Market Overview: Algaecides Market to Reach $4.7 Billion by 2034 as Precision Water Management, Regulatory Limits on Copper, and Aquaculture Expansion Drive Innovation

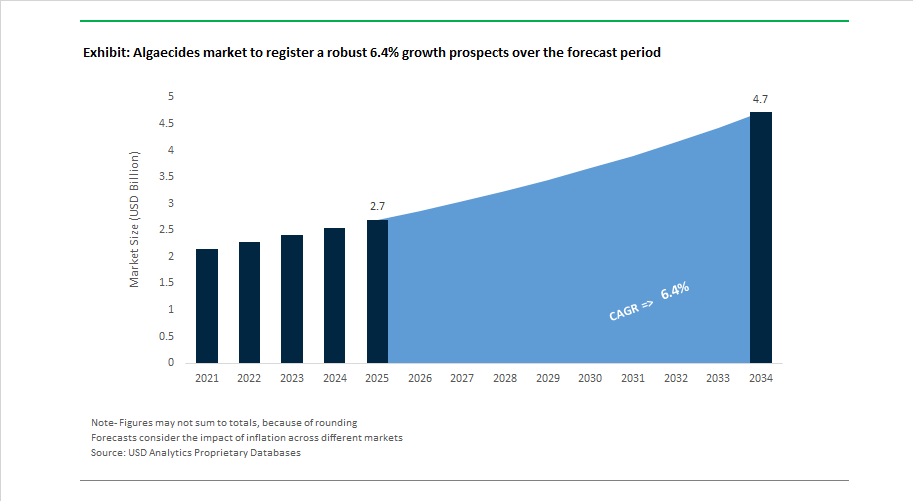

The global algaecides market is projected to grow from $2.7 billion in 2025 to $4.7 billion by 2034, registering a 6.4% CAGR supported by rising demand across aquaculture systems, irrigation reservoirs, agricultural water management, industrial cooling circuits, and recreational water bodies. Algaecides play a critical role in cyanobacteria control, algal bloom mitigation, water clarity maintenance, and biofilm suppression, ensuring water quality and operational efficiency. Growth is influenced by tightening environmental regulations on heavy metals, expansion of Recirculating Aquaculture Systems (RAS), and adoption of precision dosing technologies in fertigation. Market development is shifting toward low-copper, biodegradable, and bio-based algaecide formulations, alongside surfactant-enhanced liquids that improve penetration through dense algal mats.

Product innovation accelerated in April 2024 when Green Water Labs introduced a rapid surface bloom control solution designed for safety in residential and recreational water. Industry transformation advanced in late 2024 as AlgaEnergy restructured following its acquisition by De Sangosse, aligning algae-based technologies with broader biocontrol platforms. Sustainable alternatives gained traction in January 2025 when ARQUIMEA launched BIO100, a fully biodegradable botanical algaecide for organic agriculture. Regulatory pressure intensified in 2025 as the EU imposed strict cumulative copper application limits and California introduced enhanced copper monitoring in water standards, accelerating use of chelated copper and non-copper oxidizing agents. In June 2025, BioSafe Systems released VitriBlü, an acidified copper formulation designed for tank-mix synergy and reduced metal loading.

Industry consolidation and strategic alliances strengthened market reach. In May 2025, Solenis completed integration of NCH and Diversey assets, expanding its footprint in industrial and recreational water treatment. In November 2025, SePRO Corporation formed a strategic alliance with Gowan Company to extend distribution of aquatic and agricultural water management tools. Innovation pipelines expanded in December 2025 when UPL Limited was recognized for its patent portfolio supporting sustainable algae control. Formulation enhancement advanced in November 2025 as BASF expanded bio-based surfactant capacity, improving algaecide delivery performance. Market demand drivers intensified in January 2026 with aquaculture surpassing 35% of total algaecide consumption, and in February 2026 as AI-integrated fertigation systems enabled real-time precision dosing. These developments confirm the transition toward technology-driven, regulation-compliant algae control solutions across global water management sectors.

Strategic Market Trends and High-Value Opportunities Transforming the Algaecides Market

Market Trend: Regulatory Elimination of Copper-Based and PFAS-Linked Synthetic Algaecides Accelerates Market Reformulation

A global tightening of environmental mandates is reshaping algaecide chemistry portfolios and procurement standards, particularly across Europe and North America. The European Commission’s October 2025 MRL review signaled a move toward near-elimination of copper-based compounds for non-essential aquatic applications by 2026, following EFSA’s scientific recommendation targeting a “toxic-free environment.” While agricultural uses may receive transitional allowances, non-essential uses such as decorative ponds and recreational lakes are being redirected toward peracetic acid (PAA) and sodium carbonate peroxyhydrate formulations due to their benign degradation byproducts.

Meanwhile, updated REACH Regulation (EU) 2025/1988 is triggering substitutions by banning PFAS-linked delivery surfactants, increasing R&D expenditure by 35–40% among major producers to develop compliant encapsulation and controlled-release systems. The U.S. EPA’s 2025 Compliance Advisory under the Lead and Copper Rule Improvements (LCRI) has expanded scrutiny on copper emissions into municipal drinking systems, accelerating municipal procurement shifts toward copper-free solutions. Regulatory pressure is no longer incremental—it is acting as a market-defining filter, eliminating non-differentiated suppliers lacking environmental-safe alternatives.

Market Trend: Market Consolidation and Integrated Water Health Platforms Redefine Competition

The competitive landscape is entering an integration cycle, where market leadership is being determined by the ability to provide combined chemistry, monitoring, and digital diagnostics instead of standalone algaecide products. In June 2025, Solenis announced a merger with NCH Corporation, creating a global water-health scale player following earlier integration of Diversey’s hygiene portfolio. This portfolio consolidation enables “360-degree water management,” positioning algaecides as one module within broader water-quality ecosystems that include nutrient control, filtration, and biosecurity.

SePRO is pursuing a precision-chemistry strategy. The company’s April 2025 acquisition of Green Eyes Environmental Monitoring Solutions allows it to integrate real-time nutrient analytics into treatment plans. With quantified phosphate and nitrogen loads, SePRO can prescribe dosage based on biological drivers, reducing chemical dependency and improving lake-restoration outcomes. Strategic alliances, such as SePRO’s November 2025 partnership with Gowan, are re-engineering go-to-market pathways, enabling specialty environmental products to scale through agricultural distribution channels while SePRO concentrates on its aquatics and restoration specializations. This marks a clear industry evolution from volume-centric sales models to diagnostics-anchored, outcome-based procurement.

Market Opportunity: Aquaculture (RAS) Becomes a New Core Demand Engine for System-Safe Algaecides

Recirculating Aquaculture Systems (RAS) are emerging as one of the most influential downstream applications due to their sensitivity to environmental chemistry. Fish farms increasingly require algaecides that eliminate off-flavor blue-green algae without harming fish populations or nitrifying bacteria essential for water recycling. The European Commission’s Implementing Regulation (EU) 2025/1260 formally approving peracetic acid (biocidal type 2) for algaecide use marks a watershed for the aquaculture sector, as PAA breaks down into oxygen and water—leaving no residues in edible tissue.

New aquaculture standards in Norway and Canada require validated, quantifiable disinfection protocols, with premium pricing given to algaecides capable of 99.9% kill rates on Geosmin-producing algae while supporting 95% survival of biofilter bacteria. Because RAS deployments are scaling rapidly—with over USD 1.5 billion in announced facilities for 2025–2026—system-compatible algaecides are shifting from occasional purchase patterns into recurring operational spend. This transforms the RAS demand model into a durable, multi-cycle revenue pipeline.

Market Opportunity: Industrial Biofouling Control in Direct Lithium Extraction (DLE) Enables New Revenue Streams

The global lithium industry presents one of the least-anticipated but highest-value opportunities for algaecides. Direct Lithium Extraction plants rely on ion-exchange resins and selective membranes, both of which are extremely vulnerable to microbial and algal fouling in high-salinity brines. A mere 5% increase in biofouling has been shown to cause a 15% drop in lithium recovery efficiency, which is economically catastrophic in gigawatt-scale EV battery supply chains.

To address this, Solenis and Kemira are piloting high-salinity-tolerant algaecides engineered for geothermal and oilfield brines. These formulations must be “reagent-compatible,” preventing algae growth while avoiding adsorption interference that would lower lithium-ion capture. Sustainability is also a procurement prerequisite, since DLE’s value proposition is based on 90% less land use and groundwater-safe brine reinjection. Facilities therefore require biodegradable, zero-residue treatment agents that ensure regulatory compliance for underground aquifer discharge.

The Algaecides Market is shifting decisively toward regulation-driven reformulation, technology-integrated water-health platforms, and application-specific specialty chemistries. Suppliers that scale eco-safe copper alternatives, integrate diagnostic and digital monitoring capabilities, and develop membrane-safe algaecides for RAS and DLE will define the highest-margin growth segments through 2030.

Algaecides Market Share and Segmentation Insights

Market Share by Type: Copper-Based Algaecides Lead While PAA and Bio-Based Solutions Accelerate

Copper sulfate accounts for approximately 38% of global algaecides demand in 2025, retaining dominance due to low cost and widespread availability across freshwater reservoirs, irrigation canals, and rice paddies. However, sediment accumulation and toxicity concerns are driving regulatory pressure in Europe, gradually shifting demand toward higher-value alternatives. Chelated copper ranks second, gaining share as ethanolamine-, citric-, and EDTA-complexed formulations extend copper ion availability, reduce dosing frequency, and lower total metal loading, making them preferred for potable reservoirs and recreational lakes. Quaternary ammonium compounds remain standard in industrial systems and swimming pools, though aquatic toxicity scrutiny is rising. Peroxyacetic acid based algaecides are the fastest-growing segment, favored in wastewater treatment and organic aquaculture due to residue-free decomposition. Bio-based algaecides are expanding but face performance variability, while dyes and colorants remain the smallest, declining segment.

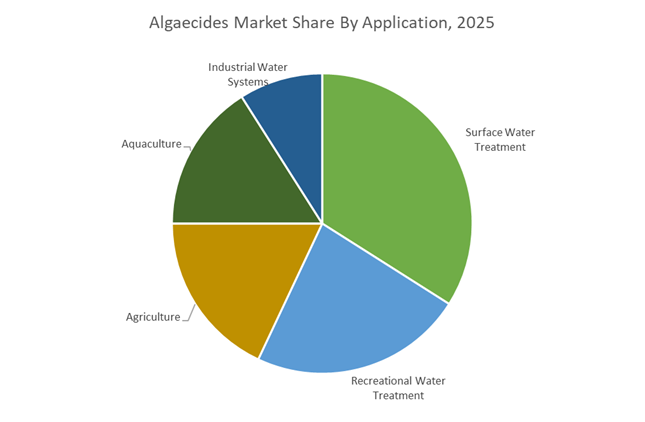

Market Share by Application: Surface Water Dominates as Aquaculture Emerges as Growth Engine

Surface water treatment represents roughly 34% of algaecides consumption in 2025, driven by municipal reservoirs and environmental agencies combating cyanobacteria blooms intensified by climate change. This is non-discretionary spending, increasingly shifting from copper sulfate toward chelated copper and PAA in developed regions. Recreational water treatment ranks second, supported by public pools, ornamental ponds, and sustained residential pool ownership, with QACs and copper formulations leading. Agriculture remains a large but price-sensitive segment, relying heavily on copper sulfate for irrigation canals, although organic mandates are slowly introducing PAA and bio-based options. Aquaculture is the fastest-growing application, as shrimp ponds and salmon farms adopt PAA for oxygen management and zero harvest withdrawal compliance, while restricting copper in marine settings. Industrial water systems remain the smallest segment, tied to cooling towers and data centers, favoring fast-acting chemistries in closed-loop operations.

Competitive Landscape: Prescription Aquatic Control and Sustainable Water Chemistry Redefining the Algaecides Market

The global Algaecides Market is transitioning from broad-spectrum chemical treatments toward precision aquatic management, low-residue oxidative chemistries, and digitally guided water productivity programs. Competitive differentiation increasingly centers on site-specific algae diagnostics, OMRI-certified non-copper solutions, low-foam industrial formulations, and ESG-aligned agricultural platforms. Leading players are integrating algaecides into wider water treatment ecosystems spanning irrigation, cooling towers, aquaculture, and municipal systems, while embedding sustainability through green chemistry, AI-driven bloom prediction, and renewable-powered manufacturing.

SePRO Corporation pioneers prescription-based algae control with field analytics

SePRO Corporation is widely regarded as the technical benchmark in aquatic management, emphasizing prescription-based algae control rather than blanket application. Its flagship products include Captain® XTR for dense algal mats and SeClear, which uniquely combines algaecide action with phosphorus sequestration to address bloom root causes. In late 2025, SePRO expanded PAK 27, a non-copper, OMRI-certified sodium carbonate peroxyhydrate algaecide safe for sensitive species such as koi and trout. The company’s proprietary SeSCRIPT® diagnostics identify algae species before treatment, while FasTEST® analytics enable real-time monitoring of chemical concentrations to ensure regulatory compliance and optimized efficacy.

Solenis integrates algaecides into global total water management platforms

Following its acquisition of Diversey and merger with NCH Industries, Solenis has emerged as a global leader in industrial water treatment. Its Total Water Management strategy positions algaecides as critical to cooling tower efficiency and process water reliability. The integration of NCH’s water treatment operations in 2025 significantly expanded Solenis’ reach across EMEA and Asia-Pacific. In early 2026, Solenis launched low-foam quaternary ammonium algaecides for high-turbulence systems, reducing reliance on secondary defoamers across pulp and paper, industrial cooling, and pool and spa applications.

UPL Limited deploys algaecides as water productivity tools in global agriculture

UPL Limited approaches algae control through its OpenAg platform, integrating algaecides into broader climate-positive agricultural systems. In late 2025, UPL achieved top ESG rankings in the S&P Global Corporate Sustainability Assessment for agricultural solutions. The company has developed drip-irrigation-compatible liquid copper formulations that prevent emitter clogging without corroding equipment. Through its Pro-Nutiva program, algaecides are paired with biostimulants to enhance crop resilience in water-stressed regions. Expansion across Latin America and Southeast Asia during 2025–2026 targets rice paddies and aquaculture, where algae management directly impacts yield and infrastructure reliability.

BioSafe Systems, LLC replaces heavy metals with oxidative, residue-free algaecides

BioSafe Systems leads the adoption of green oxidative chemistry, utilizing peroxyacetic acid and hydrogen peroxide as alternatives to copper and chlorine. Its GreenClean® and TerraClean® brands decompose into water and oxygen, leaving no toxic residues in soil or waterways. The company’s Sustainable Biosecurity strategy aligns algaecides with food safety and irrigation treatment programs, ensuring compatibility with Integrated Pest Management systems. In 2025, BioSafe introduced atomized PAA delivery for greenhouse operations, enabling 360-degree algae and pathogen control with minimal labor, reinforcing its role in sustainable horticulture and protected agriculture.

BASF SE embeds smart farming and green chemistry into algae control

BASF SE applies its global R&D and Verbund integration to supply both formulated algaecides and high-purity intermediates used by downstream producers. Under its Winning Ways strategy scaled in 2025–2026, BASF is phasing out legacy high-VOC systems in favor of Near-Zero SVOC technologies. Its Agricultural Solutions portfolio targets algae in high-value horticulture, supported by surfactants and biocides optimized for modern spray systems. BASF is also leveraging its Global Digital Hub in Hyderabad to develop AI-enabled tools that forecast algal blooms using nitrogen runoff data, embedding predictive analytics into farm-level decision making.

Lonza supplies core microbial control actives for global algaecide formulations

Lonza remains a critical upstream technology provider despite pivoting toward biopharma CDMO services. Following completion of its CHI carve-out in 2025–2026, Lonza refocused capital on specialty chemistry platforms, including quaternary ammonium compounds that serve as active ingredients in many pool and industrial algaecides. The company is expanding regional manufacturing across the US and Europe to localize supply and mitigate geopolitical risks. As of January 2026, Lonza transitioned all US and European operations to renewable electricity, strengthening its appeal to customers seeking sustainably produced microbial control agents.

United States Algaecides Market: Water Governance Tightening and Dual-Action Formulation Leadership

The United States is strengthening regulatory oversight while accelerating innovation in advanced algaecide chemistries. In late 2025, the U.S. Environmental Protection Agency advanced the Clean Water Act Section 401 Water Quality Certification Improvement Rule for final White House review. This move grants states and tribal authorities expanded control over chemical discharges in energy and infrastructure projects, directly increasing compliance requirements for algaecides used in reservoirs, cooling ponds, and industrial waterways.

Innovation is keeping pace with regulation. SePRO Corporation launched an upgraded SeClear Algaecide and Water Quality Enhancer in 2025, combining photosynthesis inhibition with phosphorus sequestration to address eutrophication at its source. Strategic market access expanded further in November 2025 when SePRO entered a marketing alliance with Gowan Company to scale advanced algaecides such as Brake® in high-value crop systems. On the demand side, the National Ground Water Association reported a regulatory push for primary drinking water standards, accelerating adoption of NSF/ANSI/CAN 60 certified products. Trade data from spring 2025 also indicate rising costs for imported petrochemical intermediates, pushing formulators toward domestic chelated copper and peroxyacetic acid routes. Ecological urgency remains high, with the U.S. Department of the Interior allocating new funds for rapid-response algaecide programs in the Great Lakes to curb toxin-producing cyanobacteria.

Brazil Algaecides Market: Bio-Inputs Momentum and Aquatic Agriculture Expansion

Brazil’s algaecides landscape is defined by regulatory velocity and sustainability-driven substitution. In December 2025, the country registered a record 560 new pesticides and chemical inputs, underscoring a fast-moving approval environment for crop protection and water treatment solutions. Notably, around 25% of 2025 registrations were classified as biological or bio-inputs, signaling a decisive shift toward eco-compatible algaecides in agriculture.

Strategic consolidation is reinforcing this transition. De Sangosse expanded its Brazilian presence in 2025 through the acquisition of specialized assets from AlgaEnergy, integrating microalgae-based biocontrol solutions into sustainable farming portfolios. At a policy and reputational level, COP30 in Belém in November 2025 highlighted the role of advanced algaecides in rice cultivation to manage methane emissions and improve water quality in flooded fields. Meanwhile, chemical pesticide imports rose sharply in late 2025, driven by the growth of aquaculture and large-scale irrigation, reinforcing Brazil’s dual reliance on imported actives and locally approved biological alternatives.

China Algaecides Market: Mandatory Standards and Export-Oriented Modernization

China is aligning scale with stricter quality governance in the algaecides sector. The implementation of GB 30981.2-2025 in early 2026 introduced tighter limits on hazardous residues in industrial algaecides and water treatment agents used in public infrastructure, raising compliance thresholds for domestic producers.

At the same time, production modernization is accelerating. BASF inaugurated a loopamid production facility in Shanghai in 2025. While primarily focused on textiles, the site’s advanced 3D-printed catalyst technology is being cross-applied to synthesize higher-efficiency algaecide precursors. Export momentum remains strong, with China reporting a 29% increase in crop protection exports through 2025 following global restocking. State-backed R&D is also intensifying, as Sinochem International received funding to develop non-persistent algaecides tailored for sensitive aquaculture ecosystems in the South China Sea.

Australia Algaecides Market: Climate Stress Response and Waterway Protection

Australia’s algaecide demand is increasingly shaped by climate variability and water security concerns. In December 2025, the Murray–Darling Basin Authority issued a Water Quality Threats report identifying critical blue-green algae outbreaks, triggering emergency algaecide protocols across New South Wales and Victoria.

Beyond emergency response, industrial rehabilitation is emerging as a key use case. The CSIRO unveiled mid-2025 research on mine site rehabilitation that integrates specialized algaecides and biological agents to treat wastewater and remove heavy metals in remote mining regions. Climate adaptation pressures are compounding demand, with the 2025 Sustainable Yields Report linking changing rainfall patterns to increased algaecide use for irrigation channel maintenance across the basin.

Germany Algaecides Market: PFAS Restrictions and Corporate Restructuring

Germany is steering the European algaecides agenda through regulatory reform and corporate realignment. In August 2025, the European Chemicals Agency published an updated PFAS restriction proposal, directly affecting fluorinated algaecides and surfactants and accelerating reformulation toward non-fluorinated alternatives.

Corporate strategy is adapting accordingly. BASF SE announced plans to IPO its Agricultural Solutions division in 2026, aiming to create a focused entity centered on sustainable crop protection and algaecide R&D. Production decarbonization is also advancing, as Solvay confirmed that most of its European soda ash plants had phased out coal by late 2025, supporting hydrogen peroxide-based algaecide production for remote water treatment.

India Algaecides Market: Patent Strength and Urban Water Rejuvenation

India’s algaecides market is being pulled by intellectual property leadership and urban water restoration programs. UPL Limited received the Best Patent Portfolio award at the CII Industrial IP Awards 2025, reflecting a deep pipeline of patents covering sustainable algaecide and surfactant technologies.

On the demand side, the Ministry of Jal Shakti launched a 2025 grant program for the rejuvenation of urban water bodies, driving procurement of liquid algaecides for municipal ponds, lakes, and recreational spaces. This combination of innovation ownership and public-sector demand is positioning India as a testing ground for scalable, environmentally compatible algaecide solutions.

Country-Level Strategic Positioning in the Algaecides Industry

Algaecides market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Industry Implication

|

|

United States

|

Water quality governance and dual-action products

|

Compliance-driven adoption with innovation premium

|

|

Brazil

|

Bio-input approvals and aquatic agriculture growth

|

Rapid substitution toward sustainable algaecides

|

|

China

|

Mandatory residue limits and export scaling

|

Higher standards with strong global supply role

|

|

Australia

|

Climate-induced water quality risks

|

Emergency and rehabilitation-focused demand

|

|

Germany

|

PFAS reform and corporate restructuring

|

Accelerated shift to non-fluorinated chemistries

|

|

India

|

Patent leadership and urban water programs

|

Innovation-led municipal and ecological use cases

|

Algaecides Market Report Scope

Algaecides market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$4.7 Billion

|

|

Market Growth Rate

|

6.4%

|

|

Segments

|

By Type (Copper Sulfate, Chelated Copper, Quaternary Ammonium Compounds, Peroxyacetic Acid Based Algaecides, Dyes and Colorants, Bio Based Algaecides), By Form (Liquid Formulations, Dry Formulations, Pressurized Sprays), By Mode of Action (Selective Algaecides, Non Selective Algaecides), By Application (Surface Water Treatment, Aquaculture, Agriculture, Industrial Water Systems, Recreational Water Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, UPL Limited, SePRO Corporation, Solvay SA, Corteva Inc, Syngenta Group, Nufarm Limited, BioSafe Systems, Lonza Group AG, Air Liquide SA, Ecolab Inc, Bayer AG, Albemarle Corporation, American Algaecide Company, Waterco Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Algaecides Market Segmentation

By Type

- Copper Sulfate

- Chelated Copper

- Quaternary Ammonium Compounds

- Peroxyacetic Acid Based Algaecides

- Dyes and Colorants

- Bio Based Algaecides

By Form

- Liquid Formulations

- Dry Formulations

- Pressurized Sprays

By Mode of Action

- Selective Algaecides

- Non Selective Algaecides

By Application

- Surface Water Treatment

- Aquaculture

- Agriculture

- Industrial Water Systems

- Recreational Water Treatment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Algaecides Industry

- BASF SE

- UPL Limited

- SePRO Corporation

- Solvay SA

- Corteva Inc

- Syngenta Group

- Nufarm Limited

- BioSafe Systems

- Lonza Group AG

- Air Liquide SA

- Ecolab Inc

- Bayer AG

- Albemarle Corporation

- American Algaecide Company

- Waterco Limited

*- List not Exhaustive