Pavement Preservation Economics and Climate-Responsive Technologies Driving Steady Expansion

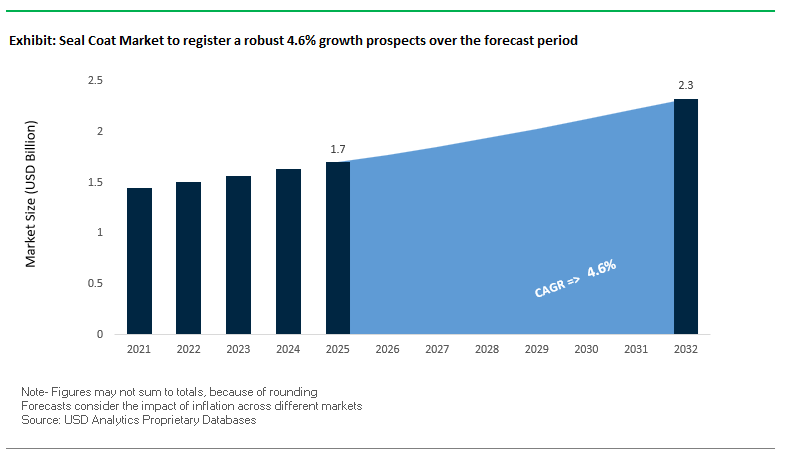

The global Seal Coat Market is experiencing consistent growth, supported by rising investments in road maintenance, pavement preservation strategies, and urban infrastructure resilience. The market was valued at $1.7 billion in 2025 and is projected to reach $2.3 billion by 2032, expanding at a CAGR of 4.6% during 2025–2032. Unlike new road construction cycles, seal coating demand is largely maintenance-driven, benefiting from recurring application requirements across highways, parking lots, airports, and municipal road networks.

A central growth driver is the increasing shift toward preventive maintenance over capital-intensive reconstruction, particularly among municipalities facing budget constraints. Seal coating offers a cost-efficient lifecycle extension solution, protecting asphalt surfaces from oxidation, UV degradation, water ingress, and chemical exposure. This economic advantage is driving adoption across both developed markets with aging infrastructure and emerging economies experiencing rapid urbanization.

Another defining trend is the emergence of climate-adaptive seal coating technologies, particularly reflective and heat-mitigating formulations. Urban centers are increasingly deploying cool pavement sealers to address urban heat island effects, improve surface durability, and align with sustainability mandates. These solutions not only enhance pavement performance but also contribute to energy savings and improved urban livability, positioning seal coatings as part of broader climate resilience strategies.

The market is also witnessing growing demand for performance-enhancing additives and advanced formulations, including polymer-modified emulsions and epoxy fortifiers. These innovations are improving abrasion resistance, flexibility, and longevity, particularly in high-traffic commercial zones such as logistics hubs and industrial parks. Additionally, expanding applications in water infrastructure, industrial containment, and specialty coatings are diversifying the market beyond traditional pavement sealing.

Market Analysis: Equipment Innovation, Reflective Pavement Programs, and Specialty Coating Expansion Reshaping Industry Dynamics

The seal coat market is undergoing a transformation driven by equipment innovation, product formulation advancements, and evolving distribution strategies, reflecting a shift toward efficiency, specialization, and sustainability. In April 2026, GemSeal introduced the KM Pothole Punisher Asphalt Hotbox, a critical advancement designed to maintain optimal asphalt temperatures during repair operations. This innovation enhances the repair-to-seal workflow, enabling contractors to achieve more consistent and durable sealcoat applications, particularly in high-volume maintenance environments.

Product innovation is increasingly centered on performance enhancement and durability optimization. Neyra Industries’ May 2025 launch of Armorflex Epoxy Fortifier and Duraflex Premium Fortifier represents a strategic push toward additive-driven performance upgrades. These formulations significantly improve the longevity and wear resistance of seal coats, addressing the needs of high-traffic commercial and municipal applications.

Weather adaptability remains a critical operational challenge in seal coating, prompting innovations such as Western Colloid’s ElastaHyde QS (March 2025). This quick-set formulation is engineered for application in damp or unpredictable weather conditions, reducing project delays and improving contractor productivity. Such solutions are particularly valuable in regions with volatile climate patterns, where downtime directly impacts project timelines and costs.

The expansion of cool pavement technologies is emerging as a major industry trend. GuardTop’s CoolSeal program expansion (December 2025) and its earlier Reflect Effect partnership (July 2024) demonstrate the increasing adoption of reflective pavement coatings capable of reducing surface temperatures by up to 20°F. These initiatives are gaining traction among municipalities seeking to mitigate urban heat islands while extending pavement life.

Distribution models are also evolving to improve market accessibility and speed. Dalton Enterprises’ June 2025 launch of DaltonCoatingsX.com represents a shift toward direct-to-contractor supply chains, reducing reliance on retail intermediaries and enabling faster procurement of specialized sealcoat products. Additionally, its QuickPatch H2O Pail (November 2024) serves as a complementary pre-seal repair solution, reinforcing integrated maintenance workflows.

Beyond traditional pavement applications, manufacturers are expanding into specialized industrial and infrastructure segments. ArmorThane’s AquaSafe polyurea coating certification (January 2026) for potable water systems highlights growing opportunities in municipal water infrastructure and liquid containment. Similarly, Seal Master Corporation’s innovation in inflatable seals for nuclear waste containment (March 2026) and SealMaster’s high-speed industrial dryer seals (September 2025) indicate diversification into high-specification industrial environments requiring advanced sealing technologies.

Market Trend: Regulatory Elimination of Coal Tar Sealers Driven by PAH Toxicity Thresholds

The seal coat industry is undergoing a structural transformation as regulatory bodies intensify restrictions on coal tar-based sealants due to their high Polycyclic Aromatic Hydrocarbon (PAH) content. Under the 2026 “Legacy CCR” Final Rule and aligned state-level legislation such as Illinois HB2487, a de facto nationwide phase-out is materializing, with an enforced sales ban effective October 1, 2026. Conventional refined coal tar sealers typically contain PAH concentrations ranging from 50,000 to 100,000 mg/kg, whereas compliant asphalt emulsion alternatives are capped below 1,000 mg/kg, representing a 100-fold reduction in toxicological impact. This sharp regulatory divergence is accelerating product reformulation strategies and forcing contractors to transition supply chains toward environmentally compliant sealcoating solutions. As of April 2026, more than 15 U.S. states and numerous municipalities have enacted restrictions, directly impacting over 40% of sealcoating operations across the Midwest and Northeast. This shift is not merely compliance-driven but is reshaping procurement specifications, contractor training requirements, and long-term pavement maintenance strategies.

Market Trend: ASTM D8265-25 Standard Expands Application Window Through Low-Temperature Curing Protocols

The introduction of ASTM D8265-25 establishes a critical technical benchmark for sealcoat application under suboptimal environmental conditions, directly addressing long-standing seasonal constraints in the pavement maintenance industry. Historically, sealcoating operations were limited to ambient temperatures above 50°F, restricting project cycles to warmer months. The new standard enables application at temperatures as low as 40°F through the integration of advanced chemical accelerants and polymer modifiers. Additionally, ASTM D8265-25 formalizes relative humidity tolerance parameters, permitting application in environments with up to 85% RH when rapid-set technologies are deployed. This expands the operational window by an estimated 30 to 45 days annually in colder regions, significantly improving contractor asset utilization and revenue continuity. The standard also introduces tighter quality control metrics for curing kinetics, adhesion performance, and moisture sensitivity, elevating consistency across large-scale commercial projects. This development is particularly impactful for municipal and infrastructure maintenance programs seeking to optimize project timelines without compromising coating durability.

Market Opportunity: Polymer-Modified Asphalt (SBR/SBS) Sealcoats Redefining High-Traffic Performance Benchmarks

The decline of coal tar sealers has created a substantial opportunity for polymer-modified asphalt (PMA) technologies, particularly formulations incorporating Styrene-Butadiene-Rubber (SBR) and Styrene-Butadiene-Styrene (SBS). These advanced materials are increasingly specified for high-load environments such as logistics hubs, industrial yards, and airport taxiways. Performance data indicates that SBR-modified emulsions deliver a 71% increase in complex shear modulus at 48°C, significantly enhancing resistance to deformation under repetitive traffic loading. Meanwhile, SBS integration at approximately 4% concentration improves the rutting factor by over 80%, establishing PMA systems as the preferred solution for heavy-duty applications. Beyond high-temperature stability, these formulations also exhibit superior low-temperature ductility exceeding 100 cm at 10°C, compared to sub-10 cm values observed in legacy coal tar systems. This translates to an estimated 35% reduction in thermal cracking over a five-year lifecycle, directly lowering maintenance costs and extending pavement service intervals. As infrastructure owners prioritize lifecycle cost optimization and durability, PMA sealcoats are positioned as a premium, performance-driven alternative within the evolving seal coat market.

Market Opportunity: High-Solids Asphalt Emulsions (≥50%) Enabling Rapid Return-to-Service in High-Throughput Environments

High-solids asphalt emulsions (HSAE) are emerging as a critical innovation segment, particularly in sectors where operational downtime directly impacts revenue, such as last-mile logistics, retail parking facilities, and distribution centers. These formulations, characterized by solids content of 50% or greater, significantly outperform conventional emulsions in curing efficiency and film build performance. Under optimal conditions, HSAE systems achieve track-free status within 2 to 4 hours, representing a 50% to 75% reduction in drying time compared to traditional clay-stabilized sealers that require up to 48 hours. The higher solids content also minimizes volumetric shrinkage during curing, enabling single-coat applications to achieve equivalent dry-film thickness as dual-coat conventional systems. This reduces labor requirements by approximately 40% per project while maintaining coating integrity. Additionally, early-stage performance metrics indicate a 20% reduction in surface marking from vehicular turning within the first 12 hours of reopening, a critical parameter for maintaining visual quality in high-traffic zones. As demand intensifies for rapid-curing, high-durability pavement coatings, HSAE technologies are capturing premium segments of the seal coat industry.

Seal Coat Market Share and Segmentation Insights: Coal Tar Dominance and Distributor-Led Supply Chain Strength

By Product Type: Coal Tar-Based Sealants Lead with Superior Durability and Cost Efficiency

The coal tar-based sealants segment dominated the seal coat market with a 37.2% share in 2025, driven by its exceptional durability, chemical resistance, and cost-performance advantage. Coal tar emulsion sealants provide superior resistance to gasoline, oil spills, and deicing salts, making them the preferred choice for high-traffic parking lots, commercial driveways, and airport pavements. These properties ensure long-lasting protection against oxidation, weathering, and surface degradation, significantly extending pavement life. Despite increasing environmental regulations and restrictions in certain regions, coal tar sealants continue to maintain strong demand, particularly in North America, due to their low cost, deep black finish, and service life of 3–5 years. This balance of performance, affordability, and aesthetic appeal positions coal tar-based formulations as the leading product type in the global seal coat market, especially in large-scale commercial paving applications.

By Distribution Channel: Distributors and Wholesalers Dominate with Bulk Supply and Regional Availability

The distributors and wholesalers segment accounted for a leading 51.6% share of the seal coat market in 2025, reflecting the strong reliance on regional supply networks for bulk procurement and contractor support. Paving contractors typically purchase seal coat materials in large volumes such as totes, drums, and tanker trucks, requiring efficient logistics and localized availability. Distributors play a crucial role by providing not only sealants but also essential application equipment such as squeegees, spray systems, and crack-filling tools, along with technical guidance. Additionally, seal coating demand is highly seasonal, with peak activity during spring and summer months, making local inventory management and just-in-time delivery critical for timely project execution. By ensuring consistent product supply, fast delivery, and operational support, distributors and wholesalers remain the backbone of the seal coat market, particularly for large commercial and municipal pavement maintenance projects.

Competitive Landscape of the Seal Coat Market

SealMaster Leads Market with Franchise-Driven Scale and Advanced Polymer-Modified Sealers

SealMaster® (ThorWorks Industries) is the global leader in the seal coat market, leveraging the industry’s largest manufacturing and distribution network. With over 100 production and distribution facilities worldwide, the company ensures localized supply and rapid delivery. Its latest innovations include polymer-modified asphalt sealers that offer 25% faster curing compared to traditional formulations, improving efficiency in high-traffic municipal applications. The MasterSeal™ and PMM product lines remain industry benchmarks for durability and resistance to fuel and chemical exposure. SealMaster is also transitioning toward water-based, eco-friendly solutions, expanding into high-margin segments such as sport surfacing.

GemSeal Strengthens Contractor Ecosystem with Digital Tools and Consistent Product Quality

GemSeal® Pavement Products is a major player in the seal coat market, focusing on reliability and contractor support. The company has introduced a digital Contractor Resource Hub featuring AI-driven estimation tools that reduce material waste by 12%. Its Fed. Spec. and Black Diamond™ sealers are widely used for commercial and municipal applications, offering consistent performance. GemSeal’s quality-controlled manufacturing ensures uniform results across large-scale projects, while its expansion into the Southeastern U.S. strengthens its presence in residential and HOA markets.

Neyra Drives Innovation with Petroleum-Resin Sealers and Integrated Pavement Preservation Solutions

Neyra Industries, Inc. is a key innovator in the seal coat market, focusing on high-performance and environmentally conscious solutions. Its Neyra Force® sealer provides the durability of coal tar while eliminating associated environmental concerns. The company specializes in polymer-modified emulsion technologies, integrating crack fillers and sealants into comprehensive pavement preservation systems. Neyra is also expanding into EV infrastructure applications, offering high-visibility, slip-resistant coatings designed for charging stations and high-load environments.

Western Emulsions Leads Sustainability with Water-Based Bitumen Technologies

Western Emulsions (Western Colloid) is a leader in the seal coat market, particularly in sustainable solutions. The company has transitioned 95% of its portfolio to water-based emulsions, aligning with stringent environmental regulations. Its PASS® systems and chip seal technologies provide cost-effective pavement rehabilitation, extending asset life without full reconstruction. Western Emulsions is also expanding its dual-market presence, offering solutions for both pavement and roofing applications.

Vibrantz Enhances Market with Advanced Pigments and Functional Additives for Seal Coatings

Vibrantz Technologies plays a critical enabling role in the seal coat market, supplying advanced pigments and additives. Its infrared-reflective pigments can reduce pavement surface temperatures by up to 12°C, addressing urban heat island challenges. The company has also developed visible-light-responsive curing agents, enabling traffic reopening in under four hours—an important innovation for urban infrastructure projects. Its expertise in mineral-based colorants ensures long-lasting aesthetic performance, maintaining coating appearance significantly longer than standard formulations.

United States Driving Seal Coat Market Transition Toward Sustainable Asphalt and DIY Innovation

The United States continues to dominate the global seal coat market, driven by a regulatory shift away from traditional coal tar-based sealants toward eco-friendly asphalt-based and acrylic sealcoats. Following EPA-backed recommendations, multiple states have implemented bans on coal tar pitch sealants due to high PAH content, accelerating the adoption of low-toxicity, environmentally compliant pavement sealers.

Technological advancements are reshaping the industry, particularly with the rise of bio-renewable sealcoats derived from agricultural by-products, offering significantly reduced carbon footprints while maintaining durability. Infrastructure investments across major municipalities are boosting demand for polymer-modified master seal (PMM) systems and liquid road technologies, extending pavement life cycles. Product innovations such as cool pavement sealants with high Solar Reflectance Index (SRI) are gaining traction in heat-prone regions, while the expanding DIY segment is being driven by fast-drying, rain-resistant sealcoat formulations. Additionally, the integration of crack filling and sealcoating systems in highway maintenance is strengthening the role of seal coats in long-term pavement preservation strategies.

China Accelerating Industrial Seal Coat Demand with Smart Application Technologies

China is rapidly advancing in the seal coating market, supported by large-scale infrastructure investments and a shift toward high-performance, resin-modified sealants. The country’s extensive logistics and road network development, under initiatives such as Belt and Road domestic upgrades, is driving unprecedented demand for industrial-grade pavement sealers.

Technological innovation is a key growth driver, with the deployment of AI-enabled robotic sealcoating systems that optimize application rates based on real-time pavement conditions. Environmental regulations under the “Blue Sky 2026” policy are pushing manufacturers toward aqueous, low-VOC sealcoat formulations. Key applications include fuel-resistant sealants in airport hubs and the development of nanotechnology-enhanced asphalt rejuvenators that restore pavement performance by balancing chemical composition. Additionally, capacity expansion in polymer-modified asphalt production is supporting urban infrastructure growth and large-scale parking developments.

India Emerging as a Green Highway Seal Coat Market Leader

India is witnessing rapid expansion in the pavement seal coat market, driven by government-led infrastructure programs and urbanization. The Green Highway Initiatives (2026) are promoting the use of recycled materials and cold-mix sealcoats, aligning with sustainability goals while reducing lifecycle road maintenance costs.

Large-scale infrastructure investments under the Gati Shakti National Master Plan are significantly increasing demand for seal coating technologies across industrial corridors and logistics hubs. The shift toward micro-seal resurfacing is improving road quality by enhancing skid resistance and surface smoothness. Regulatory mandates from the Indian Roads Congress (IRC) are also driving the adoption of anti-carbonation sealants for bridges and railway crossings. Additionally, innovations such as monsoon-resistant sealants are addressing climate-specific challenges, while growing demand for residential and urban sealcoating applications is supporting aesthetic and dust-control requirements in smart city developments.

Germany Leading Digital Seal Coat Technologies and Circular Economy Integration

Germany is at the forefront of innovation in the seal coat industry, integrating Industry 4.0 technologies and sustainability-driven solutions. The adoption of IoT-enabled pavement sensors is transforming maintenance strategies by enabling real-time monitoring of surface conditions and predictive resealing cycles.

Regulatory compliance with EU sustainability frameworks is driving the development of biodegradable sealants and microplastic-free formulations, while technological advancements such as self-healing sealcoats are extending pavement lifespan through automated repair mechanisms. Germany is also leading in the use of bio-based epoxy and polyurethane sealants derived from recycled feedstocks, aligning with net-zero goals. Key applications include antimicrobial and easy-clean sealants for urban infrastructure, while industry consolidation is accelerating the adoption of ultra-high-solid coating technologies across the European market.

Saudi Arabia Driving High-Performance Seal Coat Demand for Extreme Desert Infrastructure

Saudi Arabia is emerging as a critical market for high-performance seal coats, driven by large-scale infrastructure developments under Vision 2030. Mega projects such as NEOM and “The Line” are generating demand for sand-abrasion-resistant and extreme-heat-resistant sealants, essential for maintaining pavement integrity in desert environments.

Technological innovations such as solar-reflective cool pavement sealants are reducing surface temperatures by up to 15°C, preventing deformation and extending road life. Regulatory updates under the Saudi Building Code (SBC 601) are mandating advanced moisture-barrier sealants for industrial infrastructure. The oil and gas sector remains a major application area, utilizing chemical-resistant sealants for containment systems, while the development of UV-stable MMA sealants is enabling rapid maintenance of airport runways. Increased localization of manufacturing is further strengthening supply chains and supporting long-term market growth.

Canada Strengthening Seal Coat Market with Cold-Climate Polymer Innovations

Canada’s seal coating market is defined by its need for extreme climate resilience and advanced polymer technologies. Innovations such as high-float asphalt emulsions are enabling sealants to remain flexible at temperatures as low as -40°C, preventing cracking in harsh winter conditions.

Regulatory measures, including tariffs on imported resins, are supporting domestic production of polymer-modified sealcoats, strengthening local supply chains. Key applications include crack sealing and pavement preservation programs under municipal paving strategies aimed at reducing maintenance costs. Product innovations such as hybrid acrylic-asphalt sealers are combining aesthetic appeal with enhanced durability. Additionally, airports are adopting friction-enhancing sealcoats to improve safety during icy conditions, while sustainability initiatives are promoting the use of reclaimed asphalt pavement (RAP) in sealcoat formulations, supporting circular economy practices.

Brazil Leveraging Agribusiness and Infrastructure Growth to Expand Seal Coat Applications

Brazil’s seal coat market is heavily influenced by its extensive agribusiness network and increasing focus on domestic manufacturing. Government policies such as anti-dumping duties on chemical imports are encouraging the use of locally sourced materials for sealcoat production.

Infrastructure investments under the Nova Indústria Brasil (NIB) plan are driving demand for energy-efficient pavement preservation technologies, particularly in logistics and transportation sectors. A key application area is the use of dust-suppressant and soil-stabilizing sealcoats for unpaved agricultural roads, improving transportation efficiency in rural regions. Technological advancements include the integration of ZAM-compatible coatings for metallic infrastructure, while innovations in water management sealants are supporting irrigation and reservoir systems. Expansion in local manufacturing capacity for crack sealants is further strengthening Brazil’s position as a growing market for advanced seal coating solutions.

Seal Coat Market Report Scope

Seal Coat Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.7 Billion

|

|

Market Size (2032)

|

$2.3 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Product Type (Asphalt-Based Sealants, Coal Tar-Based Sealants, Acrylic-Based Sealants, Bio-Based, Other Specialized Formulations), By Application (Pavements, Airports and Runways, Racetracks and Sports Facilities, Repair and Refurbishment), By End-User (Residential, Commercial, Municipal, Industrial), By Distribution Channel (Direct Sales, Distributors and Wholesalers, Retail, Online Sales Platforms), By Technology (Liquid Sealing Coatings, Dry Sealing Coatings)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SealMaster, Neyra Industries, Inc., GemSeal Pavement Products, Crafco, Inc., Vance Brothers, Inc., The Sherwin-Williams Company, Star-Seal, Inc., GuardTop, LLC, RaynGuard Protective Materials, Asphalt Coatings Engineering, Inc., Western Colloid, GoldStar Asphalt Products, Pavement Rejuvenation Technologies Group, Marathon Petroleum Corporation, Fahrner Asphalt Sealers, LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Seal Coat Market Segmentation

By Product Type

- Asphalt Emulsion

- Oil-Based

- Coal Tar-Based Sealants

- Acrylic-Based Sealants

- Bio-Based

- Other Specialized Formulations

By Application

- Driveways

- Parking Lots

- Roadways and Highways

- Walkways and Sidewalks

- Airports and Runways

- Racetracks and Sports Facilities

- Repair and Refurbishment

By End-User

- Residential

- Commercial

- Municipal

- Industrial

By Distribution Channel

- Direct Sales

- Distributors and Wholesalers

- Retail

- Online Sales Platforms

By Technology

- Liquid Sealing Coatings

- Dry Sealing Coatings

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Seal Coat Industry

- SealMaster

- Neyra Industries, Inc.

- GemSeal Pavement Products

- Crafco, Inc.

- Vance Brothers, Inc.

- The Sherwin-Williams Company

- Star-Seal, Inc.

- GuardTop, LLC

- RaynGuard Protective Materials

- Asphalt Coatings Engineering, Inc.

- Western Colloid

- GoldStar Asphalt Products

- Pavement Rejuvenation Technologies Group

- Marathon Petroleum Corporation

- Fahrner Asphalt Sealers, LLC

*- List not Exhaustive