Sub-Zero Curing Polyaspartic Floor Coatings Transforming Cold Storage Maintenance Cycles

The polyaspartic coatings market is experiencing accelerated adoption in cold chain infrastructure, particularly within freezer warehouses and temperature-controlled logistics facilities. Facility operators are transitioning away from epoxy and methyl methacrylate systems due to their inability to cure effectively in sub-zero environments, creating operational bottlenecks and costly downtime.

Advanced polyaspartic floor coatings have redefined performance benchmarks by enabling full functional curing at temperatures as low as −20°F (−29°C). This capability eliminates the need for facility-wide heating cycles, which traditionally required 48 to 72 hours and significant energy expenditure. In high-throughput cold storage operations, this translates into uninterrupted logistics flow and preservation of inventory integrity.

Rapid return-to-service performance is a defining advantage. Modern formulations achieve a walk-on state within 30 to 45 minutes, allowing maintenance activities to be completed within tightly controlled operational windows. This enables facility managers to execute repairs during limited off-peak periods without disrupting supply chain continuity, a critical requirement in sectors such as food distribution and pharmaceutical cold storage.

Thermal durability further strengthens adoption. Polyaspartic coatings exhibit approximately 25% higher elongation compared to conventional epoxy systems, allowing them to withstand repeated thermal cycling during defrost operations without cracking or delamination. This resilience ensures long-term substrate protection under extreme temperature fluctuations, positioning polyaspartics as a preferred solution for high-performance industrial flooring in cold environments.

Market Analysis: High-Throughput Polyaspartic Coatings Optimizing OEM Truck Bed Liner Manufacturing

Automotive OEMs are increasingly integrating polyaspartic coatings into high-volume truck bed liner production to enhance manufacturing efficiency and product durability. This transition is driven by the limitations of traditional polyurea systems, particularly in terms of UV stability and extended processing timelines.

Polyaspartic coatings significantly compress production cycles by enabling rapid recoat and assembly timelines. While legacy polyurea systems often require up to 24 hours before secondary processing, polyaspartic systems allow mechanical assembly within 2 to 4 hours. This reduction in cycle time increases assembly line throughput by approximately 15% to 20%, directly improving production efficiency in large-scale automotive manufacturing facilities.

UV stability is a critical differentiator. As inherently aliphatic systems, polyaspartic coatings eliminate the need for additional UV-resistant topcoats. Accelerated weathering tests demonstrate zero yellowing or chalking after 3,000 hours of exposure, compared to aromatic polyurea systems that typically degrade within 500 hours. This ensures long-term aesthetic retention for exposed truck bed surfaces, a key requirement in premium and commercial vehicle segments.

Mechanical performance also supports adoption. In standardized abrasion testing (ASTM D4060), polyaspartic coatings exhibit weight loss below 30 mg under high-load conditions, outperforming conventional coatings and drop-in liners. This superior abrasion resistance enhances durability against cargo-induced wear, extending the service life of coated components and reducing warranty claims for OEMs.

Market Trend: FHWA Bridge Preservation Funding Accelerating Adoption of Fast-Cure Polyaspartic Deck Systems

The expansion of infrastructure funding in the United States is creating a substantial growth opportunity for polyaspartic coatings in bridge preservation and rehabilitation projects. The Federal Highway Administration’s Bridge Formula Program has allocated $5.3 billion for fiscal year 2026, with a significant portion directed toward preservation and protective coating applications.

Within this framework, approximately $1.85 billion is specifically targeted at preservation-focused initiatives under the Bridge Investment Program. This funding is driving demand for high-performance protective coatings that can extend asset lifespan while minimizing traffic disruption during maintenance operations.

Polyaspartic coatings are uniquely positioned to benefit from this trend due to their rapid curing characteristics. Infrastructure agencies are prioritizing accelerated bridge construction methodologies to reduce lane closure durations, particularly in high-traffic metropolitan areas where closure penalties can exceed $50,000 per day. Polyaspartic deck coatings enable same-day return to service, allowing contractors to complete rehabilitation work within compressed timeframes.

This alignment between funding priorities and performance capabilities is creating a strong adoption pipeline for polyaspartic technologies in transportation infrastructure. Coating manufacturers that can demonstrate long-term durability, rapid cure, and compliance with federal performance standards are gaining increased specification in state-level infrastructure projects.

Market Trend: China’s GB/T 50067-2026 Standards Driving Mandatory Adoption of Low-VOC Fast-Cure Floor Coatings

China’s regulatory environment is emerging as a key catalyst for polyaspartic coatings, particularly in urban infrastructure and parking facility applications. The implementation of the revised GB/T 50067-2026 standard introduces strict performance and environmental requirements for coatings used in parking structures across Tier 1 and Tier 2 cities.

A critical requirement under the new standard is the achievement of Shore D hardness greater than 60 within 24 hours of application. This performance threshold effectively excludes traditional slow-curing epoxy systems from large-scale urban renewal and infrastructure projects. Polyaspartic coatings, with their rapid curing kinetics, are among the few technologies capable of consistently meeting this requirement.

Environmental compliance is equally influential. The standard aligns with China’s broader emissions reduction strategy by capping VOC levels for indoor floor coatings at below 50 g/L. High-solids polyaspartic formulations, characterized by near-zero VOC emissions, are well-positioned to meet these stringent criteria while maintaining high-performance mechanical properties.

The scale of China’s urban development initiatives further amplifies this opportunity. With extensive investment in underground parking infrastructure and smart city projects, the demand for fast-curing, low-emission coating systems is expected to rise significantly. This regulatory-driven transition is creating a favorable market landscape for polyaspartic coating manufacturers targeting large-scale construction and refurbishment applications.

Market Opportunity: China Polyaspartic Coatings Market: Water-Immunity Innovation and Infrastructure Expansion

China dominates the global polyaspartic coatings market, driven by large-scale infrastructure development and rapid adoption of advanced coating chemistries. The deployment of “water-immunity” polyaspartic coatings in major hydraulic engineering projects, such as the Danjiangkou Reservoir, highlights the country’s leadership in high-performance coatings capable of withstanding continuous water exposure without degradation.

Regulatory developments, including GB 4806.10-2026, are accelerating the transition toward PAA-free polyaspartic formulations, particularly in food processing environments. The semiconductor sector is also fueling demand, with increased use of 100% solids polyaspartic coatings in cleanrooms due to their low outgassing and chemical resistance. Innovations such as sub-zero curing resins are expanding application possibilities in cold-chain logistics, while marine infrastructure projects are adopting polyaspartic systems to improve durability and reduce maintenance cycles. Strategic investments in precursor production are further strengthening China’s position as a global leader in polyaspartic coatings.

Market Opportunity: United States Polyaspartic Coatings Market: Logistics Expansion and PFAS-Free Transition

The U.S. polyaspartic coatings market is experiencing strong growth, driven by logistics infrastructure expansion, regulatory compliance, and advanced material innovation. The shift toward PFAS-free polyaspartic coatings is accelerating as manufacturers prepare for upcoming environmental regulations, ensuring compliance without compromising performance.

The rise of e-commerce has fueled demand for fast-return-to-service (FRTS) flooring systems, particularly in large-scale warehouse and distribution centers. Federal investments under the CHIPS Act are also boosting demand for anti-static polyaspartic coatings in semiconductor fabs. Infrastructure modernization projects funded by the IIJA are driving adoption of single-coat polyaspartic technologies for bridge recoating, reducing labor and downtime. Additionally, the integration of smart monitoring sensors within polyaspartic coatings is enabling real-time structural health tracking, reinforcing the U.S. leadership in advanced coating technologies.

Polyaspartic Coatings Market Share and Segmentation Insights

By System Type: Solid Color Polyaspartic Coatings Lead with Performance-Driven Adoption

The solid color polyaspartic coatings segment captured a dominant 38.4% market share in 2025, emerging as the leading system type due to its superior performance in commercial flooring and industrial flooring applications. Widely deployed across warehouses, automotive garages, retail showrooms, and food processing facilities, solid color systems benefit from rapid cure times (1–2 hours to foot traffic), enabling minimal downtime and faster project completion—key drivers in high-demand industrial environments. Additionally, the seamless, durable finish enhances chemical resistance and abrasion performance, positioning these coatings as a preferred alternative to traditional epoxy systems. A major growth catalyst is their exceptional UV stability, as polyaspartic topcoats resist yellowing and degradation, making them ideal for outdoor applications such as parking decks, rooftop surfaces, and driveways. This combination of fast-curing technology, long-term durability, and UV-resistant properties continues to accelerate adoption across infrastructure and construction sectors, reinforcing solid color systems’ market leadership.

By Sales Channel: Professional Contractors Capture Majority Share Through Expertise and Warranty Assurance

The professional contractor segment accounted for a commanding 65.6% share of the polyaspartic coatings market in 2025, reflecting the critical role of skilled applicators in delivering high-performance coating systems. Due to the short pot life of polyaspartic coatings (10–30 minutes), application requires precision, speed, and technical expertise—capabilities primarily offered by experienced contractors. These professionals provide advanced surface preparation techniques such as shot blasting and diamond grinding, along with moisture mitigation solutions, ensuring optimal adhesion and long-term coating performance. Furthermore, end users increasingly rely on contractor-backed warranties ranging from 5 to 15 years, covering issues like delamination, hot tire pickup, and chemical staining. This shifts operational risk away from manufacturers and enhances buyer confidence in large-scale commercial and industrial projects. As demand for high-durability, fast-installation floor coating systems grows, the contractor-led sales channel is expected to maintain its dominance in the global polyaspartic coatings market.

Competitive Landscape of the Polyaspartic Coatings Market

Covestro Leads Polyaspartic Innovation with Circular Resin Technologies and Mobility Applications

Covestro AG remains the pioneer and dominant upstream supplier in the polyaspartic coatings market, leveraging its legacy as the original patent holder of the technology. Between 2025 and 2026, the company has aggressively transitioned toward bio-based and circular feedstocks, scaling its Desmophen® NH portfolio to meet growing demand. Its Pasquick® technology reduces coating layers from three to two, cutting labor costs by up to 30% and VOC emissions by 50%. Covestro is also targeting advanced mobility applications, demonstrating signal-transparent polyaspartic coatings for 5G-enabled vehicles and autonomous systems. This strong R&D focus positions the company at the forefront of next-generation coating technologies.

Sherwin-Williams Dominates Commercial Flooring with Rapid-Cure Polyaspartic Systems

The Sherwin-Williams Company is a market leader in the polyaspartic coatings segment, particularly in construction and commercial flooring applications. Its EnviroLastic® series is widely used for same-day return-to-service coatings, ideal for high-traffic environments such as stadiums and retail spaces. The company continues to expand its “Pro-Preference” distribution model, offering technical support for large-scale projects globally. With building and construction accounting for over 30% of polyaspartic demand, Sherwin-Williams is well-positioned to capture growth in green building and infrastructure projects, supported by its focus on ISO-compliant emissions reporting.

PPG Expands Polyaspartic Applications with Automotive Integration and Infrastructure Solutions

PPG Industries, Inc. is leveraging its cross-industry expertise to expand polyaspartic coating applications across automotive OEM, infrastructure, and industrial segments. In 2026, the company introduced advanced polyaspartic clearcoats as part of its “Parallels” color initiative, enabling high-gloss, UV-resistant finishes. Its acquisition of Ozark Materials strengthens its presence in pavement markings, where polyaspartic coatings are replacing traditional thermoplastics due to their rapid curing and durability. PPG’s integration with the EV supply chain further enhances its position, providing dielectric and fire-resistant coatings for battery systems.

AkzoNobel Strengthens Premium Polyaspartic Coatings with Aerospace and Energy Applications

AkzoNobel N.V. is focusing on high-value applications in the polyaspartic coatings market, particularly in aerospace and energy-efficient infrastructure. In 2026, the company invested €50 million to upgrade its aerospace coatings facility in Illinois, enhancing production of advanced polyaspartic coatings. Its Intergard® and Interfine® series are widely used in protective and marine environments. AkzoNobel is also supplying coatings for innovative solar-absorbing wall technologies, leveraging polyaspartic hybrid binders to improve energy efficiency. Its partnerships with BASF and Arkema aim to reduce VOC emissions and carbon footprint, reinforcing its leadership in sustainable coating solutions.

Sika Leads Infrastructure Applications with High-Performance Polyaspartic Flooring Systems

Sika AG is a global leader in construction chemicals and polyaspartic coatings, particularly for infrastructure and industrial flooring. Its SikaFloor® systems incorporate polyaspartic technology to deliver fast-curing, moisture-tolerant coatings suitable for extreme conditions, including temperatures as low as -10°C. Sika is a major contributor to the growth of quartz-based polyaspartic systems used in clean rooms and food processing facilities. Its refurbishment strategy focuses on extending the service life of aging infrastructure, with polyaspartic coatings providing durability improvements of over 15 years compared to traditional systems.

Rust-Oleum Bridges DIY and Industrial Markets with High-Strength Polyaspartic Coating Systems

Rust-Oleum, part of RPM International Inc., occupies a unique position in the polyaspartic coatings market, targeting both professional and DIY segments. Its RockSolid® and Concrete Saver® product lines offer high-strength, easy-to-apply coating systems, including “One-Day Garage” kits designed for residential applications. These coatings are significantly stronger than traditional epoxy systems, providing enhanced durability and ease of use. The company is also innovating with UV-cured polyaspartic hybrids for industrial maintenance, enabling near-instant curing. With expansion plans in Asia-Pacific and the Middle East, Rust-Oleum is strengthening its position in accessible, high-performance coating solutions.

Germany Polyaspartic Coatings Market: Low-Emission Standards and Circular Economy Leadership

Germany is at the forefront of the European polyaspartic coatings market, emphasizing low-emission formulations, indoor air quality, and circular economy principles. New EU Eco-label criteria are pushing manufacturers to achieve ultra-low VOC emissions, positioning polyaspartic coatings as a preferred alternative to traditional epoxy systems.

German innovation is focused on high-performance, environmentally compliant coatings, including PVD-hybrid polyaspartic systems for hydrogen infrastructure applications. Research centers are advancing plasma-enhanced polyaspartic deposition technologies to improve coating durability on lightweight automotive components. The adoption of digital product passports is enhancing traceability and sustainability across the value chain. Additionally, the growing use of UV-stable polyaspartic coatings in renewable energy applications, such as solar farms, highlights Germany’s leadership in sustainable coating solutions.

Saudi Arabia Polyaspartic Coatings Market: Vision 2030 and High-Temperature Durability

Saudi Arabia is emerging as a key market for polyaspartic coatings, driven by large-scale infrastructure projects under Vision 2030 and the need for coatings capable of withstanding extreme climatic conditions. Developments such as NEOM are mandating the use of UV-stable polyaspartic coatings to prevent discoloration and degradation in desert environments.

The oil and gas sector is also driving demand, with polyaspartic coatings standardized for chemical-resistant flooring in Aramco facilities. Innovations such as IR-reflective “Cool-Poly” coatings are improving thermal performance in high-temperature environments. Public utility projects are increasingly adopting polyaspartic-lined structures for enhanced corrosion resistance, while localization initiatives under IKTVA are strengthening domestic production capabilities and reducing reliance on imports.

India Polyaspartic Coatings Market: Smart Cities Growth and PLI-Driven Manufacturing

India is one of the fastest-growing markets in the polyaspartic coatings industry, supported by urbanization, infrastructure development, and government incentives. The expansion of PLI schemes for specialty chemicals is encouraging domestic production of polyaspartic resins, strengthening local supply chains.

Infrastructure modernization, including railway upgrades, is driving demand for high-durability polyaspartic coatings in applications such as train flooring. The growth of premium residential and commercial construction is also boosting demand for decorative polyaspartic systems, particularly in metropolitan regions. Government initiatives like the Smart Cities Mission are promoting the use of polyaspartic-coated materials in public infrastructure to withstand harsh environmental conditions. Additionally, innovations in agritech are expanding applications into sensor protection, highlighting the versatility of polyaspartic coatings in emerging sectors.

South Korea Polyaspartic Coatings Market: Semiconductor Precision and Marine Applications

South Korea’s polyaspartic coatings market is closely aligned with its leadership in semiconductors, OLED displays, and marine engineering. The expansion of semiconductor clusters is driving demand for plasma-resistant polyaspartic coatings used in cleanroom facilities and advanced fabrication environments.

The country is also innovating in marine anti-fouling coatings, integrating polyaspartic systems with PVD technologies to enhance performance and environmental sustainability. Applications in Thin-Film Encapsulation (TFE) for flexible displays highlight the role of hybrid coatings in advanced electronics. Additionally, South Korea is leading in high-barrier packaging solutions, utilizing polyaspartic coatings to improve durability and protection. The growing demand for premium cosmetic packaging finishes is further driving innovation in PVD-metallized polyaspartic coatings.

United Arab Emirates Polyaspartic Coatings Market: Infrastructure Growth and Aviation Applications

The UAE is emerging as a high-growth hub in the polyaspartic coatings market, driven by infrastructure expansion, aviation sector growth, and luxury real estate development. Projects such as Dubai Aviation City are utilizing high-performance polyaspartic flooring systems designed to withstand heavy mechanical loads and chemical exposure.

Government investments in infrastructure are accelerating the adoption of fast-curing polyaspartic coatings for metro expansions and commercial developments. The growing demand for premium residential flooring solutions, particularly in luxury villas, is further boosting market growth. Strict building codes requiring UV-resistant waterproofing systems are increasing the adoption of polyaspartic coatings in construction. Additionally, the integration of polyaspartic coatings in public utilities is enhancing durability and corrosion resistance in high-salinity environments, positioning the UAE as a key regional market.

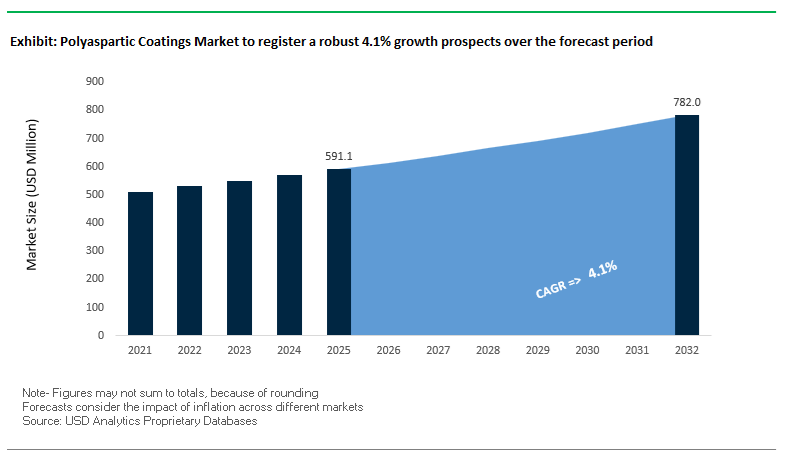

Polyaspartic Coatings Market Report Scope

Polyaspartic Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$591.1 Million

|

|

Market Size (2032)

|

$783.1 Million

|

|

Market Growth Rate

|

4.1%

|

|

Segments

|

By Type (Pure Polyaspartic, Hybrid Polyaspartic), By Technology (Solvent-borne, Water-borne, Powder-based Polyaspartic, Radiation-Cured), By System Layer (Single-Coat Systems, Multi-Layer Systems), By Number of Components (Two-Component, One-Component), By System Type (Quartz Systems, Metallic Systems, Solid Color, Flake), By End-Use Industry (Building and Construction, Infrastructure, Transportation, Industrial, Power Generation, Marine), By Application (Flooring, Corrosion Control and Protective Coating, Waterproofing and Moisture Barriers, Joint Fillers and Sealants, Decorative Architecture), By Sales Channel (Direct Sales, Specialty Construction Chemical Distributors, Professional Contractor)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, Covestro AG, PPG Industries, Inc., Akzo Nobel N.V., BASF SE, Sika AG, RPM International Inc., LATICRETE International, Inc., Hempel A/S, Jotun A/S, Flexmar Polyaspartics, The VersaFlex Companies, MAPEI S.p.A., Duraamen Engineered Products Inc., Feiyang Protech

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Polyaspartic Coatings Market Segmentation

By Type

- Pure Polyaspartic

- Hybrid Polyaspartic

By Technology

- Solvent-borne

- Water-borne

- Powder-based Polyaspartic

- Radiation-Cured

By System Layer

- Single-Coat Systems

- Multi-Layer Systems

- Topcoats

- Intermediate

- Clearcoats

By Number of Components

- Two-Component

- One-Component

By System Type

- Quartz Systems

- Metallic Systems

- Solid Color

- Flake

By End-Use Industry

- Building and Construction

- Infrastructure

- Transportation

- Industrial

- Power Generation

- Marine

By Application

- Flooring

- Corrosion Control and Protective Coating

- Waterproofing and Moisture Barriers

- Joint Fillers and Sealants

- Decorative Architecture

By Sales Channel

- Direct Sales

- Specialty Construction Chemical Distributors

- Professional Contractor

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Polyaspartic Coatings Industry

- The Sherwin-Williams Company

- Covestro AG

- PPG Industries, Inc.

- Akzo Nobel N.V.

- BASF SE

- Sika AG

- RPM International Inc.

- LATICRETE International, Inc.

- Hempel A/S

- Jotun A/S

- Flexmar Polyaspartics

- The VersaFlex Companies

- MAPEI S.p.A.

- Duraamen Engineered Products Inc.

- Feiyang Protech

*- List not Exhaustive