capabilities across the U.S. and Canada.

Consumer retail is a key area, especially in the U.S. Clorox Pool&Spa™ occupies significant space in major stores such as Walmart, Lowe’s, and The Home Depot. Its leading position comes from a diverse product lineup, including cal-hypo, dichlor, and trichlor formats. User-friendly innovations like shock pods, floating dispensers, and mobile-app dosing assistance further enhance its appeal. The brand's visibility and convenience give it an advantage in the DIY residential market.

In Asia-Pacific, Nippon Soda Co. Ltd. maintains its position as Japan’s top pool disinfectant producer, focusing on high-purity calcium hypochlorite and dichlor. Its domestic leadership relies on stable manufacturing and reliable distribution, essential for institutional pools and spas in urban areas with strict water safety rules.

The bromine market, while smaller in volume, is focused and carries a premium price. ICL Group and Albemarle Corporation are the main global suppliers of brominated pool biocides, such as BCDMH and bromochlorodimethylhydantoin. ICL uses its control over bromine extraction from the Dead Sea to provide both base chemistry and unique formulations designed for high-use environments, including spas and hot tubs. Albemarle maintains a strong global network with regional storage and blending capabilities.

An emerging competitive trend focuses on saltwater pool systems and integrated disinfection automation. Zodiac Pool Systems, part of Fluidra S.A., leads this shift with its Jandy® TruClear™ and AquaPure® salt chlorine generators. These systems cater to the growing demand for less manual work and better control over chlorine dosing. Fluidra’s acquisition strategy and global reach reinforce its leadership in pool equipment and water treatment.

In the institutional and commercial sector, companies like Solenis and Ecolab (Nalco Water) provide unique value by combining chemical programs with real-time water analysis and compliance systems. Solenis assists theme parks and busy aquatic centers with tailored water quality programs, including algaecides and biofilm control. Ecolab emphasizes closed-loop automation, giving clients real-time pathogen management and resource efficiency, which is crucial for hotel pools and wellness centers facing strict regulations.

Disinfectants and Biocides in Swimming Pools and Recreational Water Treatment Market – Segmentation Insights (2025–2034)

By Product Type: Chlorine-Based Disinfectants Dominate While Non-Halogen Oxidizers Grow Fastest

Chlorine-based disinfectants hold the largest market share, accounting for approximately 54.3% of the swimming pool and recreational water treatment chemicals market in 2025. Chlorine remains the go-to solution due to its broad-spectrum antimicrobial efficacy, rapid pathogen inactivation, and cost-effectiveness. Popular chlorine-based products include sodium hypochlorite (liquid form) and trichloroisocyanuric acid (TCCA) tablets, widely used in residential and public pools for routine disinfection. Despite growing concerns over chloramine formation and potential skin/eye irritation, the reliability and affordability of chlorine keep it dominant across global markets. In contrast, non-halogen oxidizing biocides are the fastest-growing segment, projected to expand at a 7.1% CAGR through 2034. This growth is led by increasing adoption of potassium monopersulfate (MPS) and advanced oxidation technologies like ozone and UV systems, particularly in commercial and high-traffic aquatic facilities aiming to reduce combined chlorine levels and improve water quality. Bromine-based disinfectants remain a preferred option in spas and hot tubs, where their stability at elevated temperatures and lower odor profiles make them highly effective. Non-oxidizing algaecides and specialty chemicals such as clarifiers and enzyme-based treatments continue to support pool hygiene and user experience, especially in automated and maintenance-light systems.

.png)

By End-User: Residential Pools Lead While Spas & Hot Tubs Grow Fastest

Residential pools represent the largest end-user segment, comprising approximately 42.9% of market share in 2025. This dominance is largely attributed to the widespread use of chlorine tablets and liquid disinfectants in backyard pools and home-based recreational setups. The DIY nature of residential pool maintenance, coupled with the affordability and availability of chlorine products, fuels consistent chemical consumption in this segment. Meanwhile, spas and hot tubs are witnessing the fastest growth, projected at a 6.7% CAGR through 2034. The rise of wellness tourism, premium hospitality offerings, and in-home spa installations is driving the demand for more specialized disinfectants such as bromine and silver ion hybrid systems, which offer superior performance at high temperatures with reduced skin irritation. Commercial and public pools covering hotels, water parks, and municipal facilities remain key drivers of innovation, adopting automated dosing systems, UV-C disinfection, and low-chlorine strategies to improve safety, reduce chemical usage, and comply with evolving public health regulations. As consumers become more conscious of water quality and recreational hygiene, all segments are expected to integrate advanced biocide formulations and real-time water monitoring technologies over the forecast period.

United States: Smart Technologies and Alternative Sanitizers Revolutionize Pool Disinfectant Market

The United States leads the market for swimming pool disinfectants and biocides, driven by consumer demand for safer, more comfortable pool experiences and an evolving regulatory landscape. Advanced oxidation processes (AOPs) are becoming mainstream, with the integration of UV and ozone systems to create hydroxyl radicals providing superior destruction of chlorine-resistant pathogens like Cryptosporidium. This shift enables a reduction in chlorine usage, improving user comfort by minimizing traditional pool odors and chemical irritation. Another defining trend is the rise of AI-powered smart pool automation platforms. These systems offer real-time water chemistry monitoring and automatic chemical dosing, resulting in improved water quality, chemical savings, and extended equipment life.

The U.S. market also favors mineral-based sanitization, particularly systems using copper or silver ions, which can reduce chlorine demand by up to 50%. This aligns with a growing preference for low-maintenance, user-friendly alternatives in both residential and public pools. Regulatory clarity is evolving as well; a 2025 Supreme Court ruling on the Clean Water Act is influencing stricter discharge requirements, driving public pool operators toward precision water treatment solutions. The combination of smart automation, alternative sanitizers, and proactive regulation solidifies the U.S. as an innovation leader in recreational water treatment.

Germany: Multi-Barrier Approaches and Chlorine Reduction Set the Standard in Pool Water Hygiene

Germany is recognized for its stringent pool and spa water hygiene standards, underpinned by the DIN 19643 standard, which regulates free and combined chlorine, pH, and by-product formation. This has encouraged a widespread adoption of advanced disinfection systems including UV and ozone that effectively reduce harmful chloramines and trihalomethanes (THMs) in public and private pools. Multi-barrier strategies are now the norm, combining primary chlorine disinfection with flocculation, high-performance filtration, and powdered activated carbon to ensure consistent water quality and minimal chemical exposure.

Germany is also at the forefront of the "biological pool" or "natural pool" movement, reflecting a consumer shift toward chemical-free recreational water. While not permitted for public venues, these pools highlight a growing preference for environmentally friendly alternatives. A further innovation is the development of mobile water treatment plants, which provide flexible, rapid deployment for temporary or remote recreational sites. Overall, Germany’s strong regulatory framework and technological leadership drive continuous improvement in pool safety and sustainability.

China: Automated Monitoring and Advanced Oxidation Drive Rapid Growth in Recreational Water Safety

China’s market for pool disinfectants and biocides is expanding rapidly, underpinned by a booming recreational sector and robust government health initiatives. The “Action Plan for Prevention and Control of Water Pollution” has triggered widespread investment in pool and waterpark infrastructure, leading to greater uptake of advanced disinfection technologies. Automated water quality monitoring and dosing systems are increasingly deployed to maintain compliance with national standards, offering precise control over pH, turbidity, and microbial safety.

Demand is surging for alternatives to traditional chlorine, with UV and ozone systems favored for their ability to eliminate "pool smell" and mitigate health risks associated with chloramines. Leading suppliers are offering integrated water treatment solutions blending filtration, chemical dosing, and advanced oxidation to ensure optimal water clarity and pathogen control. As pool construction accelerates across urban centers, China’s market is positioned for long-term growth in high-performance, user-friendly recreational water treatment.

Brazil: Regulatory Framework and Private Investment Advance Pool Disinfection Practices

Brazil’s disinfectants and biocides market is being transformed by the country’s new national sanitation framework, which promotes universal access to safe water. This policy shift has led to an influx of private investment, raising standards in public and private pool management. Anvisa, Brazil’s sanitary surveillance authority, has set clear guidelines for pool water, mandating at least 1.0 ppm free residual chlorine and other hygiene benchmarks creating stable demand for chlorine-based disinfectants.

Advanced systems are gaining traction, with saltwater chlorinators and UV-based disinfection becoming popular in luxury and commercial pools for their user comfort and reduced manual handling. Companies are also focused on operator education and compliance support, helping ensure that new regulations translate into practical water quality improvements. This dual focus on robust regulatory standards and cutting-edge technology is accelerating the evolution of Brazil’s recreational water treatment market.

United Kingdom: Multi-Barrier Guidance and Sustainability Initiatives Shape Pool Water Quality

The United Kingdom stands out for its science-driven approach to pool disinfection, guided by the Pool Water Treatment Advisory Group (PWTAG) and referenced by regulatory bodies. Updated guidance in 2025 emphasizes a multi-barrier method combining filtration, chemical disinfection, and secondary processes like UV and ozone to ensure consistently high water safety. This framework has spurred demand for integrated chemical and non-chemical treatment systems capable of managing modern challenges, from resistant pathogens to chemical by-products.

Sustainability is also a core trend, with new chemical formulations designed to extend water life and reduce the need for draining and refilling. The UK government’s commitment to public health and environmental protection ensures ongoing innovation and investment in this sector. Companies are responding with next-generation products that balance hygiene, user comfort, and resource conservation, making the UK a benchmark for progressive recreational water treatment.

Australia: Drought Resilience and Smart Control Systems Transform Pool Disinfection Market

Australia’s pool chemical market is shaped by its climate challenges and high pool ownership rates. Drought resilience and water conservation are top priorities, leading to the widespread adoption of efficient sanitizers and automation technologies. Calcium hypochlorite has gained prominence for its reduced need for draining, while advanced controllers and sensors are now commonplace delivering precise chemical dosing and minimizing waste. These solutions enable pool operators to optimize costs, improve water quality, and align with national sustainability goals.

Secondary disinfection, notably UV and ozone systems, is increasingly being installed to reduce chlorine reliance and elevate user comfort. This shift is further encouraged by award-winning industry partnerships that spotlight sustainable water management practices. Australia’s focus on smart, water-efficient solutions is setting new standards for pool disinfection in water-stressed regions.

Japan: Automated Filtration and Water Recycling Lead the Way in Hygienic Pool Treatment

Japan’s market for pool disinfectants and biocides is marked by technological maturity and a culture of high hygiene. Rigorous public health regulations drive the adoption of advanced filtration and disinfection systems, particularly in high-traffic facilities. Automation is a major trend, with smart systems that monitor and regulate water chemistry autonomously, reducing labor needs and ensuring consistent quality.

Japan’s emphasis on water conservation is visible in the development of recycling and reuse systems for recreational water. These solutions reduce the environmental footprint of pools and spas, a key consideration in a country with limited water resources. The integration of advanced oxidation processes and highly efficient filtration technologies makes Japan a leader in hygienic, resource-efficient recreational water treatment.

India: Urbanization and Regulatory Standards Accelerate Growth in Disinfectants and Biocides

India’s recreational water treatment market is surging, driven by rapid urbanization, a rising middle class, and new regulatory guidelines. The expansion of public and private pools creates strong demand for a spectrum of disinfectants and biocides, with Indian Standard IS 3328:1965 ensuring safety through requirements on turnover rates, chlorine levels, and pH.

While chlorine remains the primary disinfectant, adoption of alternative methods including UV, ozone, and bio-based products is on the rise, reflecting growing consumer interest in sustainability and user comfort. The trend toward natural, chemical-free pools underscores a broader preference for environmentally conscious solutions. As the market matures, India is set to become a major growth driver for innovative, multi-modal recreational water treatment chemicals.

Disinfectants and Biocides in Swimming Pools and Recreational Water Treatment Market Report Scope

Disinfectants and Biocides in Swimming Pools and Recreational Water Treatment Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.8 Billion

|

|

Market Size (2034)

|

$2.9 Billion

|

|

Market Growth Rate

|

5.3%

|

|

Segments

|

By Product Type (Chlorine-based Disinfectants, Bromine-based Disinfectants, Non-Halogen Oxidizing Biocides, Non-Oxidizing Biocides/Algaecides, Specialty/Ancillary Chemicals), By Application (Continuous Disinfection, Shock Treatment/Superchlorination, Algae Control and Prevention, Biofilm Control, Winterization Chemicals), By End-User (Residential Pools, Commercial and Public Pools, Spas and Hot Tubs

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Lonza Group (Switzerland), Axiall Corporation (Westlake Chemical Corporation) (U.S.), Olin Corporation (U.S.), ICL Group (Israel), Albemarle Corporation (U.S.), Nippon Soda Co. Ltd. (Japan), Clorox PoolandSpa (U.S.), Zodiac Pool Systems (Fluidra S.A.) (Spain), Solenis LLC (U.S.), Ecolab Inc. (U.S.),

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Disinfectants and Biocides in Swimming Pools and Recreational Water Treatment Market Segmentation

By Product Type

- Chlorine-based Disinfectants

- Bromine-based Disinfectants

- Non-Halogen Oxidizing Biocides

- Non-Oxidizing Biocides/Algaecides

- Specialty/Ancillary Chemicals

By Application

- Continuous Disinfection

- Shock Treatment/Superchlorination

- Algae Control and Prevention

- Biofilm Control

- Winterization Chemicals

By End-User

- Residential Pools

- Commercial and Public Pools

- Public Swimming Pools

- Hotel and Resort Pools

- Water Parks and Aquatic Centers

- Fitness and Health Club Pools

- School and University Pools

- Community and Municipal Pools

- Therapeutic/Rehabilitation Pools

- Spas and Hot Tubs

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Disinfectants and Biocides in Swimming Pools and Recreational Water Treatment Market

- Lonza Group (Switzerland)

- Axiall Corporation (Westlake Chemical Corporation) (U.S.)

- Olin Corporation (U.S.)

- ICL Group (Israel)

- Albemarle Corporation (U.S.)

- Nippon Soda Co. Ltd. (Japan)

- Clorox PoolandSpa (U.S.)

- Zodiac Pool Systems (Fluidra S.A.) (Spain)

- Solenis LLC (U.S.)

- Ecolab Inc. (U.S.)

* List Not Exhaustive

Research Coverage

This report investigates the evolving dynamics of the Disinfectants and Biocides in Swimming Pools and Recreational Water Treatment Market, offering an in-depth analysis of market trends, technological breakthroughs, and regulatory developments driving growth. USDAnalytics delivers a comprehensive review of competitive strategies, product innovations, and adoption patterns across global markets. This report highlights growth opportunities, advanced disinfection solutions, and sustainability-focused innovations, making it an essential resource for decision-makers, investors, and water treatment professionals seeking actionable insights and strategic foresight.

Scope Highlights:

- Segmentation:

- By Product Type: Chlorine-based Disinfectants, Bromine-based Disinfectants, Non-Halogen Oxidizing Biocides, Non-Oxidizing Biocides/Algaecides, Specialty/Ancillary Chemicals

- By Application: Continuous Disinfection, Shock Treatment/Superchlorination, Algae Control and Prevention, Biofilm Control, Winterization Chemicals

- By End-User: Residential Pools, Commercial and Public Pools, Spas and Hot Tubs

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Data Coverage: Historic data from 2021 to 2024 and forecast data from 2025 to 2034.

- Companies Covered: Lonza Group, Axiall Corporation (Westlake Chemical), Olin Corporation, ICL Group, Albemarle Corporation, Nippon Soda Co. Ltd., Clorox Pool&Spa, Zodiac Pool Systems (Fluidra S.A.), Solenis LLC, Ecolab Inc.

Methodology

USDAnalytics applies a hybrid research methodology integrating extensive primary and secondary research. Primary insights are gathered through expert interviews with manufacturers, distributors, and pool operators, while secondary research leverages verified industry databases, regulatory documents, and technical whitepapers. Market sizing and forecasts rely on a combination of top-down and bottom-up approaches, enhanced by data triangulation to validate assumptions and trends. This rigorous methodology ensures accurate projections, aligning with evolving disinfection technologies, sustainability imperatives, and global market dynamics for the forecast period 2025–2034.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Country-Level Forecasts & Analysis

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements