China Industrial Water Treatment Chemicals Market Overview

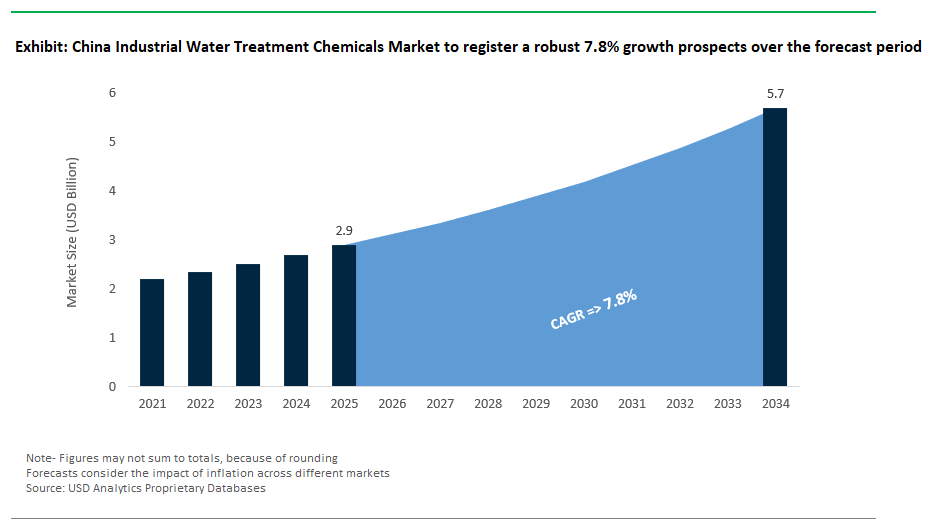

China Industrial Water Treatment Chemicals Market Size is estimated at $2.9 Billion in 2025 and is forecast to register an annual growth rate (CAGR) of 7.8% to reach $5.7 Billion by 2034.

China’s industrial water treatment chemicals market is highly diversified, reflecting its expansive industrial base and evolving environmental regulatory framework. The Ministry of Ecology and Environment (MEE) and various sector-specific discharge standards under the “GB” national standard system define effluent parameters that industrial facilities must meet. This has led to increased adoption of chemical treatments tailored to industry-specific water quality and reuse requirements.

In the power generation sector, particularly coal-fired plants, boiler feedwater treatment is governed by the DL/T 561 standard for thermal power water treatment, which specifies guidelines for oxygen scavenging and pH conditioning. Common oxygen scavengers used in Chinese power plants include carbohydrazide, recognized for its low toxicity and performance in high-pressure systems. Feedwater pH is often maintained using neutralizing amines such as ammonia or ethanolamine (ETA), in accordance with internal treatment practices to mitigate flow-accelerated corrosion (FAC), a known issue in heat recovery and condensate systems.

Cooling water treatment in thermal and industrial facilities is typically managed under DL/T 806, the Chinese standard for industrial circulating cooling water treatment. This includes the use of phosphonate-Zn formulations for corrosion control and dispersants to manage scaling in systems where high levels of dissolved silica (exceeding 200–250 ppm) are present. These formulations have been validated for use at elevated temperatures (>70°C) in power plant cooling circuits.

In the petrochemical and refining industry, demulsifier chemicals are essential for crude desalting. Chinese refiners commonly deploy nonionic polyol ester-based demulsifiers at dosage rates of 5–25 ppm to reduce basic sediment and water (BS&W) levels, consistent with the SH/T 0206 standard for crude oil quality. Achieving BS&W levels below 0.5% is typical to protect downstream heat exchangers and catalytic units.

Steel and metallurgical operations, particularly in provinces such as Hebei and Liaoning, are regulated under the GB 13456-2012 standard for effluent discharge from the iron and steel industry. Wastewater generated from cold-rolling and pickling processes is treated using acid demulsifiers followed by ultrafiltration membranes to reduce residual oil content below 10 mg/L necessary for compliance with discharge limits on petroleum hydrocarbons.

In electronics and semiconductor manufacturing, ultrapure water (UPW) generation is aligned with the SEMI F63 and China Electronic Grade Water Standards (SJ/T 31469). TOC levels are typically controlled below 0.5 ppb using 185 nm UV oxidation and membrane degasification. Selective ion exchange resins are employed for boron removal, a key requirement in semiconductor-grade water systems. Additionally, fluoride-laden wastewater from etching processes is treated using calcium chloride (CaCl₂) precipitation to form calcium fluoride (CaF₂), reducing fluoride concentrations to below 15 mg/L, in line with semiconductor industry wastewater treatment practices.

The textile and dyeing sectors in Zhejiang and Jiangsu provinces face significant wastewater challenges due to high color and COD content. Treatment practices follow the GB 4287-2012 discharge standard for textile finishing. Chemical oxidation processes such as Fenton's reagent and ozone systems are used for color removal, while electrodialysis (ED) and nanofiltration are increasingly deployed to concentrate and recover NaCl brine from dye bath effluents. Membrane scaling in these systems is prevented using antiscalants dosed typically in the 3–8 ppm range.

China’s broader environmental goals such as the “Dual Carbon” policy drive green chemistry initiatives across industrial water treatment. Under the Circular Economy Promotion Law and the NDRC’s Industrial Solid Waste Comprehensive Utilization Plan, manufacturers are increasingly incorporating coal fly ash-based materials into the production of inorganic flocculants, contributing to resource recycling targets. Simultaneously, biodegradable alternatives to phosphonates, such as polyaspartic acid (PASP) and polyepoxysuccinic acid (PESA), are promoted for corrosion and scale control applications to support long-term carbon reduction and eco-toxicity goals.

Market Trend: "Dual Carbon" Policy and Water Reuse Mandates Influence Chemical Demand

China's industrial water treatment chemicals market is undergoing a strategic shift as national environmental policies prioritize both carbon emissions reduction and water conservation. Central to this transformation is the “Dual Carbon” initiative, which aims to peak carbon emissions by 2030 and achieve carbon neutrality by 2060. The 14th Five-Year Plan (2021–2025) includes strict mandates for industrial water reuse and pollutant discharge reduction, particularly targeting water-intensive sectors such as thermal power generation, iron & steel production, and electronics manufacturing.

According to China's Ministry of Ecology and Environment (MEE), new discharge standards under GB 37823-2024 will take effect in June 2025, setting a maximum phosphorus concentration of 0.5 mg/L in effluent from petrochemical facilities. This regulation has led to increased demand for phosphorus-free or low-phosphorus antiscalants and dispersants, particularly polyaspartic acid and polyepoxysuccinic acid (PESA), which offer enhanced biodegradability and lower environmental impact compared to traditional phosphate-based agents.

Industrial parks in provinces like Jiangsu and Zhejiang are implementing advanced water recycling infrastructure to meet high reuse targets. The Jiangsu Provincial Department of Ecology and Environment has mandated water reuse rates above 85% for textile industrial clusters, resulting in growing demand for high-performance antiscalants and sludge-reducing additives. These chemicals are used to improve the performance of reverse osmosis systems and thermal evaporators essential to Zero Liquid Discharge (ZLD) compliance.

Baowu Steel Group, one of China’s largest steelmakers, has publicly partnered with Bluetech Clean Energy to optimize chemical dosing using AI-driven systems. Their deployment of Bluetech’s WiseWater platform reportedly reduced chemical consumption and minimized sludge generation, contributing to operational efficiency and regulatory compliance in closed-loop water systems.

Market Opportunity: Semiconductor Industry Drives Demand for Ultra-Pure Water (UPW) Treatment Chemicals

China’s semiconductor manufacturing expansion spurred by state policy support, strategic investment, and supply chain localization has created a growing market for ultra-pure water (UPW) treatment chemicals. The Ministry of Industry and Information Technology (MIIT) has included semiconductor fabrication in its strategic high-tech priorities under the “Made in China 2025” initiative, resulting in over ¥1 trillion in government-backed investments.

Leading domestic foundries such as Semiconductor Manufacturing International Corporation (SMIC), Yangtze Memory Technologies (YMTC), and ChangXin Memory Technologies (CXMT) are rapidly building fabs with UPW requirements ranging from 10,000 to 50,000 m³/day per site. According to SEMI (Semiconductor Equipment and Materials International), UPW used in advanced node manufacturing (≤5nm) must meet ultrapure standards such as <0.05 μg/L silica, <0.1 μg/L total organic carbon (TOC), and extremely low levels of metal ions.

To meet these specifications, suppliers are phasing out conventional reagents that risk trace metal contamination. Companies like Entegris and Pall have introduced ultra-high-purity filtration systems and chemical blends certified under SEMI C79 and SEMI F57 standards. Domestic suppliers including OriginWater and Beijing Tri-High are also developing metal-free formulations and PFAS-free coagulants to align with both environmental and technical purity requirements.

The market for ozone-based oxidants is also expanding due to their role in lithography and wafer cleaning. On-site ozone generation systems often based on Proton Exchange Membrane (PEM) technology require compatible high-purity chemicals, which must exceed 99.999% purity to prevent damage to silicon wafers.

With more than 150 fabs announced or under construction across China, industry analysts from China Semiconductor Industry Association (CSIA) estimate cumulative UPW-related chemical demand could reach ¥25 billion (~US$3.4 billion) by 2030. This includes not only treatment chemicals but also prequalified dosing agents, chelating resins, and filtration additives all of which are subject to strict SEMI material compatibility standards. The combination of regulatory backing and localized production incentives offers significant opportunities for global and Chinese water chemical suppliers alike.

Competitive Landscape: China Industrial Water Treatment Chemicals Market

The competitive landscape of China’s industrial water treatment chemicals market is complex and features a mix of global players, local firms, and state-owned enterprises. Each group of competitors has its own role in the value chain, influenced by cost, innovation, regulation, and location. Multinational corporations (MNCs) lead the premium segment with advanced and customized solutions. In contrast, domestic companies are strong in cost-sensitive and regionally focused applications. State-owned enterprises (SOEs) also affect purchasing trends through centralized buying connected to national industrial strategies.

MNCs such as Ecolab (Nalco), Solenis, BASF, Kemira, and Suez lead high-value sectors like power generation, petrochemicals, and advanced manufacturing. These companies use proprietary chemistries, including corrosion inhibitors, membrane treatments, biocides, and antiscalants, while securing long-term contracts through their global expertise and commitment to international environmental standards. Their strength comes from ongoing investments in R&D, especially in sustainable and digital water treatment technologies. This positions them at the forefront of demand driven by innovation.

On the other hand, domestic players like Beijing OriginWater, Jiangsu Jianghai, Shandong Taihe, and Zibo Jinxing focus on the mid- and low-end market, providing competitively priced products and flexible service networks. These companies are well-established in municipal and industrial water treatment, especially where local supply chains and cost efficiency matter more than cutting-edge formulations. They benefit from supportive government policies, lower input costs, and quicker project turnaround times, making them preferred suppliers in many tier-2 and tier-3 cities.

State-owned enterprises like Sinopec, CNPC, and Huaneng Group play a key role as both customers and providers. They often buy from domestic suppliers in line with government policies favoring local content, particularly in projects heavy on infrastructure like thermal power plants, oil refining, and steel production. Although they are not typically seen as innovators, SOEs influence market direction by enforcing local procurement clauses and backing national priorities such as energy security and pollution control.

Competition among these players grows stronger due to their strategic focuses. MNCs generally maintain premium pricing and concentrate on R&D for green chemistry and digital solutions, while domestic firms prioritize volume sales, cost efficiency, and rapid growth in specific regions. SOEs follow a procurement-driven approach that aligns with policy and long-term infrastructure goals. Distribution strategies also differ, with global firms building direct industrial partnerships, local firms leveraging extensive regional dealer networks, and SOEs depending on internal sourcing or affiliated procurement divisions.

The rise of startups and hybrid business models is also changing the market. Companies like Bluetech and Aowei Technology introduce digital monitoring systems and bio-based treatment options, appealing to sustainability-focused customers. Additionally, joint ventures between foreign and local firms are becoming more common, helping MNCs navigate regulatory challenges while improving localization efforts.

Looking ahead, the focus is expected to shift toward green and digital solutions. China's "Double Carbon" goal, which aims for carbon peaking before 2030 and neutrality before 2060, is encouraging all players to focus on low-toxicity, biodegradable, and energy-efficient chemistries. At the same time, the integration of Internet of Things (IoT) technologies into treatment plants is creating new ways to stand out, particularly among industrial clients who want real-time water quality monitoring and remote control features. Moreover, the ongoing tension between localization and globalization will continue to shape strategies, as domestic firms seek to acquire foreign technologies while MNCs localize production to enhance their market presence.

China Industrial Water Treatment Chemicals Market – Segmentation Insights (2025–2034)

China Industrial Water Treatment Chemicals Market: Cooling Water Treatment Dominates, Water Recycling Leads Growth

In the China industrial water treatment chemicals market, cooling water treatment is projected to hold the largest market share at 33.9% in 2025, reflecting the extensive deployment of cooling towers across China’s power generation and heavy manufacturing sectors. With industries such as steel, chemicals, and cement relying heavily on recirculating cooling systems, there is a consistent demand for chemicals that prevent scaling, corrosion, and microbial fouling. China’s industrial base continues to expand in energy-intensive zones, further reinforcing the importance of cooling water treatment in ensuring system efficiency and operational longevity. On the growth frontier, the water reuse and recycling segment is anticipated to witness the highest CAGR at 9.2% from 2025 to 2034, driven by China’s aggressive water conservation policies, including the national "Sponge City" program and industrial circular economy mandates. As the country combats water scarcity and pollution challenges, industries are increasingly investing in closed-loop water systems that rely on high-performance chemicals for reuse optimization. This shift is also being fueled by the enforcement of Zero Liquid Discharge (ZLD) regulations and a growing trend toward sustainable, cost-efficient water management practices in key industrial corridors such as the Yangtze River Delta and Greater Bay Area.

China Industrial Water Treatment Chemicals Market: Power Sector Dominates, Electronics Drive Fastest Growth

In 2025, the power generation sector is expected to lead the China industrial water treatment chemicals market with a 29.6% market share, owing to the dominance of thermal power plants and the critical need for chemical treatment of boiler feedwater and cooling systems. Power plants across China, especially coal-fired facilities, consume large volumes of water and depend on corrosion inhibitors, antiscalants, and oxygen scavengers to optimize equipment performance and reduce unplanned downtimes. This segment remains a stronghold due to aging infrastructure and high water-related maintenance requirements. However, the most significant growth is forecasted in the electronics and semiconductors industry, which is set to expand at a CAGR of 9.6% through 2034. The rapid growth of this sector driven by China's ambition to become self-sufficient in chip manufacturing demands ultrapure water (UPW) systems supported by specialty water treatment chemicals. As fabrication plants (fabs) ramp up operations in regions such as Shanghai, Chengdu, and Wuhan, the need for high-grade membrane cleaners, chelating agents, and low-conductivity treatment solutions is accelerating. This trend positions the electronics segment as a key growth engine in China’s evolving water treatment chemicals landscape.

.png)

China Industrial Water Treatment Chemicals Report Scope

China Industrial Water Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2034)

|

$5.7 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Type of Chemical (Coagulants and Flocculants, Corrosion and Scale Inhibitors, Biocides and Disinfectants, pH Adjusters and Neutralizers, Oxygen Scavengers, Defoamers and Antifoaming Agents, Membrane Cleaning Chemicals, H2S Scavengers, Others), By Application (Cooling Water Treatment, Boiler Water Treatment, Process Water Treatment, Industrial Wastewater Treatment, Water Reuse and Recycling, Industrial Desalination, Sludge Treatment), By End-User Industry (Power Generation, Chemical and Petrochemical, Mining and Metallurgy, Pulp and Paper, Food and Beverage, Electronics and Semiconductors, Textile and Dyeing, Pharmaceutical, Automotive, Oil and Gas, Other Manufacturing Industries), By Form of Chemical (Liquid, Powder/Solid), By Distribution Channel (Direct Sales, Distributors/Channel Partners

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ecolab Inc. (U.S.), Solenis LLC (U.S.), Kemira Oyj (Finland), BASF SE (Germany), SNF Floerger (France), Kurita Water Industries Ltd. (Japan), Veolia Water Technologies (France), The Dow Chemical Company (U.S.), Shandong ThFine Chemical Co., Ltd., Shandong XinTai Water Treatment Co., Ltd., HIXEN Chemicals Co., Ltd., Yixing Bluwat Chemicals Co., Ltd., Zibo Anquan Chemical Co., Ltd., Wujin Fine Chemical Factory,

|

China Industrial Water Treatment Chemicals Market Segmentation

By Type of Chemical

- Coagulants and Flocculants

- Corrosion and Scale Inhibitors

- Biocides and Disinfectants

- pH Adjusters and Neutralizers

- Oxygen Scavengers

- Defoamers and Antifoaming Agents

- Membrane Cleaning Chemicals

- H2S Scavengers

- Others

By Application

- Cooling Water Treatment

- Boiler Water Treatment

- Process Water Treatment

- Industrial Wastewater Treatment

- Water Reuse and Recycling

- Industrial Desalination

- Sludge Treatment

By End-User Industry

- Power Generation

- Chemical and Petrochemical

- Mining and Metallurgy

- Pulp and Paper

- Food and Beverage

- Electronics and Semiconductors

- Textile and Dyeing

- Pharmaceutical

- Automotive

- Oil and Gas

- Other Manufacturing Industries

By Form of Chemical

By Distribution Channel

- Direct Sales

- Distributors/Channel Partners

Top Companies in China Industrial Water Treatment Chemicals Market

- Ecolab Inc. (U.S.)

- Solenis LLC (U.S.)

- Kemira Oyj (Finland)

- BASF SE (Germany)

- SNF Floerger (France)

- Kurita Water Industries Ltd. (Japan)

- Veolia Water Technologies (France)

- The Dow Chemical Company (U.S.)

- Shandong ThFine Chemical Co., Ltd.

- Shandong XinTai Water Treatment Co., Ltd.

- HIXEN Chemicals Co., Ltd.

- Yixing Bluwat Chemicals Co., Ltd.

- ZibAnquan Chemical Co., Ltd.

- Wujin Fine Chemical Factory

* List Not Exhaustive

Research Coverage

This report by USDAnalytics investigates the China Industrial Water Treatment Chemicals Market, delivering in-depth analysis reviews, technological breakthroughs, and competitive assessments across key industrial sectors. It highlights the strategic impact of policies like “Dual Carbon” and the national push for water reuse, alongside emerging opportunities in ultra-pure water treatment for semiconductor manufacturing. By exploring segmentation dynamics, ESG-driven procurement trends, and the rise of advanced formulations, this report is an essential resource for stakeholders aiming to navigate China’s evolving industrial water chemistry landscape.

Scope Includes:

- By Type of Chemical: Coagulants & Flocculants, Corrosion & Scale Inhibitors, Biocides & Disinfectants, pH Adjusters & Neutralizers, Oxygen Scavengers, Defoamers & Antifoaming Agents, Membrane Cleaning Chemicals, H₂S Scavengers, Others

- By Application: Cooling Water Treatment, Boiler Water Treatment, Process Water Treatment, Industrial Wastewater Treatment, Water Reuse & Recycling, Industrial Desalination, Sludge Treatment

- By End-User Industry: Power Generation, Chemical & Petrochemical, Mining & Metallurgy, Electronics & Semiconductors, Textile & Dyeing, Food & Beverage, Pharmaceutical, Automotive, Oil & Gas, Other Manufacturing Industries

- By Form: Liquid, Powder/Solid

- Study Period: Historic: 2021–2024; Forecast: 2025–2034

- Companies: Ecolab Inc., Solenis LLC, Kemira Oyj, BASF SE, SNF Floerger, Kurita Water Industries Ltd., Veolia Water Technologies, The Dow Chemical Company, Shandong ThFine Chemical Co. Ltd., Shandong XinTai Water Treatment Co. Ltd., HIXEN Chemicals Co. Ltd., Yixing Bluwat Chemicals Co. Ltd., ZibAnquan Chemical Co. Ltd., Wujin Fine Chemical Factory.

Methodology

The methodology integrates top-down and bottom-up modeling, leveraging primary research with Chinese industrial operators and water chemical suppliers, combined with secondary data sources including MIIT, SEMI, GB standards, and verified trade publications. Forecasting uses econometric modeling with scenario-based adjustments for policy mandates, industrial expansion, and ESG-linked procurement patterns. Data triangulation ensures reliability, while competitive intelligence frameworks benchmark sustainability innovation, pricing structures, and localization strategies.

Deliverables

- Complete Market Research Report (PDF, Excel): data tables, market charts, and visual insights.

- Segment-wise Revenue Projections (2025–2034)

- Competitive Benchmarking & SWOT Analysis

- Recent Developments & News Tracker

- Executive summary and key takeaway slides for boardroom presentations

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements